Discount retail company Big Lots (NYSE:BIG) reported results in line with analysts' expectations in Q4 FY2023, with revenue down 7.2% year on year to $1.43 billion. It made a non-GAAP loss of $0.28 per share, improving from its loss of $0.28 per share in the same quarter last year.

Big Lots (BIG) Q4 FY2023 Highlights:

- Revenue: $1.43 billion vs analyst estimates of $1.43 billion (small beat)

- EPS (non-GAAP): -$0.28 vs analyst estimates of -$0.26

- Gross Margin (GAAP): 38%, up from 36.3% in the same quarter last year

- Same-Store Sales were down 8.6% year on year

- Store Locations: 1,300 at quarter end, decreasing by 125 over the last 12 months

- Market Capitalization: $147 million

Priding itself on carrying brand-name items, Big Lots (NYSE:BIG) is a discount retailer that acquires excess inventory and then sells at meaningful discounts to the prices of traditional retailers.

For example, if Target orders large quantities of Martha Stewart Living bath towels that don’t sell as well as expected, Target may sell those in bulk to Big Lots at pennies on the dollar rather than discount the items and try to sell them individually. This is often done to clear shelf space for new products or because of restrictions on discounting certain brands.

Big Lots’s buying approach focuses on finding excess inventory or overstocked items from other retailers, so selection can change and be varied. Shopping at Big Lots is often a treasure hunt–what the consumer loses in reliable selection is made up for with low prices. Housewares and home decor, snacks, toys and games, and furniture are key product categories at the typical Big Lots store, and brands such as Serta, Whirlpool, Kraft, Nestle, and Sony can often be found there.

The core customer is the middle class, value-conscious shopper who values a one-stop shop for most of a household’s needs but is ok with changing selection. The typical Big Lots store is mid-sized, averaging 30,000 square feet and located in suburban or urban areas shopping centers.

Discount General Merchandise Retailer

Broadline discount retailers understand that many shoppers love a good deal, and they focus on providing excellent value to shoppers by selling general merchandise at major discounts. They can do this because of unique purchasing, procurement, and pricing strategies that involve scouring the market for trendy goods or buying excess inventory from manufacturers and other retailers. They then turn around and sell these snacks, paper towels, toys, and myriad other products at highly enticing prices. Despite the unique draw and lure of discounts, these discount retailers must also contend with the secular headwinds of online shopping and challenged retail foot traffic in places like suburban strip malls.

Discount retail competitors include TJX (NYSE:TJX), Ollie’s Bargain Outlet (NASDAQ:OLLI), and Ross Stores (NASDAQ:ROST).Sales Growth

Big Lots is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the other hand, it has an edge over smaller competitors with fewer resources and can still flex high growth rates because it's growing off a smaller base than its larger counterparts.

