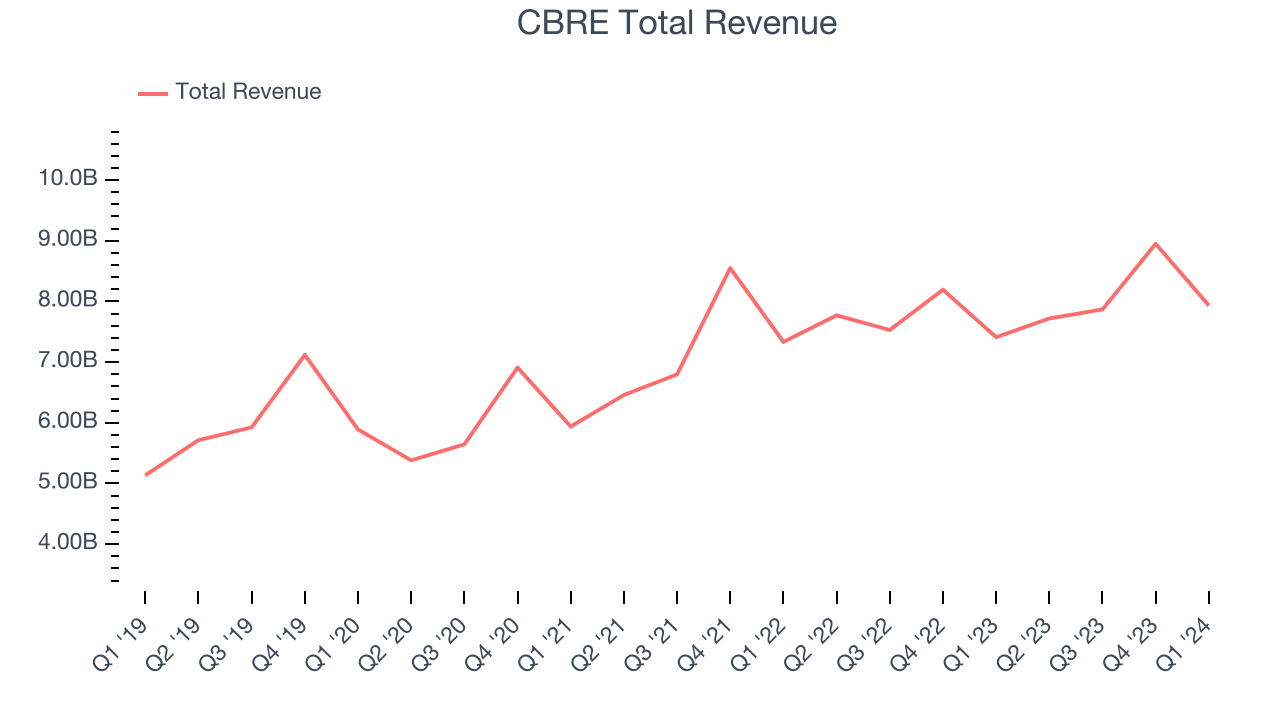

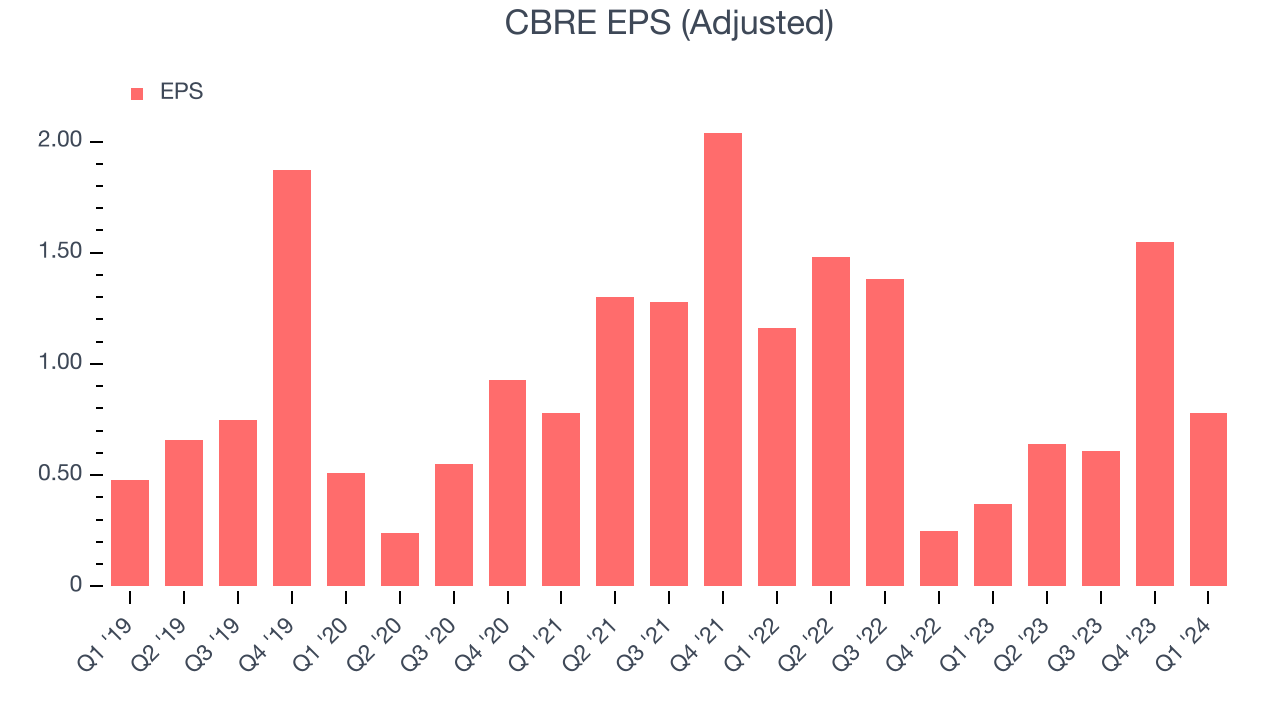

Commercial real estate firm CBRE (NYSE:CBRE) reported results in line with analysts' expectations in Q1 CY2024, with revenue up 7.1% year on year to $7.94 billion. It made a non-GAAP profit of $0.78 per share, improving from its profit of $0.37 per share in the same quarter last year.

CBRE (CBRE) Q1 CY2024 Highlights:

- Revenue: $7.94 billion vs analyst estimates of $7.95 billion (small miss)

- EBITDA: $424 million vs analyst estimates of $438 million (3.2% miss)

- EPS (non-GAAP): $0.78 vs analyst estimates of $0.69 (12.7% beat)

