Auto parts and accessories retailer AutoZone (NYSE:AZO) reported results in line with analysts' expectations in Q2 FY2024, with revenue up 4.6% year on year to $3.86 billion. It made a GAAP profit of $28.89 per share, improving from its profit of $24.64 per share in the same quarter last year.

AutoZone (AZO) Q2 FY2024 Highlights:

- Revenue: $3.86 billion vs analyst estimates of $3.85 billion (small beat)

- EPS: $28.89 vs analyst estimates of $26.62 (8.5% beat)

- Free Cash Flow of $689.5 million, up from $209.6 million in the same quarter last year

- Gross Margin (GAAP): 53.9%, up from 52.3% in the same quarter last year

- Same-Store Sales were up 3% year on year

- Store Locations: 7,191 at quarter end, increasing by 177 over the last 12 months

- Market Capitalization: $47.91 billion

Aiming to be a one-stop shop for the DIY customer, AutoZone (NYSE:AZO) is an auto parts and accessories retailer that sells everything from car batteries to windshield wiper fluid to brake pads.

While the company has a history of addressing the DIY customer’s needs, it also serves the professional mechanic. The company understands that these DIY mechanics may have varying levels of expertise in auto repair, so stores feature automotive expert sales associates who can help you find which tail light will fit your 2013 Toyota Camry SE, for example. There is also diagnostic testing to pinpoint exact issues. For the professional mechanic, Autozone offers rewards programs, commercial delivery options, and rental of specialized tools.

AutoZone stores are typically located in urban and suburban areas, with many stores situated along major roads and highways. The typical store is roughly 6,000 square feet and organized in a very logical way. Accessories such as floor mats and seat covers are usually near the entrance. Beyond that, there are sections for fluids, filters, brakes, batteries, and electrical, just to name a few.

In addition to its brick-and-mortar stores, AutoZone has an e-commerce presence that was launched in 1999. The company's website allows customers to browse and purchase products online, as well as access repair guides and instructional videos.

Auto Parts Retailer

Cars are complex machines that need maintenance and occasional repairs, and auto parts retailers cater to the professional mechanic as well as the do-it-yourself (DIY) fixer. Work on cars may entail replacing fluids, parts, or accessories, and these stores have the parts and accessories or these jobs. While e-commerce competition presents a risk, these stores have a leg up due to the combination of broad and deep selection as well as expertise provided by sales associates. Another change on the horizon could be the increasing penetration of electric vehicles.

Competitors offering auto parts and accessories include Advance Auto Parts (NYSE:AAP), O’Reilly Automotive (NASDAQ:ORLY), Genuine Parts (NYSE:GPC), and private company Pep Boys.Sales Growth

AutoZone is one of the larger companies in the consumer retail industry and benefits from economies of scale, enabling it to gain more leverage on fixed costs and offer consumers lower prices.

