Packaged foods company Conagra Brands (NYSE:CAG) reported results in line with analysts' expectations in Q1 CY2024, with revenue down 1.7% year on year to $3.03 billion. It made a non-GAAP profit of $0.69 per share, down from its profit of $0.76 per share in the same quarter last year.

Conagra (CAG) Q1 CY2024 Highlights:

- Revenue: $3.03 billion vs analyst estimates of $3.03 billion (small beat)

- EPS (non-GAAP): $0.69 vs analyst estimates of $0.65 (6.2% beat)

- Increasing full year guidance for operating margin to 15.8% from 15.6% previously (maintaining previously-provided full year organic sales and EPS guidance)

- Gross Margin (GAAP): 28.3%, up from 27.2% in the same quarter last year

- Free Cash Flow of $581.1 million, up 70.6% from the previous quarter

- Organic Revenue was down 2% year on year (beat vs. expectations of down 2.6% year on year)

- Sales Volumes were down 1.8% year on year

- Market Capitalization: $13.89 billion

Founded in 1919 as Nebraska Consolidated Mills in Omaha, Nebraska, Conagra Brands today (NYSE:CAG) boasts a diverse portfolio of packaged foods brands that includes everything from whipped cream to jarred pickles to frozen meals.

When the company was first established, co-founders Frank Little and Alva Kinney consolidated the operations of four small flour mills. In the 1980s under CEO Charles Harper, Conagra underwent rapid expansion and transformed from a flour-mill company to a leading food products company. In the 1980s and 1990s, acquisitions to expand the packaged foods portfolio included Banquet Foods, Beatrice Foods, and the Hunt’s and Swiss Miss brands from Nestlé.

Today, Conagra is best known for its Reddi Wip canned whipped cream, its Slim Jim jerky snacks, its Vlasic pickles, and its Marie Callender’s frozen meals, among other iconic packaged food products. The company’s products cater to everyday consumers, families, and individuals who prioritize convenience, taste, and trusted brands in packed goods.

Conagra Brands’ products are widely distributed. Retailers from the largest supermarkets to the corner deli or bodega carry that Orville Redenbacher microwave popcorn or those Banquet prepared meals. Given the company’s scale and traffic-driving brands, Conagra often has prominent placement on retailer shelves.

Shelf-Stable Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Competitors with a broad packaged and frozen foods portfolio include Kraft Heinz (NASDAQ:KHC), General Mills (NYSE:GIS), and Kellogg's (NYSE:K).Sales Growth

Conagra is one of the larger consumer staples companies and benefits from a well-known brand, giving it customer mindshare and influence over purchasing decisions.

