Payments and billing software maker Bill.com (NYSE:BILL) announced better-than-expected results in Q1 CY2024, with revenue up 18.5% year on year to $323 million. On top of that, next quarter's revenue guidance ($325 million at the midpoint) was surprisingly good and 3.3% above what analysts were expecting. It made a non-GAAP profit of $0.60 per share, improving from its profit of $0.50 per share in the same quarter last year.

Bill.com (BILL) Q1 CY2024 Highlights:

- Revenue: $323 million vs analyst estimates of $306 million (5.6% beat)

- EPS (non-GAAP): $0.60 vs analyst estimates of $0.54 (12.1% beat)

- Revenue Guidance for Q2 CY2024 is $325 million at the midpoint, above analyst estimates of $314.5 million

- Gross Margin (GAAP): 83%, down from 86.1% in the same quarter last year

- Free Cash Flow of $62.96 million, down 15.2% from the previous quarter

- Market Capitalization: $6.60 billion

Started by René Lacerte in 2006 after selling his previous payroll and accounting software company PayCycle to Intuit, Bill.com (NYSE:BILL) is a software as a service platform that aims to make payments and billing processes easier for small and medium-sized businesses.

The software offers a central cloud repository for invoices and provides an interface where its users can issue, process, approve and pay invoices in an easy to use environment. By automating a lot of previously laborious manual work, Bill.com brings down the cost of running the accounts receivable/payable department. The company charges its customers software subscription and also processing fees on the payments they make through the platform.

Finance and Accounting Software

Finance and accounting software benefits from dual trends around costs savings and ease of use. First is the SaaS-ification of businesses, large and small, who much prefer the flexibility of cloud-based, web-browser delivered software paid for on a subscription basis than the hassle and expense of purchasing and managing on-premise enterprise software. Second is the consumerization of business software, whereby multiple standalone processes like supply chain and tax management are aggregated into a single, easy to use platforms.

Today, Bill.com is mainly competing with legacy manual processes and software companies like SAP (NYSE:SAP) that primarily focus on large enterprises.

