Auto parts and accessories retailer Advance Auto Parts (NYSE:AAP) reported results in line with analysts' expectations in Q4 FY2023, with revenue flat year on year at $2.46 billion. On the other hand, the company's full-year revenue guidance of $11.35 billion at the midpoint came in slightly below analysts' estimates. It made a GAAP loss of $0.59 per share, down from its profit of $2.88 per share in the same quarter last year.

Advance Auto Parts (AAP) Q4 FY2023 Highlights:

- Revenue: $2.46 billion vs analyst estimates of $2.46 billion (small beat)

- EPS: -$0.59 vs analyst estimates of $0.19 (-$0.78 miss)

- Management's revenue guidance for the upcoming financial year 2024 is $11.35 billion at the midpoint, missing analyst estimates by 0.9% and implying 0.6% growth (vs 1.2% in FY2023)

- Management's EPS guidance for the upcoming financial year 2024 is $4.00 per share at the midpoint, well above analyst estimates of $3.49

- Free Cash Flow of $200.5 million, up 34.8% from the same quarter last year

- Gross Margin (GAAP): 38.6%, down from 44.1% in the same quarter last year

- Same-Store Sales were down 1.4% year on year (slight miss vs expectations of down 1.1% year on year)

- Store Locations: 5,107 at quarter end, increasing by 21 over the last 12 months

- Market Capitalization: $3.83 billion

Founded in Virginia in 1932, Advance Auto Parts (NYSE:AAP) is an auto parts and accessories retailer that sells everything from carburetors to motor oil to car floor mats.

The company serves both do-it-yourself (DIY) customers as well as professional mechanics and auto repair businesses. The company understands that DIY customers may have varying levels of expertise in auto repair, so stores feature automotive expert sales associates who can help you find which brake pads will fit your 2019 Ford Focus, for example.

For the professional mechanic, Advance Auto Parts has a particularly strong selection of commercial products such as heavy-duty truck parts. The company also offers a commercial program with dedicated account managers, customized billing options, and professional-grade tools for rent. A fleet of commercial delivery vehicles thousands strong make sure professional customers get what they need in a timely manner.

Advance Auto Parts stores are typically located in smaller towns and more rural areas compared to auto parts peers, with a strong footprint in the Eastern US. The typical store is roughly 7,500 square feet, with many featuring areas and help desks specifically for professional customers. In addition to its brick-and-mortar stores, Advance Auto Parts also has an e-commerce presence that allows customers to buy products to be shipped to their homes or to buy and pick up at the nearest store to save time.

Auto Parts Retailer

Cars are complex machines that need maintenance and occasional repairs, and auto parts retailers cater to the professional mechanic as well as the do-it-yourself (DIY) fixer. Work on cars may entail replacing fluids, parts, or accessories, and these stores have the parts and accessories or these jobs. While e-commerce competition presents a risk, these stores have a leg up due to the combination of broad and deep selection as well as expertise provided by sales associates. Another change on the horizon could be the increasing penetration of electric vehicles.

Competitors offering auto parts and accessories include AutoZone (NYSE:AZO), O’Reilly Automotive (NASDAQ:ORLY), Genuine Parts (NYSE:GPC), and private company Pep Boys.Sales Growth

Advance Auto Parts is larger than most consumer retail companies and benefits from economies of scale, giving it an edge over its competitors.