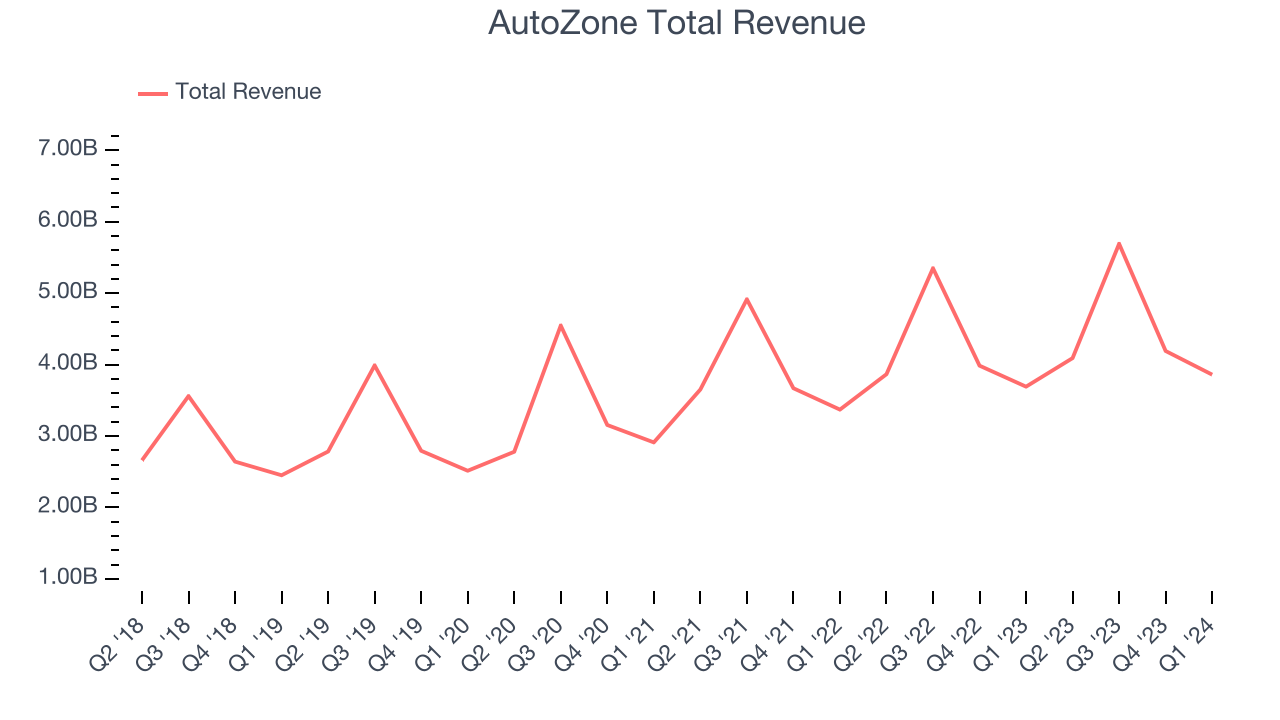

As you can see below, the company's annualized revenue growth rate of 9.5% over the last five years was steady as it opened new stores and grew sales at existing, established stores.

This quarter, AutoZone grew its revenue by 4.6% year on year, and its $3.86 billion in revenue was in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 7.3% over the next 12 months, an acceleration from this quarter.

