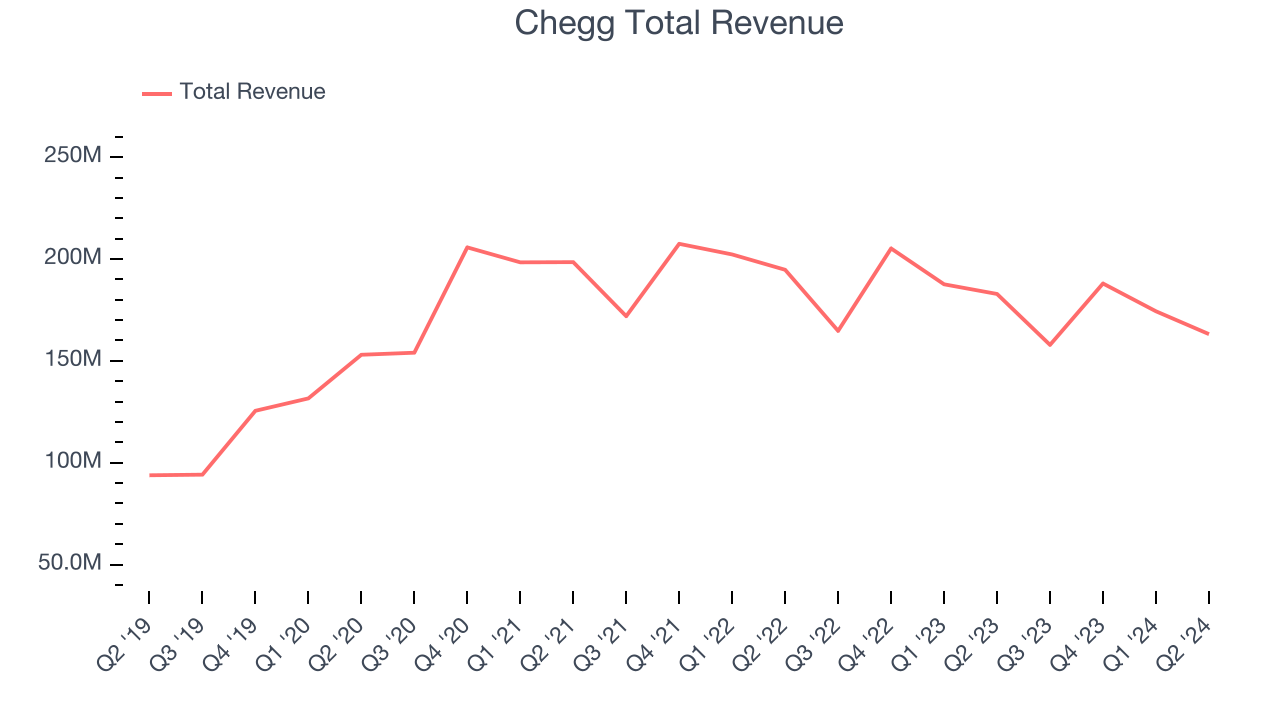

Online study and academic help platform Chegg (NYSE:CHGG) reported Q2 CY2024 results topping analysts' expectations, with revenue down 10.8% year on year to $163.1 million. On the other hand, next quarter's revenue guidance of $134 million was less impressive, coming in 6.3% below analysts' estimates. It made a non-GAAP profit of $0.24 per share, down from its profit of $0.28 per share in the same quarter last year.

Is now the time to buy Chegg? Find out by accessing our full research report, it's free.

Chegg (CHGG) Q2 CY2024 Highlights:

- Revenue: $163.1 million vs analyst estimates of $160 million (2% beat)

- EPS (non-GAAP): $0.24 vs analyst estimates of $0.23 (5.7% beat)

- Revenue Guidance for Q3 CY2024 is $134 million at the midpoint, below analyst estimates of $143 million

- Adjusted EBITDA Guidance for Q3 CY2024 is $20 million at the midpoint, well below analyst estimates of $34 million

- Gross Margin (GAAP): 72.2%, down from 74.1% in the same quarter last year

- Adjusted EBITDA Margin: 27%, down from 32.7% in the same quarter last year

- Free Cash Flow was -$3.57 million, down from $25.3 million in the previous quarter