- Gross Margin (GAAP): 18.4%, down from 19.2% in the same quarter last year

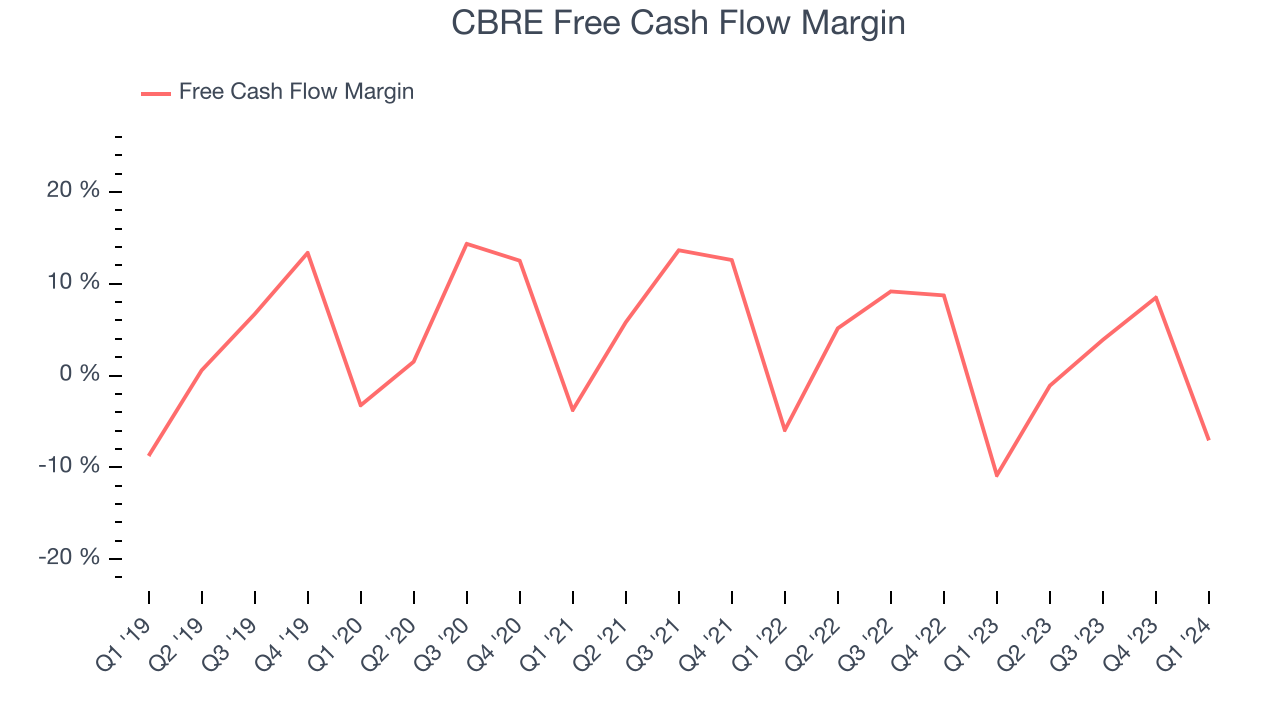

- Free Cash Flow was -$560 million, down from $759.6 million in the previous quarter

- Market Capitalization: $26.19 billion

Established in 1906, CBRE (NYSE:CBRE) is one of the largest commercial real estate services firms in the world.

CBRE’s comprehensive offerings include property management, leasing, commercial property and corporate facility management, project management, capital markets solutions (including property sales, mortgage brokerage, and loan origination), valuation, and advisory services. This wide range of services positions CBRE as a full-service provider in the commercial real estate market, capable of meeting a diverse array of client needs.

The company operates through three primary business segments: Advisory Services, Global Workplace Solutions, and Real Estate Investments. Advisory Services provides a broad range of services to property owners and investors, including leasing, capital markets, property management, valuation, and consulting. Global Workplace Solutions offers a comprehensive suite of facilities management and project management services for occupiers of commercial properties. The Real Estate Investments segment includes investment management services through CBRE Global Investors and development services through Trammell Crow Company.

CBRE’s global footprint is extensive, with more than 500 offices and tens of thousands of employees worldwide. This expansive network allows the company to serve clients across various geographies and industries, offering local market insight along with global expertise.

Real Estate Services

Technology has been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

CBRE’s primary competitors include Jones Lang LaSalle (NYSE:JLL), Cushman & Wakefield (NYSE:CWK), Colliers International (NASDAQ:CIGI), and BGC Partners (NASDAQ:BGCP).Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. CBRE's annualized revenue growth rate of 8.3% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. CBRE's recent history shows the business has slowed as its annualized revenue growth of 5.6% over the last two years is below its five-year trend.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. CBRE's recent history shows the business has slowed as its annualized revenue growth of 5.6% over the last two years is below its five-year trend.

We can dig even further into the company's revenue dynamics by analyzing its three most important segments: Advisory Services, Workplace Solutions, and Investment Management, which are 24%, 73.2%, and 2.9% of revenue. Over the last two years, CBRE's Workplace Solutions revenue (facilities and project management) averaged 36.6% year-on-year growth while its Advisory Services (leasing, capital markets) and Investment Management (real estate investments) revenues averaged 6.8% and 7% declines.

This quarter, CBRE grew its revenue by 7.1% year on year, and its $7.94 billion of revenue was in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 10.7% over the next 12 months, an acceleration from this quarter.