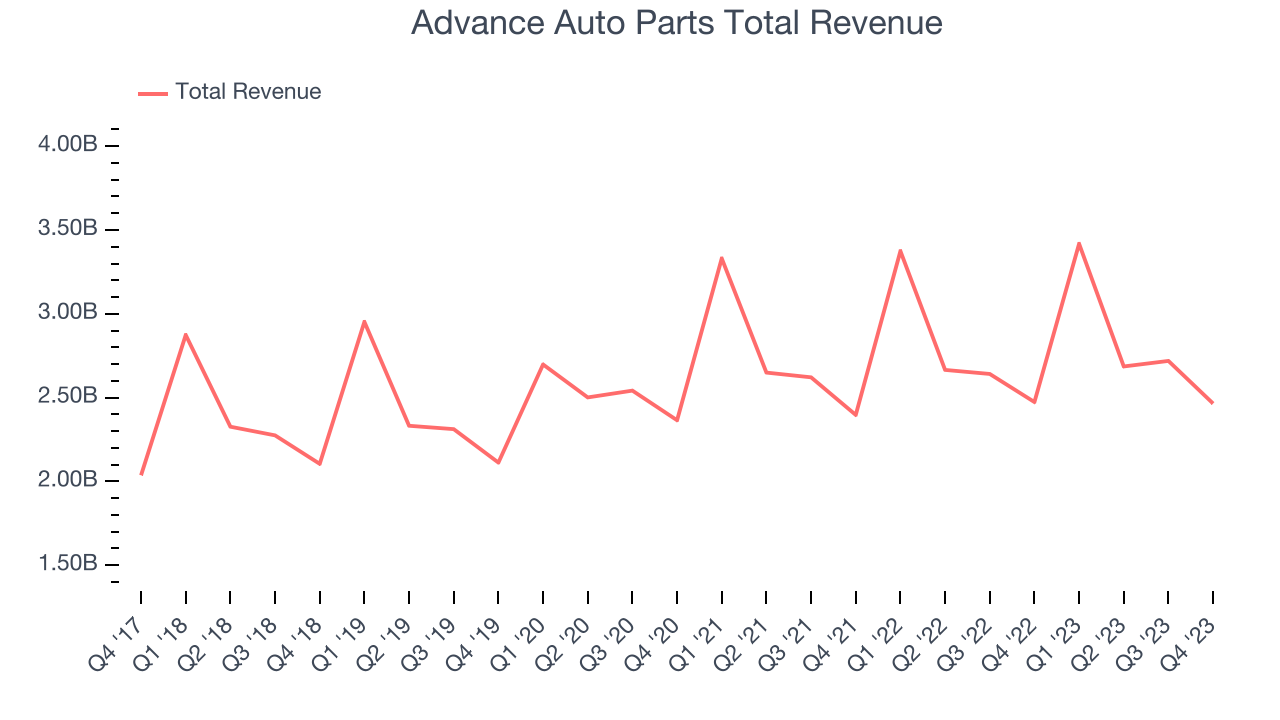

As you can see below, the company's annualized revenue growth rate of 3.8% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was weak as its store footprint remained relatively unchanged, implying that growth was driven by more sales at existing, established stores.

This quarter, Advance Auto Parts reported a rather uninspiring 0.4% year-on-year revenue decline to $2.46 billion in revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 1.6% over the next 12 months, an acceleration from this quarter.

