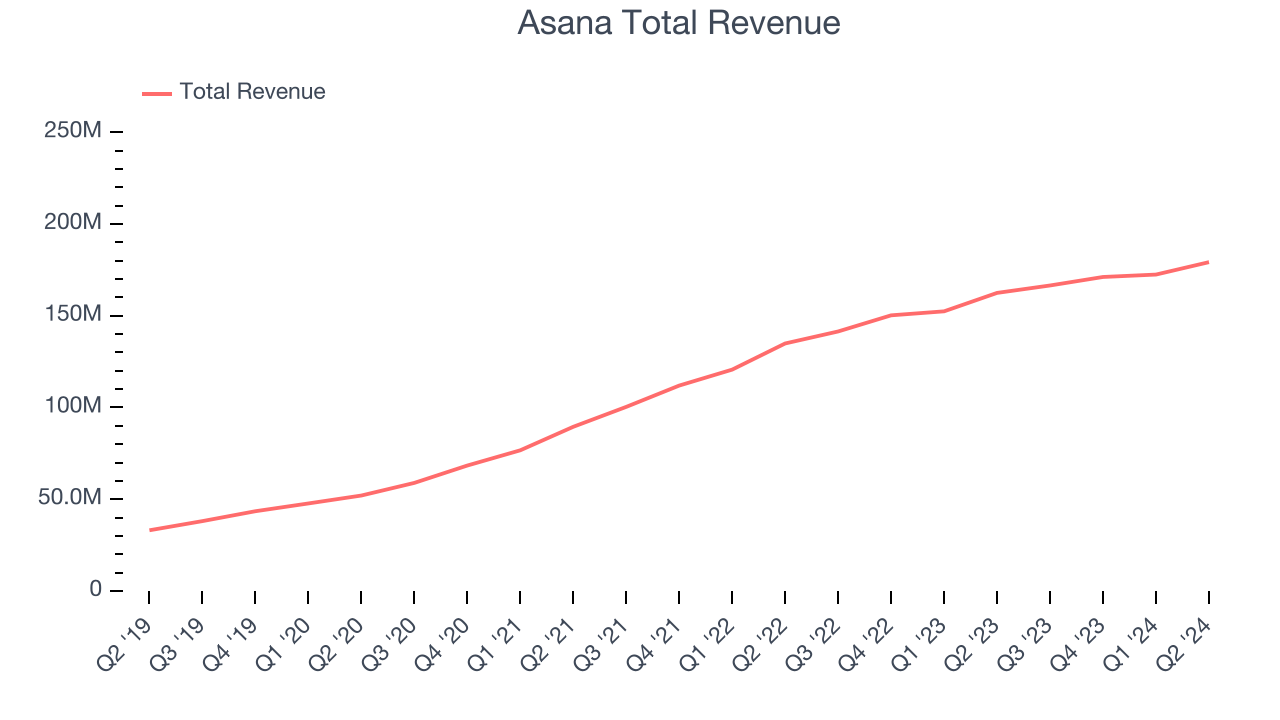

Work management software maker Asana (NYSE: ASAN) beat analysts’ expectations in Q2 CY2024, with revenue up 10.3% year on year to $179.2 million. On the other hand, the company expects next quarter’s revenue to be around $180.5 million, slightly below analysts’ estimates. It made a non-GAAP loss of $0.05 per share, improving from its loss of $0.33 per share in the same quarter last year.

Is now the time to buy Asana? Find out by accessing our full research report, it’s free.

Asana (ASAN) Q2 CY2024 Highlights:

- Revenue: $179.2 million vs analyst estimates of $177.7 million (small beat)

- Adjusted Operating Income: -$15.66 million vs analyst estimates of -$21.44 million (27% beat)

- EPS (non-GAAP): -$0.05 vs analyst estimates of -$0.08

- The company reconfirmed its revenue guidance for the full year of $720 million at the midpoint

- EPS (non-GAAP) guidance for the full year is -$0.20 at the midpoint, beating analyst estimates by 3.6%

- Gross Margin (GAAP): 88.8%, down from 90% in the same quarter last year

- Free Cash Flow was $12.76 million, up from -$4.28 million in the previous quarter

- Net Revenue Retention Rate: 98%, down from 100% in the previous quarter

- Market Capitalization: $3.21 billion

“In Q2, Asana continued to execute on our enterprise transition and make significant strides in AI. We're seeing momentum in key areas, including 17% growth in customers spending over $100,000, success in key verticals, and a record number of multi-year deals,” said Dustin Moskovitz, Co-Founder and Chief Executive Officer of Asana.

