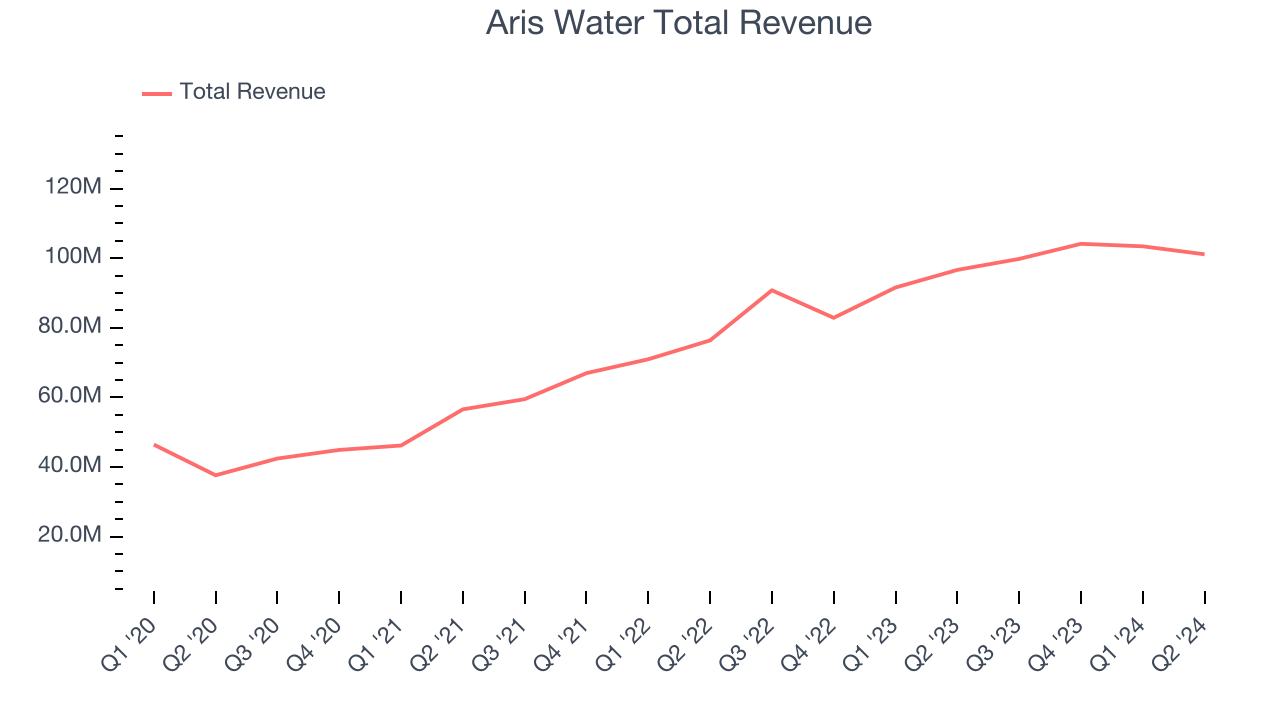

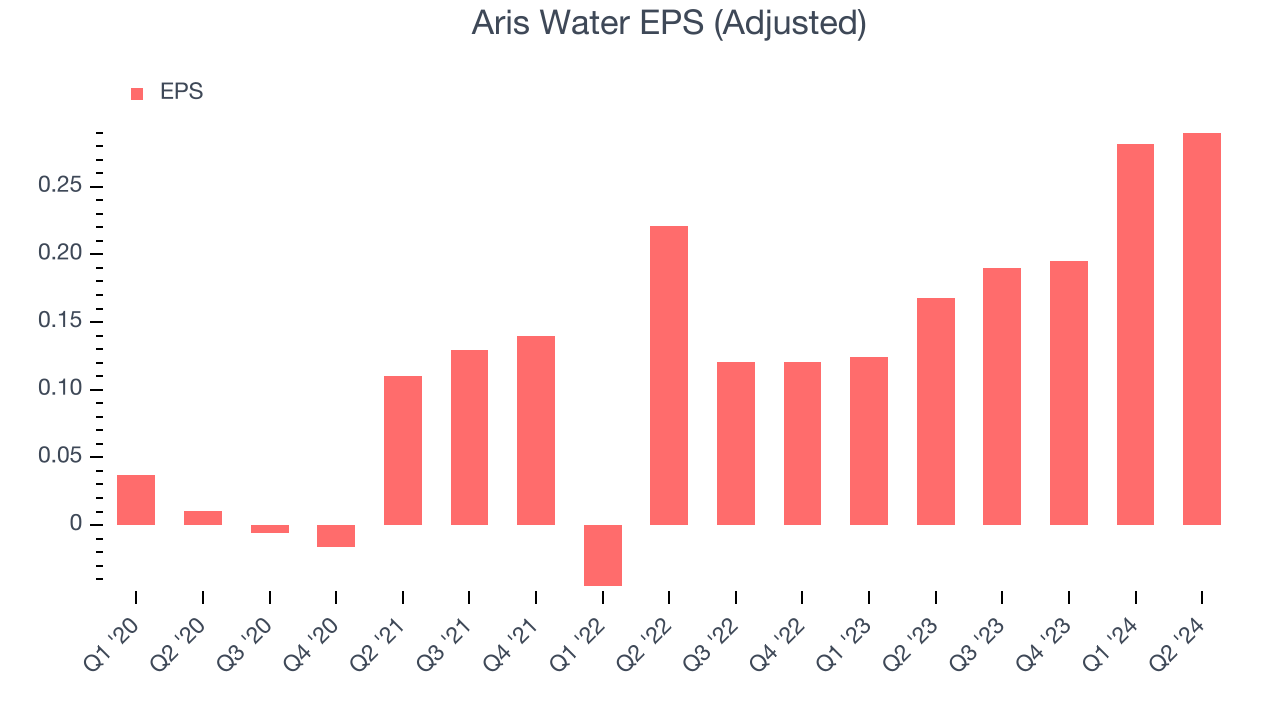

Water handling and recycling company Aris Water (NYSE:ARIS) announced better-than-expected results in Q2 CY2024, with revenue up 4.6% year on year to $101.1 million. It made a non-GAAP profit of $0.29 per share, improving from its profit of $0.17 per share in the same quarter last year.

Is now the time to buy Aris Water? Find out by accessing our full research report, it's free.

Aris Water (ARIS) Q2 CY2024 Highlights:

- Revenue: $101.1 million vs analyst estimates of $96.92 million (4.3% beat)

- EPS (non-GAAP): $0.29 vs analyst estimates of $0.24 (21.9% beat)

- EBITDA guidance for the full year is $200 million at the midpoint (raised from previous), above analyst estimates of $198 million

- Gross Margin (GAAP): 40.8%, down from 54.3% in the same quarter last year

- Adjusted EBITDA Margin: 49.4%, up from 44.1% in the same quarter last year

- Free Cash Flow was -$22.96 million, down from $24.23 million in the previous quarter