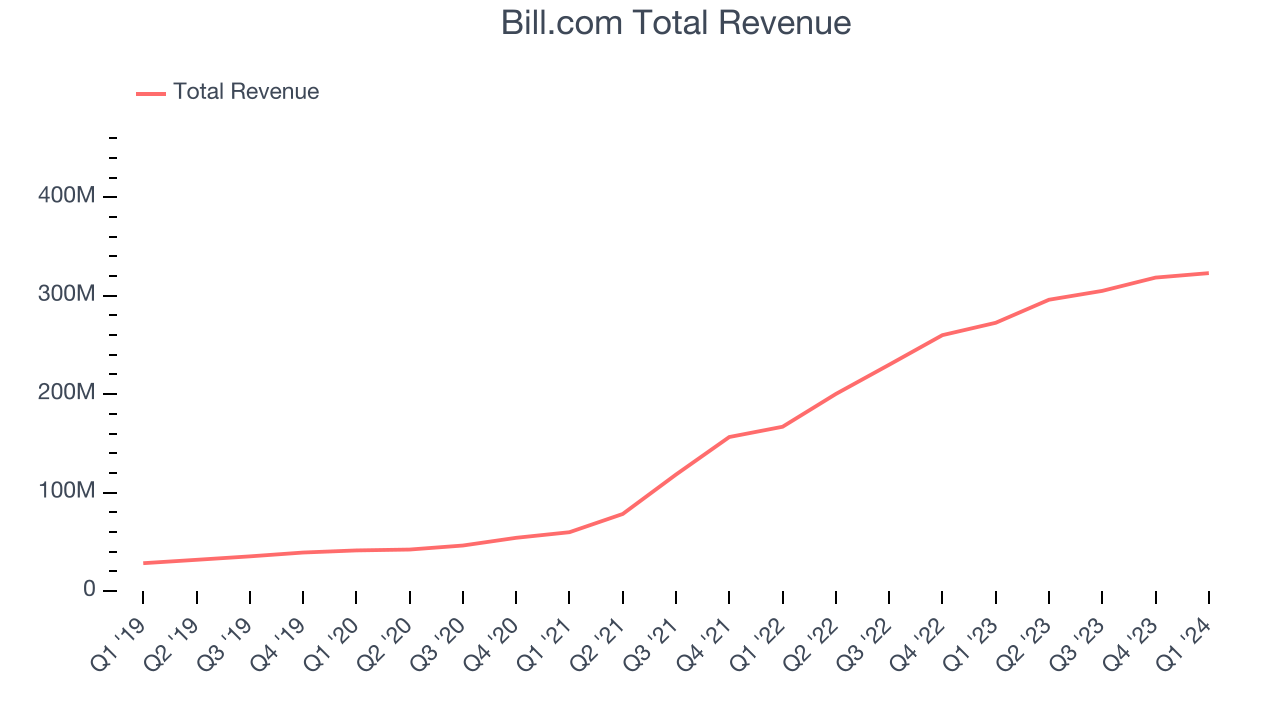

Sales Growth

As you can see below, Bill.com's revenue growth has been incredible over the last three years, growing from $59.74 million in Q3 2021 to $323 million this quarter.

This quarter, Bill.com's quarterly revenue was once again up 18.5% year on year. However, its growth did slow down compared to last quarter as the company's revenue increased by just $4.53 million in Q1 compared to $13.51 million in Q4 CY2023. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Next quarter's guidance suggests that Bill.com is expecting revenue to grow 9.8% year on year to $325 million, slowing down from the 47.8% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 9.1% over the next 12 months before the earnings results announcement.

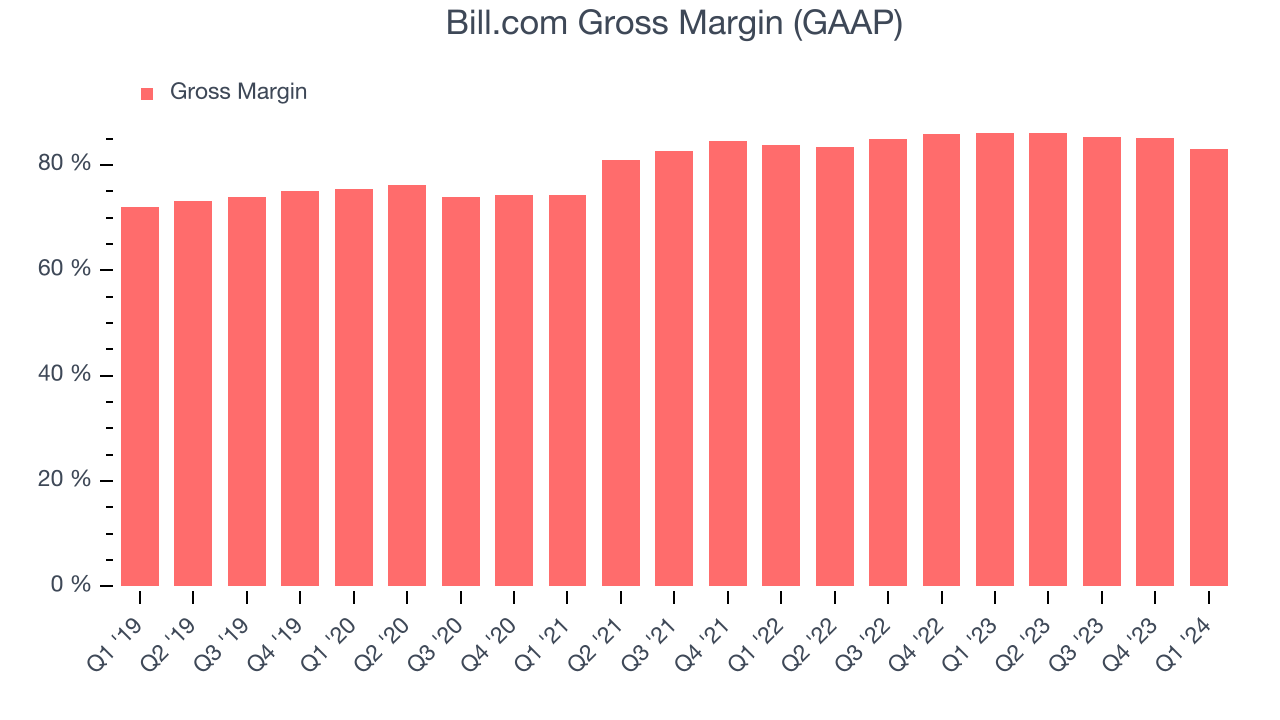

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Bill.com's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 83% in Q1.

That means that for every $1 in revenue the company had $0.83 left to spend on developing new products, sales and marketing, and general administrative overhead. Despite its decline over the last year, Bill.com's excellent gross margin allows it to fund large investments in product and sales during periods of rapid growth and achieve profitability when reaching maturity.

