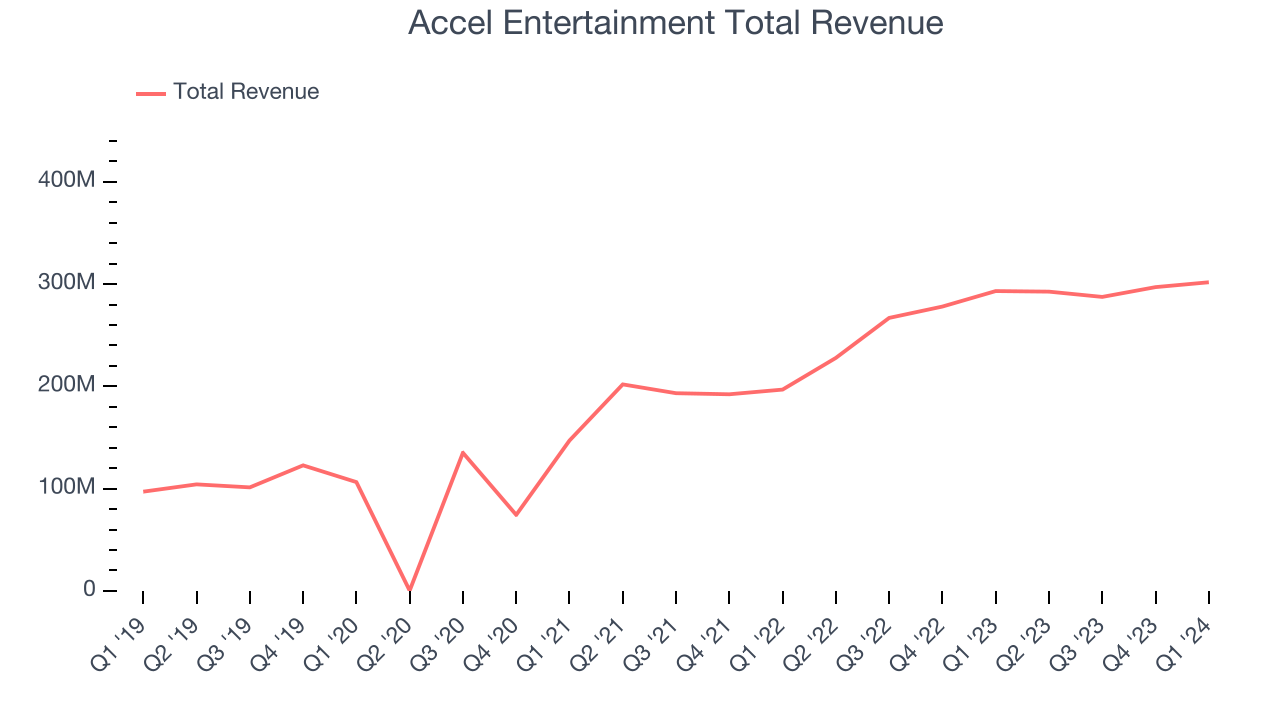

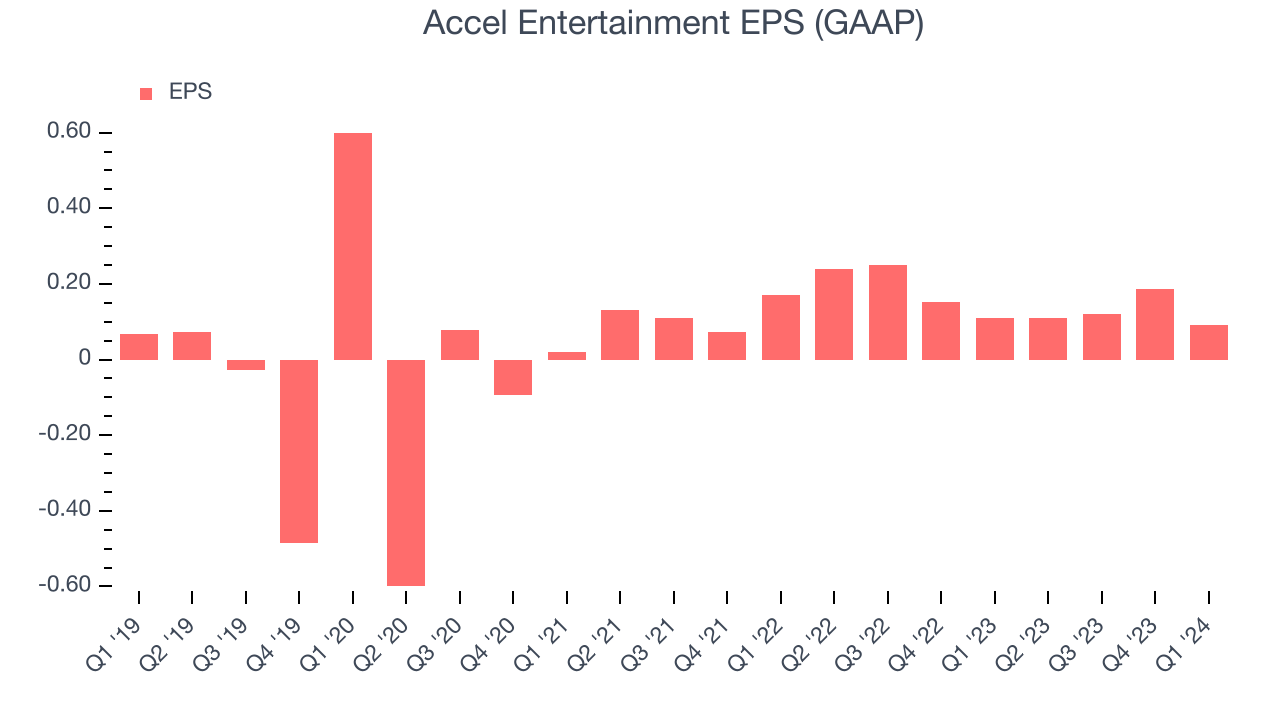

Slot machine and terminal operator Accel Entertainment (NYSE:ACEL) reported Q1 CY2024 results beating Wall Street analysts' expectations, with revenue up 2.9% year on year to $301.8 million. It made a GAAP profit of $0.09 per share, down from its profit of $0.11 per share in the same quarter last year.

Accel Entertainment (ACEL) Q1 CY2024 Highlights:

- Revenue: $301.8 million vs analyst estimates of $295.8 million (2.1% beat)

- EPS: $0.09 vs analyst expectations of $0.14 (35.8% miss)