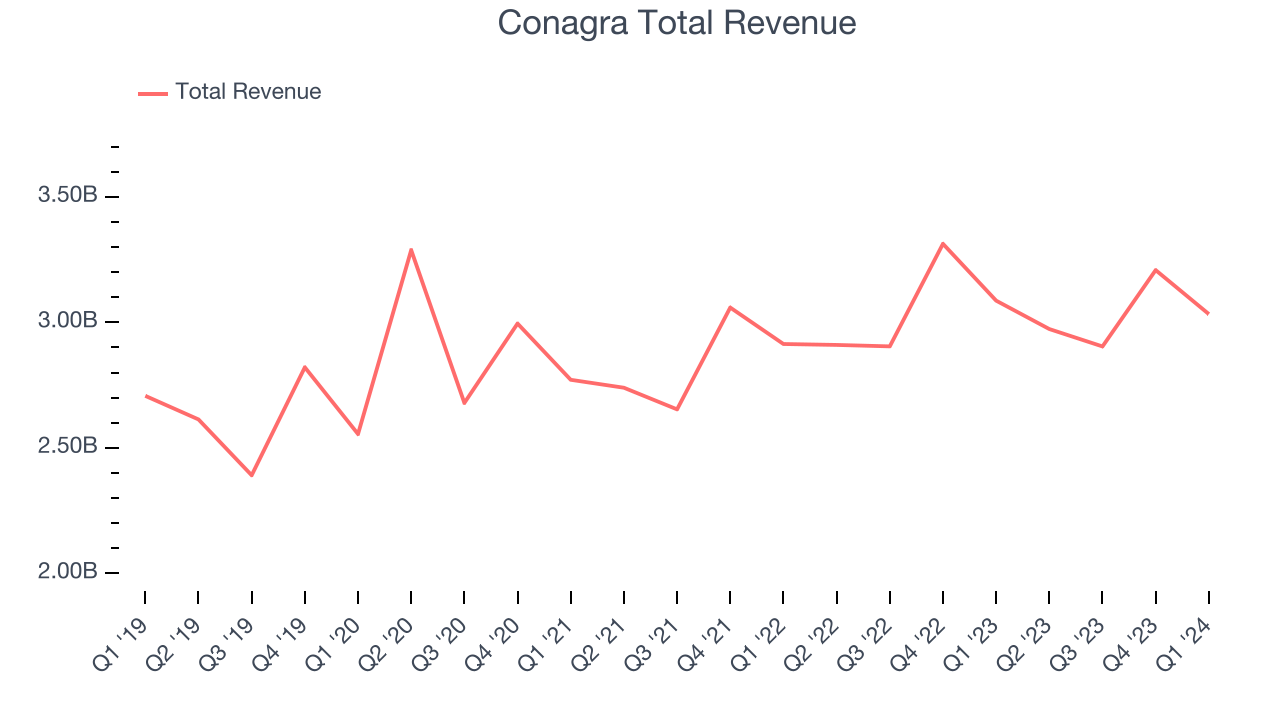

As you can see below, the company's annualized revenue growth rate of 1.1% over the last three years was weak as consumers bought less of its products. We'll explore what this means in the "Volume Growth" section.

This quarter, Conagra reported a rather uninspiring 1.7% year-on-year revenue decline to $3.03 billion in revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

Volume Growth

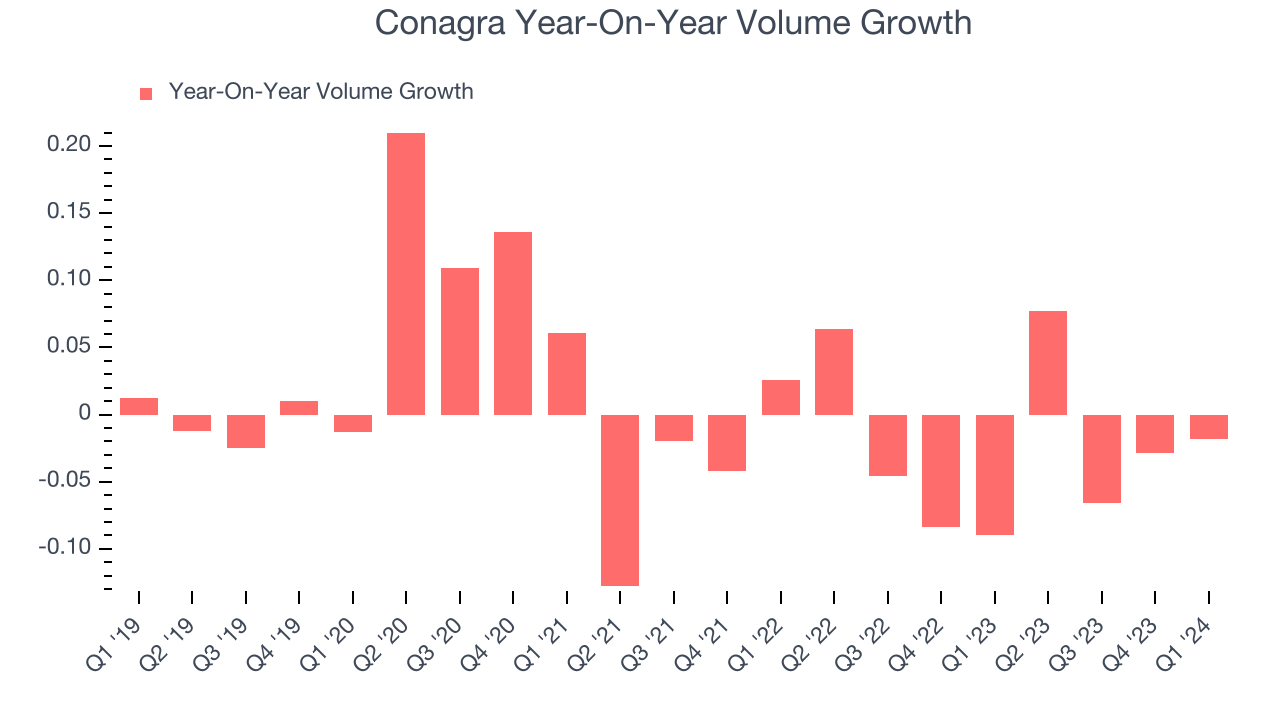

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

To analyze whether Conagra generated its growth from changes in price or volume, we can compare its volume growth to its organic revenue growth, which excludes non-fundamental impacts on company financials like mergers and currency fluctuations.