Number of Stores

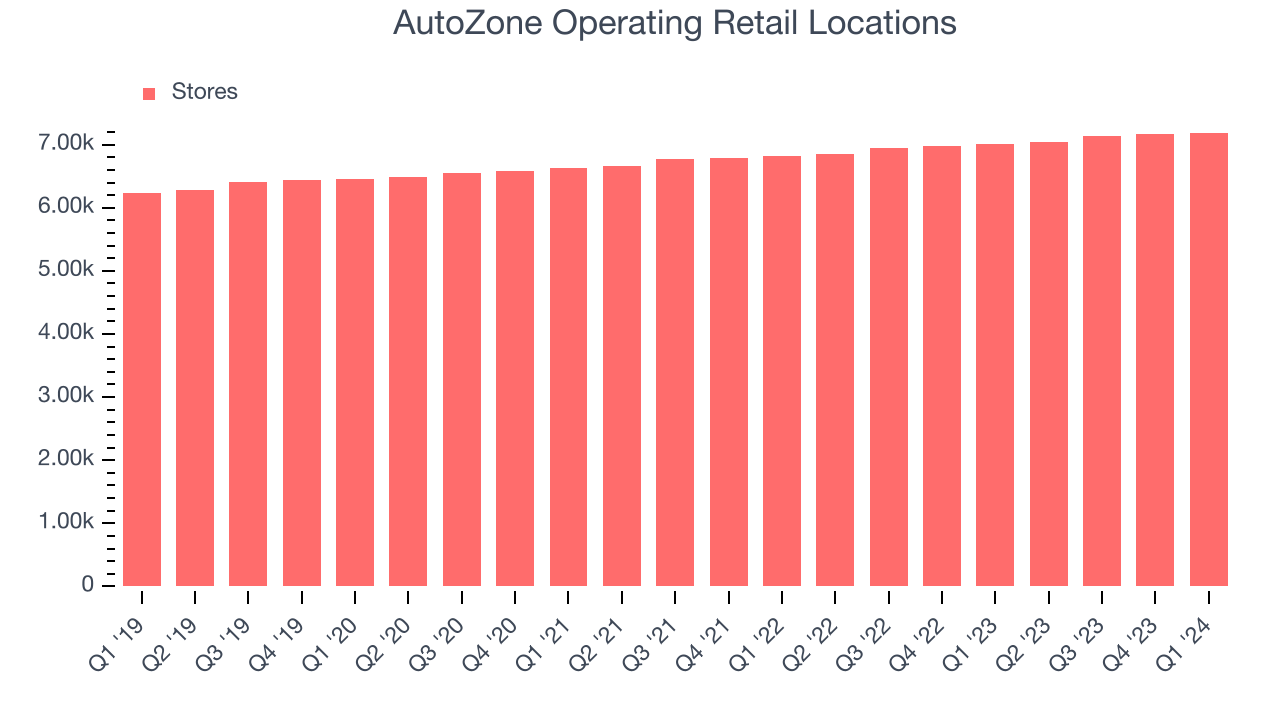

A retailer's store count often determines on how much revenue it can generate.

When a retailer like AutoZone is opening new stores, it usually means it's investing for growth because demand is greater than supply. Since last year, AutoZone's store count increased by 177 locations, or 2.5%, to 7,191 total retail locations in the most recently reported quarter.

Taking a step back, the company has generally opened new stores over the last eight quarters, averaging 2.8% annual growth in its physical footprint. This is decent store growth and in line with other retailers. With an expanding store base and demand, revenue growth can come from multiple vectors: sales from new stores, sales from e-commerce, or increased foot traffic and higher sales per customer at existing stores.

Same-Store Sales

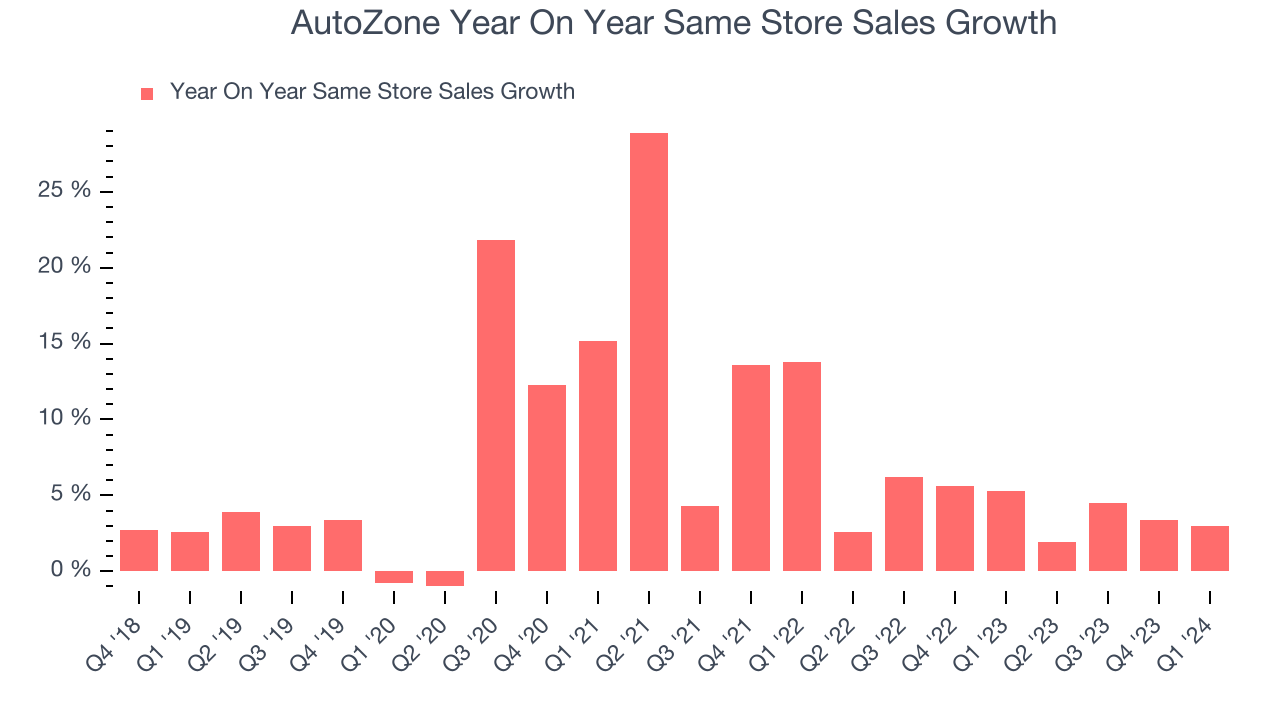

Same-store sales growth is an important metric that tracks demand for a retailer's established brick-and-mortar stores and e-commerce platform.