Number of Stores

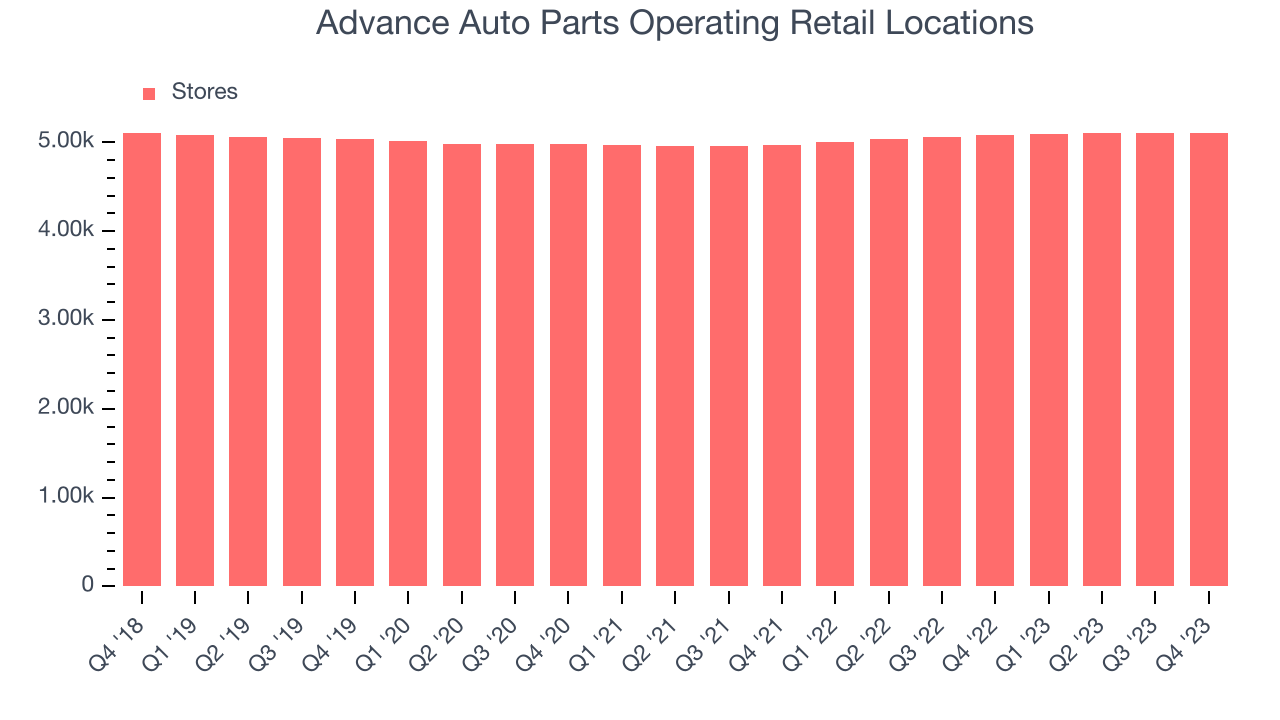

A retailer's store count often determines on how much revenue it can generate.

When a retailer like Advance Auto Parts keeps its store footprint steady, it usually means that demand is stable and it's focused on improving operational efficiency to increase profitability. As of the most recently reported quarter, Advance Auto Parts operated 5,107 total retail locations, in line with its store count a year ago.

Over the last two years, the company has only opened a few new stores, averaging 1.4% annual growth in new locations. This sluggish pace lags the broader sector. A flat store base means that revenue growth must come from increased e-commerce sales or higher foot traffic and sales per customer at existing stores.

Same-Store Sales

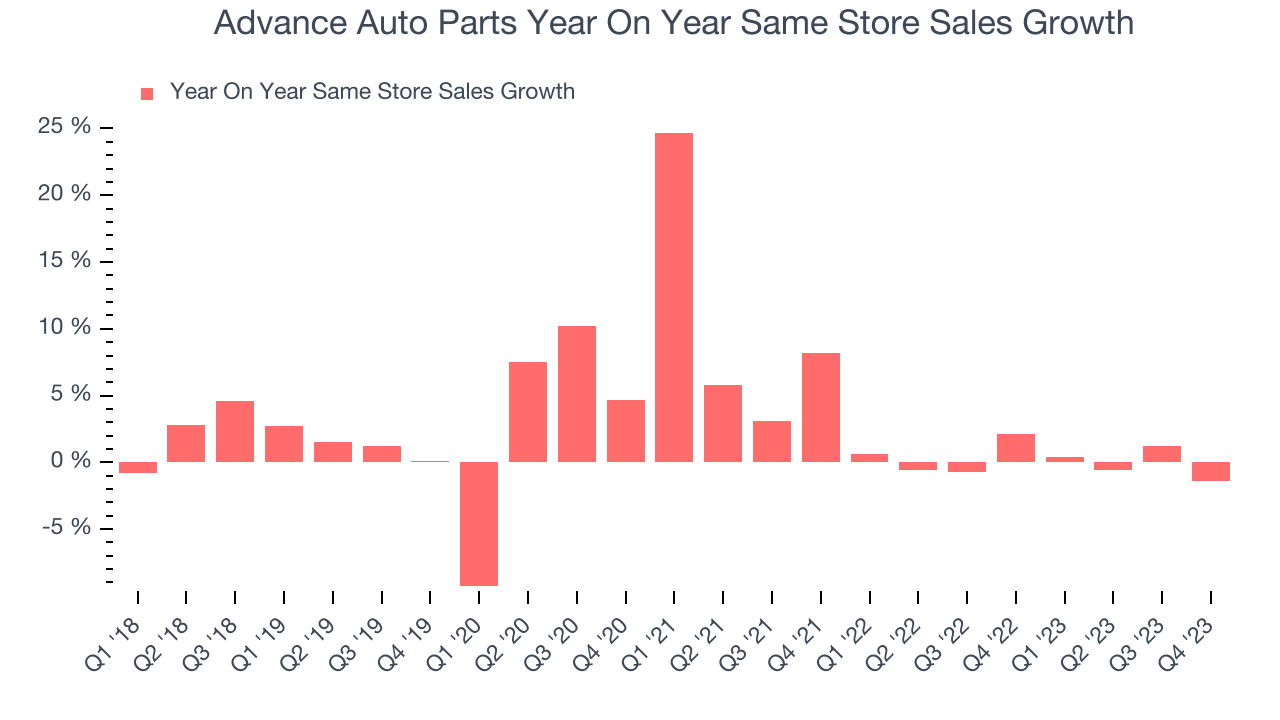

Advance Auto Parts's demand within its existing stores has barely increased over the last eight quarters. On average, the company's same-store sales growth has been flat.

