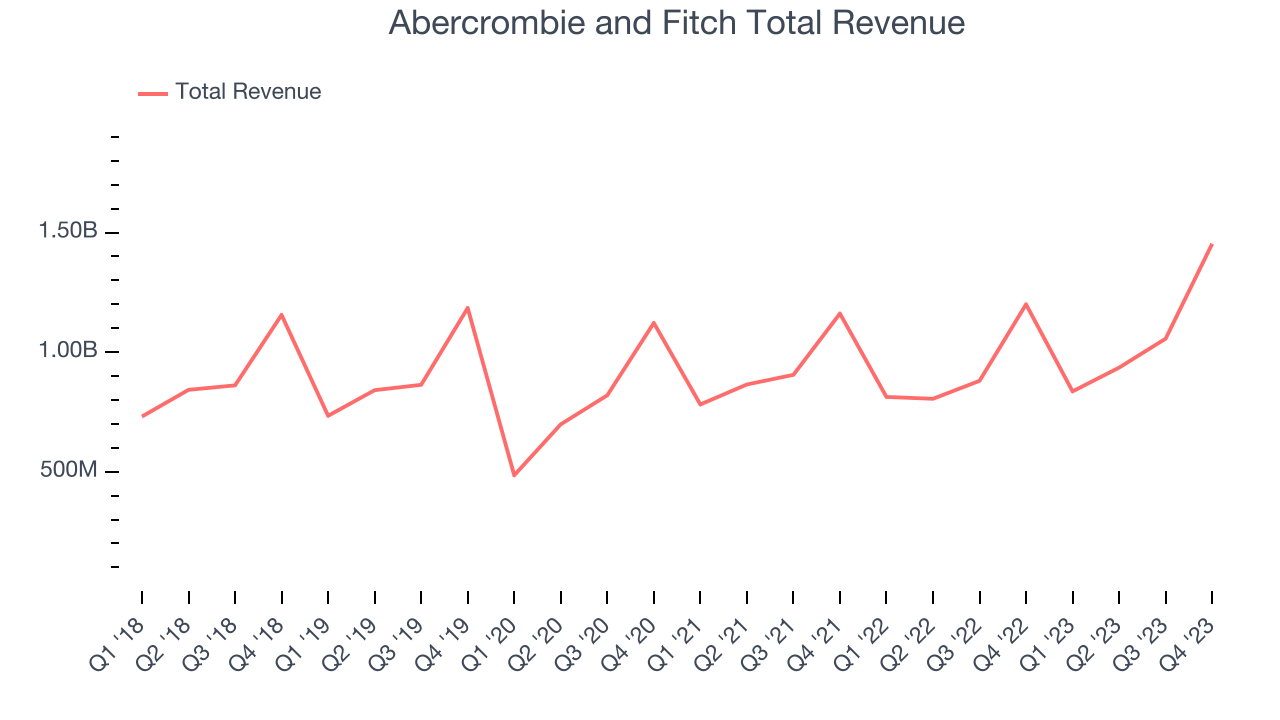

Young adult apparel retailer Abercrombie & Fitch (NYSE:ANF) reported results ahead of analysts' expectations in Q4 FY2023, with revenue up 21.1% year on year to $1.45 billion. It made a non-GAAP profit of $2.97 per share, improving from its profit of $0.81 per share in the same quarter last year.

Abercrombie and Fitch (ANF) Q4 FY2023 Highlights:

- Revenue: $1.45 billion vs analyst estimates of $1.43 billion (1.5% beat)

- EPS (non-GAAP): $2.97 vs analyst estimates of $2.85 (4.4% beat)

