Security technology and services company ADT (NYSE:ADT) reported results in line with analysts' expectations in Q1 CY2024, with revenue down 25% year on year to $1.21 billion. It made a non-GAAP profit of $0.16 per share, improving from its profit of $0.14 per share in the same quarter last year.

ADT (ADT) Q1 CY2024 Highlights:

- Revenue: $1.21 billion vs analyst estimates of $1.21 billion (small miss)

- EPS (non-GAAP): $0.16 vs analyst estimates of $0.15 (6.2% beat)

- Full year EPS (non-GAAP) guidance: $0.65, maintained from previous, in line with analyst estimates

- Gross Margin (GAAP): 80.5%, up from 68.1% in the same quarter last year

- Free Cash Flow of $323 million, up from $94 million in the previous quarter

- Market Capitalization: $5.75 billion

Founded in 1874 and headquartered in Boca Raton, Florida, ADT (NYSE:ADT) is a provider of security, automation, and smart home solutions, offering comprehensive services for home and business protection.

ADT has evolved into a prominent security company since its early days, offering a comprehensive range of products and services designed to protect homes, businesses, and individuals from security and safety threats.

ADT's extensive product lineup includes burglar alarms, fire and smoke detectors, carbon monoxide alarms, video surveillance systems, and smart home automation technology. The company's solutions extend beyond traditional security systems, integrating software to provide smart, interconnected solutions for modern living. This includes remote monitoring and control capabilities, allowing customers to manage their security systems, lights, thermostats, and cameras using smartphones and other devices.

A cornerstone of ADT's operations is its vast network of monitoring centers, which provide 24/7 monitoring services to ensure rapid response to emergencies and alerts. This around-the-clock protection is a cornerstone of ADT's value proposition, offering peace of mind to millions of customers across the United States and Canada.

Specialized Consumer Services

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

ADT's primary competitors include Ring (owned by Amazon NASDAQ:AMZN), Honeywell (NYSE:HON), Nest Secure (owned by Google NASDAQ:GOOGL), Xfinity Home Security (owned by Comcast NASDAQ:CMCSA), and private companies Vivint Smart Home, SimpliSafe, Brinks Home Security, and Frontpoint.Sales Growth