In the latest quarter, Advance Auto Parts's same-store sales fell 1.4% year on year. This decline was a reversal from the 2.1% year-on-year increase it posted 12 months ago. We'll be keeping a close eye on the company to see if this turns into a longer-term trend.

Gross Margin & Pricing Power

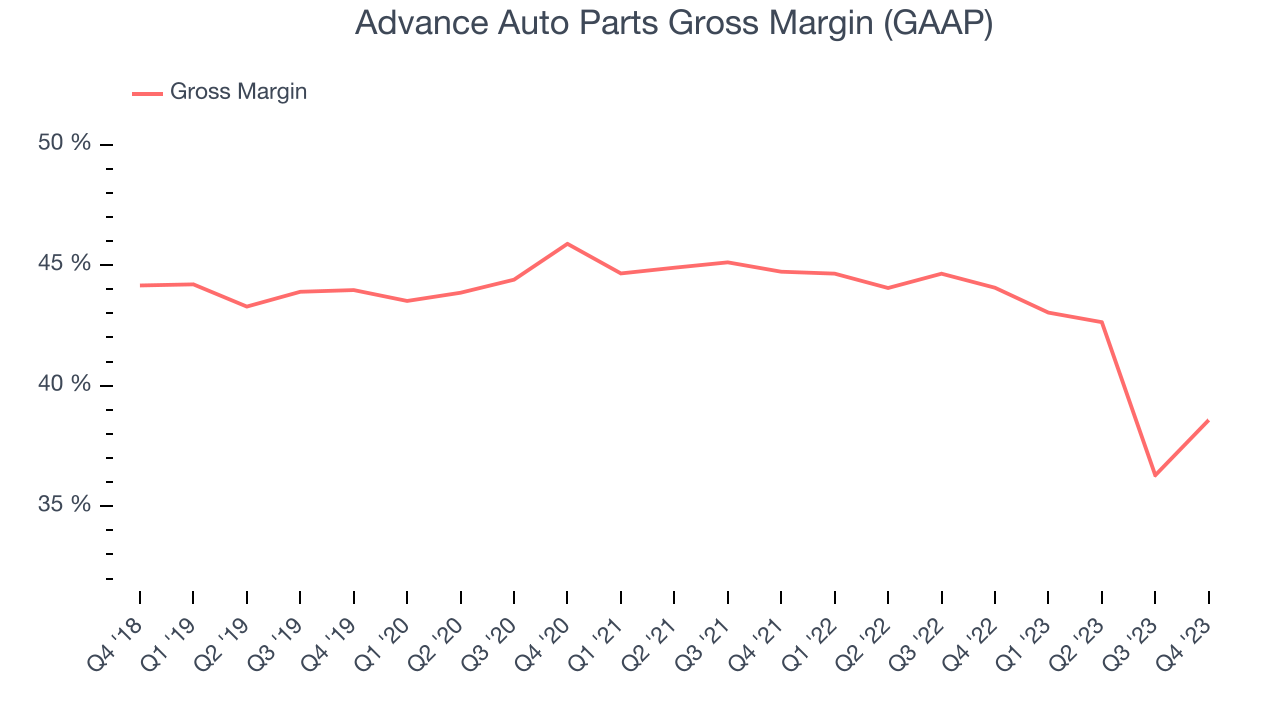

Advance Auto Parts has good unit economics for a retailer, giving it the opportunity to invest in areas such as marketing and talent to stay competitive. As you can see below, it's averaged a healthy 42.3% gross margin over the last two years. This means the company makes $0.42 for every $1 in revenue before accounting for its operating expenses.

