Work management software maker Asana (NYSE: ASAN) reported Q4 FY2024 results exceeding Wall Street analysts' expectations, with revenue up 13.9% year on year to $171.1 million. The company expects next quarter's revenue to be around $168.5 million, in line with analysts' estimates. It made a non-GAAP loss of $0.04 per share, improving from its loss of $0.15 per share in the same quarter last year.

Is now the time to buy Asana? Find out by accessing our full research report, it's free.

Asana (ASAN) Q4 FY2024 Highlights:

- Revenue: $171.1 million vs analyst estimates of $168 million (1.9% beat)

- EPS (non-GAAP): -$0.04 vs analyst estimates of -$0.10

- Revenue Guidance for Q1 2025 is $168.5 million at the midpoint, roughly in line with what analysts were expecting (however, operating loss for this period was guided worse than expectations)

- Management's revenue guidance for the upcoming financial year 2025 is $719 million at the midpoint, in line with analyst expectations and implying 10.2% growth (vs 19.6% in FY2024) (however, operating loss for this period was guided worse than expectations)

- Gross Margin (GAAP): 89.8%, in line with the same quarter last year

- Free Cash Flow was -$16.95 million compared to -$11.47 million in the previous quarter

- Net Revenue Retention Rate: 100%, in line with the previous quarter

- Market Capitalization: $4.22 billion

“Asana’s Q4 and fiscal year results beat expectations on the top and bottom line. Overall revenue growth was better than our guidance, and operating margin improved significantly during the year, as we target to be free cash flow positive by the end of this year,” said Dustin Moskovitz, co-founder and chief executive officer of Asana.

Founded in 2008 by Facebook’s co-founder Dustin Moskovitz, Asana (NYSE:ASAN) is a cloud-based project management software, where you can plan and assign tasks to employees and monitor and discuss progress of work.

Project Management Software

The future of work requires teams to collaborate across departments and remote offices. Project management software is both driving this change and benefiting from it. While the trend of collaborative work management has been strong for a while, the Covid pandemic has definitively accelerated the demand for tools that allow work to be done remotely.

Sales Growth

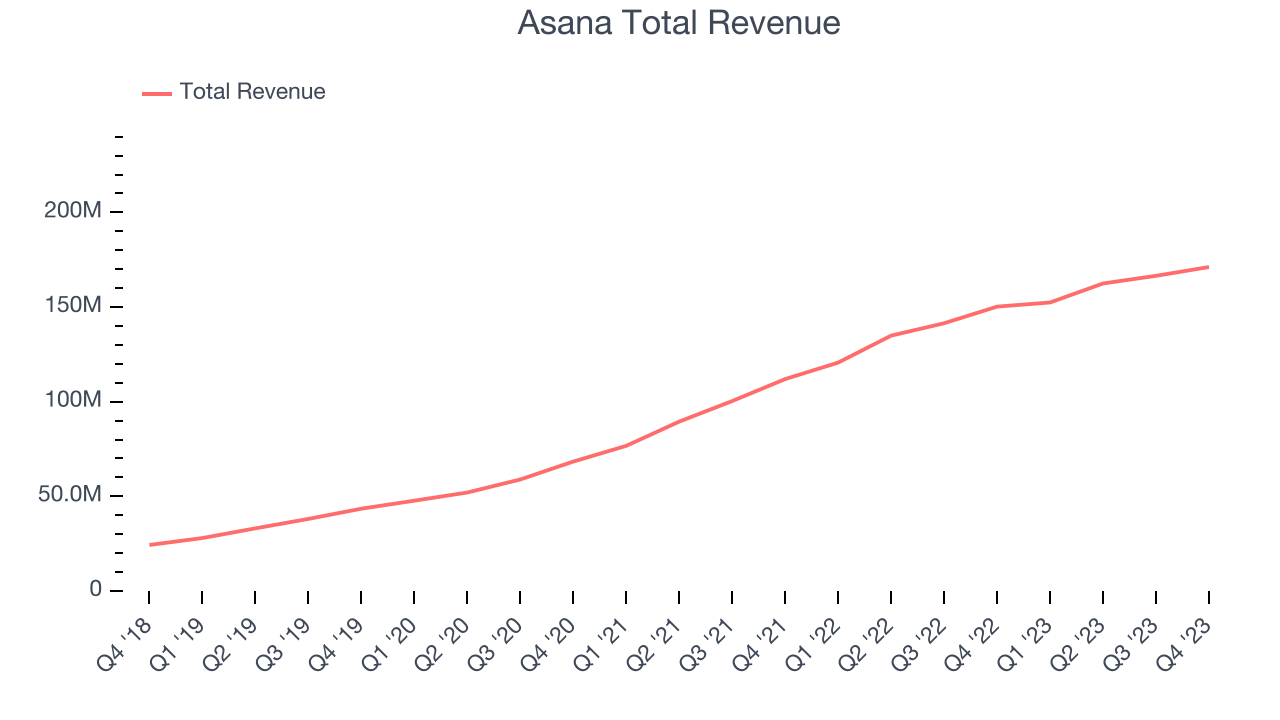

As you can see below, Asana's revenue growth has been impressive over the last three years, growing from $68.37 million in Q4 2021 to $171.1 million this quarter.