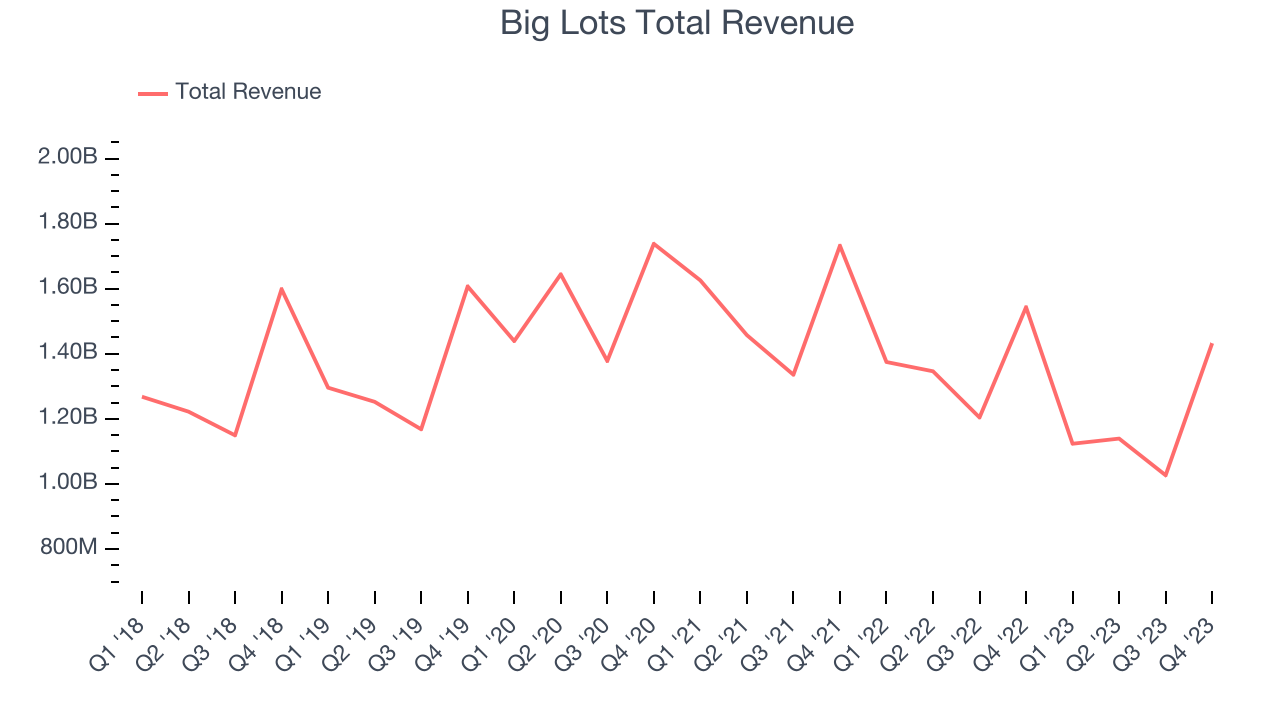

As you can see below, the company's revenue has declined over the last four years, dropping 3% annually as its store count and sales at existing, established stores have both shrunk.

This quarter, Big Lots reported a rather uninspiring 7.2% year-on-year revenue decline to $1.43 billion in revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects revenue to decline 5.3% over the next 12 months.

Number of Stores

When a retailer like Big Lots keeps its store footprint steady, it usually means that demand is stable and it's focused on improving operational efficiency to increase profitability. Big Lots's store count shrank by 125 locations, or 8.8%, over the last 12 months to 1,300 total retail locations in the most recently reported quarter.

Taking a step back, the company has kept its physical footprint more or less flat over the last two years while other consumer retail businesses have opted for growth. A flat store base means that revenue growth must come from increased e-commerce sales or higher foot traffic and sales per customer at existing stores.

Same-Store Sales

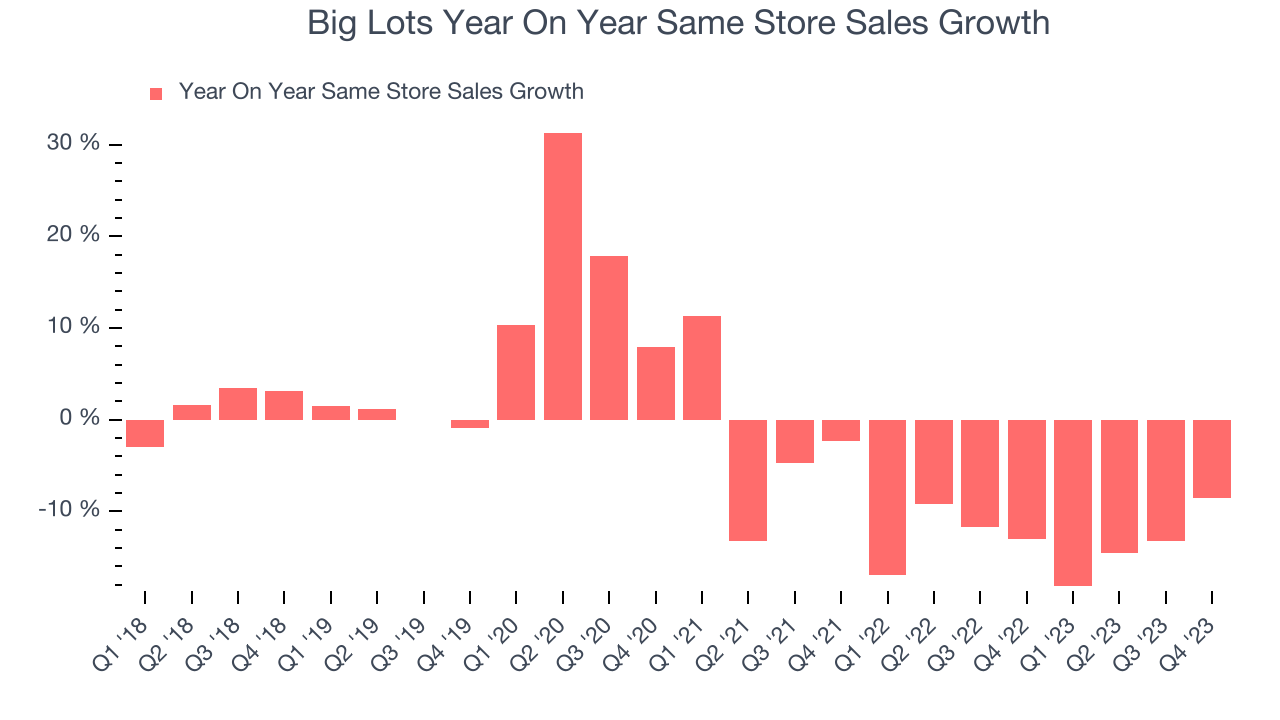

A company's same-store sales growth shows the year-on-year change in sales for its brick-and-mortar stores that have been open for at least a year, give or take, and e-commerce platform. This is a key performance indicator for retailers because it measures organic growth and demand.