Advance Auto Parts produced a 38.6% gross profit margin in Q4, marking a 5.5 percentage point decrease from 44.1% in the same quarter last year. Although the company could've performed better, we care more about its long-term trends rather than just one quarter. Additionally, a retailer's gross margin can often change due to factors outside its control, such as product discounting and dynamic input costs (think distribution and freight expenses to move goods). We'll keep a close eye on this.

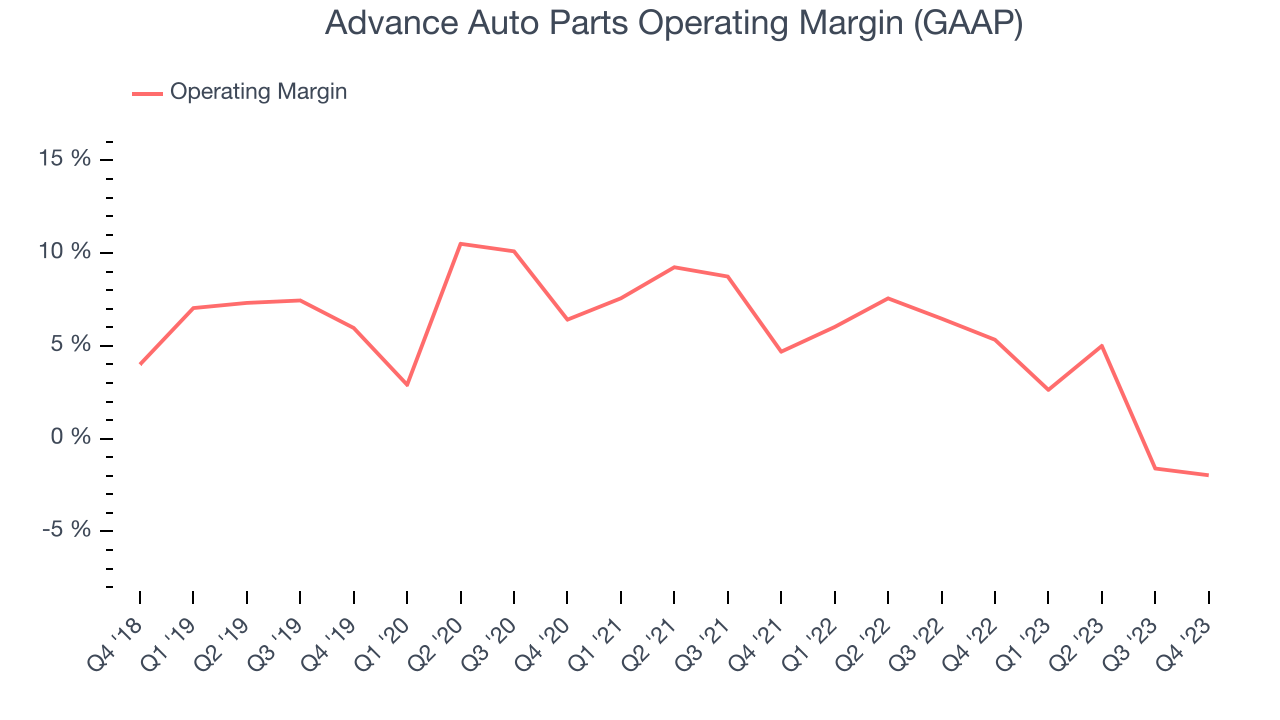

Operating Margin

Operating margin is an important measure of profitability for retailers as it accounts for all expenses keeping the lights on, including wages, rent, advertising, and other administrative costs.

This quarter, Advance Auto Parts generated an operating profit margin of negative 2%, down 7.3 percentage points year on year. We can infer Advance Auto Parts was less efficient with its expenses or had lower leverage on its fixed costs because its operating margin decreased more than its gross margin.

Zooming out, Advance Auto Parts was profitable over the last two years but held back by its large expense base. Its average operating margin of 3.7% has been paltry for a consumer retail business. On top of that, Advance Auto Parts's margin has declined, on average, by 5.2 percentage points year on year. This shows the company is heading in the wrong direction, and investors were likely hoping for better results.