- Guidance for full year 2024 slightly ahead for revenue and operating profit

- Free Cash Flow of $145.5 million, down 42.9% from the same quarter last year

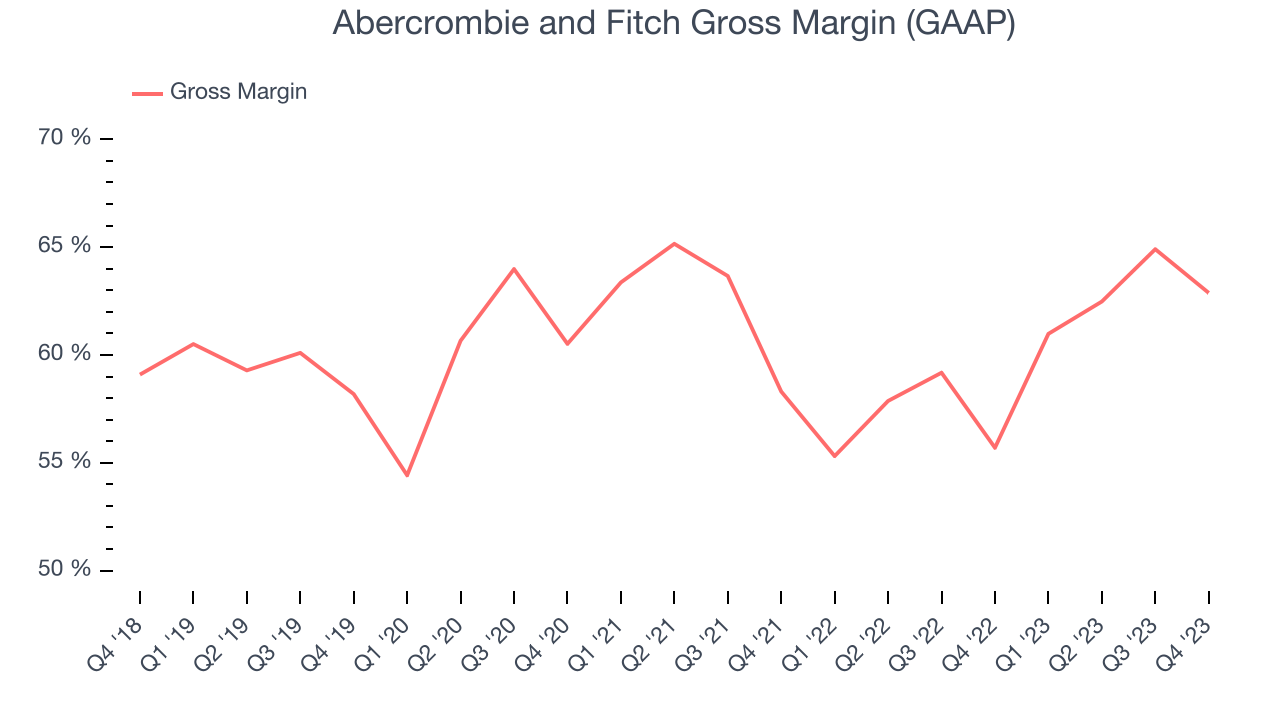

- Gross Margin (GAAP): 62.9%, up from 55.7% in the same quarter last year

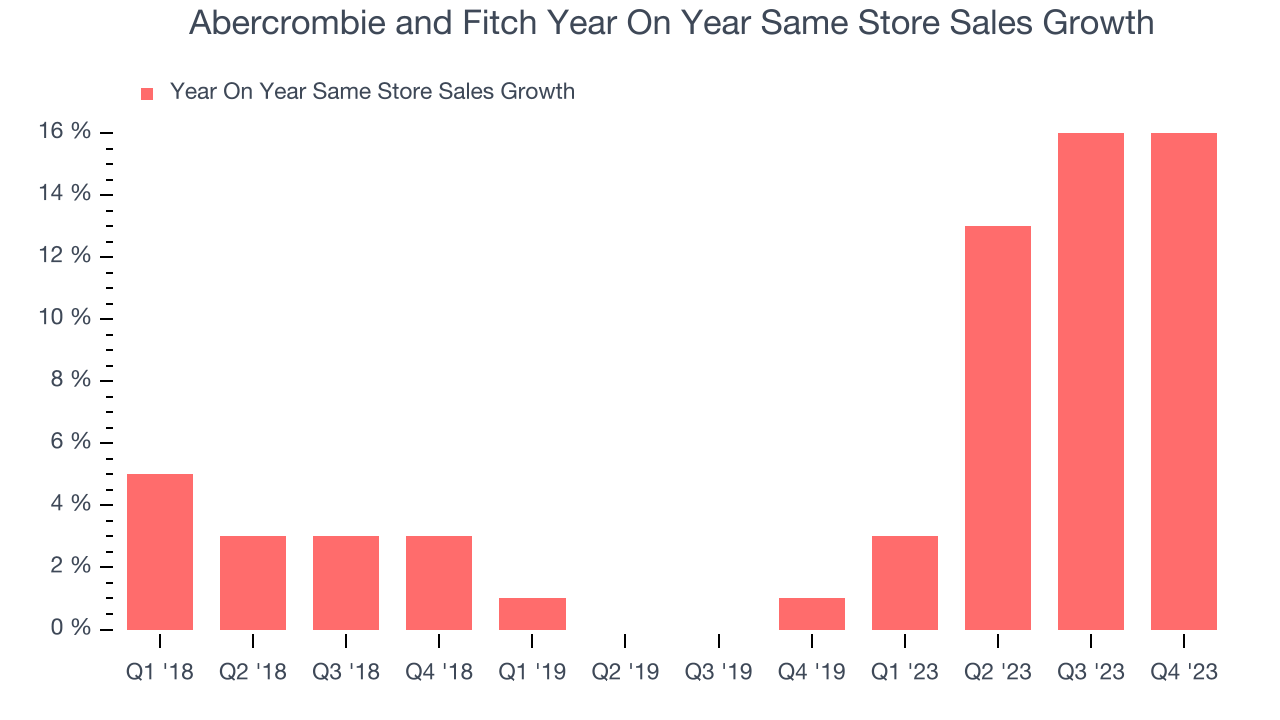

- Same-Store Sales were up 16% year on year (roughly in line)

- Market Capitalization: $7.05 billion

Founded as an outdoor and sporting brand, Abercrombie & Fitch (NYSE:ANF) evolved to become a specialty retailer that sells its own brand of fashionable clothing to young adults.

The core customer is the high school or college student (male and female) who cares about fashion and appearances but prefers casual, somewhat nondescript clothing. In recent years, Abercrombie & Fitch has added a level of sophistication to its designs to appeal to slightly older customers as well. Prices for its jeans, t-shirts, sweatshirts, and casual dresses are considered mid-tier, neither approaching the stratospheric prices of luxury brands but also not as affordable as fast fashion peers.

Historically, Abercrombie & Fitch was known for hiring attractive young store associates, although the company has recently put more emphasis on diversity rather than looks. Stores tend to be roughly 8,000 square feet and located in malls or shopping centers along with other retailers. The ambiance tends to be characterized by dim lighting, loud music, and the smell of its branded fragrance.

In addition to brick and mortar stores, Abercrombie & Fitch has an ecommerce presence that was launched in 1999. This omnichannel approach gives customers options such as pure online shopping or buying online and picking up in store.

Apparel Retailer

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

Retailers offering youth-focused apparel and accessories include American Eagle Outfitters (NYSE:AEO), Urban Outfitters (NASDAQ:URBN), and The Gap (NYSE:GPS).Sales Growth

Abercrombie and Fitch is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the other hand, it has an edge over smaller competitors with fewer resources and can still flex high growth rates because it's growing off a smaller base than its larger counterparts.