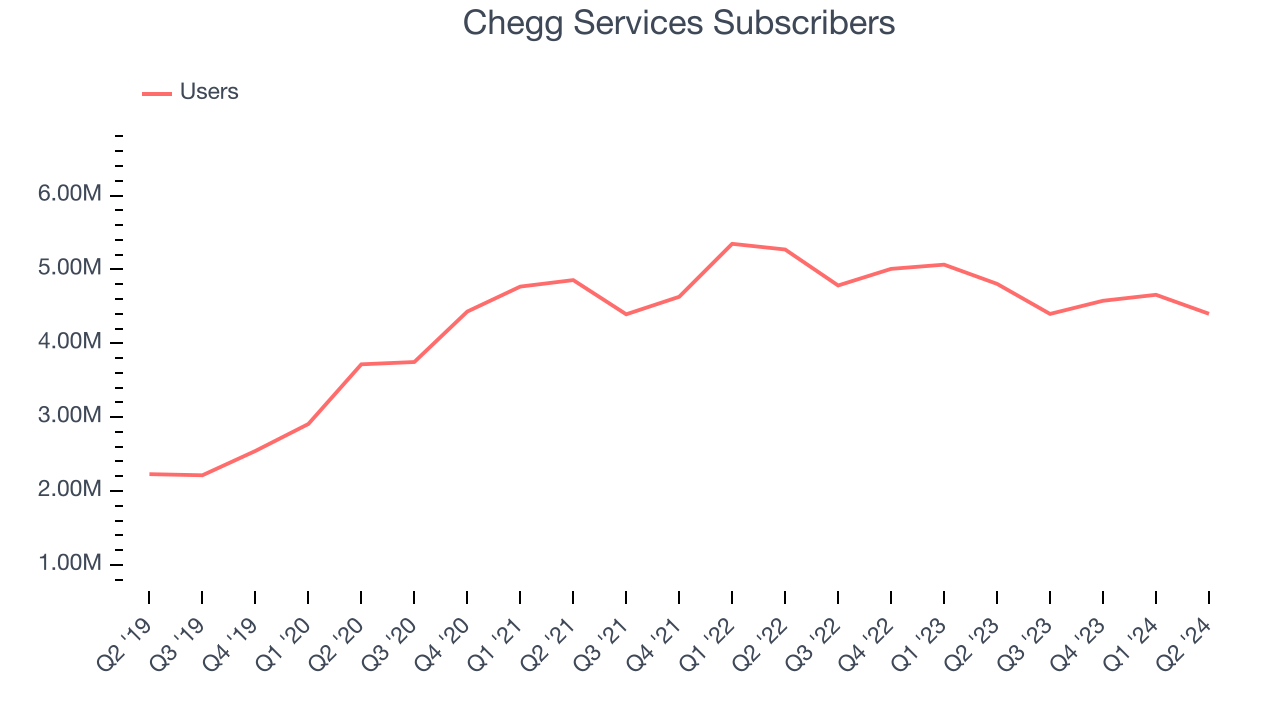

- Services Subscribers: 4.4 million, down 405,000 year on year

- Market Capitalization: $306.7 million

“Q2 has been transformational for Chegg, completing our restructure, outlining an exciting vision for the future, and completing the rollout of conversational instruction capability and automated solutions just in time for the back-to-school season,” said Nathan Schultz, Chief Executive Officer & President of Chegg,

Started as a physical textbook rental service, Chegg (NYSE:CHGG) is now a digital platform addressing student pain points by providing study and academic assistance.

Consumer Subscription

Consumers today expect goods and services to be hyper-personalized and on demand. Whether it be what music they listen to, what movie they watch, or even finding a date, online consumer businesses are expected to delight their customers with simple user interfaces that magically fulfill demand. Subscription models have further increased usage and stickiness of many online consumer services.

Sales Growth

Chegg's revenue has been declining over the last three years, dropping on average by 3% annually. This quarter, Chegg beat analysts' estimates but reported a year on year revenue decline of 10.8%.

Chegg is expecting next quarter's revenue to decline 15.1% year on year to $134 million, a further deceleration from the 4.2% year-on-year decrease it recorded in the comparable quarter last year. Before the earnings results were announced, analysts were projecting revenue to decline -6% over the next 12 months.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Usage Growth

As a subscription-based app, Chegg generates revenue growth by expanding both its subscriber base and the amount each subscriber spends over time.