This quarter, Asana's quarterly revenue was once again up 13.9% year on year. We can see that Asana's revenue increased by $4.63 million in Q4, up from $4.05 million in Q3 2024. While we've no doubt some investors were looking for higher growth, it's good to see that quarterly revenue is accelerating.

Next quarter's guidance suggests that Asana is expecting revenue to grow 10.6% year on year to $168.5 million, slowing down from the 26.3% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $719 million at the midpoint, growing 10.2% year on year compared to the 19.2% increase in FY2024.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

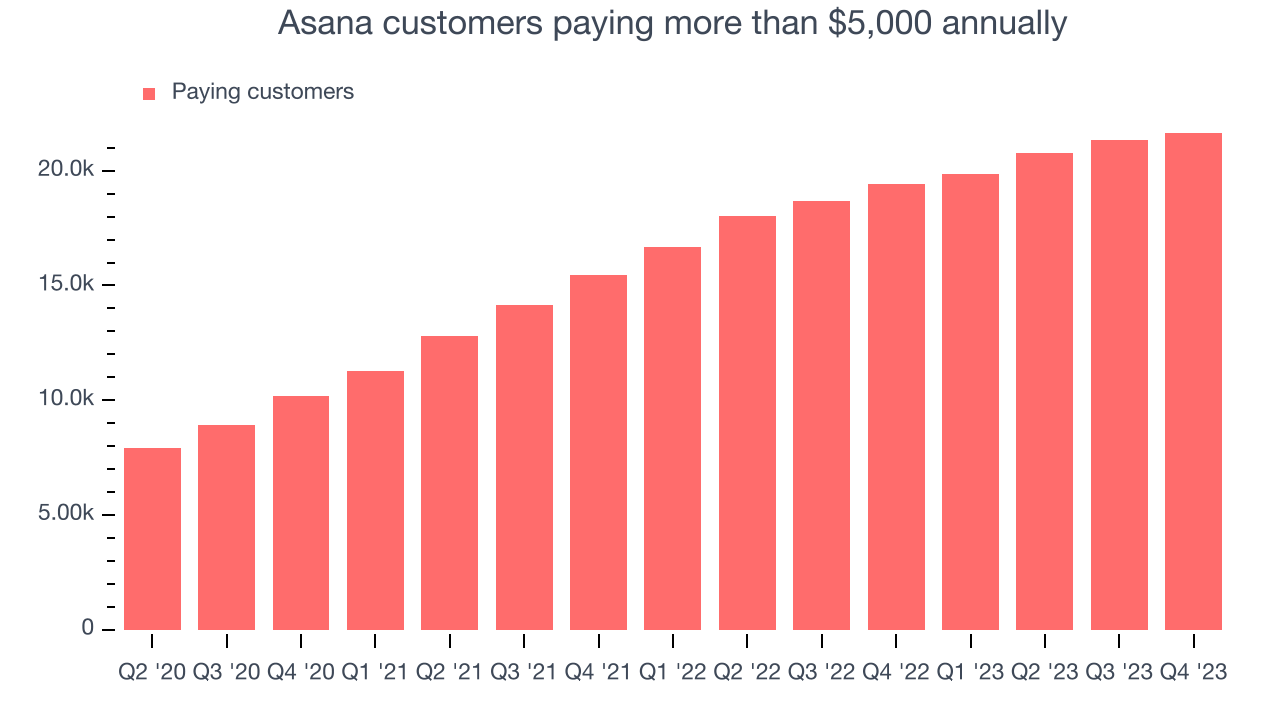

Large Customers Growth

This quarter, Asana reported 21,646 enterprise customers paying more than $5,000 annually, an increase of 300 from the previous quarter. That's a bit fewer contract wins than last quarter and quite a bit below what we've typically observed over the past four quarters, suggesting that its sales momentum with large customers is slowing.

Key Takeaways from Asana's Q4 Results

We were impressed by how strongly Asana blew past analysts' billings expectations this quarter, which led to the company narrowly outperforming Wall Street's estimates on the reported revenue line. On the other hand, while revenue guidance for next quarter the the full year was in line with expectations, Asana's guidance for operating loss for those periods was worse than expectations. Additionally, its revenue guidance for next year suggests a meaningful slowdown in growth. Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The market was likely expecting more, however, and the stock is down 3.1% after reporting, trading at $18.2 per share.

So should you invest in Asana right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.