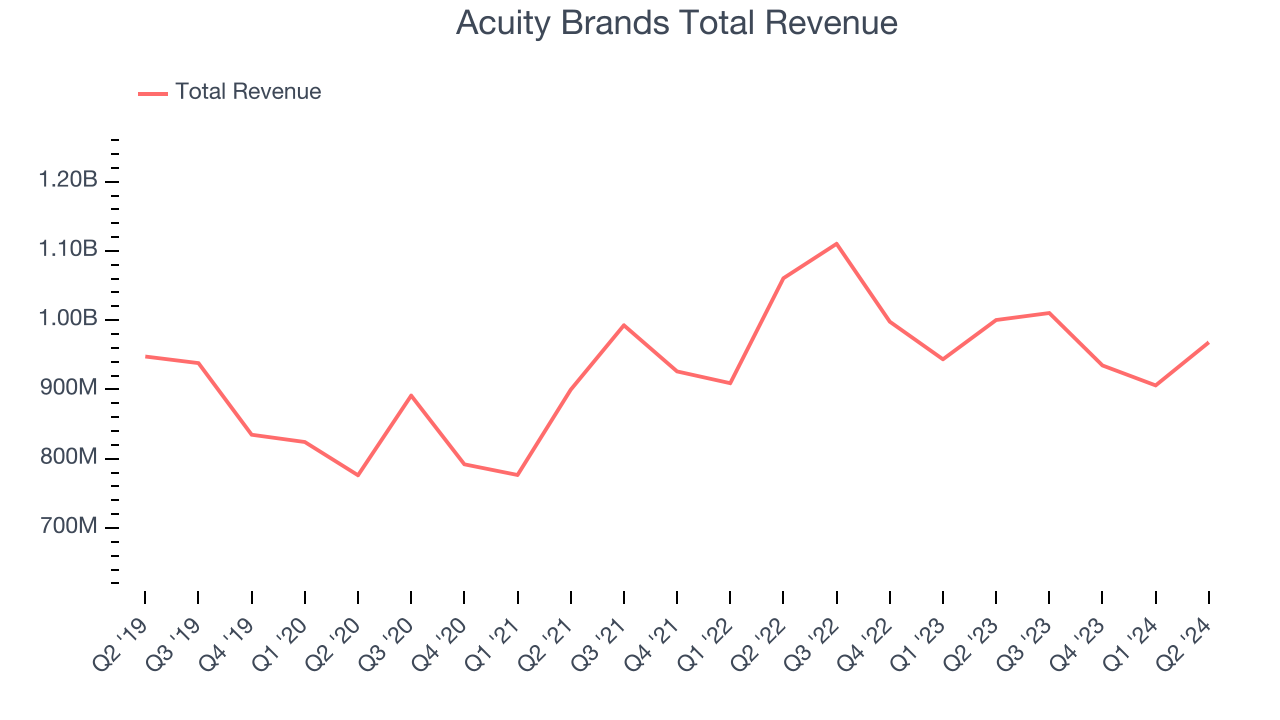

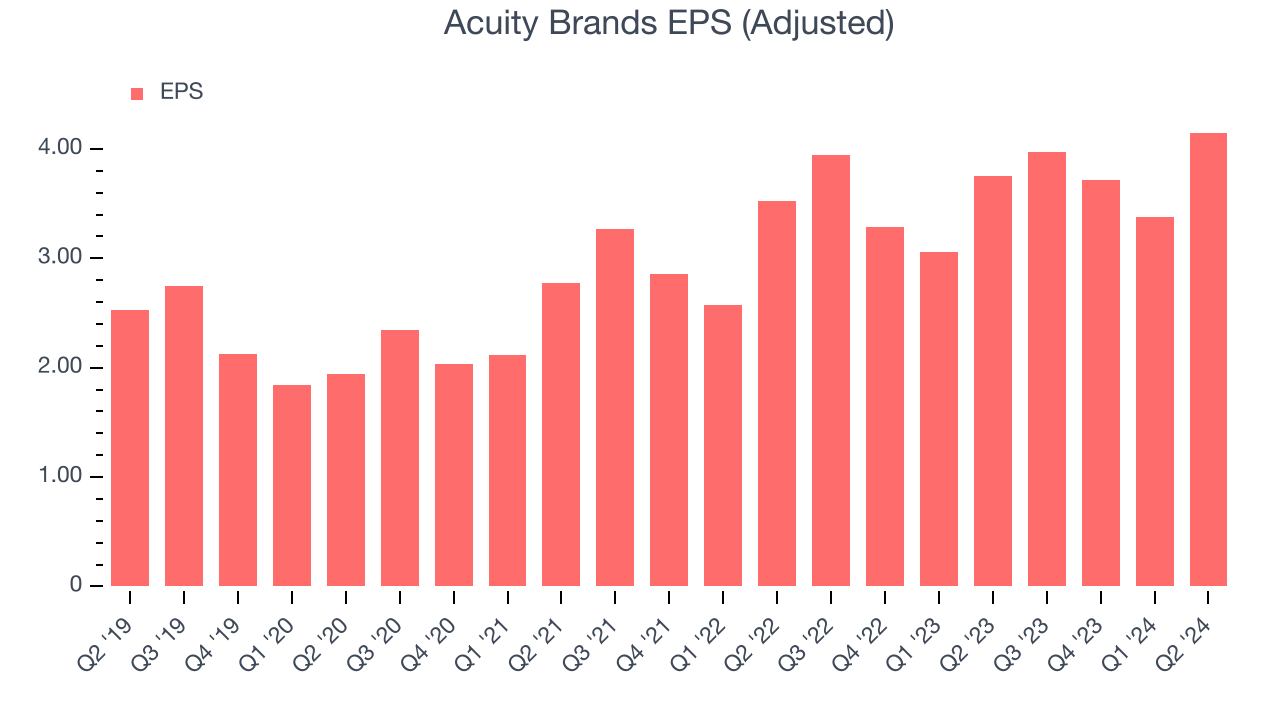

Lighting and building management solutions company Acuity (NYSE:AYI) missed analysts' expectations in Q2 CY2024, with revenue down 3.2% year on year to $968.1 million. It made a non-GAAP profit of $4.15 per share, improving from its profit of $3.75 per share in the same quarter last year.

Is now the time to buy Acuity Brands? Find out by accessing our full research report, it's free.

Acuity Brands (AYI) Q2 CY2024 Highlights:

- Revenue: $968.1 million vs analyst estimates of $996.5 million (2.9% miss)

- EPS (non-GAAP): $4.15 vs analyst estimates of $4.08 (1.6% beat)