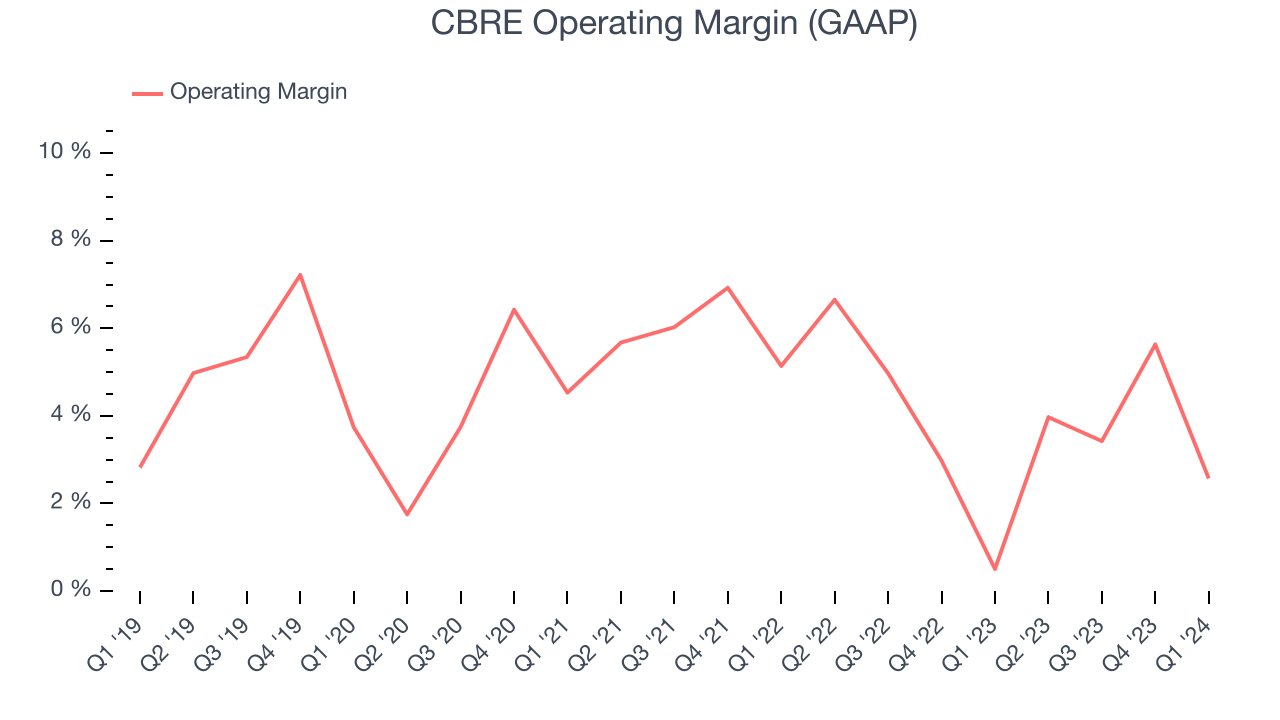

Operating Margin

Operating margin is an important measure of profitability. It’s the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. Operating margin is also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

CBRE was profitable over the last two years but held back by its large expense base. Its average operating margin of 3.9% has been paltry for a consumer discretionary business.

In Q1, CBRE generated an operating profit margin of 2.6%, up 2.1 percentage points year on year.

Over the next 12 months, Wall Street expects CBRE to maintain its LTM operating margin of 4%.EPS

We track long-term historical earnings per share (EPS) growth for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Over the last five years, CBRE's EPS grew 13.7%, translating into a weak 2.6% compounded annual growth rate.

In Q1, CBRE reported EPS at $0.78, up from $0.37 in the same quarter last year. This print beat analysts' estimates by 12.7%. Over the next 12 months, Wall Street expects CBRE to grow its earnings. Analysts are projecting its LTM EPS of $3.58 to climb by 37.4% to $4.92.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, CBRE has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 2.2%, subpar for a consumer discretionary business.

CBRE burned through $560 million of cash in Q1, equivalent to a negative 7.1% margin, increasing its cash burn by 30.4% year on year.