Over the last two years, Conagra's average quarterly sales volumes have shrunk by 2.4%. This decrease isn't ideal as the quantity demanded for consumer staples products is typically stable. Luckily, Conagra was able to offset fewer customers purchasing its products by charging higher prices, enabling it to generate 3.5% average organic revenue growth. We hope the company can grow its volumes soon, however, as consistent price increases (on top of inflation) aren't sustainable over the long term unless the business is really really special.

In Conagra's Q1 2024, sales volumes dropped 1.8% year on year. This result was a step in the right direction compared to its 9% year-on-year decline 12 months ago.

Gross Margin & Pricing Power

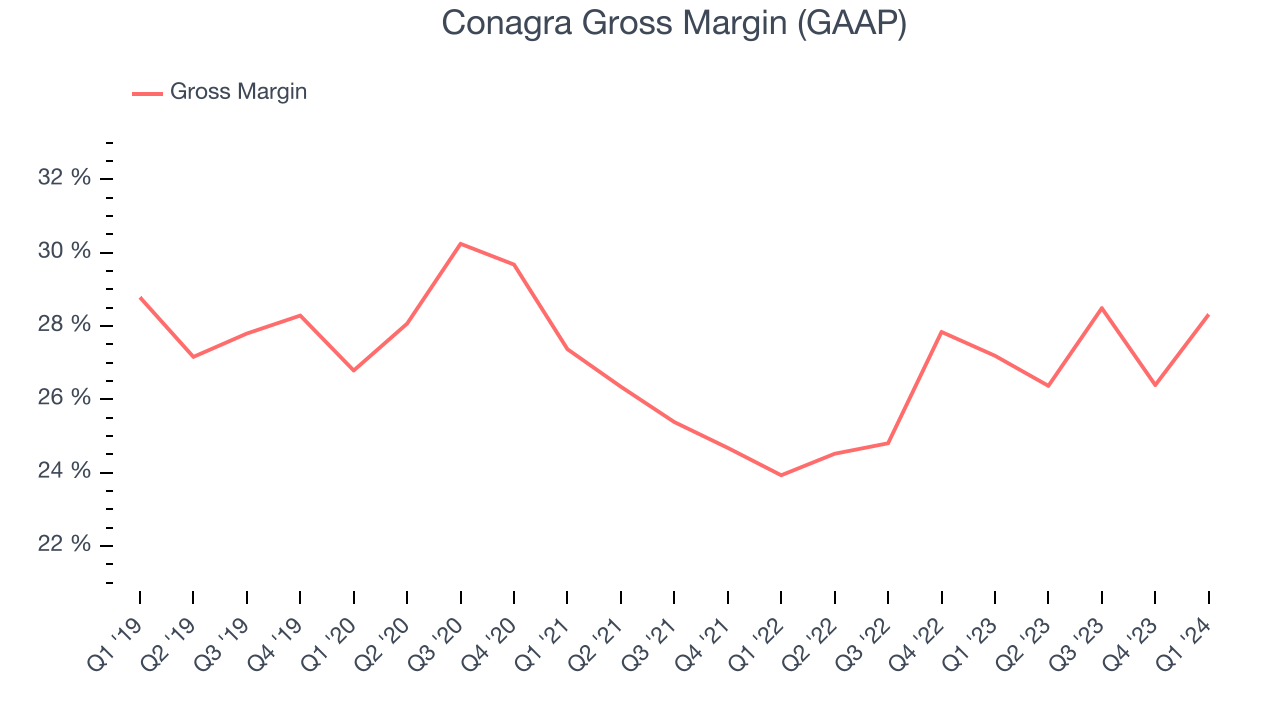

This quarter, Conagra's gross profit margin was 28.3%, up 1.1 percentage points year on year. That means for every $1 in revenue, a chunky $0.72 went towards paying for raw materials, production of goods, and distribution expenses.

