Upscale bowling alley chain Bowlero (NYSE:BOWL) fell short of analysts' expectations in Q1 CY2024, with revenue up 7% year on year to $337.7 million. It made a GAAP profit of $0.13 per share, improving from its loss of $0.22 per share in the same quarter last year.

Is now the time to buy Bowlero? Find out by accessing our full research report, it's free.

Bowlero (BOWL) Q1 CY2024 Highlights:

- Revenue: $337.7 million vs analyst estimates of $340.9 million (small miss)

- Adjusted EBITDA: $122.8 million vs analyst estimates of $133.1 million (7.7% miss)

- EPS: $0.13 vs analyst expectations of $0.23 (44.1% miss)

- Gross Margin (GAAP): 33.1%, down from 40% in the same quarter last year

- Market Capitalization: $1.87 billion

“Third quarter fiscal year 2024 started slowly due to weather. Post the first three weeks of January, we found a stable footing and increased investments to drive traffic. After the first three weeks of the quarter, we achieved a positive same-store-comp and double-digit total growth. Lucky Strike Miami opened in the quarter with exciting results, and we expect to have four more new builds opening in the next nine months with two in the Denver area and two in California. Summer Season Pass returned this year, and we expect that our continued investments in traffic will drive results throughout the spring and fall,” said Thomas Shannon, Founder and Chief Executive Officer of Bowlero.

Operating over 300 locations globally, Bowlero (NYSE:BOWL) is a contemporary bowling company merging classic lanes with entertainment and deluxe food offerings.

Leisure Facilities

Leisure facilities companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted their spending from "things" to "experiences". Leisure facilities seek to benefit but must innovate to do so because of the industry's high competition and capital intensity.

Sales Growth

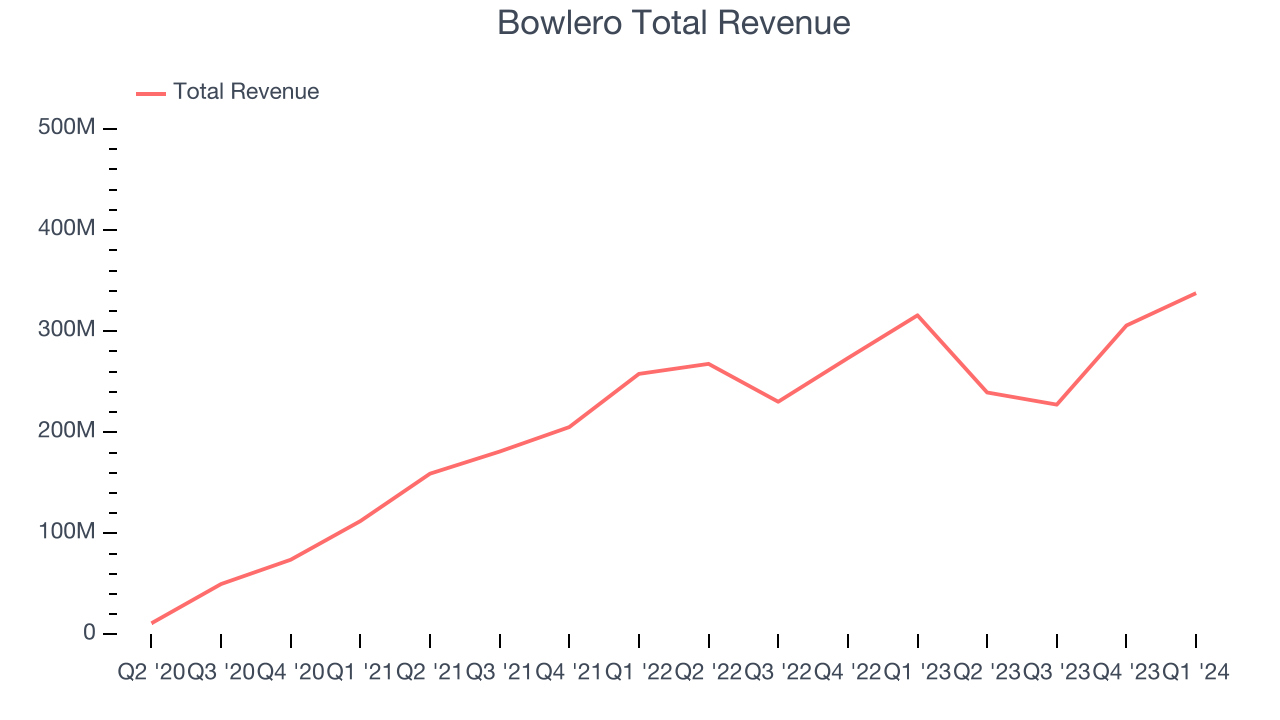

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Bowlero's annualized revenue growth rate of 65% over the last three years was incredible for a consumer discretionary business.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Bowlero's recent history shows its momentum has slowed as its annualized revenue growth of 17.6% over the last two years is below its three-year trend.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Bowlero's recent history shows its momentum has slowed as its annualized revenue growth of 17.6% over the last two years is below its three-year trend.

