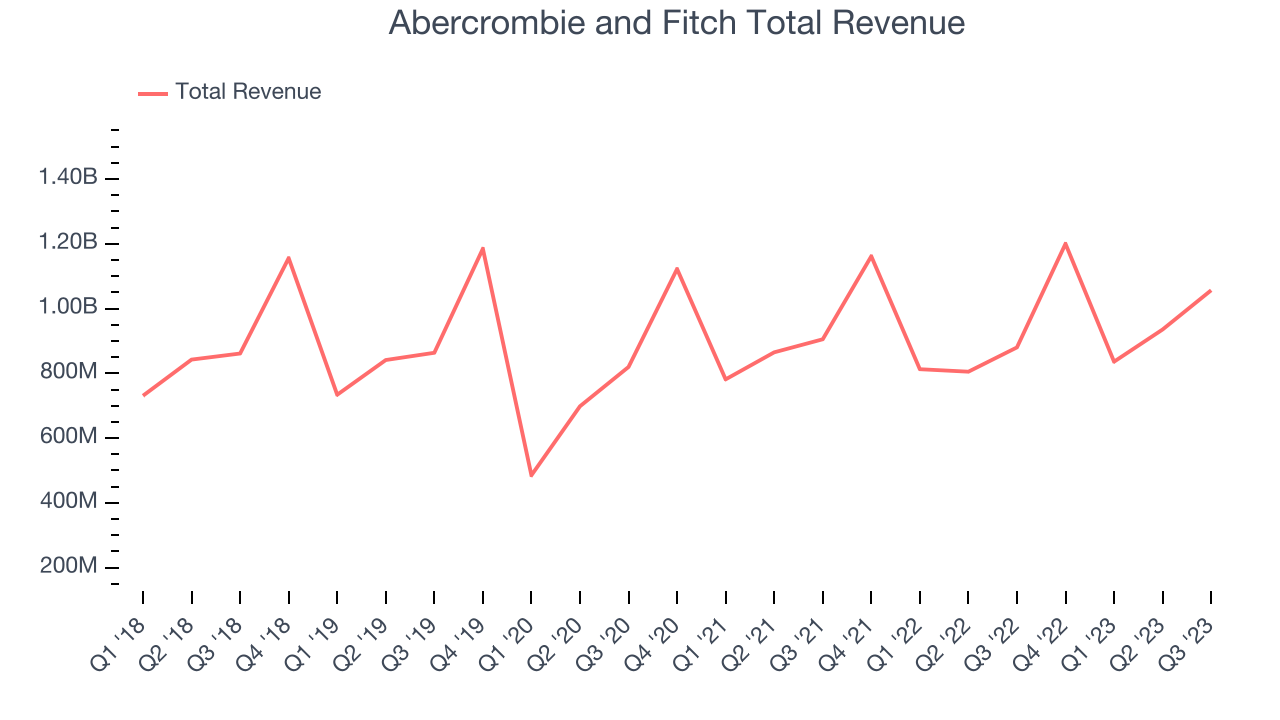

Young adult apparel retailer Abercrombie & Fitch (NYSE:ANF) beat analysts' expectations in Q3 FY2023, with revenue up 20% year on year to $1.06 billion. Turning to EPS, Abercrombie and Fitch made a non-GAAP profit of $1.83 per share, improving from its profit of $0.01 per share in the same quarter last year.

Is now the time to buy Abercrombie and Fitch? Find out by accessing our full research report, it's free.

Abercrombie and Fitch (ANF) Q3 FY2023 Highlights:

- Revenue: $1.06 billion vs analyst estimates of $981.2 million (7.7% beat)

- EPS (non-GAAP): $1.83 vs analyst estimates of $1.18 (54.7% beat)

- Full year guidance for net sales growth and operating margin both raised

- Free Cash Flow of $223.6 million is up from -$102.2 million in the same quarter last year (beat)

- Gross Margin (GAAP): 64.9%, up from 59.2% in the same quarter last year (beat)