Conagra has subpar unit economics for a consumer staples company, making it difficult to invest in areas such as marketing and talent to grow its brand. As you can see above, it's averaged a 26.8% gross margin over the last two years. Its margin, however, has been trending up over the last 12 months, averaging 5.3% year-on-year increases each quarter. If this trend continues, it could suggest a less competitive environment.

Operating Margin

Operating margin is an important measure of profitability accounting for key expenses such as marketing and advertising, IT systems, wages, and other administrative costs.

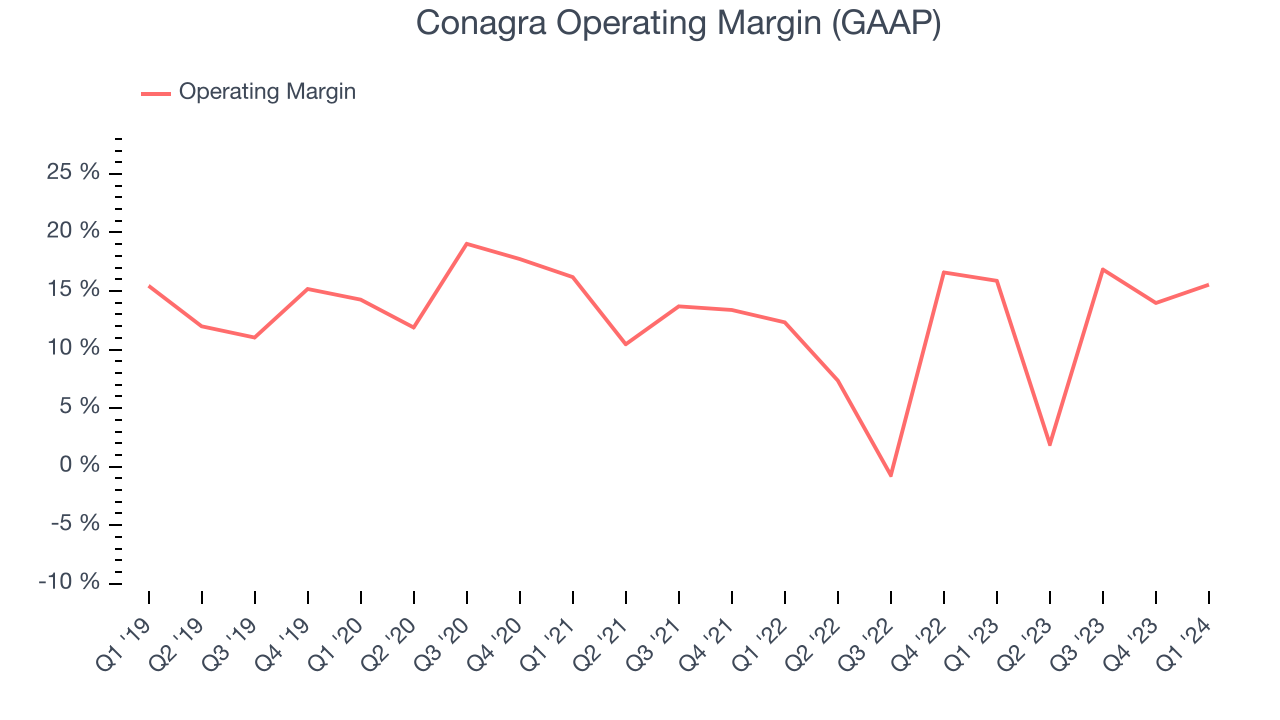

This quarter, Conagra generated an operating profit margin of 15.5%, in line with the same quarter last year. This indicates the company's costs have been relatively stable.

Zooming out, Conagra has done a decent job managing its expenses over the last eight quarters. The company has produced an average operating margin of 11.1%, higher than the broader consumer staples sector. On top of that, its margin has risen by 2 percentage points on average over the last year, showing the company is improving its fundamentals. The company's operating profitability was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes tectonic shifts to move meaningfully. Companies have more control over their operating margins, and it signals strength if they're high when gross margins are low (like for Conagra).