Zooming out, Advance Auto Parts was profitable over the last two years but held back by its large expense base. Its average operating margin of 3.7% has been paltry for a consumer retail business. On top of that, Advance Auto Parts's margin has declined, on average, by 5.2 percentage points year on year. This shows the company is heading in the wrong direction, and investors were likely hoping for better results.EPS

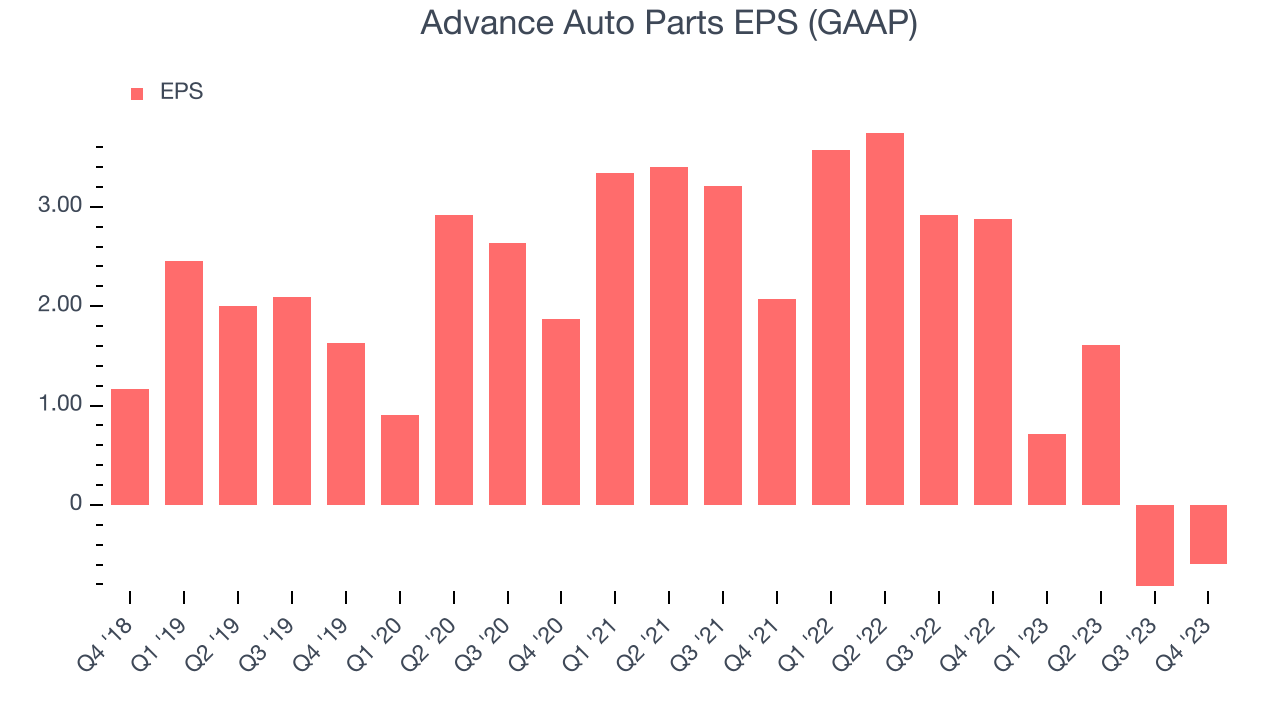

Earnings growth is a critical metric to track, but for long-term shareholders, earnings per share (EPS) is more telling because it accounts for dilution and share repurchases.

In Q4, Advance Auto Parts reported EPS at negative $0.59, down from $2.88 in the same quarter a year ago. This print unfortunately missed Wall Street's estimates, but we care more about long-term EPS growth rather than short-term movements.

Between FY2019 and FY2023, Advance Auto Parts's adjusted diluted EPS dropped 86.5%, translating into 39.4% annualized declines. In a mature sector such as consumer retail, we tend to steer our readers away from companies with falling EPS. If there's no earnings growth, it's difficult to build confidence in a business's underlying fundamentals, leaving a low margin of safety around the company's valuation (making the stock susceptible to large downward swings).

On the bright side, Wall Street expects the company's earnings to grow over the next 12 months, with analysts projecting an average 259% year-on-year increase in EPS.

