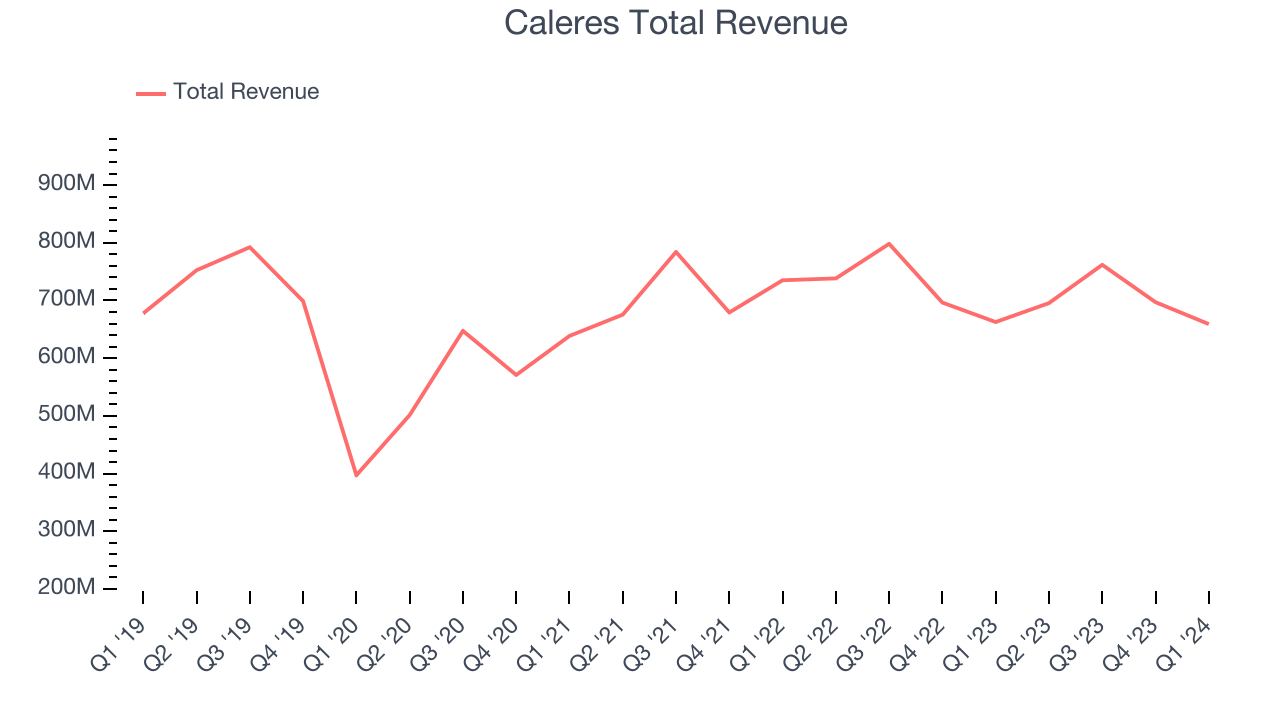

Footwear company Caleres (NYSE:CAL) missed analysts' expectations in Q1 CY2024, with revenue flat year on year at $659.2 million. It made a GAAP profit of $0.88 per share, down from its profit of $0.97 per share in the same quarter last year.

Is now the time to buy Caleres? Find out by accessing our full research report, it's free.

Caleres (CAL) Q1 CY2024 Highlights:

- Revenue: $659.2 million vs analyst estimates of $664.8 million (small miss)