Zooming out, Conagra has done a decent job managing its expenses over the last eight quarters. The company has produced an average operating margin of 11.1%, higher than the broader consumer staples sector. On top of that, its margin has risen by 2 percentage points on average over the last year, showing the company is improving its fundamentals. The company's operating profitability was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes tectonic shifts to move meaningfully. Companies have more control over their operating margins, and it signals strength if they're high when gross margins are low (like for Conagra).EPS

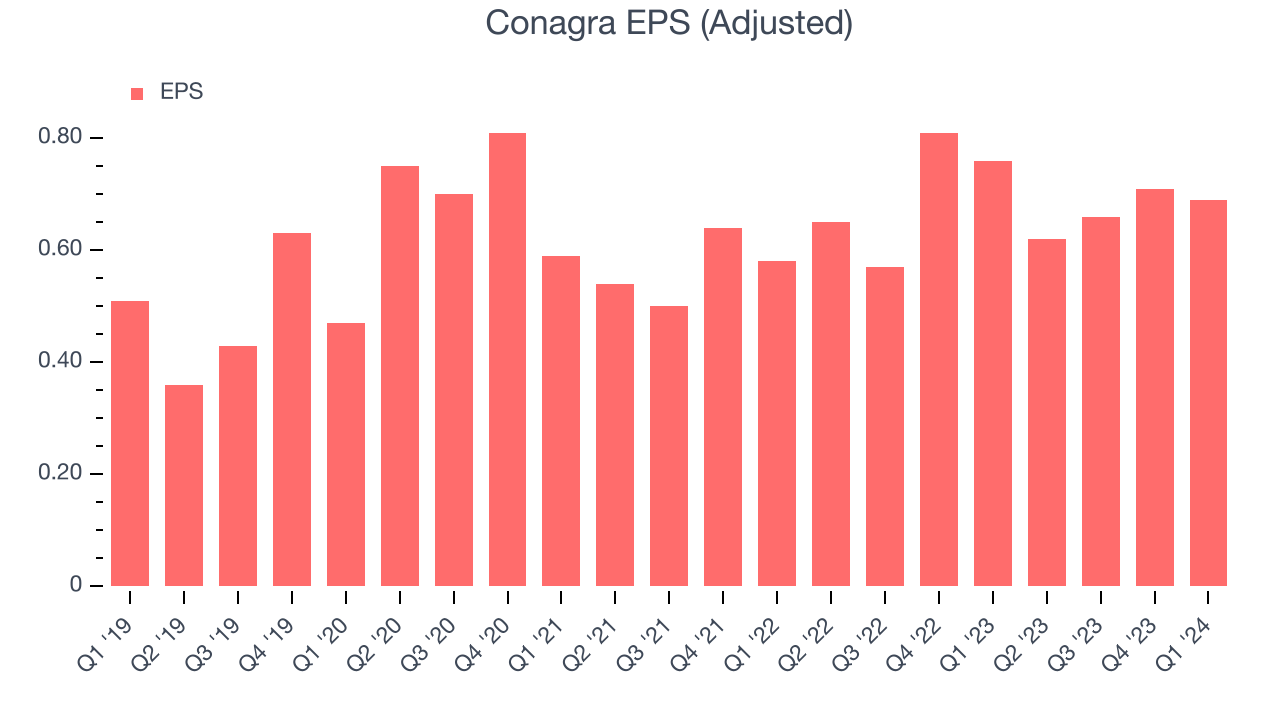

Earnings growth is a critical metric to track, but for long-term shareholders, earnings per share (EPS) is more telling because it accounts for dilution and share repurchases.

In Q1, Conagra reported EPS at $0.69, down from $0.76 in the same quarter a year ago. This print beat Wall Street's estimates by 6.2%.

Between FY2021 and FY2024, Conagra's EPS dropped 6%, translating into 2% annualized declines. We tend to steer our readers away from companies with falling EPS, especially in the consumer staples sector, where shrinking earnings could imply changing secular trends or consumer preferences. If there's no earnings growth, it's difficult to build confidence in a business's underlying fundamentals, leaving a low margin of safety around the company's valuation (making the stock susceptible to large downward swings).

Earnings stability could be coming, however, as Wall Street is projecting Conagra's EPS to stay flat over the next 12 months.