As you can see below, the company's annualized revenue growth rate of 4.3% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was weak , but to its credit, it opened new stores and grew sales at existing, established stores.

This quarter, Abercrombie and Fitch reported remarkable year-on-year revenue growth of 21.1%, and its $1.45 billion in revenue topped Wall Street's estimates by 1.5%. Looking ahead, Wall Street expects sales to grow 4.3% over the next 12 months, a deceleration from this quarter.

Same-Store Sales

Same-store sales growth is a key performance indicator used to measure organic growth and demand for retailers.

Abercrombie and Fitch's demand within its existing stores has generally risen over the last two years but lagged behind the broader consumer retail sector. On average, the company's same-store sales have grown by 6.8% year on year. With positive same-store sales growth amid an increasing physical footprint of stores, Abercrombie and Fitch is reaching more customers and growing sales.

In the latest quarter, Abercrombie and Fitch's same-store sales rose 16% year on year. This growth was an acceleration from the 2.3% year-on-year increase it posted 12 months ago, which is always an encouraging sign.

Gross Margin & Pricing Power

Abercrombie and Fitch has best-in-class unit economics for a retailer, enabling it to invest in areas such as marketing and talent to stay one step ahead of the competition. As you can see below, it's averaged an exceptional 60.1% gross margin over the last two years. This means the company makes $0.60 for every $1 in revenue before accounting for its operating expenses.

Abercrombie and Fitch's gross profit margin came in at 62.9% this quarter, marking a 7.2 percentage point increase from 55.7% in the same quarter last year. This margin expansion is a good sign in the near term. It shows the company increased its pricing power, and if this trend continues, it could signal a less competitive environment where it has more negotiating leverage and stable input costs (such as distribution expenses to move goods).