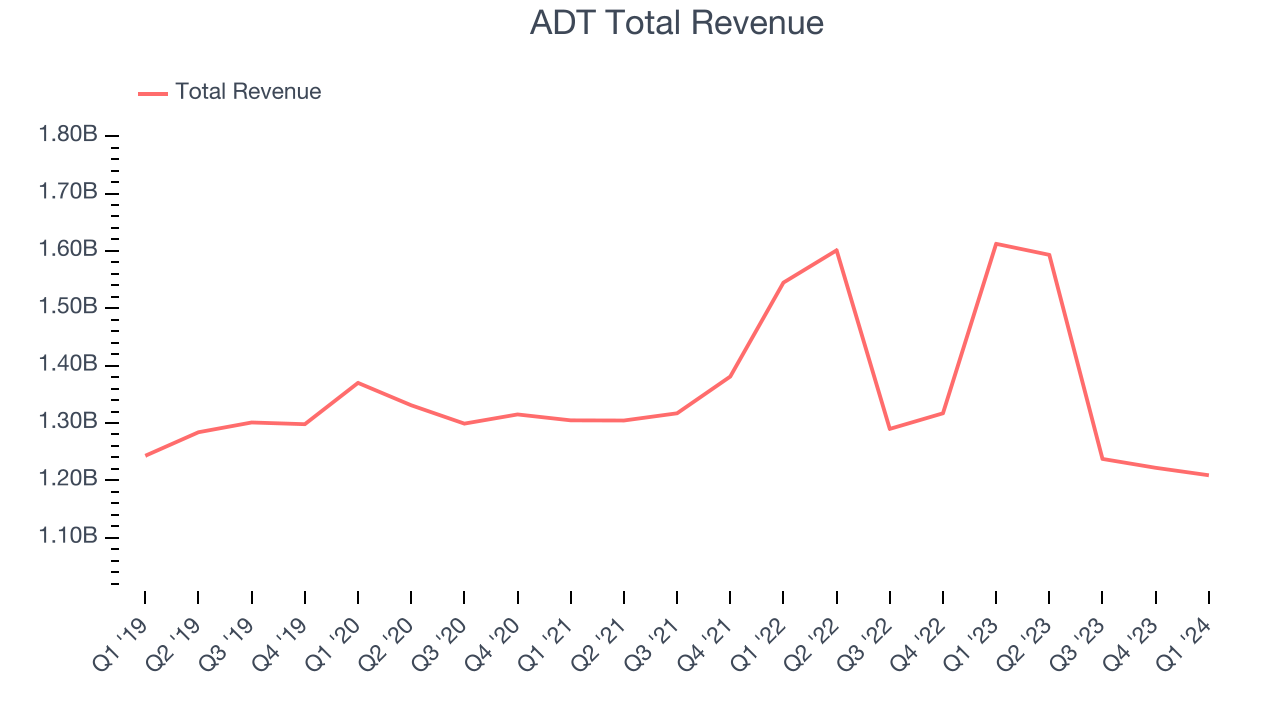

A company’s long-term performance can give signals about its business quality. Any business can put up a good quarter or two, but many enduring ones muster years of growth. ADT's annualized revenue growth rate of 2.3% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. ADT's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 2.6% over the last two years.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. ADT's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 2.6% over the last two years.

This quarter, ADT reported a rather uninspiring 25% year-on-year revenue decline to $1.21 billion of revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects revenue to decline 6% over the next 12 months.

