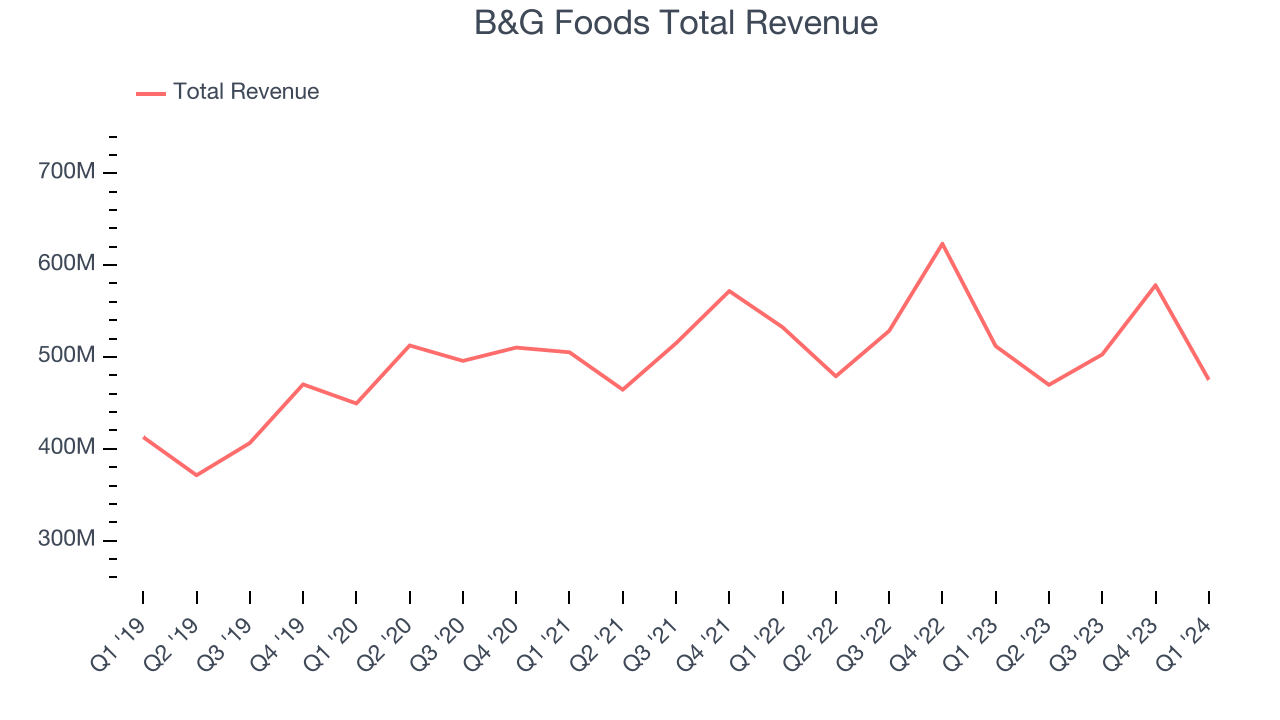

Packaged foods company B&G Foods (NYSE:BGS) fell short of analysts' expectations in Q1 CY2024, with revenue down 7.1% year on year to $475.2 million. On the other hand, the company's outlook for the full year was close to analysts' estimates with revenue guided to $1.97 billion at the midpoint. It made a non-GAAP profit of $0.18 per share, down from its profit of $0.27 per share in the same quarter last year.

Is now the time to buy B&G Foods? Find out by accessing our full research report, it's free.

B&G Foods (BGS) Q1 CY2024 Highlights:

- Revenue: $475.2 million vs analyst estimates of $482.1 million (1.4% miss)

- EPS (non-GAAP): $0.18 vs analyst expectations of $0.21 (15.4% miss)

- The company dropped its revenue guidance for the full year from $2.00 billion to $1.97 billion at the midpoint, a 1.4% decrease

- Gross Margin (GAAP): 22.9%, up from 22.5% in the same quarter last year

- Sales Volumes were down 1.4% year on year

- Market Capitalization: $896.4 million

Started as a small grocery store in New York City, B&G Foods (NYSE:BGS) is an American packaged foods company with a diverse portfolio of more than 50 brands.

Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Sales Growth

B&G Foods carries some recognizable brands and products but is a mid-sized consumer staples company. Its size could bring disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the other hand, B&G Foods can still achieve high growth rates because its revenue base is not yet monstrous.

As you can see below, the company's revenue was flat over the last three years. This is poor for a consumer staples business.