Founded in 2008 by Facebook’s co-founder Dustin Moskovitz, Asana (NYSE:ASAN) is a cloud-based project management software, where you can plan and assign tasks to employees and monitor and discuss progress of work.

Project Management Software

The future of work requires teams to collaborate across departments and remote offices. Project management software is both driving this change and benefiting from it. While the trend of collaborative work management has been strong for a while, the Covid pandemic has definitively accelerated the demand for tools that allow work to be done remotely.

Sales Growth

As you can see below, Asana’s 32.9% annualized revenue growth over the last three years has been excellent, and its sales came in at $179.2 million this quarter.

This quarter, Asana’s quarterly revenue was once again up 10.3% year on year. We can see that Asana’s revenue increased by $6.76 million quarter on quarter, which is a solid improvement from the $1.31 million increase in Q1 CY2024. This acceleration of growth was a great sign.

Next quarter’s guidance suggests that Asana is expecting revenue to grow 8.4% year on year to $180.5 million, slowing down from the 17.7% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 10.8% over the next 12 months before the earnings results announcement.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

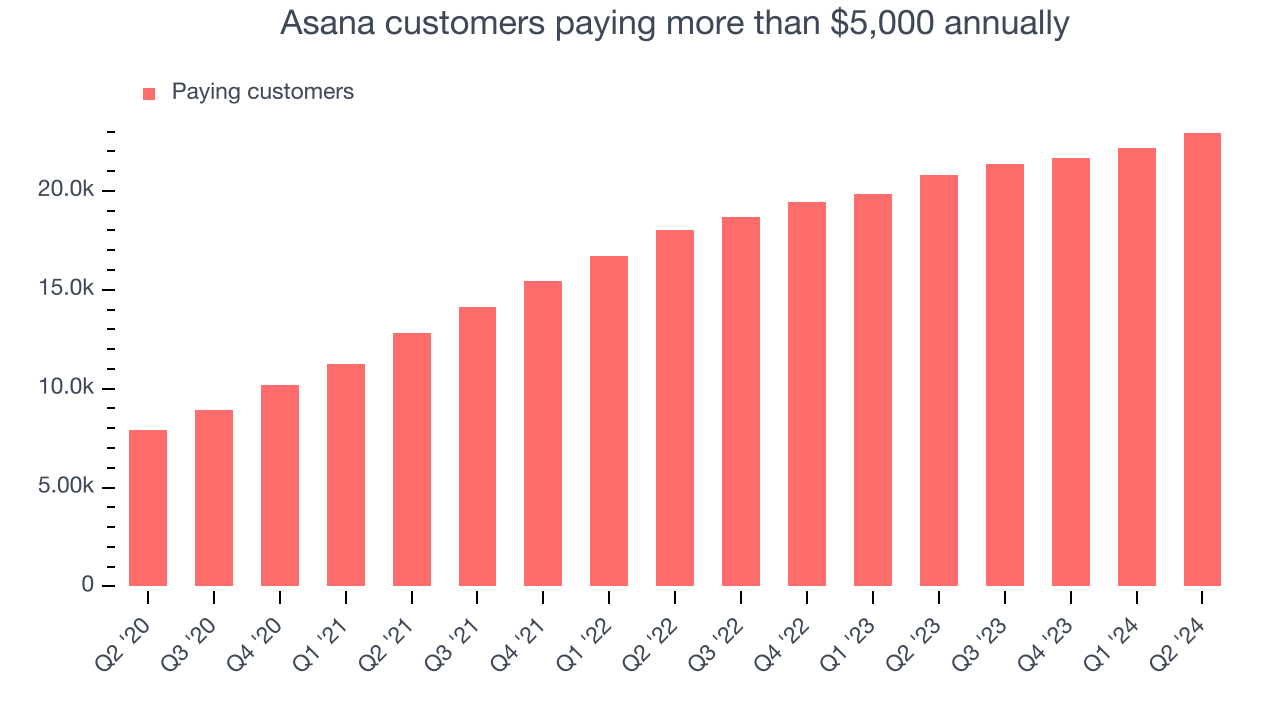

Large Customers Growth

This quarter, Asana reported 22,948 enterprise customers paying more than $5,000 annually, an increase of 786 from the previous quarter. That’s quite a bit more contract wins than last quarter but also quite a bit below what we’ve typically observed over the last year, suggesting that the company may be reinvigorating growth.

Key Takeaways from Asana’s Q2 Results

We struggled to find many strong positives in these results. Although this quarter's revenue and earnings beat, its full-year revenue guidance missed Wall Street’s estimates. Furthermore, its net revenue retention fell below 100%, meaning its customers spent less on its products. Overall, this was a weaker quarter. The stock traded down 12% to $11.68 immediately following the results.

Asana may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.