Clothing and footwear retailer Boot Barn (NYSE:BOOT) fell short of analysts' expectations in Q3 FY2024, with revenue up 1.1% year on year to $520.4 million. Next quarter's revenue guidance of $381 million also underwhelmed, coming in 4.9% below analysts' estimates. It made a GAAP profit of $1.81 per share, improving from its profit of $1.74 per share in the same quarter last year.

Is now the time to buy Boot Barn? Find out by accessing our full research report, it's free.

Boot Barn (BOOT) Q3 FY2024 Highlights:

- Market Capitalization: $2.24 billion

- Revenue: $520.4 million vs analyst estimates of $528 million (1.4% miss)

- EPS: $1.81 vs analyst estimates of $1.79 (1.1% beat)

- Revenue Guidance for Q4 2024 is $381 million at the midpoint, below analyst estimates of $400.5 million (EPS guidance also below)

- Revenue Guidance for full year 2024 is $1.659 billion at the midpoint, below analyst estimates of $1.680 billion (EPS guidance also below)

- Free Cash Flow of $68.39 million, down 42.3% from the same quarter last year

- Gross Margin (GAAP): 38.3%, up from 36.5% in the same quarter last year

- Same-Store Sales were down 9.7% year on year

- Store Locations: 382 at quarter end, increasing by 49 over the last 12 months

Jim Conroy, President and Chief Executive Officer, commented “I am pleased with our third quarter performance. We added 11 new stores and were able to maintain our consistent track record of delivering growth. Excluding three quarters in calendar 2020 that were impacted by the pandemic, the third quarter marks our 38th consecutive quarter of year-over-year sales growth since our IPO in 2014, nearly ten years ago. Our top line was driven by the sales from the 49 new stores opened over the past 12 months, which more than offset a 9.7% decline in same store sales. We also grew earnings compared to last year through a combination of sales growth, disciplined expense control and an increase in merchandise margin, which benefited from improved freight. These results underscore the strength of the Boot Barn business model and are a testament to solid execution across the organization.”

With a strong store presence in Texas, California, Florida, and Oklahoma, Boot Barn (NYSE:BOOT) is a western-inspired apparel and footwear retailer.

Footwear Retailer

Footwear sales–like their apparel counterparts–are driven by seasons, trends, and innovation more so than absolute need and similarly face the bigger-picture secular trend of e-commerce penetration. Footwear plays a part in societal belonging, personal expression, and occasion, and retailers selling shoes recognize this. Therefore, they aim to balance selection, competitive prices, and the latest trends to attract consumers. Unlike their apparel counterparts, footwear retailers most sell popular third-party brands (as opposed to their own exclusive brands), which could mean less exclusivity of product but more nimbleness to pivot to what’s hot.

Sales Growth

Boot Barn is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale. On the other hand, one advantage is that its growth rates can be higher because it's growing off a small base.