Cash Is King

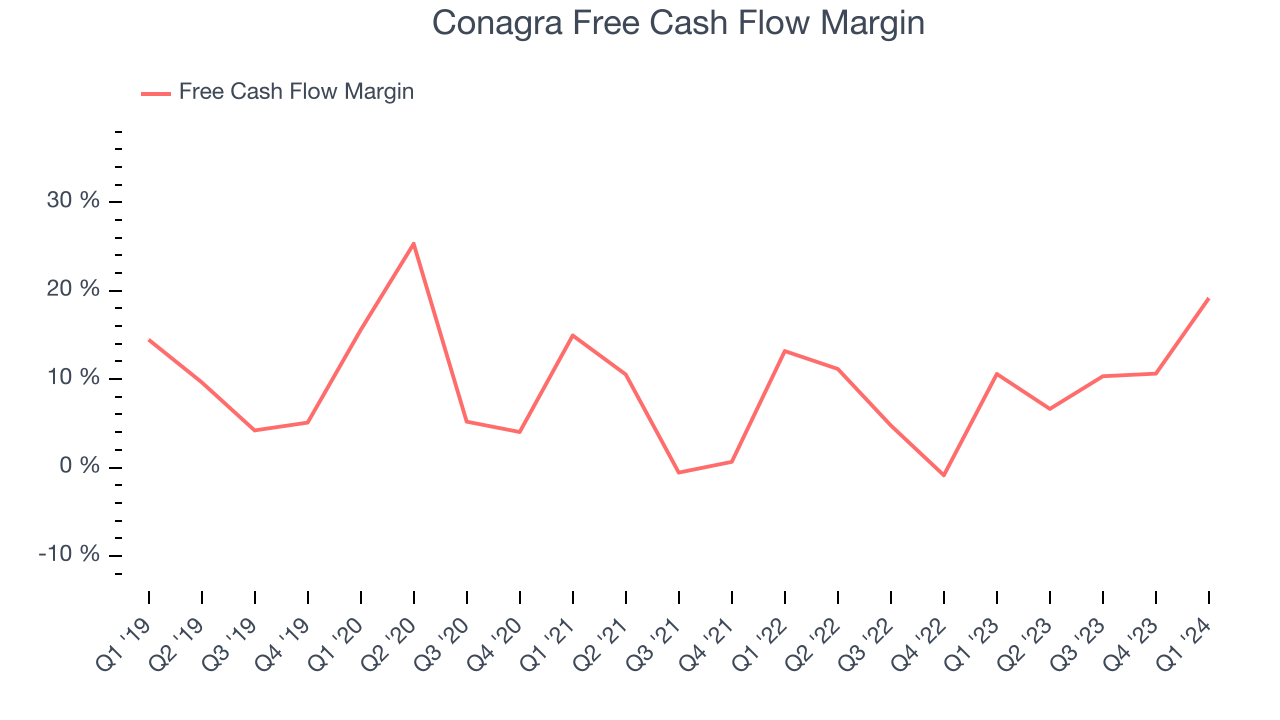

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Conagra's free cash flow came in at $581.1 million in Q1, up 77.9% year on year. This result represents a 19.2% margin.

Over the last eight quarters, Conagra has shown solid cash profitability, giving it the flexibility to reinvest or return capital to investors. The company's free cash flow margin has averaged 9%, above the broader consumer staples sector. Furthermore, its margin has averaged year-on-year increases of 5.5 percentage points over the last 12 months. This likely pleases the company's investors.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Conagra's five-year average ROIC was 7.2%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Conagra's ROIC over the last five years averaged 1.7 percentage point decreases each year. In conjunction with its already low returns, these declines suggest the company's profitable business opportunities are few and far between.

Key Takeaways from Conagra's Q1 Results

We liked how Conagra beat analysts' organic revenue growth expectations this quarter. We were also excited its gross margin outperformed Wall Street's estimates. For the full year, it was comforting that organic sales guidance was maintained while operating margin guidance was raised. The CEO struck an optimistic tone in the release, saying that "Volume trends in our domestic retail business continued to improve as targeted investments, particularly in frozen, generated strong lifts and unit share gains." Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is up 6.6% after reporting and currently trades at $30.99 per share.

Is Now The Time?

Conagra may have had a favorable quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Conagra, we'll be cheering from the sidelines. Its revenue growth has been weak over the last three years, and analysts expect growth to deteriorate from here. And while its well-known brand makes it a household name consumers consistently turn to, the downside is its projected EPS for the next year is lacking. On top of that, its shrinking sales volumes suggest it'll need to change its strategy to succeed.

Conagra's price-to-earnings ratio based on the next 12 months is 10.9x. While the price is reasonable and there are some things to like about Conagra, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $29.97 per share right before these results (compared to the current share price of $30.99).

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.