Big Lots's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 13.2% year on year. The company has been reducing its store count as fewer locations sometimes lead to higher same-store sales, but that hasn't been the case here.

In the latest quarter, Big Lots's same-store sales fell 8.6% year on year. This decrease was a further deceleration from the 13% year-on-year decline it posted 12 months ago. We hope the business can get back on track.

Gross Margin & Pricing Power

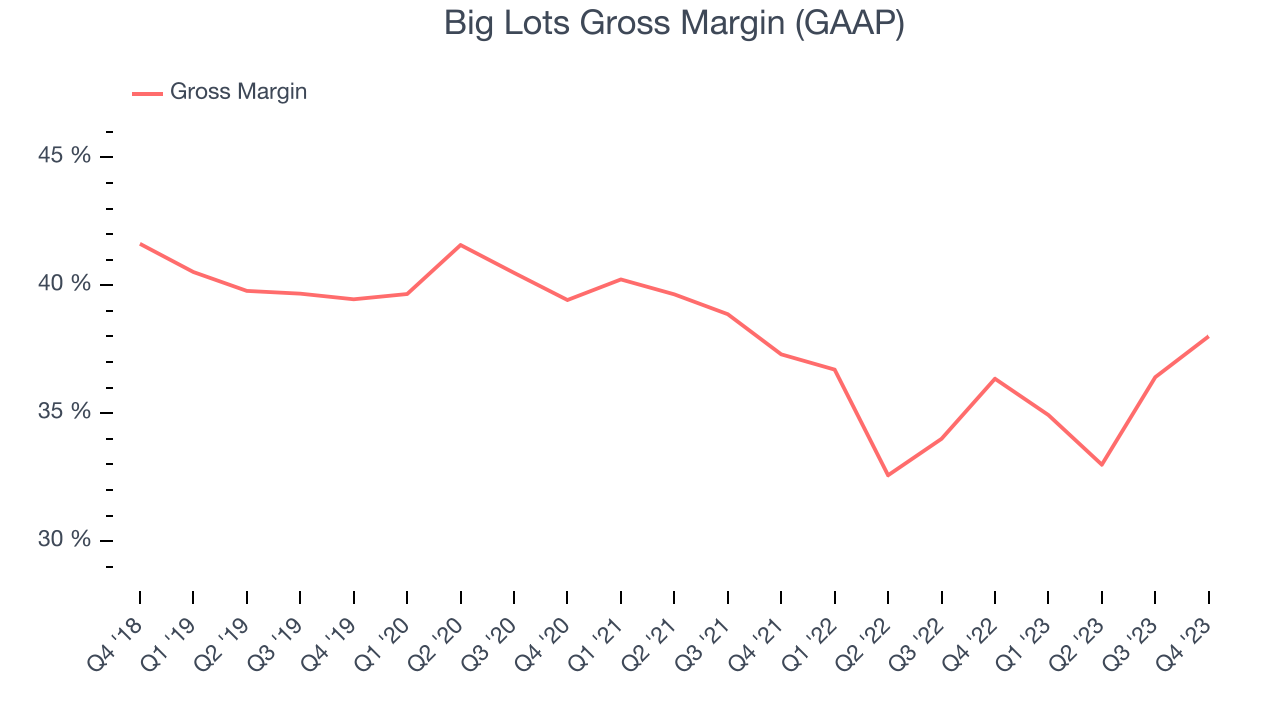

Big Lots's unit economics are higher than the typical retailer, giving it the flexibility to invest in areas such as marketing and talent to reach more consumers. As you can see below, it's averaged a decent 35.3% gross margin over the last eight quarters. This means the company makes $0.35 for every $1 in revenue before accounting for its operating expenses.

Big Lots's gross profit margin came in at 38% this quarter, marking a 1.7 percentage point increase from 36.3% in the same quarter last year. This margin expansion is a good sign in the near term. If this trend continues, it could signal a less competitive environment where the company has better pricing power, less pressure to discount products, and more stable input costs (such as distribution expenses to move goods).