- No forward guidance given in earnings release

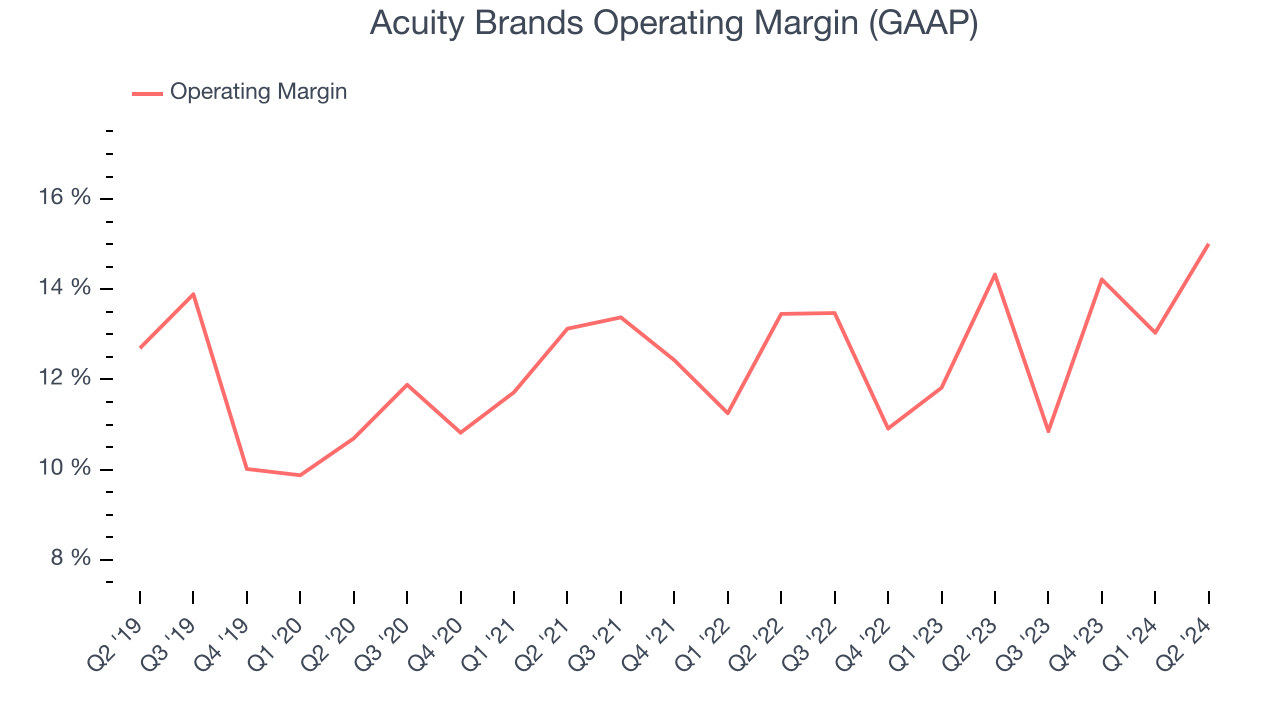

- Gross Margin (GAAP): 46.7%, up from 44.7% in the same quarter last year

- Free Cash Flow of $140.5 million, up 59.3% from the previous quarter

- Market Capitalization: $7.31 billion

“In our fiscal 2024 third quarter we delivered solid results as we continued to execute on our strategy,” stated Neil Ashe, Chairman, President and Chief Executive Officer of Acuity Brands,

One of the pioneers of smart lights, Acuity (NYSE:AYI) designs and manufactures light fixtures and building management systems used in various industries.

Electrical Systems

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one tends to sustain growth for years. Acuity Brands struggled to generate demand over the last five years as its sales were flat. This is a tough starting point for our quality assessment.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Just like its five-year trend, Acuity Brands's revenue over the last two years was flat, suggesting it is in a slump. We also note many other Electrical Systems businesses have faced declining sales because of cyclical headwinds. While Acuity Brands's growth wasn't the best, it did perform better than its peers.

This quarter, Acuity Brands missed Wall Street's estimates and reported a rather uninspiring 3.2% year-on-year revenue decline, generating $968.1 million of revenue. Looking ahead, Wall Street expects sales to grow 4.2% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

Acuity Brands has been an efficient company over the last five years. It demonstrated it can be one of the more profitable businesses in the industrials sector, boasting an average operating margin of 12.4%. This isn't surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Acuity Brands's annual operating margin rose by 2 percentage points over the last five years, showing its efficiency has improved.

This quarter, Acuity Brands generated an operating profit margin of 15%, in line with the same quarter last year. This indicates the company's cost structure has recently been stable.

EPS

We track the long-term growth in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Acuity Brands's EPS grew at a decent 9.9% compounded annual growth rate over the last five years, higher than its flat revenue. This tells us management responded to softer demand by adapting its cost structure.