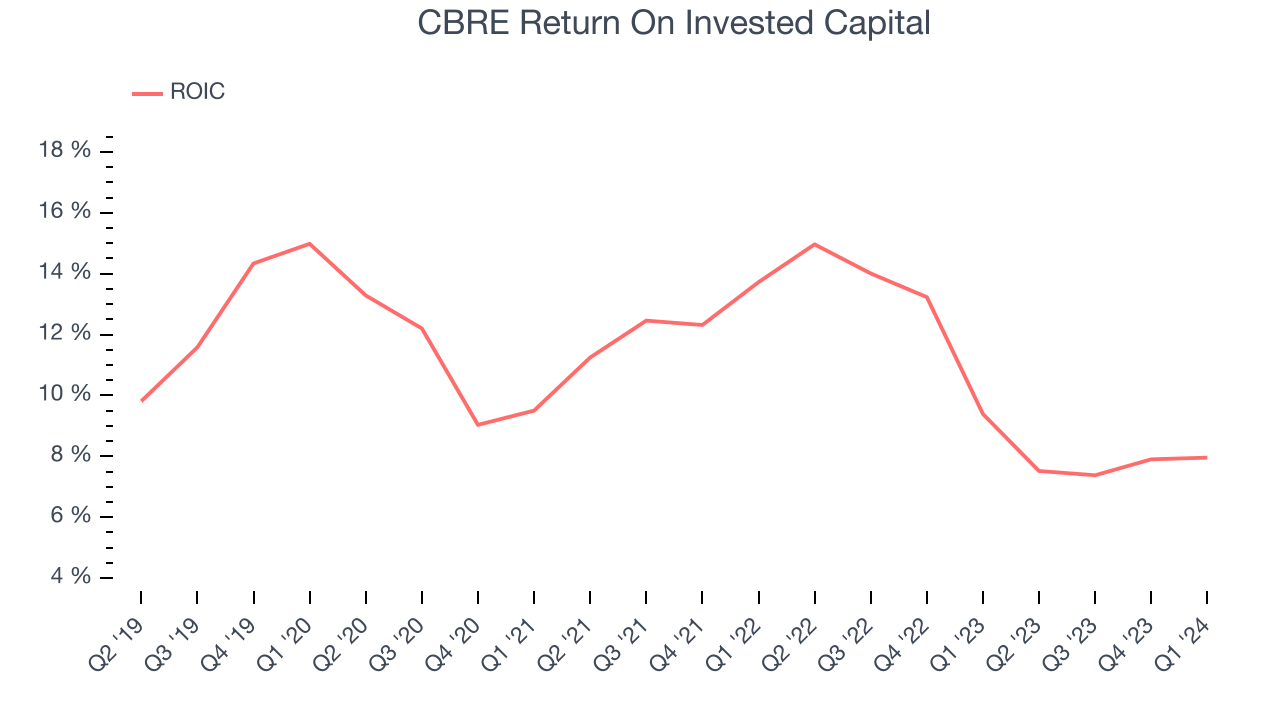

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

CBRE's five-year average return on invested capital was 11.1%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, CBRE's ROIC averaged 3.6 percentage point decreases over the last few years. Paired with its already low returns, these declines suggest the company's profitable business opportunities are few and far between.

Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly.

CBRE reported $1.04 billion of cash and $5.43 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $2.1 billion of EBITDA over the last 12 months, we view CBRE's 2.1x net-debt-to-EBITDA ratio as safe. We also see its $84.59 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from CBRE's Q1 Results

CBRE's key Workplace Solutions revenue outperformed Wall Street's estimates. However, that's where the good news ends. Total revenue missed slightly and EBITDA missed by more. On the other hand, its operating margin missed. Overall, this was a mediocre quarter for CBRE. The company is down 2.9% on the results and currently trades at $84.32 per share.

Is Now The Time?

When considering an investment in CBRE, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We cheer for all companies serving consumers, but in the case of CBRE, we'll be cheering from the sidelines. Its revenue growth has been a little slower over the last five years, but at least growth is expected to increase in the short term. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its low free cash flow margins give it little breathing room. On top of that, its operating margins reveal poor profitability compared to other consumer discretionary companies.

CBRE's price-to-earnings ratio based on the next 12 months is 17.7x. While we've no doubt one can find things to like about CBRE, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $104.11 per share right before these results (compared to the current share price of $84.32).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.