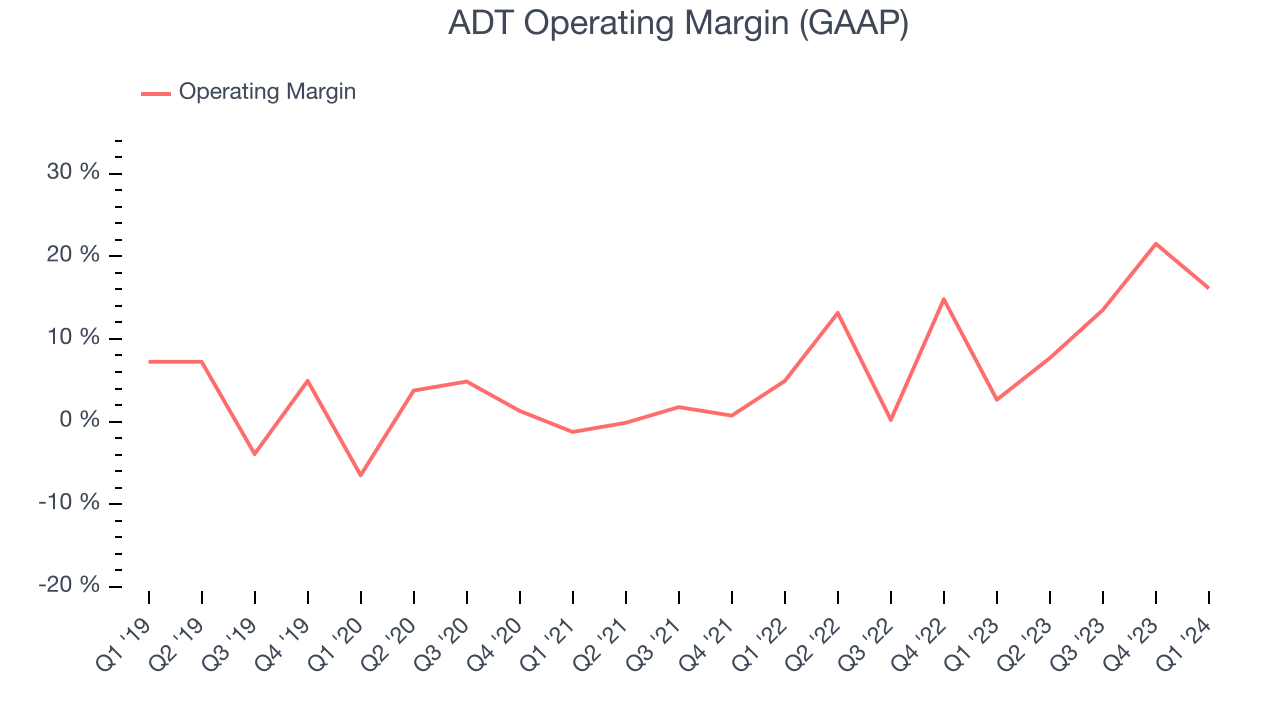

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

ADT has done a decent job managing its expenses over the last eight quarters. The company has produced an average operating margin of 10.8%, higher than the broader consumer discretionary sector.

In Q1, ADT generated an operating profit margin of 16.1%, up 13.5 percentage points year on year.

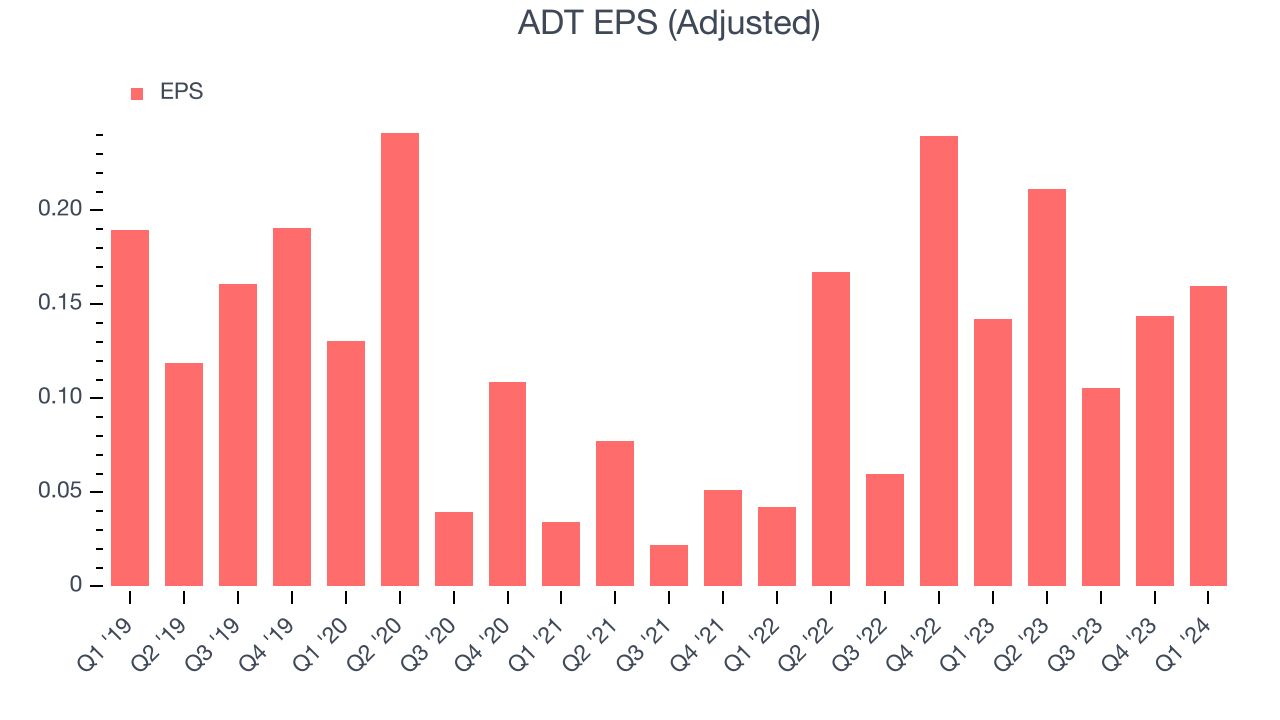

EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last five years, ADT's EPS grew 20.2%, translating into a weak 3.8% compounded annual growth rate. This performance, however, is materially higher than its 2.3% annualized revenue growth over the same period. Let's dig into why.