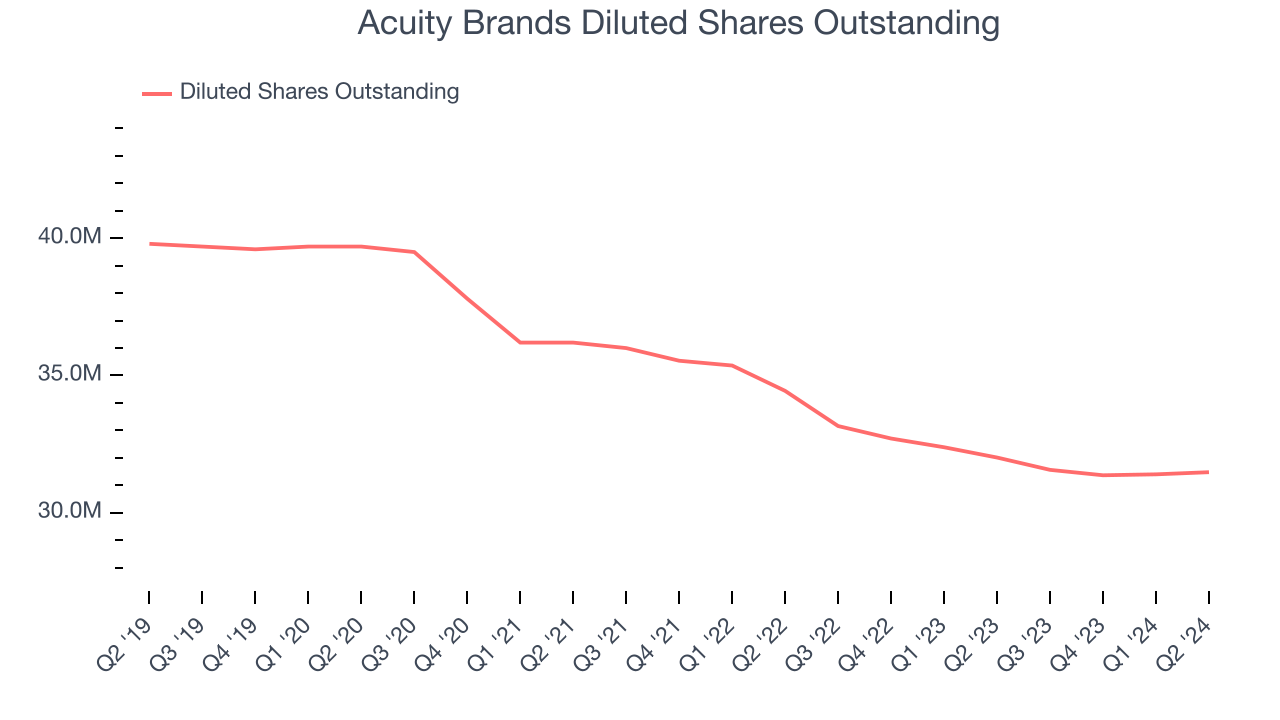

We can take a deeper look into Acuity Brands's earnings quality to better understand the drivers of its performance. As we mentioned earlier, Acuity Brands's operating margin was flat this quarter but expanded by 2 percentage points over the last five years. On top of that, its share count shrank by 20.9%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we also analyze EPS over a shorter period to see if we are missing a change in the business. For Acuity Brands, its two-year annual EPS growth of 11.6% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q2, Acuity Brands reported EPS at $4.15, up from $3.75 in the same quarter last year. This print beat analysts' estimates by 1.6%. Over the next 12 months, Wall Street expects Acuity Brands to grow its earnings. Analysts are projecting its EPS of $15.22 in the last year to climb by 4.6% to $15.92.

Key Takeaways from Acuity Brands's Q2 Results

We struggled to find many strong positives in these results. Its revenue unfortunately missed and its operating margin fell short of Wall Street's estimates. Overall, this was a bad quarter for Acuity Brands. The stock traded down 2.1% to $235 immediately following the results.

Acuity Brands may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.