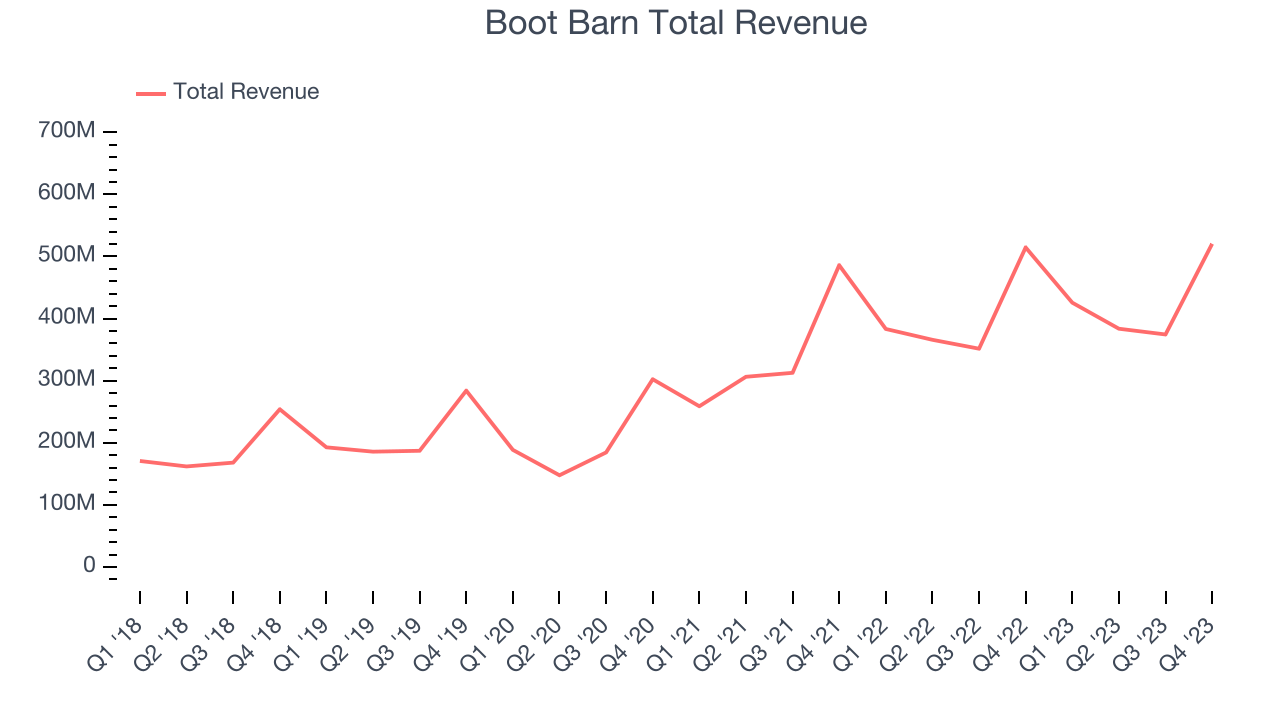

As you can see below, the company's annualized revenue growth rate of 19% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was excellent as it added more brick-and-mortar locations and increased sales at existing, established stores.

This quarter, Boot Barn's revenue grew 1.1% year on year to $520.4 million, falling short of Wall Street's estimates. The company is guiding for a 10.5% year-on-year revenue decline next quarter to $381 million, a reversal from the 11% year-on-year increase it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 4.2% over the next 12 months, an acceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Number of Stores

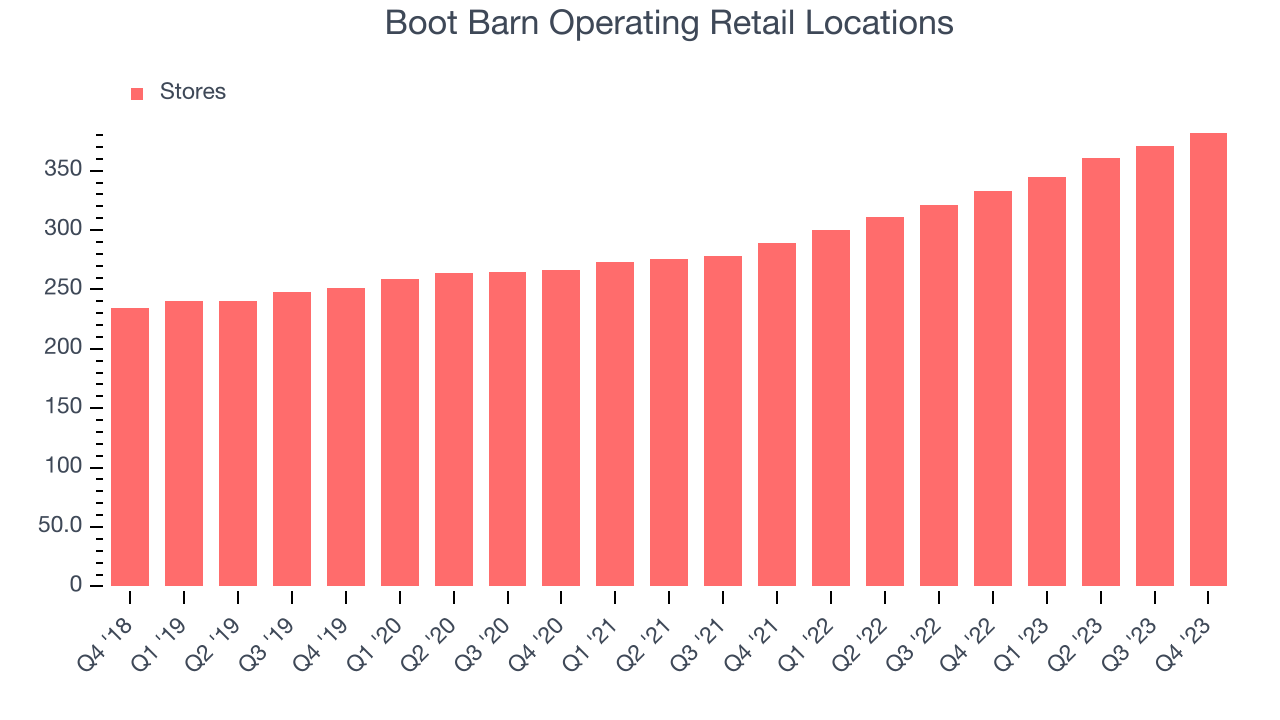

A retailer's store count is a crucial factor influencing how much it can sell, and store growth is a critical driver of how quickly its sales can grow.