AutoZone's demand within its existing stores has generally risen over the last two years but lagged behind the broader consumer retail sector. On average, the company's same-store sales have grown by 4.4% year on year. With positive same-store sales growth amid an increasing physical footprint of stores, AutoZone is reaching more customers and growing sales.

In the latest quarter, AutoZone's same-store sales rose 3% year on year. This growth was a deceleration from the 5.3% year-on-year increase it posted 12 months ago, showing the business is still performing well but lost a bit of steam.

Gross Margin & Pricing Power

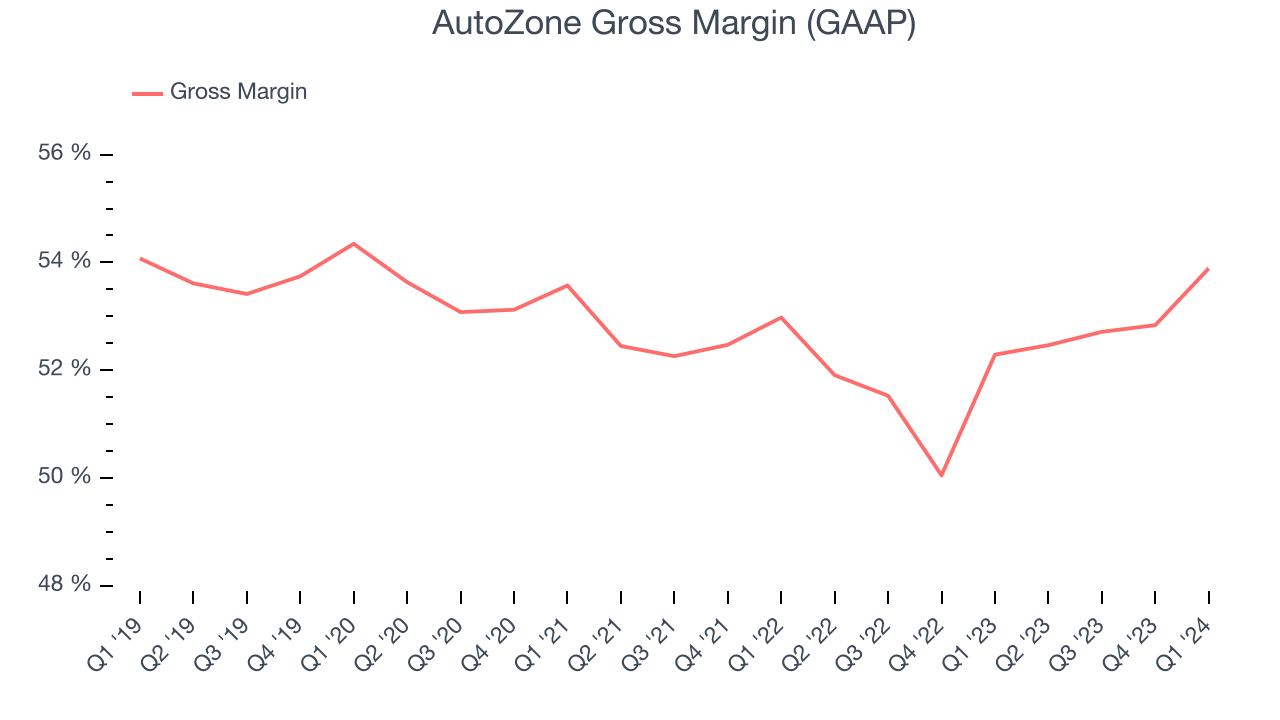

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate product differentiation, negotiating leverage, and pricing power.

AutoZone has best-in-class unit economics for a retailer, enabling it to invest in areas such as marketing and talent to stay one step ahead of the competition. As you can see below, it's averaged an exceptional 52.2% gross margin over the last two years. This means the company makes $0.52 for every $1 in revenue before accounting for its operating expenses.

