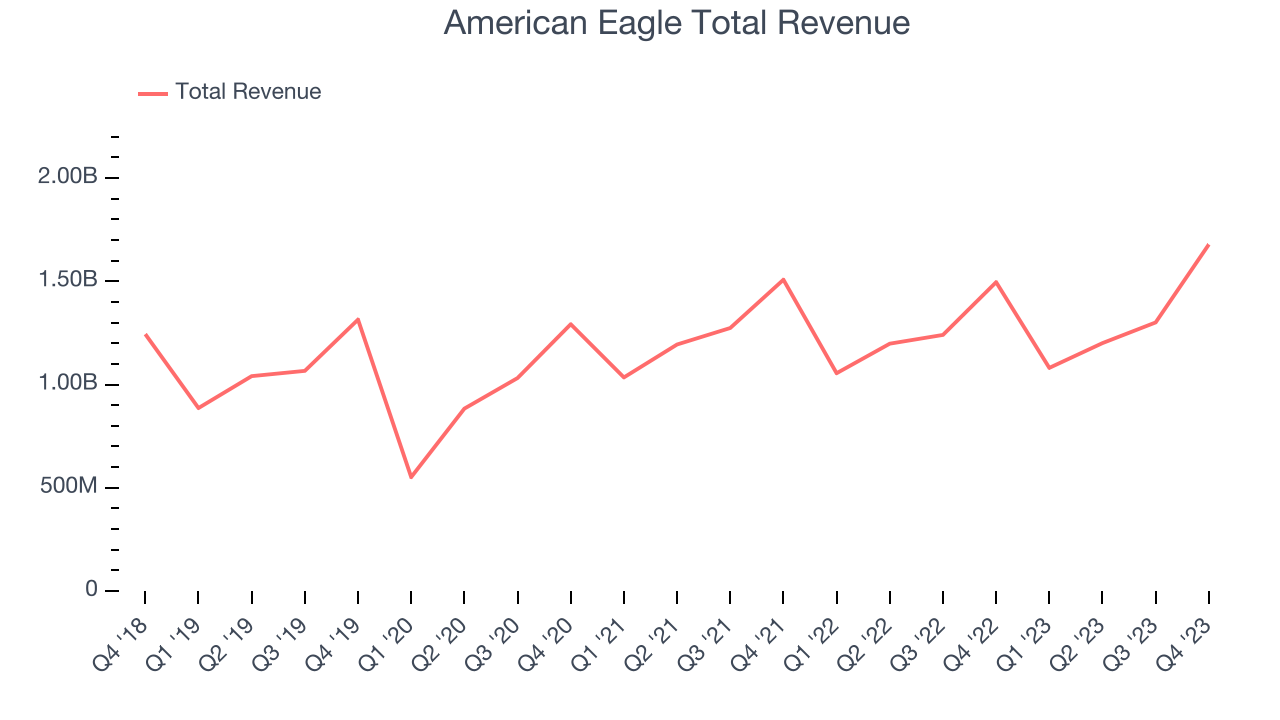

Young adult apparel retailer American Eagle Outfitters (NYSE:AEO) reported results in line with analysts' expectations in Q4 FY2023, with revenue up 12.2% year on year to $1.68 billion. It made a non-GAAP profit of $0.61 per share, improving from its profit of $0.37 per share in the same quarter last year.

Is now the time to buy American Eagle? Find out by accessing our full research report, it's free.

American Eagle (AEO) Q4 FY2023 Highlights:

- Revenue: $1.68 billion vs analyst estimates of $1.67 billion (small beat)

- EPS (non-GAAP): $0.61 vs analyst estimates of $0.50 (20.9% beat)

- Gross Margin (GAAP): 36.6%, up from 33.9% in the same quarter last year

- Store Locations: 1,182 at quarter end, increasing by 7 over the last 12 months

- Market Capitalization: $4.63 billion

“I am proud of how the teams executed in the fourth quarter. As our profit improvement initiatives took hold, we delivered a material improvement in business, underscoring the power of our brands, operations and strategic focus. Customers responded well to our strong merchandise collections fueling positive results across brands and channels,” commented Jay Schottenstein, AEO’s Executive Chairman of the Board and Chief Executive Officer.

With a heavy focus on denim, American Eagle Outfitters (NYSE:AEO) is a specialty retailer offering an assortment of apparel and accessories to young adults.