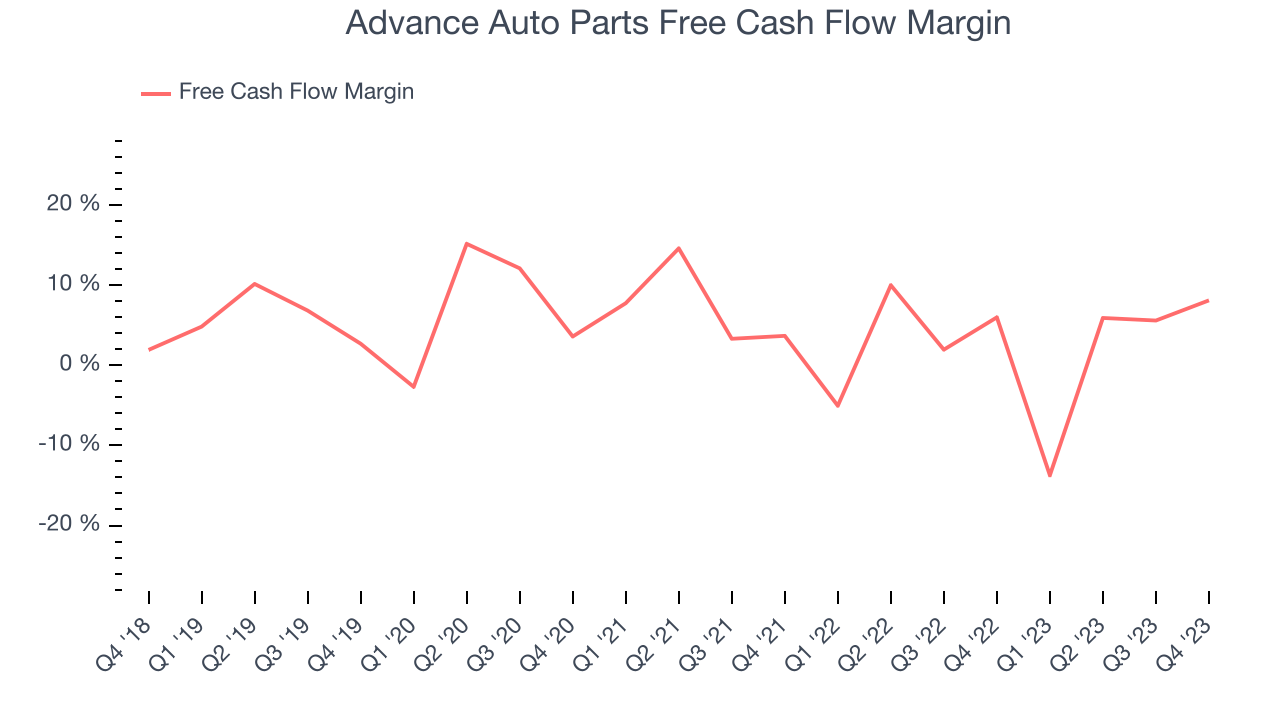

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Advance Auto Parts's free cash flow came in at $200.5 million in Q4, up 34.8% year on year. This result represents a 8.1% margin.

Over the last eight quarters, Advance Auto Parts has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 1.5%, subpar for a consumer retail business. Furthermore, its margin has averaged year-on-year declines of 2.3 percentage points.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Advance Auto Parts's five-year average ROIC was 7.7%, somewhat low compared to the best retail companies that consistently pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Advance Auto Parts's ROIC over the last two years averaged 3.8 percentage point decreases each year. In conjunction with its already low returns, these declines suggest the company's profitable business opportunities are few and far between.

Key Takeaways from Advance Auto Parts's Q4 Results

We were impressed by Advance Auto Parts's optimistic full-year earnings forecast, which blew past analysts' expectations. Additionally, the company said it "recently launched an initiative to eliminate costs related to our indirect spend by an additional $50 million on an annualized basis". Finally, Advance Auto Parts is undergoing an "ongoing operational and strategic review of the business, including the separate sales processes for Worldpac and our Canadian business." The stock is up 9.3% after reporting and currently trades at $70.65 per share.

Is Now The Time?

Advance Auto Parts may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Advance Auto Parts, we'll be cheering from the sidelines. Its revenue growth has been a little slower over the last four years, and analysts expect growth to deteriorate from here. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its declining EPS over the last four years makes it hard to trust. On top of that, its poor same-store sales performance has been a headwind.

Advance Auto Parts's price-to-earnings ratio based on the next 12 months is 18.4x. While we've no doubt one can find things to like about Advance Auto Parts, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $56.69 per share right before these results (compared to the current share price of $70.65), implying they didn't see much short-term potential in Advance Auto Parts.

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.