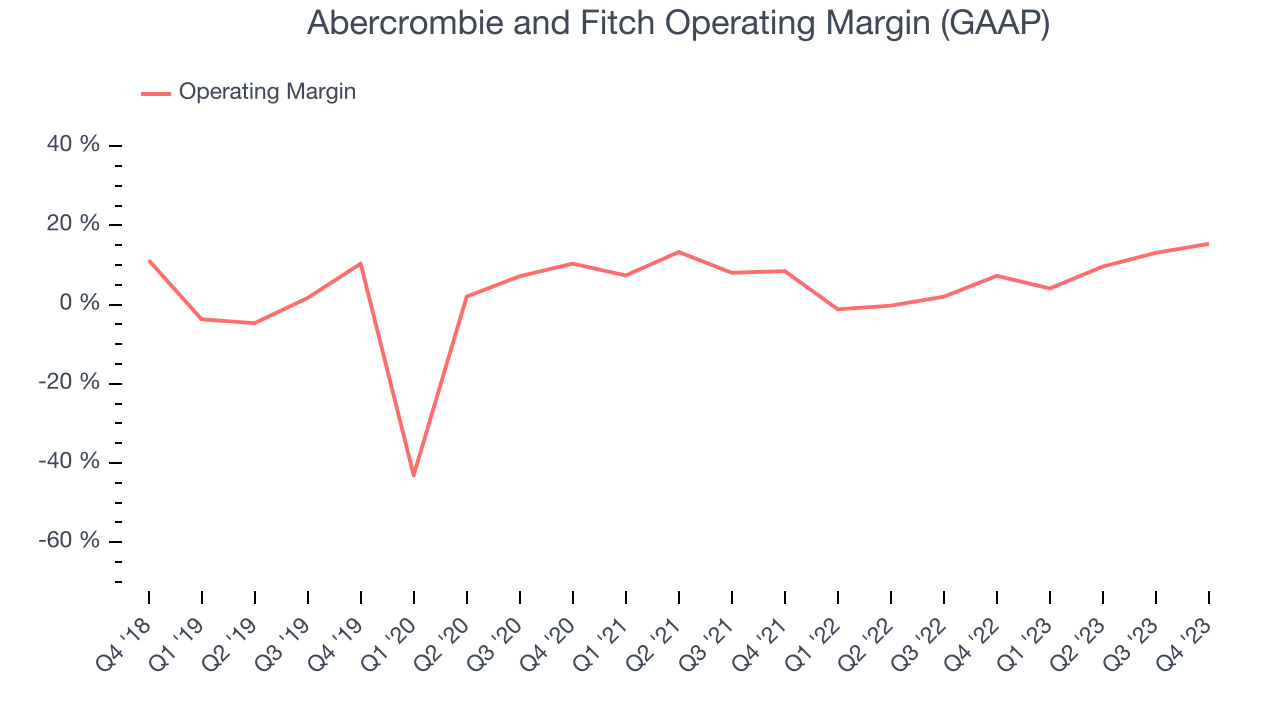

Operating Margin

Operating margin is an important measure of profitability for retailers as it accounts for all expenses keeping the lights on, including wages, rent, advertising, and other administrative costs.

This quarter, Abercrombie and Fitch generated an operating profit margin of 15.3%, up 8.1 percentage points year on year. This increase was encouraging, and we can infer Abercrombie and Fitch was more disciplined with its expenses or gained leverage on fixed costs because its operating margin expanded more than its gross margin.

Zooming out, Abercrombie and Fitch was profitable over the last two years but held back by its large expense base. It's demonstrated mediocre profitability for a consumer retail business, producing an average operating margin of 7.2%. However, Abercrombie and Fitch's margin has improved, on average, by 8.8 percentage points year on year, an encouraging sign for shareholders. The tide could be turning.