When a retailer like Boot Barn is opening new stores, it usually means it's investing for growth because demand is greater than supply. Since last year, Boot Barn's store count increased by 49 locations, or 14.7%, to 382 total retail locations in the most recently reported quarter.

Taking a step back, the company has rapidly opened new stores over the last eight quarters, averaging 14.3% annual growth in its physical footprint. This store growth is much higher than other retailers and gives Boot Barn a chance to scale towards a mid-sized company over time. With an expanding store base and demand, revenue growth can come from multiple vectors: sales from new stores, sales from e-commerce, or increased foot traffic and higher sales per customer at existing stores.

Same-Store Sales

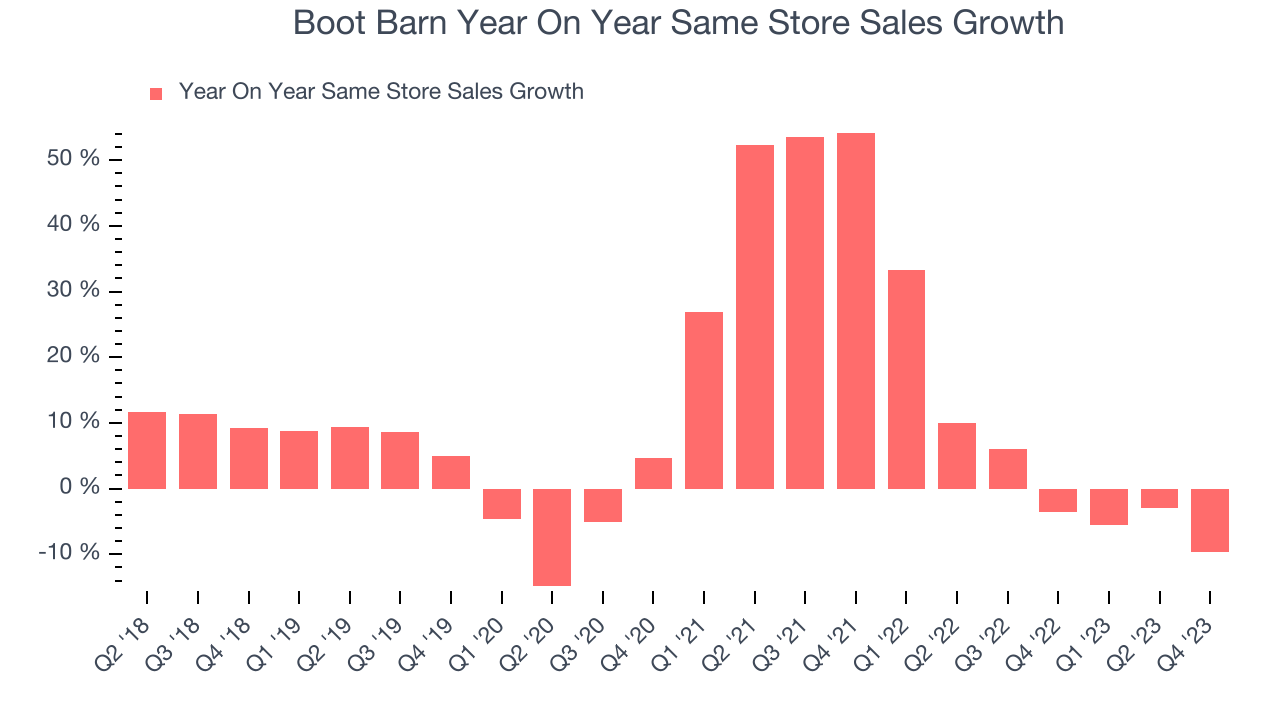

A company's same-store sales growth shows the year-on-year change in sales for its brick-and-mortar stores that have been open for at least a year, give or take, and e-commerce platform. This is a key performance indicator for retailers because it measures organic growth and demand.

Boot Barn's demand within its existing stores has been relatively stable over the last eight quarters but fallen behind the broader consumer retail sector. On average, the company's same-store sales have grown by 2.4% year on year. With positive same-store sales growth amid an increasing physical footprint of stores, Boot Barn is reaching more customers and growing sales.

In the latest quarter, Boot Barn's same-store sales fell 9.7% year on year. This decrease was a further deceleration from the 3.6% year-on-year decline it posted 12 months ago. We hope the business can get back on track.

Key Takeaways from Boot Barn's Q3 Results

We struggled to find many strong positives in these results. Revenue and EPS both missed, and full year guidance was lowered, showing that the headwinds to the business will continue. This trend continued with next quarter's guidance, which was also largely below expectations for key metrics such as revenue and EPS. Overall, this was a mediocre quarter for Boot Barn. The company is down 6.19% on the results and currently trades at $65 per share.

Boot Barn may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.