This quarter, Bowlero's revenue grew 7% year on year to $337.7 million, missing Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 11% over the next 12 months, an acceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

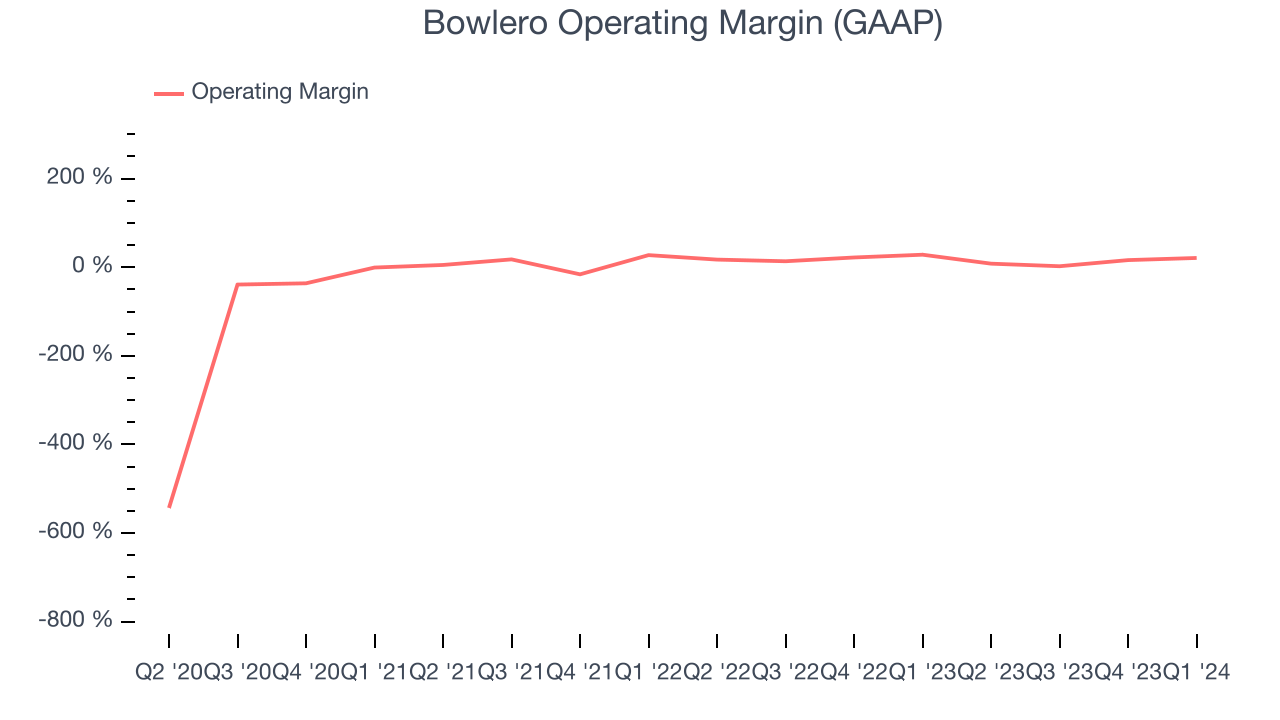

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Bowlero has been a well-managed company over the last eight quarters. It's demonstrated it can be one of the more profitable businesses in the consumer discretionary sector, boasting an average operating margin of 17%.

This quarter, Bowlero generated an operating profit margin of 21%, down 7.3 percentage points year on year.

Over the next 12 months, Wall Street expects Bowlero to become more profitable. Analysts are expecting the company’s LTM operating margin of 13.1% to rise to 19.8%.Key Takeaways from Bowlero's Q1 Results

We struggled to find many strong positives in these results. Its adjusted EBITDA and EPS both missed Wall Street's estimates. Overall, the results could have been better. The company is down 10.9% on the results and currently trades at $11.12 per share.

Bowlero may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.