Carnival’s (NYSE:CCL) Q3: Beats On Revenue

Radek Strnad /

September 30, 2024

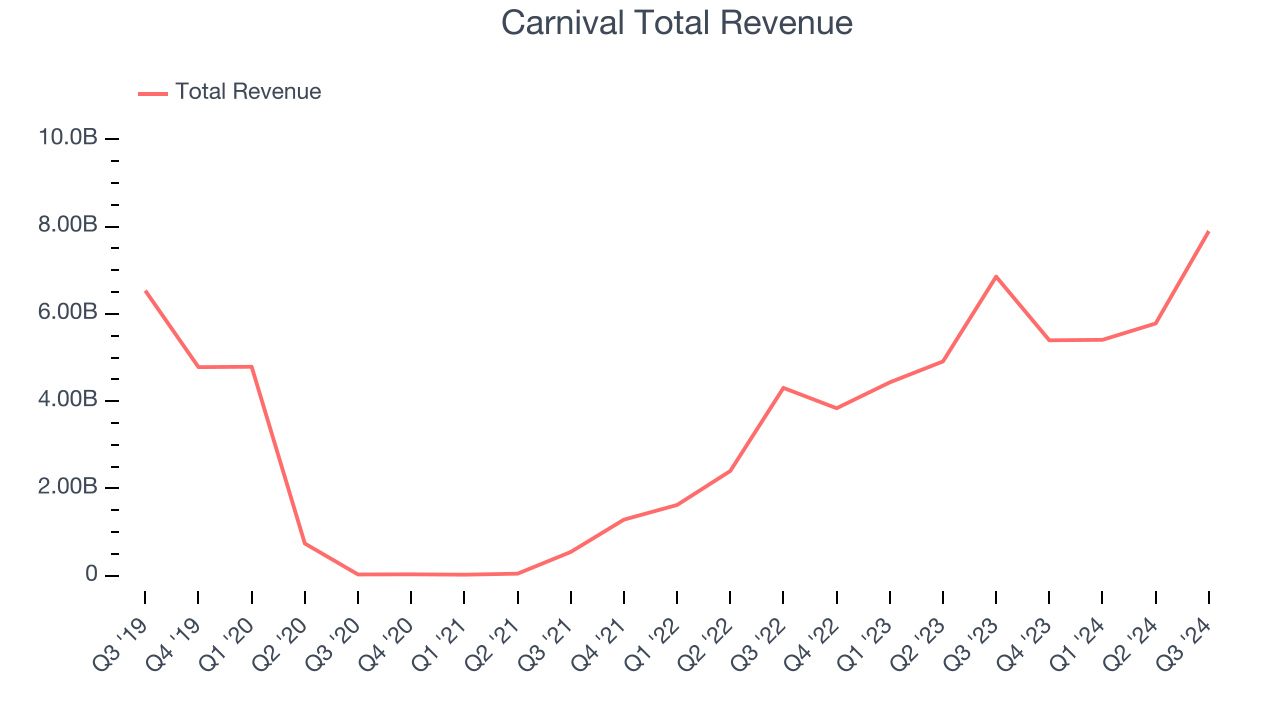

Cruise ship company Carnival (NYSE:CCL) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 15.2% year on year to $7.90 billion. Its non-GAAP profit of $1.27 per share was 10% above analysts’ consensus estimates.

Is now the time to buy Carnival? Find out in our full research report.

Carnival (CCL) Q3 CY2024 Highlights:

- Revenue: $7.90 billion vs analyst estimates of $7.82 billion (in line)

- EPS (non-GAAP): $1.27 vs analyst estimates of $1.15 (10% beat)

- Management raised its full-year EPS (non-GAAP) guidance to $1.33 at the midpoint, a 12.7% increase

- EBITDA guidance for the full year is $6 billion at the midpoint, above analyst estimates of $5.91 billion