Zooming out, Abercrombie and Fitch was profitable over the last two years but held back by its large expense base. It's demonstrated mediocre profitability for a consumer retail business, producing an average operating margin of 7.2%. However, Abercrombie and Fitch's margin has improved, on average, by 8.8 percentage points year on year, an encouraging sign for shareholders. The tide could be turning.EPS

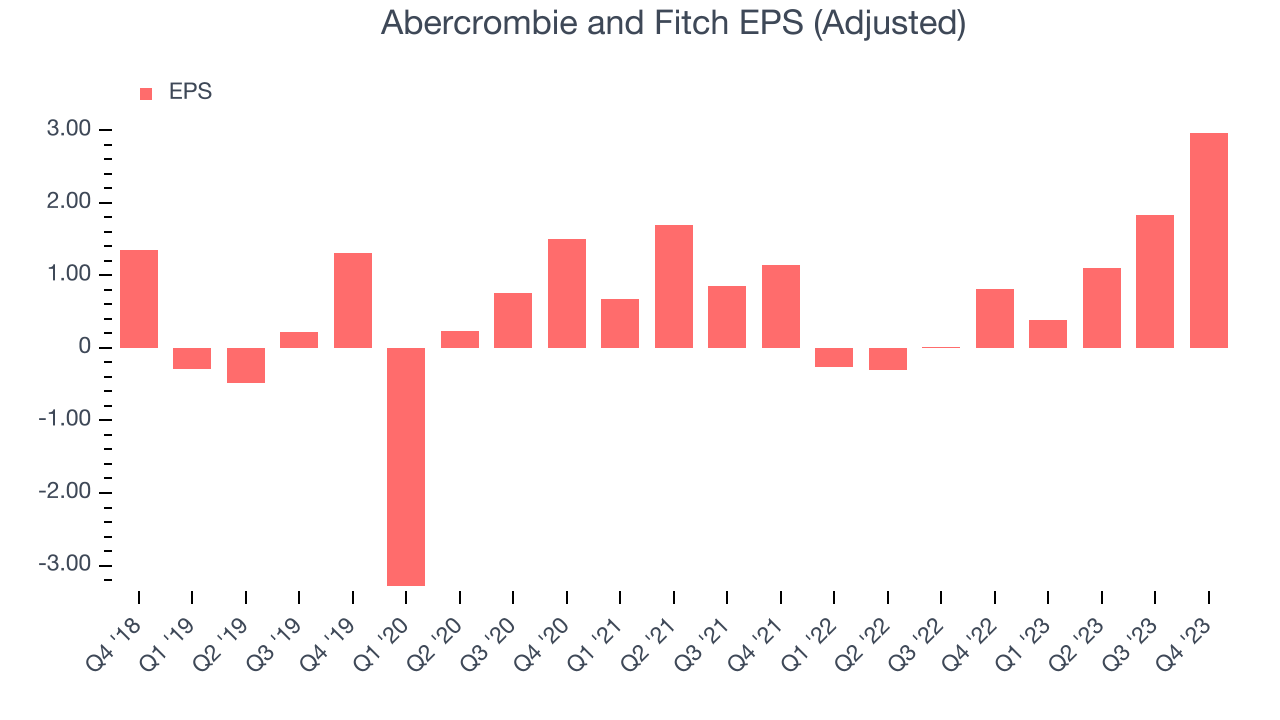

These days, some companies issue new shares like there's no tomorrow. That's why we like to track earnings per share (EPS) because it accounts for shareholder dilution and share buybacks.

In Q4, Abercrombie and Fitch reported EPS at $2.97, up from $0.81 in the same quarter a year ago. This print beat Wall Street's estimates by 4.4%.

Between FY2019 and FY2023, Abercrombie and Fitch's adjusted diluted EPS grew 719%, translating into an astounding 69.2% compounded annual growth rate. This growth is materially higher than its revenue growth over the same period and was driven by excellent expense management (leading to higher profitability) and share repurchases (leading to higher PER share earnings).

Wall Street expects the company to continue growing earnings over the next 12 months, with analysts projecting an average 5.2% year-on-year increase in EPS.