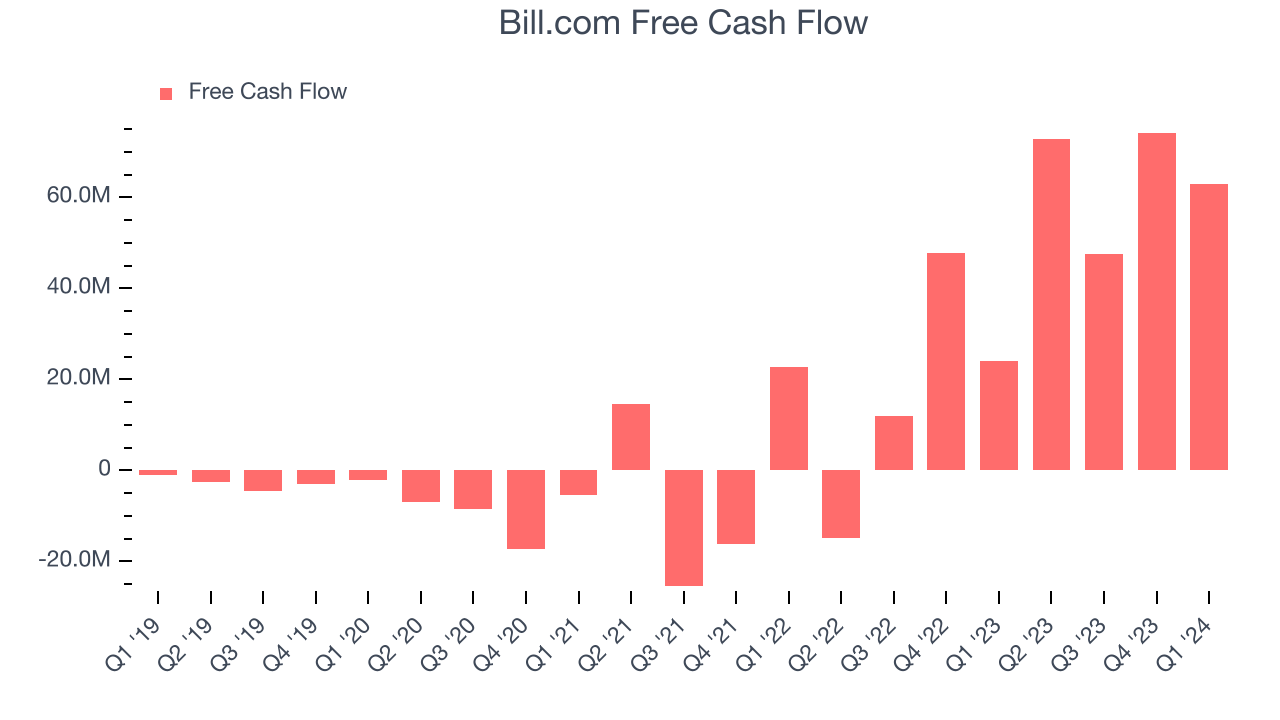

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Bill.com's free cash flow came in at $62.96 million in Q1, up 163% year on year.

Bill.com has generated $257.7 million in free cash flow over the last 12 months, an impressive 20.7% of revenue. This high FCF margin stems from its asset-lite business model and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a cash cushion.

Key Takeaways from Bill.com's Q1 Results

We enjoyed seeing Bill.com exceed analysts' revenue expectations this quarter. We were also glad next quarter's revenue guidance came in higher than Wall Street's estimates. On the other hand, its gross margin declined. Overall, we think this was a really good quarter that should please shareholders. Investors were likely expecting more, however, and the stock is down 2% after reporting, trading at $62 per share.

Is Now The Time?

When considering an investment in Bill.com, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We think Bill.com is a good business. We'd expect growth rates to moderate from here, but its revenue growth has been exceptional over the last three years. On top of that, its impressive gross margins indicate excellent business economics and its bountiful generation of free cash flow empowers it to invest in growth initiatives.

Given its price-to-sales ratio of 5.2x based on the next 12 months, the market is certainly expecting long-term growth from Bill.com. There are definitely a lot of things to like about Bill.com, and looking at the tech landscape right now, it seems to be trading at a pretty compelling price.

Wall Street analysts covering the company had a one-year price target of $84.68 right before these results (compared to the current share price of $62), implying they see short-term upside potential in Bill.com.

To get the best start with StockStory, check out our most recent Stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released. Especially for companies reporting pre-market, this often gives investors the chance to react to the results before everyone else has fully absorbed the information.