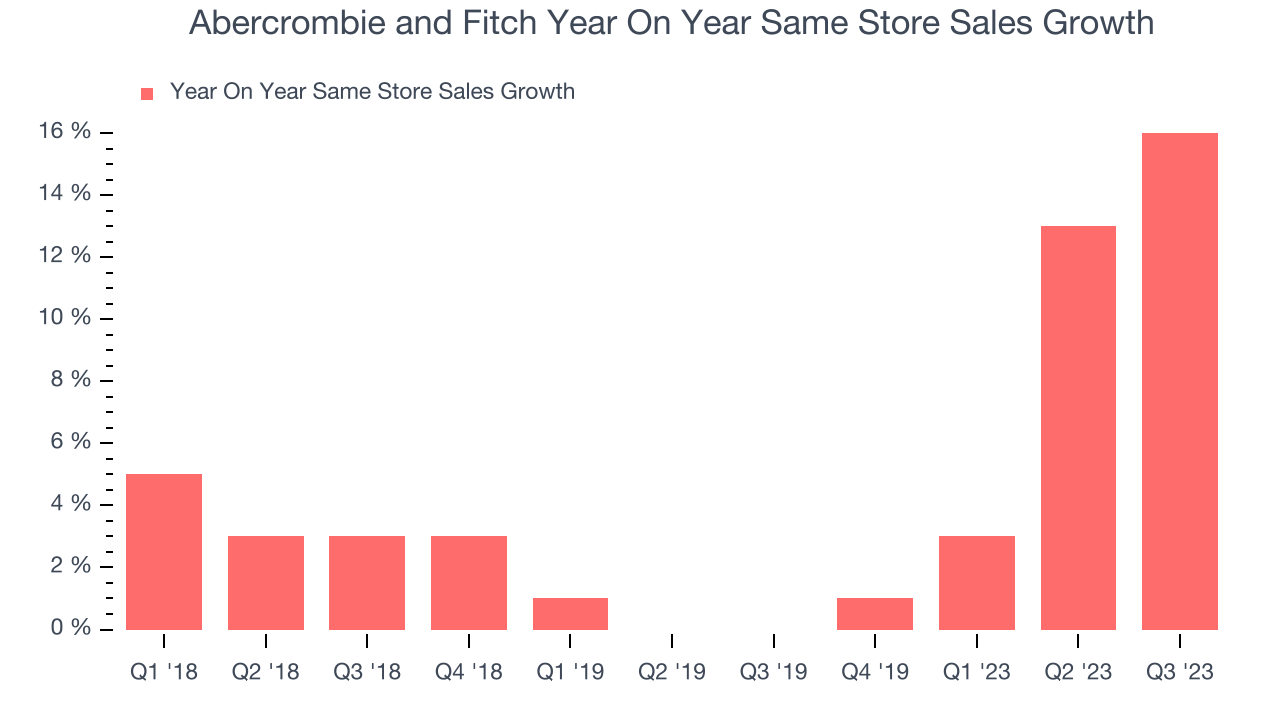

- Same-Store Sales were up 16% year on year (big beat vs. expectations of up 9% year on year)

- Store Locations: 760 at quarter end, increasing by 9 over the last 12 months

Fran Horowitz, Chief Executive Officer, said, “Our strong third quarter results, with net sales and operating margin well-exceeding our expectations, speak to the power of our playbook working globally across our brand portfolio. Net sales growth of 20% accelerated from the second quarter and was once again led by Abercrombie brands with exceptional growth of 30%. At Hollister brands, we had a solid back to school season, delivering 11% net sales growth for the quarter as our assortment and brand evolution is resonating with our teen customer. With strong product acceptance and tightly-controlled inventories across brands, we delivered gross profit rate expansion of 570 basis points to last year in addition to global sales growth. Operationally, we made investments in technology, marketing and our people while delivering strong year-over-year operating leverage resulting in an operating margin of 13.1% for the quarter.

Founded as an outdoor and sporting brand, Abercrombie & Fitch (NYSE:ANF) evolved to become a specialty retailer that sells its own brand of fashionable clothing to young adults.

Apparel Retailer

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

Sales Growth

Abercrombie and Fitch is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the other hand, it has an edge over smaller competitors with fewer resources and can still flex high growth rates because it's growing off a smaller base than its larger counterparts.

As you can see below, the company's annualized revenue growth rate of 2.9% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was mediocre as its store footprint remained relatively unchanged, implying that growth was driven by more sales at existing, established stores.

This quarter, Abercrombie and Fitch reported remarkable year-on-year revenue growth of 20%, and its $1.06 billion in revenue topped Wall Street's estimates by 7.7%. Looking ahead, analysts expect sales to grow 2.8% over the next 12 months.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Number of Stores

A retailer's store count often determines on how much revenue it can generate.

When a retailer like Abercrombie and Fitch keeps its store footprint steady, it usually means that demand is stable and it's focused on improving operational efficiency to increase profitability. Since last year, Abercrombie and Fitch's store count increased by 9 locations, or 1.2%, to 760 total retail locations in the most recently reported quarter.

Over the last two years, the company has only opened a few new stores, averaging 1.9% annual growth in new locations. This sluggish pace lags the broader sector. A flat store base means that revenue growth must come from increased e-commerce sales or higher foot traffic and sales per customer at existing stores.

Same-Store Sales

Abercrombie and Fitch has generated solid demand for its products over the last two years. On average, the company's same-store sales have grown by a healthy 10.7% year on year. Given its flat store count over the same period, this performance stems from increased foot traffic at existing stores or higher e-commerce sales as the company shifts demand from in-store to online.

In the latest quarter, Abercrombie and Fitch's same-store sales rose 16% year on year.

Key Takeaways from Abercrombie and Fitch's Q3 Results

Sporting a market capitalization of $3.64 billion, Abercrombie and Fitch is among smaller companies, but its more than $649.5 million in cash on hand and positive free cash flow over the last 12 months puts it in an attractive position to invest in growth.

We were impressed by how significantly Abercrombie and Fitch blew past analysts' same-store sales, revenue, gross margin, and EPS expectations this quarter. Guidance for the full year was raised across the board. Zooming out, we think this was a great quarter that shareholders will appreciate. The market was likely expecting more, however, and the stock is down 4.3% after reporting, trading at $69.15 per share.

Abercrombie and Fitch may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned in this report.