AutoZone produced a 53.9% gross profit margin in Q2, marking a 1.6 percentage point increase from 52.3% in the same quarter last year. This margin expansion is a good sign in the near term. If this trend continues, it could signal a less competitive environment where the company has better pricing power, less pressure to discount products, and more stable input costs (such as distribution expenses to move goods).

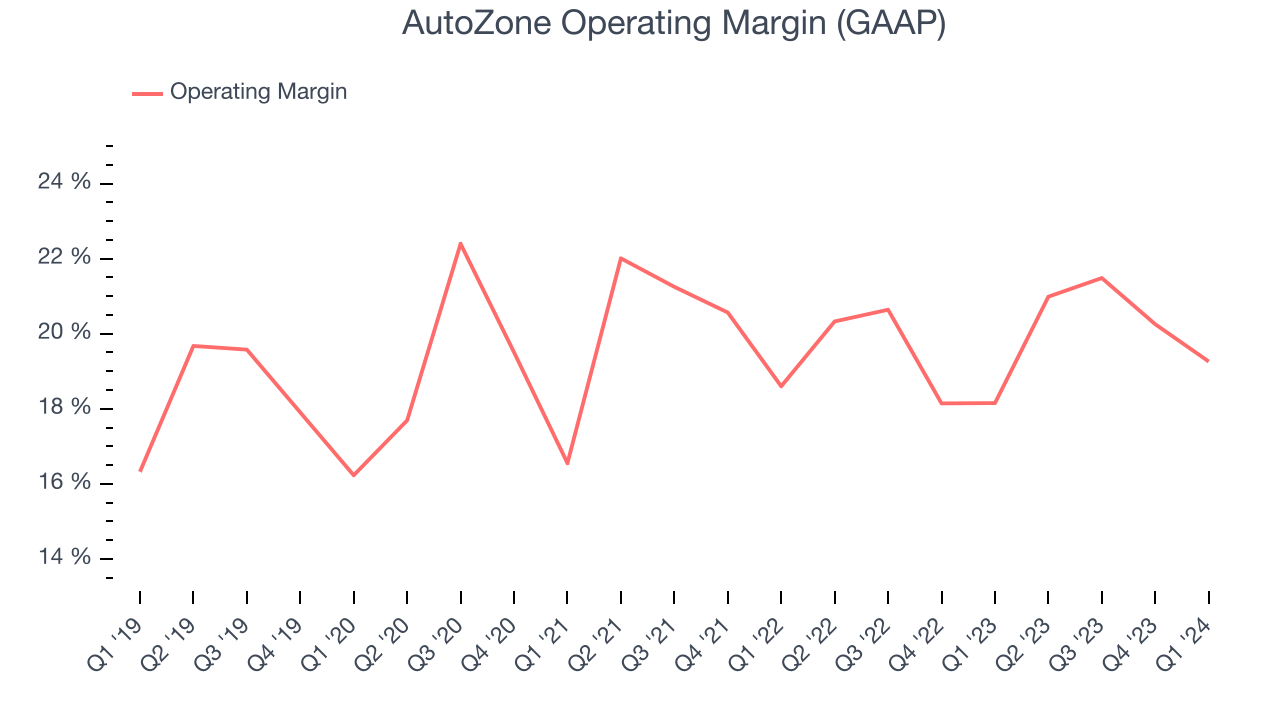

Operating Margin

Operating margin is a key profitability metric for retailers because it accounts for all expenses keeping the lights on, including wages, rent, advertising, and other administrative costs.

In Q2, AutoZone generated an operating profit margin of 19.3%, up 1.1 percentage points year on year. This increase was solid and driven by stronger pricing power, as indicated by the company's larger rise in gross margin.

Zooming out, AutoZone has been a well-managed company over the last two years. It's demonstrated elite profitability for a consumer retail business, boasting an average operating margin of 20%. On top of that, its margin has improved by 1.2 percentage points year on year (on average), an extremely encouraging sign for shareholders.