ADT's operating margin has expanded 8.9 percentage points over the last five years, leading to higher profitability and earnings. Taxes and interest expenses can also affect EPS growth, but they don't tell us as much about a company's fundamentals.In Q1, ADT reported EPS at $0.16, up from $0.14 in the same quarter last year. This print beat analysts' estimates by 6.2%. Over the next 12 months, Wall Street expects ADT to grow its earnings. Analysts are projecting its LTM EPS of $0.62 to climb by 7.8% to $0.67.

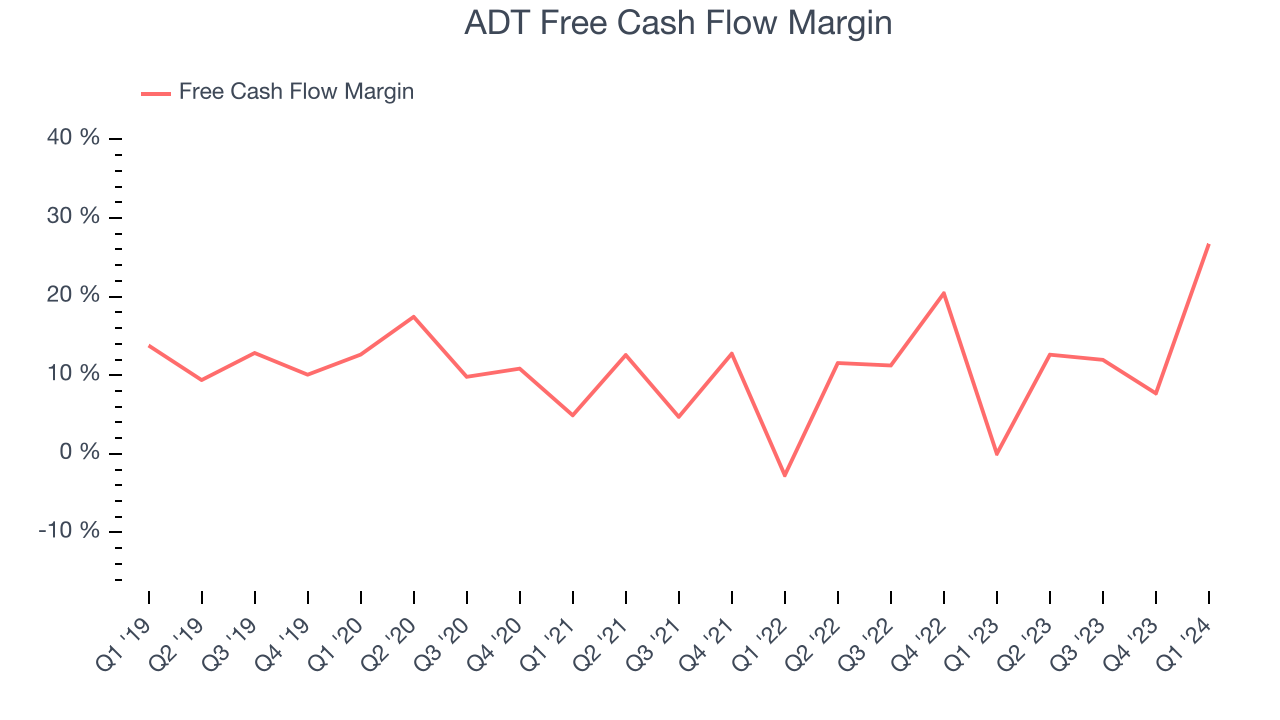

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, ADT has shown decent cash profitability, giving it some reinvestment opportunities. The company's free cash flow margin has averaged 12.3%, slightly better than the broader consumer discretionary sector.

ADT's free cash flow came in at $323 million in Q1, equivalent to a 26.7% margin and up 185,532% year on year.