- Gross Margin (GAAP): 30.7%, up from 30.1% in the same quarter last year

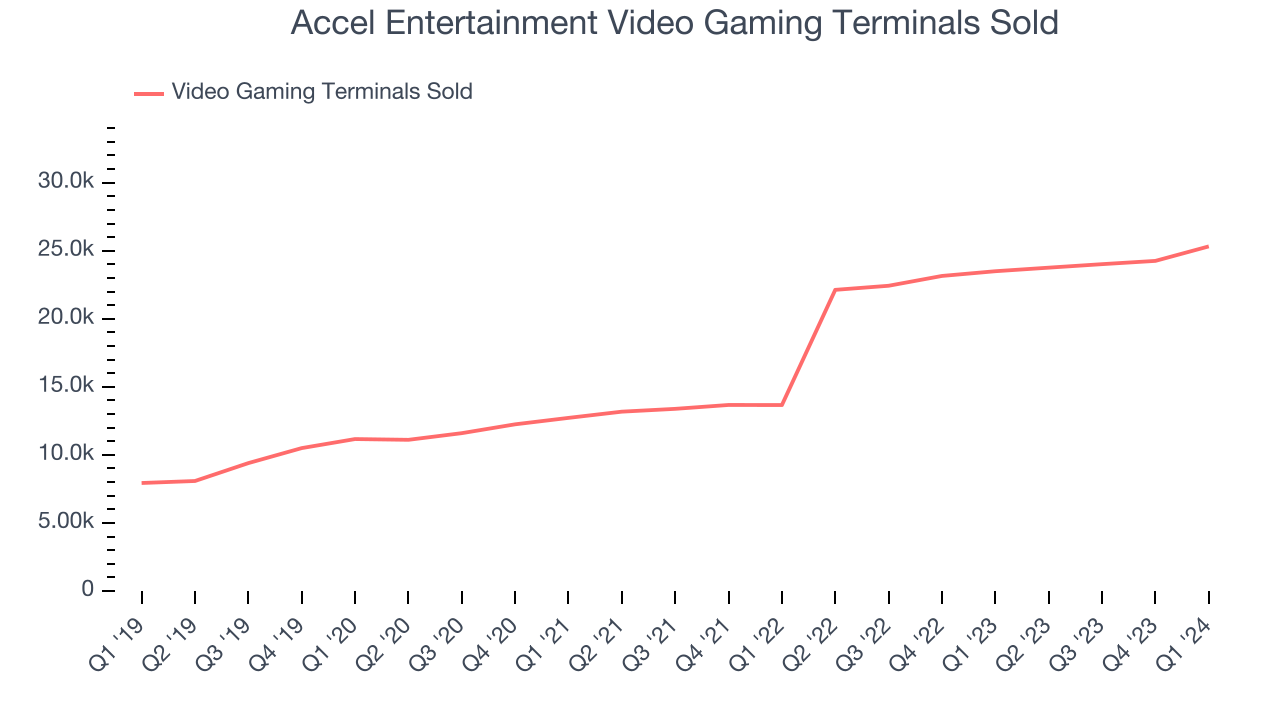

- Video Gaming Terminals Sold: 25,321

- Market Capitalization: $963.4 million

Established in Illinois, Accel Entertainment (NYSE:ACEL) is a provider of electronic gaming machines and interactive amusement terminals to bars and entertainment venues.

Accel Entertainment was founded to capitalize on new legislation in Illinois that permitted video gaming terminals (VGTs) in licensed non-casino locations such as bars, restaurants, and truck stops. This strategic move allowed the company to establish a foothold in a niche market, providing gaming solutions in environments different from traditional casinos.

The company specializes in providing an array of electronic gaming machines tailored for use in various entertainment settings. By offering engaging gaming experiences, it addresses the needs of venue owners seeking to enhance their customers' entertainment options. This service diversifies the entertainment experience for patrons and provides an additional revenue stream for venue operators.

Accel Entertainment’s revenue model is built on partnerships with venue operators. The company installs gaming machines at partner locations and participates in revenue share agreements, where it gets paid depending on how much money its machines win per day. This model is mutually beneficial as operators do not have to purchase these expensive machines outright, which can cost north of $10,000.

Gaming Solutions

Gaming solution companies operate in a dynamic and evolving market, and the digital transformation of the gaming industry presents significant opportunities for innovation and growth, whether it be immersive slot machine terminals or mobile sports betting. However, the gaming solution industry is not without its challenges. Regulatory compliance is a crucial consideration as companies must navigate a complex and often fragmented regulatory landscape across different jurisdictions. Changes in regulations can impact product offerings, operational practices, and market access, requiring companies to maintain flexibility and adaptability in their business strategies. Additionally, the competitive nature of the industry necessitates continuous investment in research and development to stay ahead of competitors and meet evolving consumer demands.

Competitors in the video gaming terminal (VGT) market include Everi Holdings (NYSE:EVRI), PlayAGS (NYSE:AGS), and Inspired Entertainment (NASDAQ:INSE)Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one may grow for years. Accel Entertainment's annualized revenue growth rate of 26.9% over the last five years was excellent for a consumer discretionary business.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Accel Entertainment's recent history shows its momentum has slowed as its annualized revenue growth of 22.6% over the last two years is below its five-year trend.

We can better understand the company's revenue dynamics by analyzing its number of video gaming terminals sold, which reached 25,321 in the latest quarter. Over the last two years, Accel Entertainment's video gaming terminals sold averaged 38% year-on-year growth. Because this number is higher than its revenue growth during the same period, we can see the company's monetization of its consumers has fallen.

This quarter, Accel Entertainment reported reasonable year-on-year revenue growth of 2.9%, and its $301.8 million of revenue topped Wall Street's estimates by 2.1%. Looking ahead, Wall Street expects sales to grow 2.1% over the next 12 months, a deceleration from this quarter.