Apparel Retailer

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

Sales Growth

American Eagle is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the other hand, it has an edge over smaller competitors with fewer resources and can still flex high growth rates because it's growing off a smaller base than its larger counterparts.

As you can see below, the company's annualized revenue growth rate of 5.1% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was weak , but to its credit, it opened new stores and expanded its reach.

This quarter, American Eagle's year-on-year revenue growth clocked in at 12.2%, and its $1.68 billion in revenue was in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 2.4% over the next 12 months, a deceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

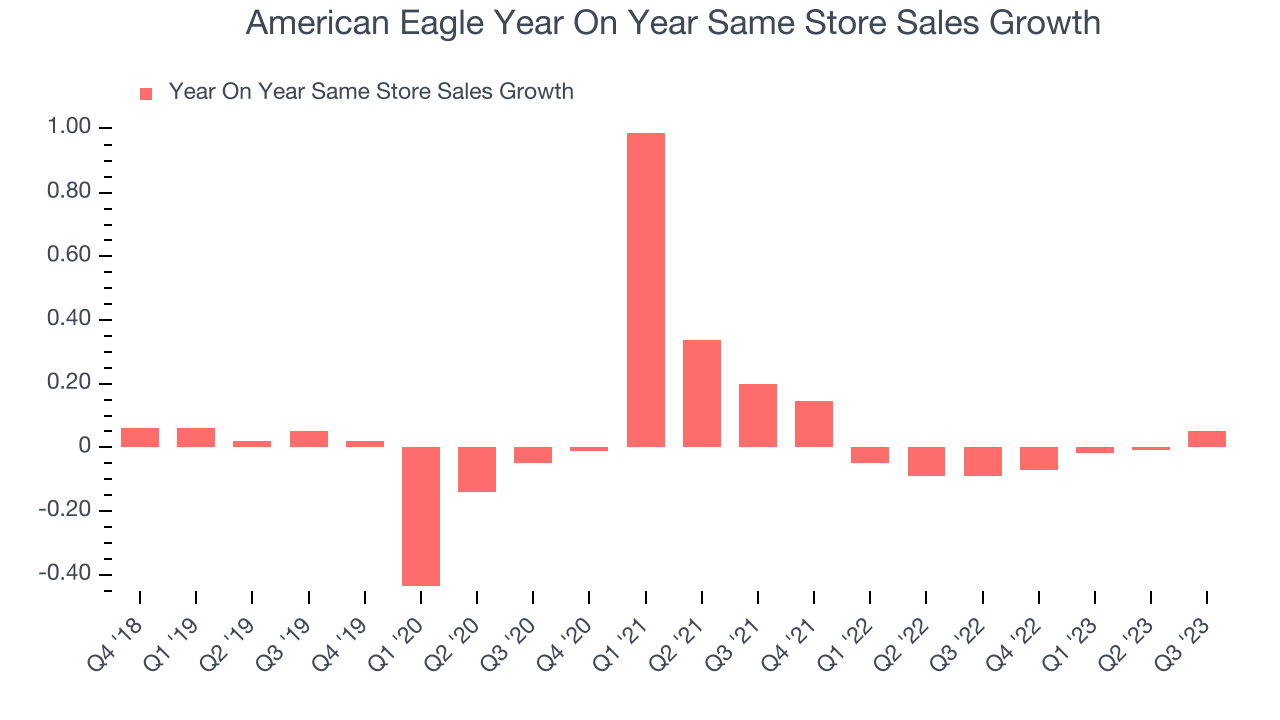

Same-Store Sales

A company's same-store sales growth shows the year-on-year change in sales for its brick-and-mortar stores that have been open for at least a year, give or take, and e-commerce platform. This is a key performance indicator for retailers because it measures organic growth and demand.

American Eagle's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 3.9% year on year. This performance is quite concerning and the company should reconsider its strategy before investing its precious capital into new store buildouts.

Key Takeaways from American Eagle's Q4 Results

We enjoyed seeing American Eagle exceed analysts' revenue and EPS expectations this quarter. Outperformance was driven by its Aerie brand, which saw same-store sales growth of 13% compared to 6% for the flagship American Eagle brand, which is still good.

Looking ahead, management expects revenue to rise by 3% in the full year 2024, falling short of analysts' estimates. However, its forecasted full-year operating income of $455 million easily cleared analysts' expectations of $362 million.

Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is up 12.1% after reporting and currently trades at $26.3 per share.

American Eagle may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.