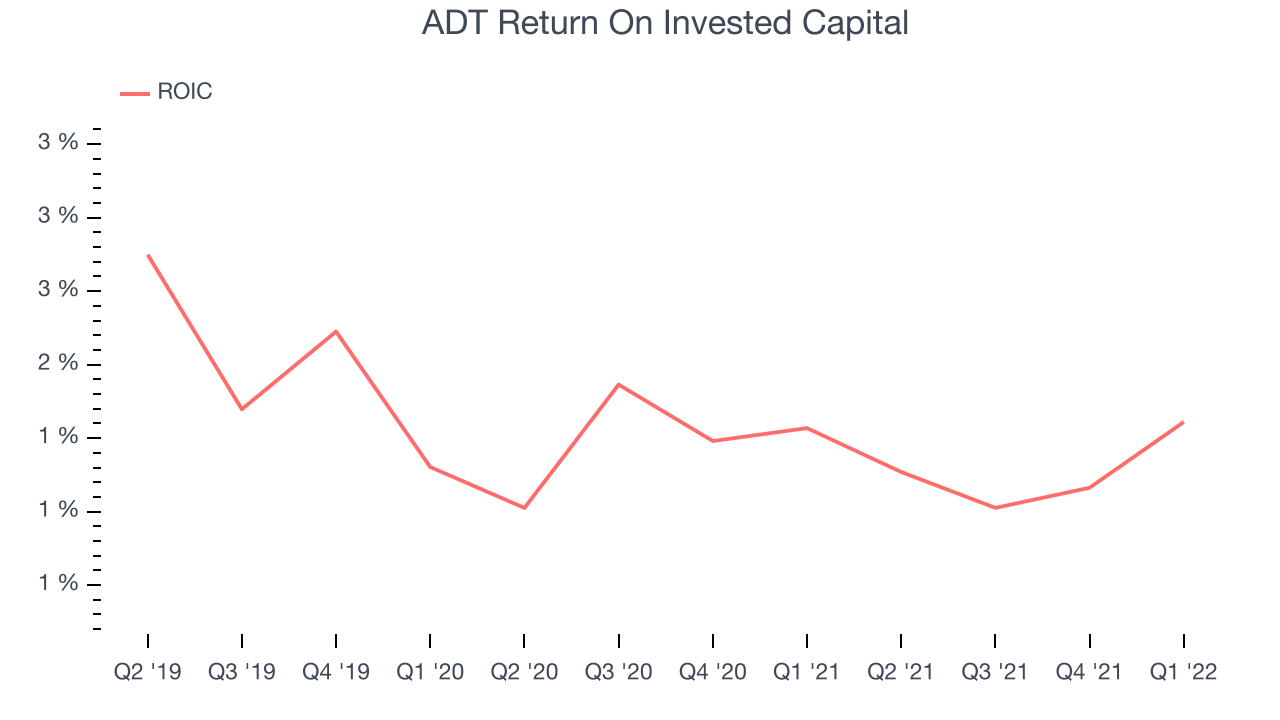

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to how much money the business raised (debt and equity).

ADT's five-year average return on invested capital was 1.5%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly.

ADT reported $4 million of cash and $7.89 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $2.38 billion of EBITDA over the last 12 months, we view ADT's 3.3x net-debt-to-EBITDA ratio as safe. We also see its $422.5 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from ADT's Q1 Results

It was good to see ADT beat analysts' EPS expectations this quarter. On the other hand, its revenue missed slightly, as did operating margin. For the full year, the company maintained its EPS guidance from the previous outlook, showing that the environment in which it operates and its internal expectations haven't changed much from roughly three months ago. Overall, the results were mixed. The stock is flat after reporting and currently trades at $6.4 per share.

Is Now The Time?

ADT may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of ADT, we'll be cheering from the sidelines. Its revenue growth has been weak over the last five years, and analysts expect growth to deteriorate from here. And while its solid free cash flow generation gives it re-investment options, the downside is its number of customers has been disappointing. On top of that, its relatively low ROIC suggests it has historically struggled to find compelling business opportunities.

ADT's price-to-earnings ratio based on the next 12 months is 9.5x. While there are some things to like about ADT and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $9.37 per share right before these results (compared to the current share price of $6.40).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.