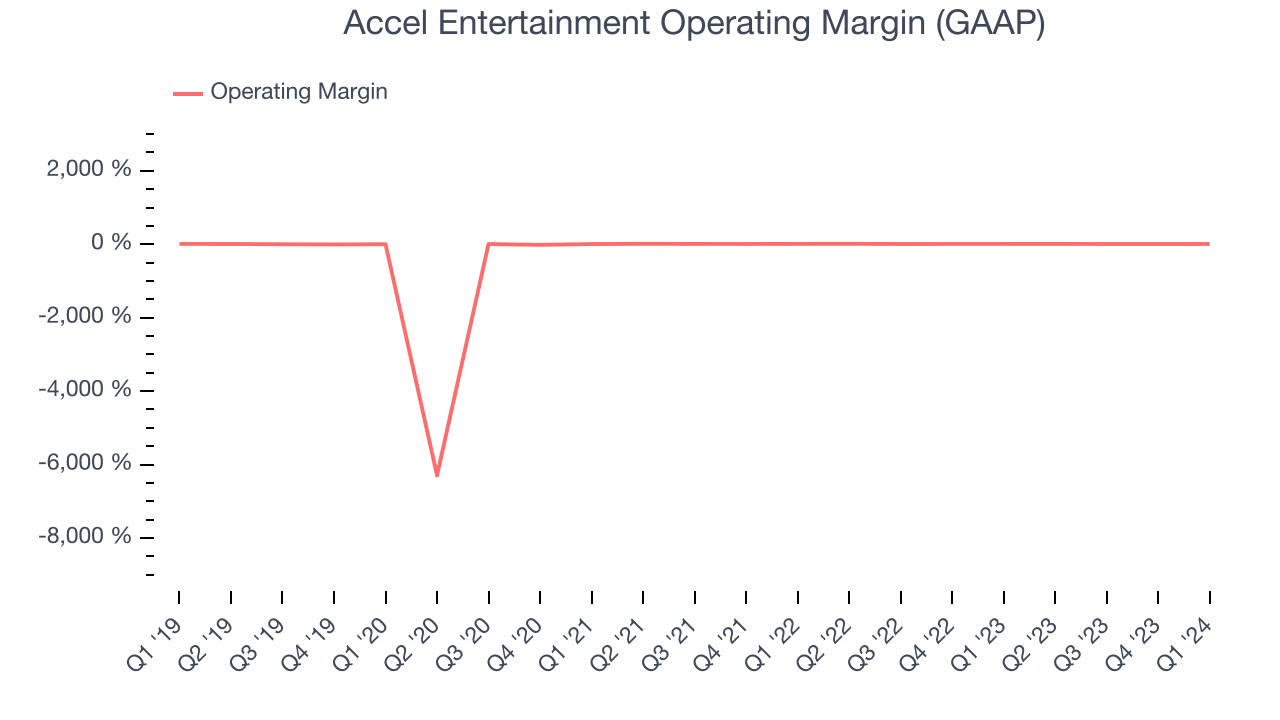

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Accel Entertainment was profitable over the last two years but held back by its large expense base. It's demonstrated mediocre profitability for a consumer discretionary business, producing an average operating margin of 9.3%.

In Q1, Accel Entertainment generated an operating profit margin of 8.5%, in line with the same quarter last year. This indicates the company's costs have been relatively stable.

EPS

We track long-term historical earnings per share (EPS) growth for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Over the last five years, Accel Entertainment's EPS dropped 47.3%, translating into 8.1% annualized declines. Thankfully, Accel Entertainment has bucked its trend as of late, growing its EPS over the last three years. We'll see if the company's growth is sustainable.

In Q1, Accel Entertainment reported EPS at $0.09, down from $0.11 in the same quarter last year. This print unfortunately missed analysts' estimates. We also like to analyze expected EPS growth based on Wall Street analysts' consensus projections, but unfortunately, there is insufficient data.