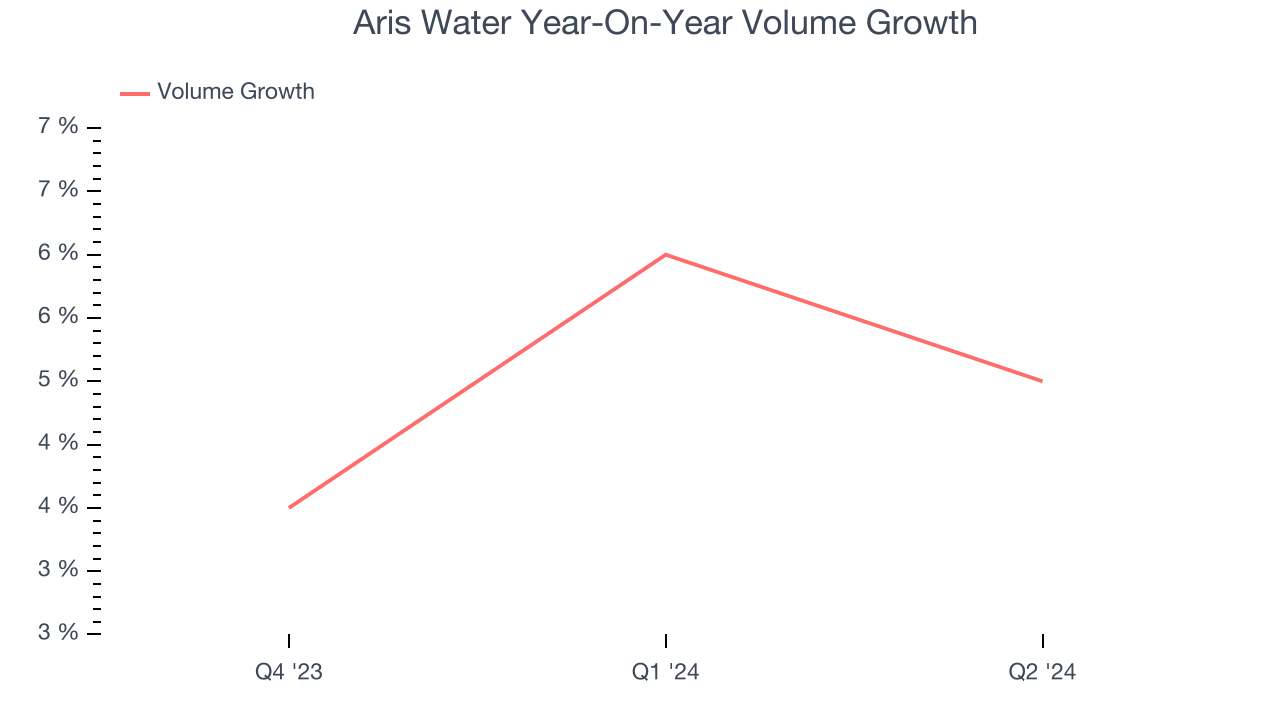

- Sales Volumes were up 5% year on year

- Market Capitalization: $437.1 million

“Aris had a strong second quarter as resilient produced water volumes and operating margins combined to deliver outstanding results. Our customers are steadily growing their production and associated water volumes in our dedicated acreage, and we are pleased with how well Aris has performed to date this year. In the second half of the year, we will remain focused on operating and capital efficiencies, driving free cash flow and working with new and existing customers as we evaluate opportunities for further growth,” said Amanda Brock, President and CEO of Aris.

Primarily serving the oil and gas industry, Aris Water (NYSE:ARIS) is a provider of water handling and recycling solutions.

Air and Water Services

Many air and water services are statutorily mandated or non-discretionary. This means recurring revenues are often earned through contracts, making for more predictable top-line trends. Additionally, there has been an increasing focus on emissions and water conservation over the last decade, driving innovation in the sector and demand for new services. On the other hand, air and water services companies are at the whim of economic cycles. Interest rates, for example, can greatly impact manufacturing or industrial processes that drive incremental demand for these companies’ offerings.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one tends to grow for years. Over the last four years, Aris Water grew its sales at an incredible 24.9% compounded annual growth rate. This is a great starting point for our analysis because it shows Aris Water's offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Aris Water's annualized revenue growth of 22.1% over the last two years is below its four-year trend, but we still think the results were good and suggest demand was strong.

Aris Water also reports its sales volumes, which show how much product it was pushing. Over the last two years, Aris Water's sales volumes averaged 5% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Aris Water reported reasonable year-on-year revenue growth of 4.6%, and its $101.1 million of revenue topped Wall Street's estimates by 4.3%. Looking ahead, Wall Street expects sales to grow 2.3% over the next 12 months, a deceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Operating Margin

Aris Water has been an optimally-run company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 14.9%. This result isn't surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Aris Water's annual operating margin rose by 23 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q2, Aris Water generated an operating profit margin of 23.7%, up 3 percentage points year on year. This increase was encouraging, and since the company's gross margin actually decreased, we can assume it was recently more efficient because its operating expenses like sales, marketing, R&D, and administrative overhead grew slower than its revenue.

EPS

We track the long-term growth in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Aris Water's EPS grew at an astounding 86% compounded annual growth rate over the last four years, higher than its 24.9% annualized revenue growth. This tells us the company became more profitable as it expanded.

Like with revenue, we also analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business. For Aris Water, its two-year annual EPS growth of 46.6% was lower than its four-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q2, Aris Water reported EPS at $0.29, up from $0.17 in the same quarter last year. This print easily cleared analysts' estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Aris Water to grow its earnings. Analysts are projecting its EPS of $0.96 in the last year to climb by 28.1% to $1.23.

Key Takeaways from Aris Water's Q2 Results

We were impressed by how significantly Aris Water blew past analysts' revenue expectations this quarter. We were also excited its EPS outperformed Wall Street's estimates. The company raised full year EBITDA guidance, which is icing on the cake. Zooming out, we think this was an solid quarter. The stock remained flat at $14.91 immediately following the results.

So should you invest in Aris Water right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.