Zooming out, AutoZone has been a well-managed company over the last two years. It's demonstrated elite profitability for a consumer retail business, boasting an average operating margin of 20%. On top of that, its margin has improved by 1.2 percentage points year on year (on average), an extremely encouraging sign for shareholders. EPS

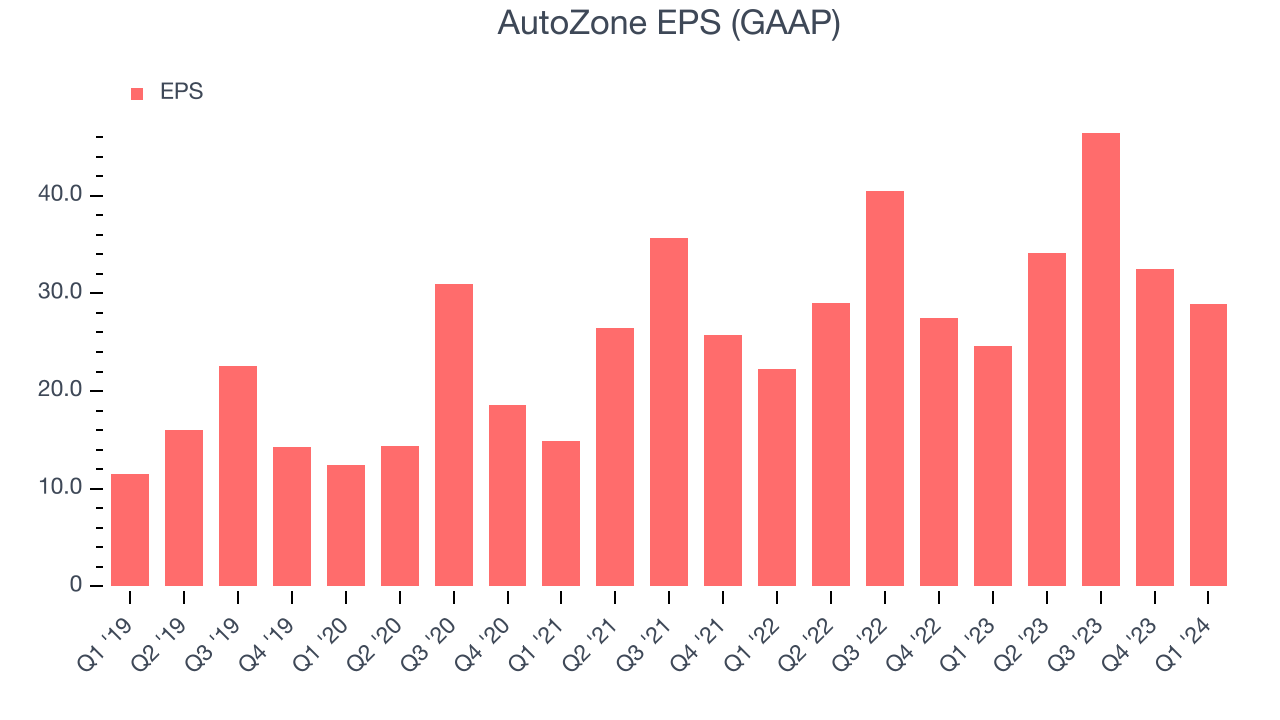

Earnings growth is a critical metric to track, but for long-term shareholders, earnings per share (EPS) is more telling because it accounts for dilution and share repurchases.

In Q2, AutoZone reported EPS at $28.89, up from $24.64 in the same quarter a year ago. This print beat Wall Street's estimates by 8.5%.

Wall Street expects the company to continue growing earnings over the next 12 months, with analysts projecting an average 10.4% year-on-year increase in EPS.