- Gross Margin (GAAP): 58.1%, up from 56.3% in the same quarter last year

- EBITDA Margin: 35.7%, up from 32.4% in the same quarter last year

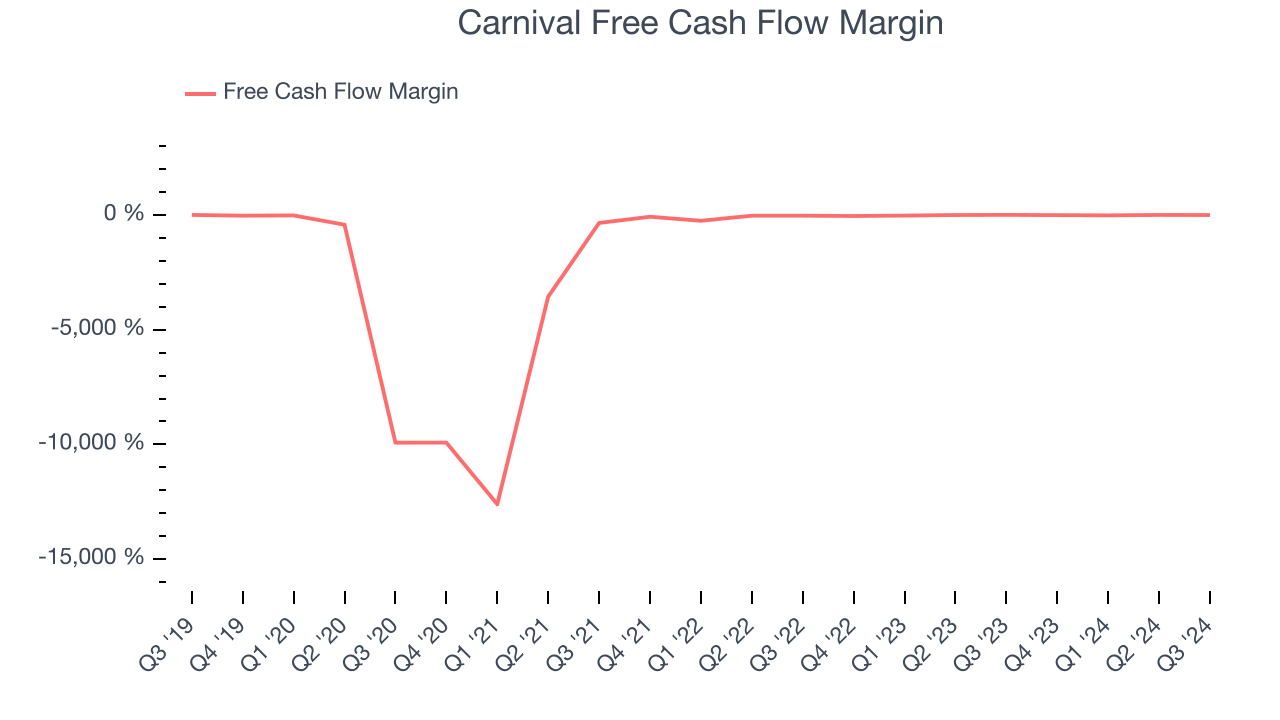

- Free Cash Flow Margin: 7.9%, down from 14.5% in the same quarter last year

- Passenger Cruise Days: 28.1 million, up 2.3 million year on year

- Market Capitalization: $23.28 billion

"We delivered a phenomenal third quarter, breaking operational records and outperforming across the board. Our strong improvements were led by high-margin, same-ship yield growth, driving a 26 percent improvement in unit operating income, the highest level we have reached in fifteen years," commented Carnival Corporation & plc's Chief Executive Officer Josh Weinstein.

Company Overview

Boasting outrageous amenities like a planetarium on board its ships, Carnival (NYSE:CCL) is one of the world's largest leisure travel companies and a prominent player in the cruise industry.

Hotels, Resorts and Cruise Lines

Hotels, resorts, and cruise line companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted from buying "things" (wasteful) to buying "experiences" (memorable). In addition, the internet has introduced new ways of approaching leisure and lodging such as booking homes and longer-term accommodations. Traditional hotel, resorts, and cruise line companies must innovate to stay relevant in a market rife with innovation.

Sales Growth

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Carnival’s 3.6% annualized revenue growth over the last five years was sluggish. This shows it failed to expand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or emerging trend. Carnival’s annualized revenue growth of 59.6% over the last two years is above its five-year trend, suggesting its demand recently accelerated. Note that COVID hurt Carnival’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

We can better understand the company’s revenue dynamics by analyzing its number of passenger cruise days, which reached 28.1 million in the latest quarter. Over the last two years, Carnival’s passenger cruise days averaged 73.6% year-on-year growth. Because this number is higher than its revenue growth during the same period, we can see the company’s monetization has fallen.

This quarter, Carnival’s year-on-year revenue growth clocked in at 15.2%, and its $7.90 billion of revenue was in line with Wall Street’s estimates. Looking ahead, Wall Street expects sales to grow 5.6% over the next 12 months, a deceleration versus the last two years.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Carnival has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 1.5%, lousy for a consumer discretionary business.

Carnival’s free cash flow clocked in at $627 million in Q3, equivalent to a 7.9% margin. The company’s cash profitability regressed as it was 6.6 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends are more important.

Key Takeaways from Carnival’s Q3 Results

We were impressed by Carnival’s optimistic full-year earnings forecast, which blew past analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its earnings forecast for next quarter missed. Overall, this quarter was mixed with some key positives. The stock traded up 1.1% to $18.75 immediately after reporting.

Big picture, is Carnival a buy here and now?If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings.We cover that in our actionable full research report which you can read here, it’s free.