Operating Margin

Operating margin is a key profitability metric for retailers because it accounts for all expenses keeping the lights on, including wages, rent, advertising, and other administrative costs.

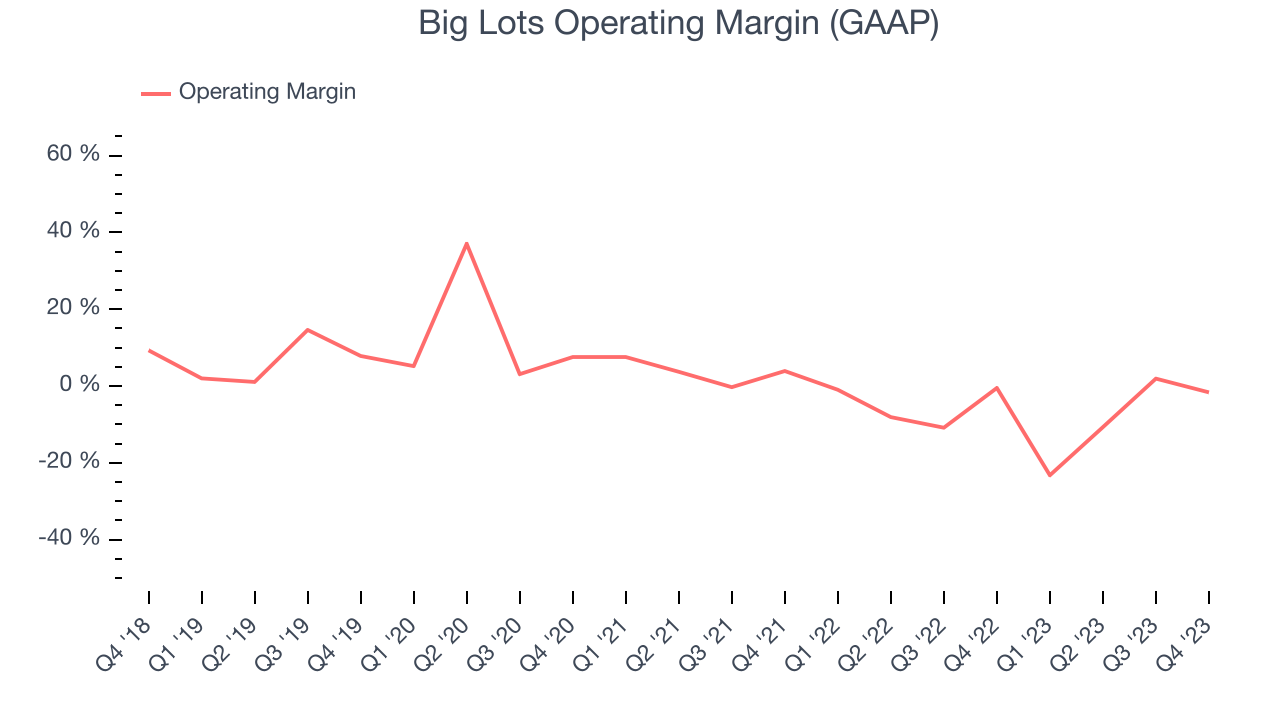

This quarter, Big Lots generated an operating profit margin of negative 1.7%, down 1.1 percentage points year on year. Conversely, the company's gross margin actually increased, so we can assume the reduction was driven by weaker cost controls or operating leverage on fixed costs.

Unprofitable publicly traded companies are few and far between in the consumer retail sector, and over the last two years, Big Lots has been one of them. Its high expenses have contributed to an average operating margin of negative 6.4%. On top of that, Big Lots's margin has declined, on average, by 3.4 percentage points year on year. This shows the company is heading in the wrong direction, and investors were likely hoping for better results.

Unprofitable publicly traded companies are few and far between in the consumer retail sector, and over the last two years, Big Lots has been one of them. Its high expenses have contributed to an average operating margin of negative 6.4%. On top of that, Big Lots's margin has declined, on average, by 3.4 percentage points year on year. This shows the company is heading in the wrong direction, and investors were likely hoping for better results.EPS