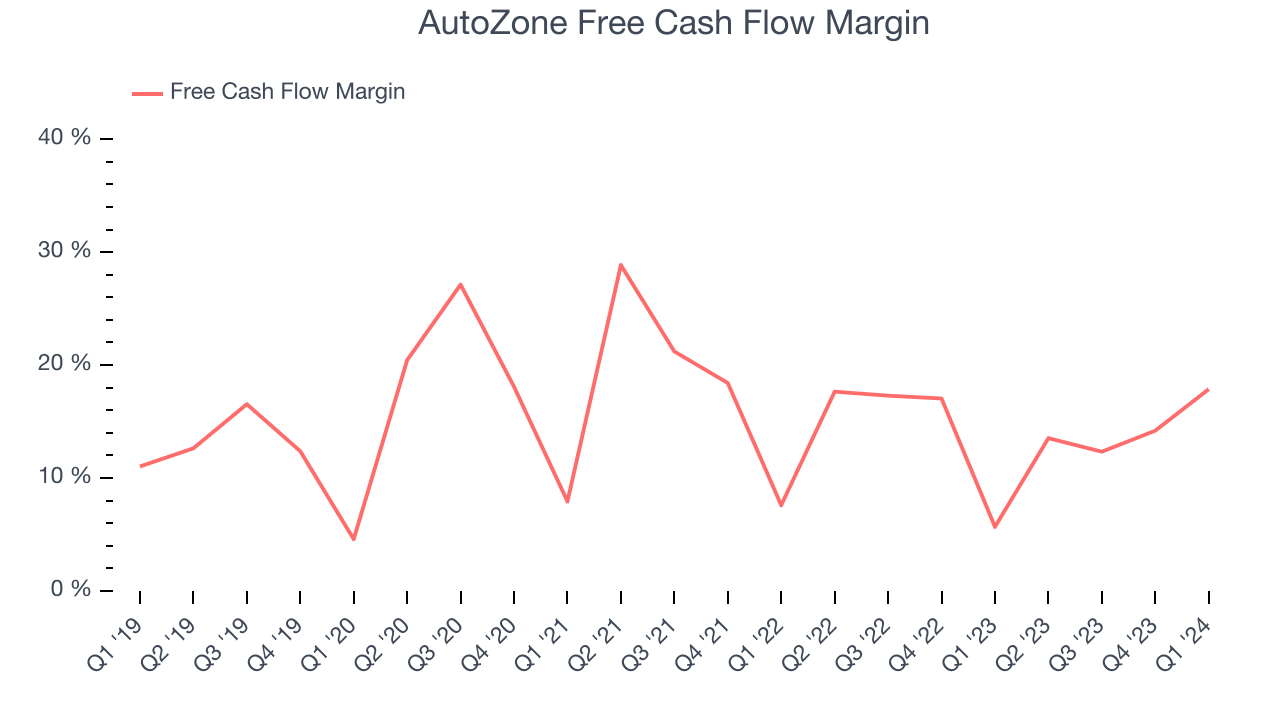

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe in the end, cash is king, and you can't use accounting profits to pay the bills.

AutoZone's free cash flow came in at $689.5 million in Q2, up 229% year on year. This result represents a 17.9% margin.

Over the last eight quarters, AutoZone has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining a robust cash balance. The company's free cash flow margin has been among the best in consumer retail, averaging 14.5%. Furthermore, its margin has been flat, showing that the company's cash flows are relatively stable.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

AutoZone's five-year average ROIC was 39.2%, placing it among the best retail companies. Just as you’d like your investment dollars to generate returns, AutoZone's invested capital has produced excellent profits.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last two years, AutoZone's ROIC averaged 9.9 percentage point increases each year. The company has historically shown the ability to generate good returns, and its rising ROIC is a great sign. It could suggest its competitive advantage or profitable business opportunities are expanding.

Key Takeaways from AutoZone's Q2 Results

It was good to see AutoZone beat analysts' gross margin expectations this quarter. We were also glad its EPS outperformed Wall Street's estimates. Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is up 2.3% after reporting and currently trades at $2,840 per share.

Is Now The Time?

AutoZone may have had a favorable quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

There are several reasons why we think AutoZone is a great business. Although its revenue growth has been mediocre over the last five years with analysts expecting growth to slow from here, its impressive gross margins are a wonderful starting point for the overall profitability of the business. On top of that, its impressive operating margins show it has a highly efficient business model.

AutoZone's price-to-earnings ratio based on the next 12 months is 17.6x. Looking at the consumer landscape today, AutoZone's qualities stand out and we still like it at this price.

Wall Street analysts covering the company had a one-year price target of $2,963 per share right before these results (compared to the current share price of $2,840), implying they saw upside in buying AutoZone in the short term.

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.