- Gross Margin (GAAP): 46.9%, up from 45.7% in the same quarter last year

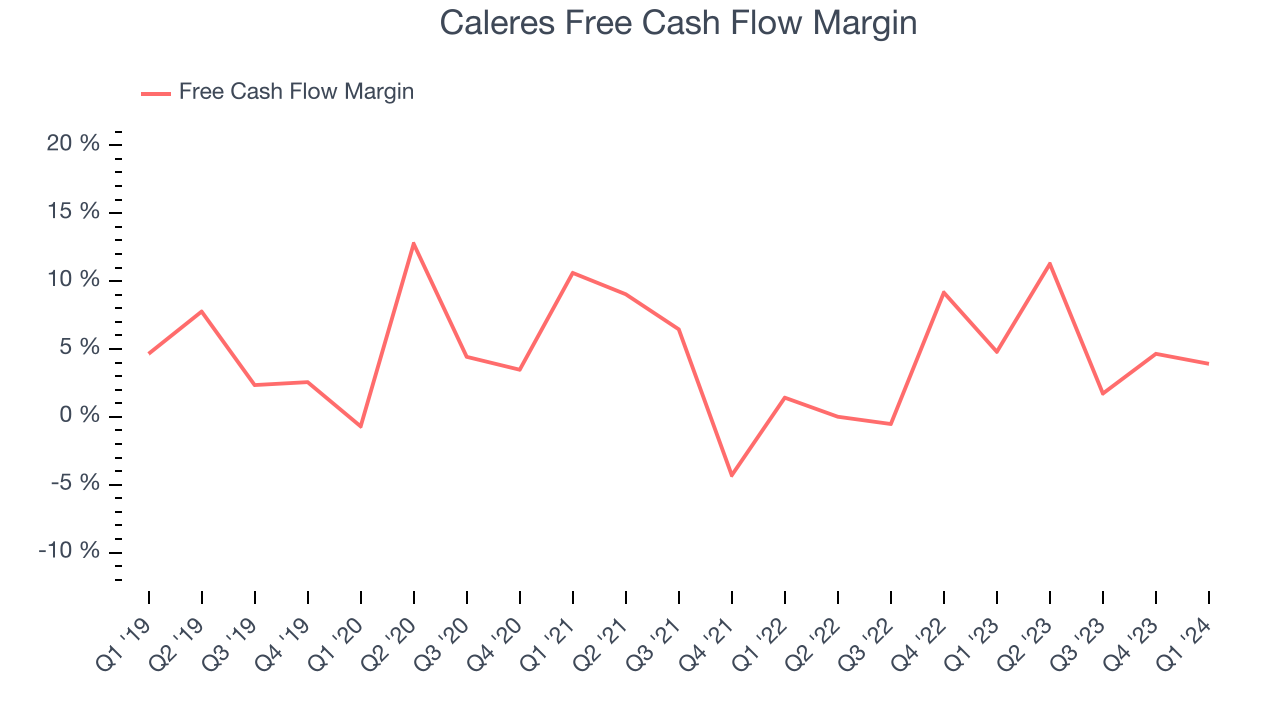

- Free Cash Flow of $25.75 million, down 20.4% from the previous quarter

- Market Capitalization: $1.29 billion

“Caleres began 2024 in strong fashion, achieving earnings per share ahead of expectations, generating record first quarter consolidated gross margin, and making significant progress on our key strategic initiatives, all while investing for the long-term,” said Jay Schmidt, President and Chief Executive Officer.

The owner of Dr. Scholl's, Caleres (NYSE:CAL) is a footwear company offering a range of styles.

Footwear

Before the advent of the internet, styles changed, but consumers mainly bought shoes by visiting local brick-and-mortar shoe, department, and specialty stores. Today, not only do styles change more frequently as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some footwear companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

A company’s long-term performance can indicate its business health. Any business can put up a good quarter or two, but many enduring ones tend to grow for years. Over the last five years, Caleres's sales were flat. This shows its demand was soft and is a tough starting point for our quality assessment.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Caleres's annualized revenue declines of 1.1% over the last two years align with its five-year trend, suggesting its demand consistently shrunk.

This quarter, Caleres missed Wall Street's estimates and reported a rather uninspiring 0.5% year-on-year revenue decline, generating $659.2 million of revenue. Looking ahead, Wall Street expects sales to grow 1.8% over the next 12 months, an acceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Caleres has shown poor cash profitability over the last two years, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin averaged 4.2%, lousy for a consumer discretionary business.

Caleres's free cash flow clocked in at $25.75 million in Q1, equivalent to a 3.9% margin. This quarter's margin was in line with the comparable period last year. Over the next year, analysts' consensus estimates show they're expecting Caleres's free cash flow margin of 5.3% for the last 12 months to remain the same.

Key Takeaways from Caleres's Q1 Results

We were impressed by Caleres's optimistic earnings forecast for the next quarter and full year, which blew past analysts' expectations. On the other hand, this quarter's revenue unfortunately missed, but the strong outlook was enough to overcome it. Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is up 2.3% after reporting and currently trades at $37.50 per share.

Caleres may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.