This quarter, B&G Foods missed Wall Street's estimates and reported a rather uninspiring 7.1% year-on-year revenue decline, generating $475.2 million in revenue. Looking ahead, Wall Street expects revenue to decline 1.8% over the next 12 months.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

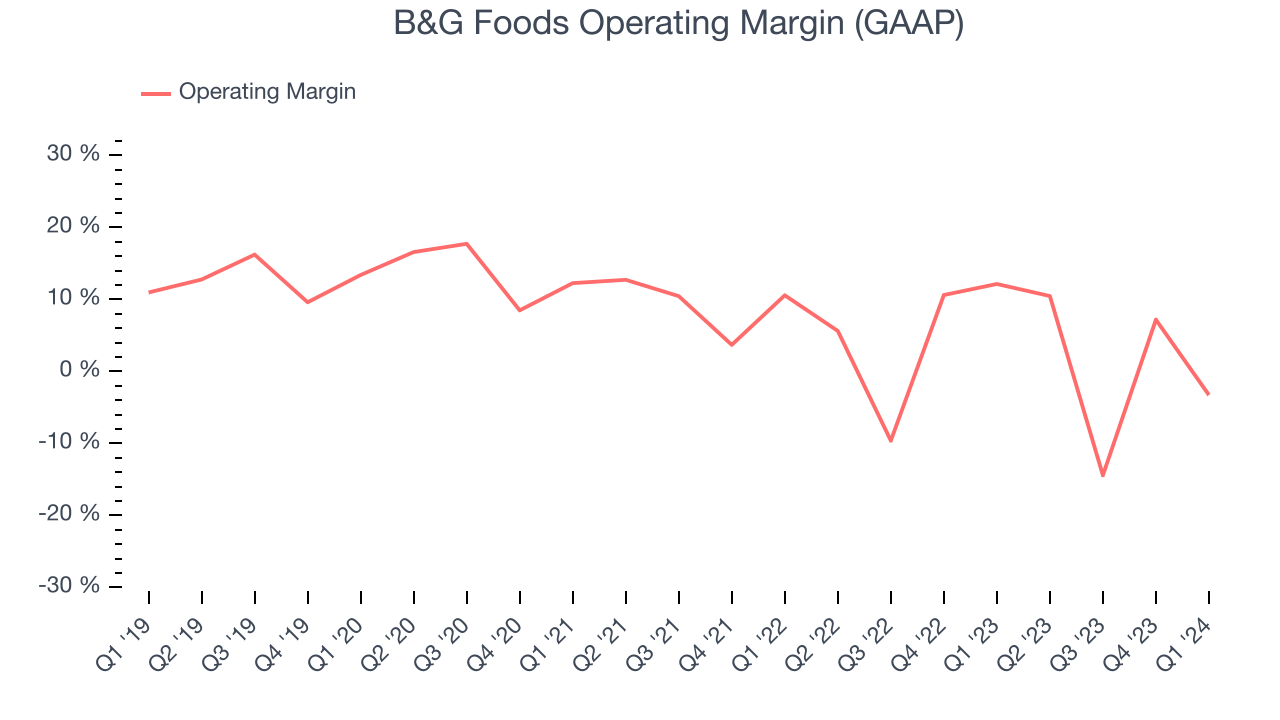

Operating Margin

Operating margin is an important measure of profitability accounting for key expenses such as marketing and advertising, IT systems, wages, and other administrative costs.

This quarter, B&G Foods generated an operating profit margin of negative 3.3%, down 15.4 percentage points year on year. Conversely, the company's gross margin actually increased, so we can assume the reduction was driven by operational inefficiencies and a step up in discretionary spending in areas like corporate overhead and advertising.

Zooming out, B&G Foods was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer staples business, producing an average operating margin of 2.6%. On top of that, B&G Foods's margin has declined by 4.7 percentage points on average over the last year. This shows the company is heading in the wrong direction, and investors are likely hoping for better results in the future.

Zooming out, B&G Foods was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer staples business, producing an average operating margin of 2.6%. On top of that, B&G Foods's margin has declined by 4.7 percentage points on average over the last year. This shows the company is heading in the wrong direction, and investors are likely hoping for better results in the future.Key Takeaways from B&G Foods's Q1 Results

It was encouraging to see B&G Foods slightly top analysts' gross margin expectations this quarter. On the other hand, its revenue, operating margin, and EPS missed Wall Street's estimates as its sales volumes declined 1.4% year on year. Overall, the results could have been better. The company is down 7.4% on the results and currently trades at $10.7 per share.

B&G Foods may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.