Chegg has been struggling to grow its users, a key performance metric for the company. Over the last two years, its users have declined 3.8% annually to 4.4 million. This is one of the lowest rates of growth in the consumer internet sector.

In Q2, Chegg's users decreased by 405,000, a 8.4% drop since last year.

Revenue Per User

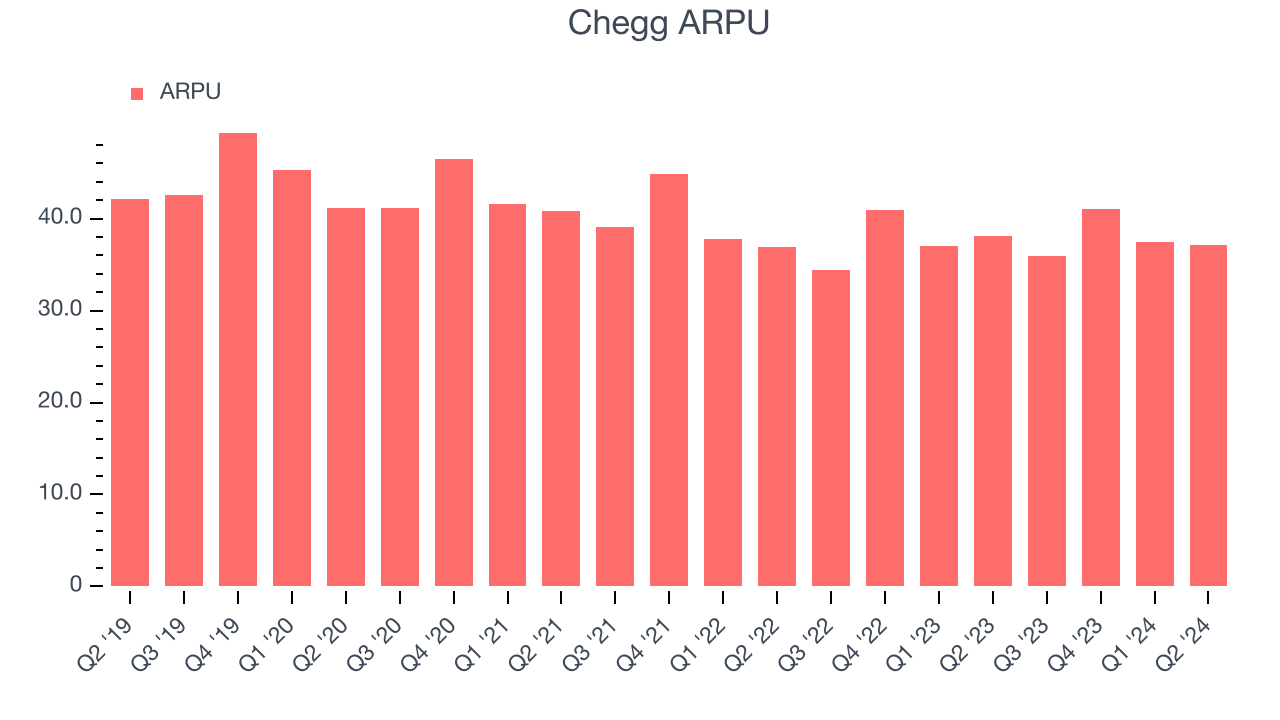

Average revenue per user (ARPU) is a critical metric to track for consumer internet businesses like Chegg because it measures how much the average user spends. ARPU is also a key indicator of how valuable its users are (and can be over time).

Chegg's ARPU has declined over the last two years, averaging 2.1%. On top of that, its users have also shrunk, indicating that the business is encountering some serious problems. This quarter, ARPU declined 2.6% year on year to $37.08 per user.

Key Takeaways from Chegg's Q2 Results

It was good to see Chegg narrowly top analysts' revenue expectations this quarter. On the other hand, its number of users declined and its revenue growth was quite weak. Both revenue and adjusted EBITDA guidance for next quarter missed expectations. Overall, this was a bad quarter for Chegg, which is unfortunate because the market is quite skeptical about this company with the rise of AI. This quarter is not proving that the business can overcome being replaced by AI. The stock traded down 13.6% to $2.54 immediately after reporting.

Chegg may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.