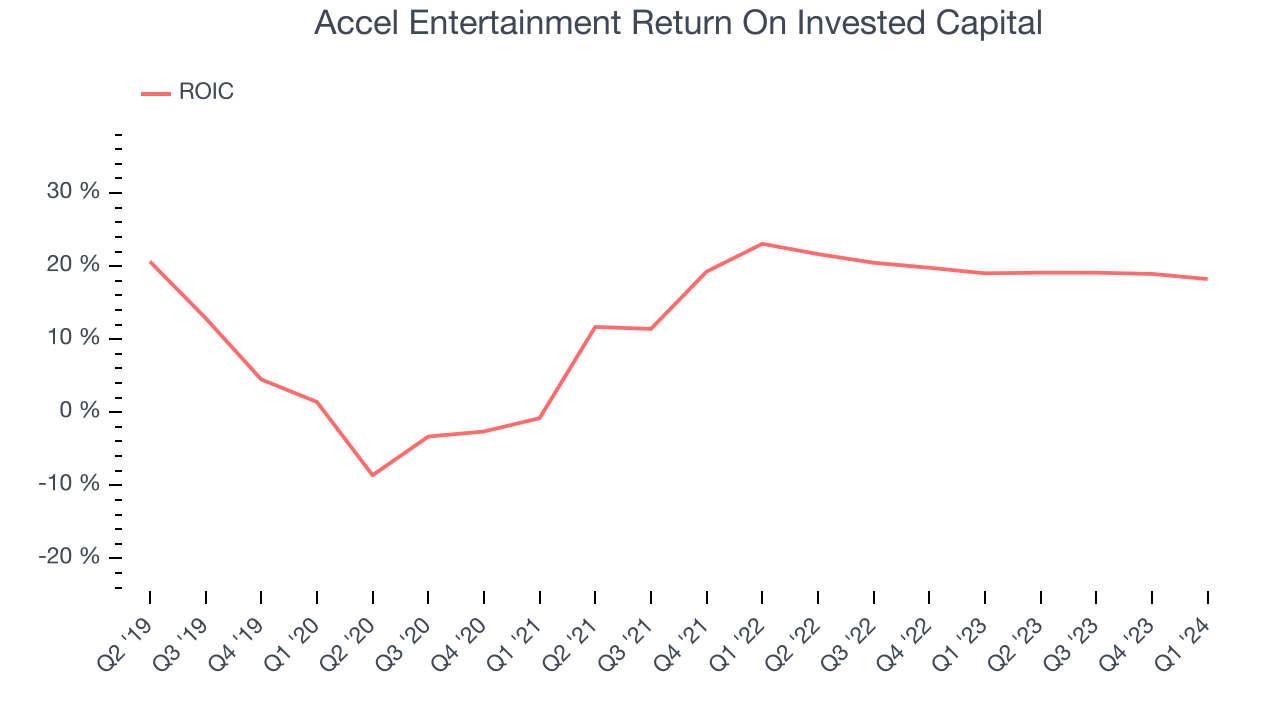

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Accel Entertainment's five-year average return on invested capital was 12.2%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last few years, Accel Entertainment's ROIC has significantly increased. This is a good sign, and if the company's returns keep rising, there's a chance it could evolve into an investable business.

Balance Sheet Risk

As long-term investors, the risk we care most about is the permanent loss of capital. This can happen when a company goes bankrupt or raises money from a disadvantaged position and is separate from short-term stock price volatility, which we are much less bothered by.

Accel Entertainment reported $253.9 million of cash and $539.9 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $181.6 million of EBITDA over the last 12 months, we view Accel Entertainment's 1.6x net-debt-to-EBITDA ratio as safe. We also see its $17.74 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from Accel Entertainment's Q1 Results

It was good to see Accel Entertainment beat analysts' revenue expectations this quarter as its number of video gaming terminals sold outperformed. On the other hand, its EPS missed Wall Street's estimates. Overall, this was a bad quarter for Accel Entertainment. The company is down 2.8% on the results and currently trades at $11.3 per share.

Is Now The Time?

Accel Entertainment may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

Accel Entertainment isn't a bad business, but it probably wouldn't be one of our picks. Although its revenue growth has been exceptional over the last five years, its declining EPS over the last five years makes it hard to trust. And while its number of video gaming terminals sold have surged over the last two years, the downside is its mediocre ROIC suggests it has grown profits at a slow pace historically.

Accel Entertainment's price-to-earnings ratio based on the next 12 months is 12.8x. In the end, beauty is in the eye of the beholder. While Accel Entertainment wouldn't be our first pick, if you like the business, the shares are trading at a pretty interesting price right now.

Wall Street analysts covering the company had a one-year price target of $14 per share right before these results (compared to the current share price of $11.30).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.