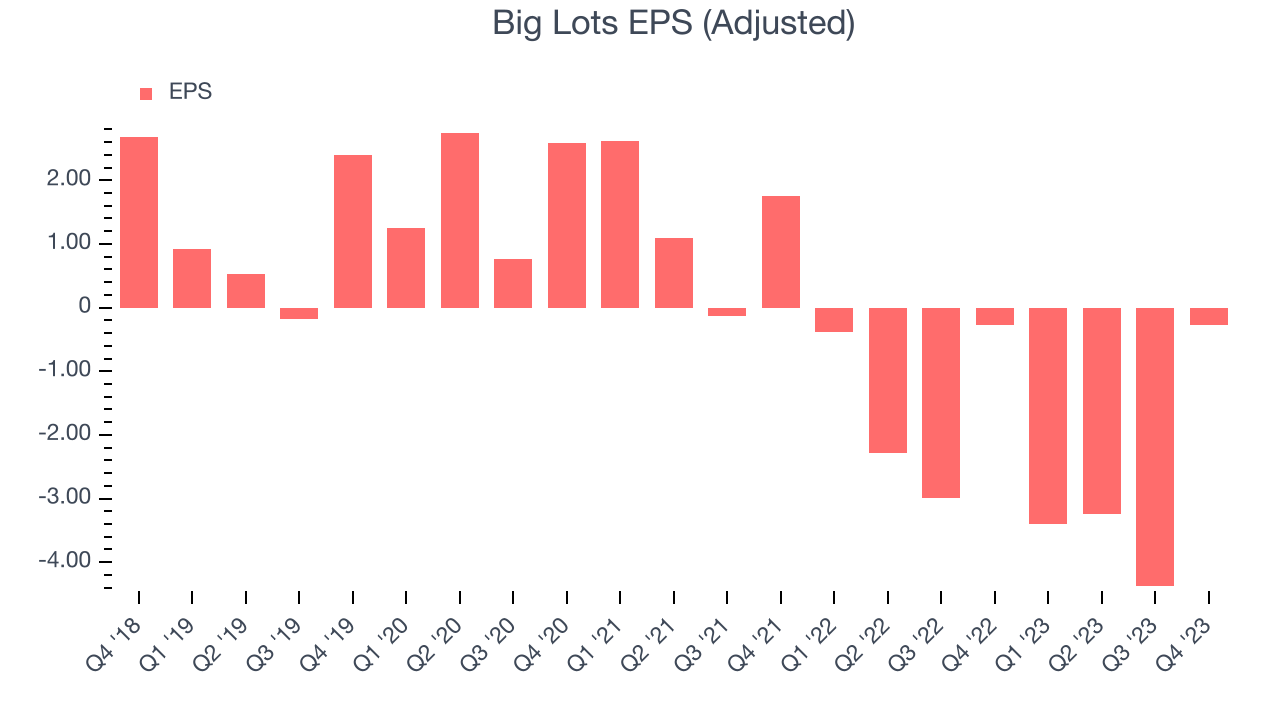

These days, some companies issue new shares like there's no tomorrow. That's why we like to track earnings per share (EPS) because it accounts for shareholder dilution and share buybacks.

In Q4, Big Lots reported EPS at negative $0.28, up from negative $0.28 in the same quarter a year ago. This print unfortunately missed Wall Street's estimates, but we care more about long-term EPS growth rather than short-term movements.

Between FY2019 and FY2023, Big Lots's adjusted diluted EPS dropped 93.8%, translating into 50.2% annualized declines. In a mature sector such as consumer retail, we tend to steer our readers away from companies with falling EPS. If there's no earnings growth, it's difficult to build confidence in a business's underlying fundamentals, leaving a low margin of safety around the company's valuation (making the stock susceptible to large downward swings).

On the bright side, Wall Street expects the company's earnings to grow over the next 12 months, with analysts projecting an average 28.5% year-on-year increase in EPS.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Big Lots's five-year average ROIC was 4.5%, somewhat low compared to the best retail companies that consistently pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Big Lots's ROIC over the last two years averaged 30.9 percentage point decreases each year. In conjunction with its already low returns, these declines suggest the company's profitable business opportunities are few and far between.

Key Takeaways from Big Lots's Q4 Results

It was encouraging to see Big Lots narrowly top analysts' revenue expectations this quarter. On the other hand, its EPS missed analysts' expectations. Overall, this was a mediocre quarter for Big Lots. The stock is flat after reporting and currently trades at $4.99 per share.

Is Now The Time?

When considering an investment in Big Lots, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We cheer for all companies serving consumers, but in the case of Big Lots, we'll be cheering from the sidelines. Its revenue has declined over the last four years, and analysts expect growth to deteriorate from here. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its declining EPS over the last four years makes it hard to trust. On top of that, its relatively low ROIC suggests it has struggled to grow profits historically.

While we've no doubt one can find things to like about Big Lots, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $4.30 per share right before these results (compared to the current share price of $4.99), implying they didn't see much short-term potential in Big Lots.

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.