Cash Is King

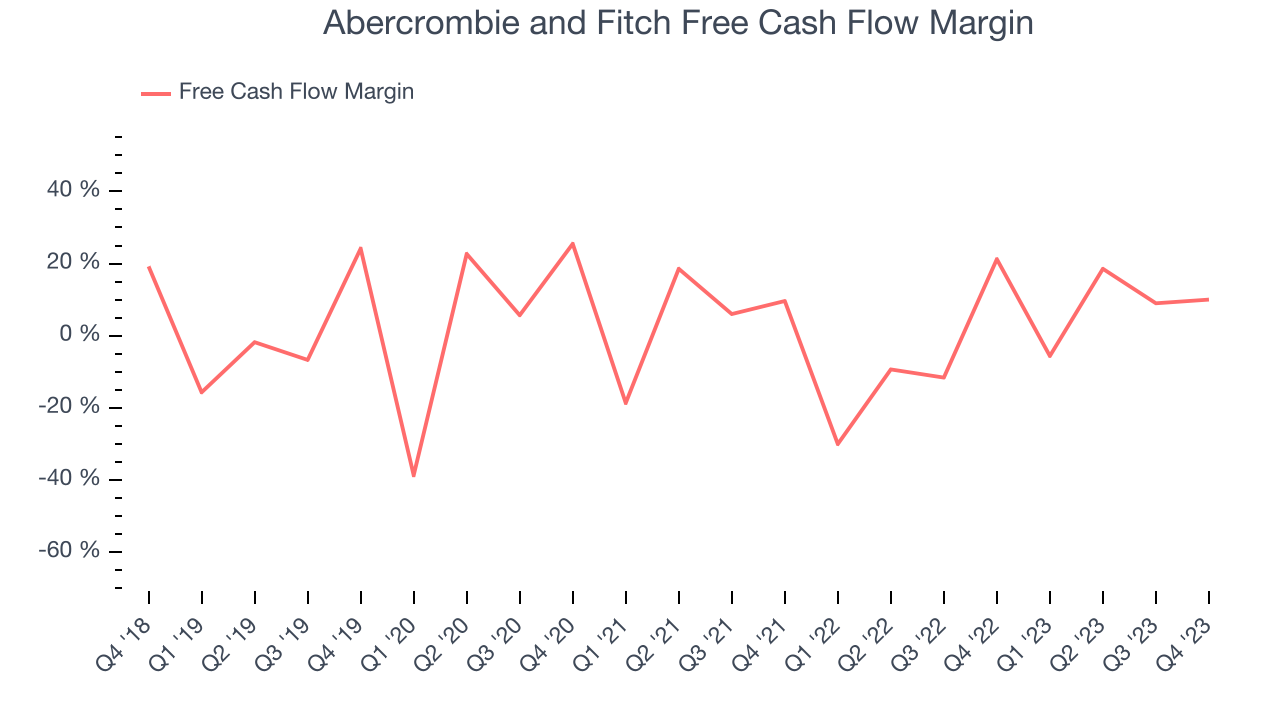

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe in the end, cash is king, and you can't use accounting profits to pay the bills.

Abercrombie and Fitch's free cash flow came in at $145.5 million in Q4, down 42.9% year on year. This result represents a 10% margin.

Over the last two years, Abercrombie and Fitch has shown decent cash profitability, giving it some reinvestment opportunities. The company's free cash flow margin has averaged 2.5%, slightly better than the broader consumer retail sector. Furthermore, its margin has averaged year-on-year increases of 13.1 percentage points. Shareholders should be excited as this will certainly help Abercrombie and Fitch achieve its long-term strategic goals.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Abercrombie and Fitch's five-year average ROIC was 9.6%, somewhat low compared to the best retail companies that consistently pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last two years, Abercrombie and Fitch's ROIC averaged 15.2 percentage point increases each year. This is a good sign, and if the company's returns keep rising, there's a chance it could evolve into an investable business.

Key Takeaways from Abercrombie and Fitch's Q4 Results

We were impressed that Abercrombie and Fitch beat on revenue, gross margin, and EPS. Full year guidance for revenue and operating profit were also slightly ahead of expectations. Overall, we think this was a strong quarter that should satisfy shareholders. The stock is flat after reporting and currently trades at $139 per share.

Is Now The Time?

Abercrombie and Fitch may have had a good quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We have other favorites, but we understand the arguments that Abercrombie and Fitch isn't a bad business. Although its revenue growth has been a little slower over the last four years, its impressive gross margins are a wonderful starting point for the overall profitability of the business. Investors should still be cautious, however, as its relatively low ROIC suggests it has struggled to grow profits historically.

Abercrombie and Fitch's price-to-earnings ratio based on the next 12 months is 21.2x. We don't really see a big opportunity in the stock at the moment, but in the end, beauty is in the eye of the beholder. If you like Abercrombie and Fitch, it seems to be trading at a reasonable price.

Wall Street analysts covering the company had a one-year price target of $122.67 per share right before these results (compared to the current share price of $139).

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.