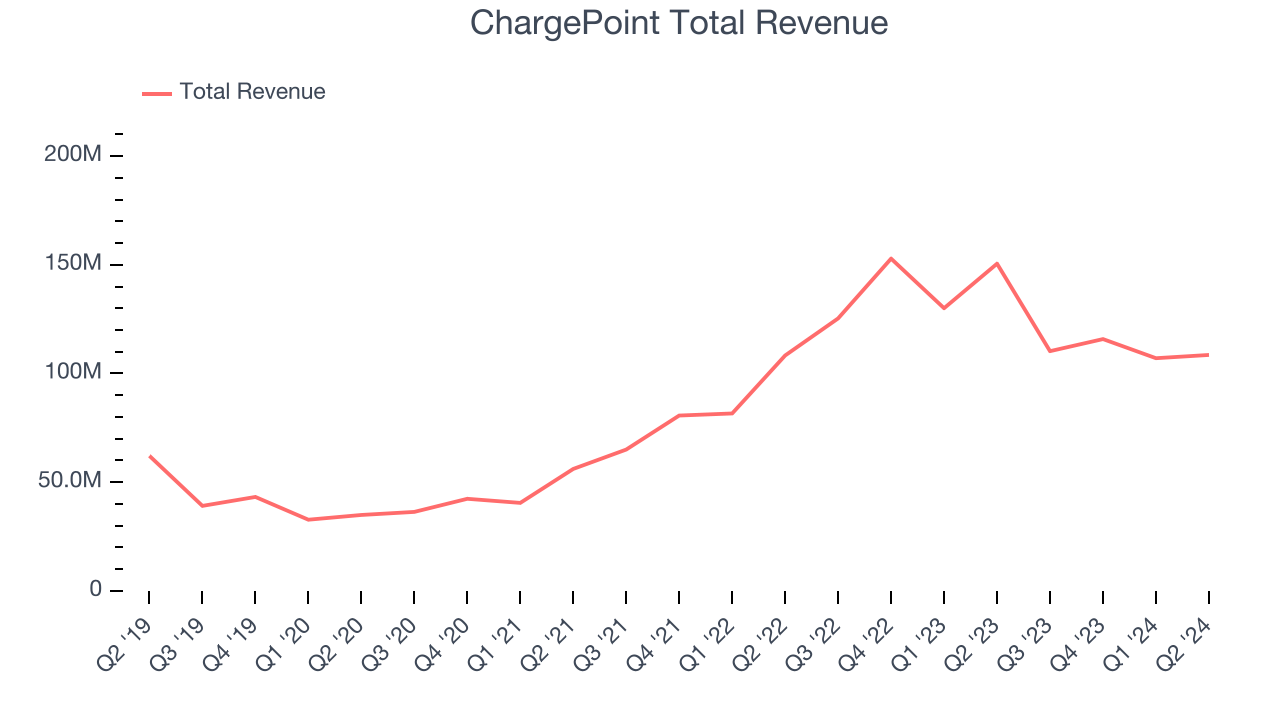

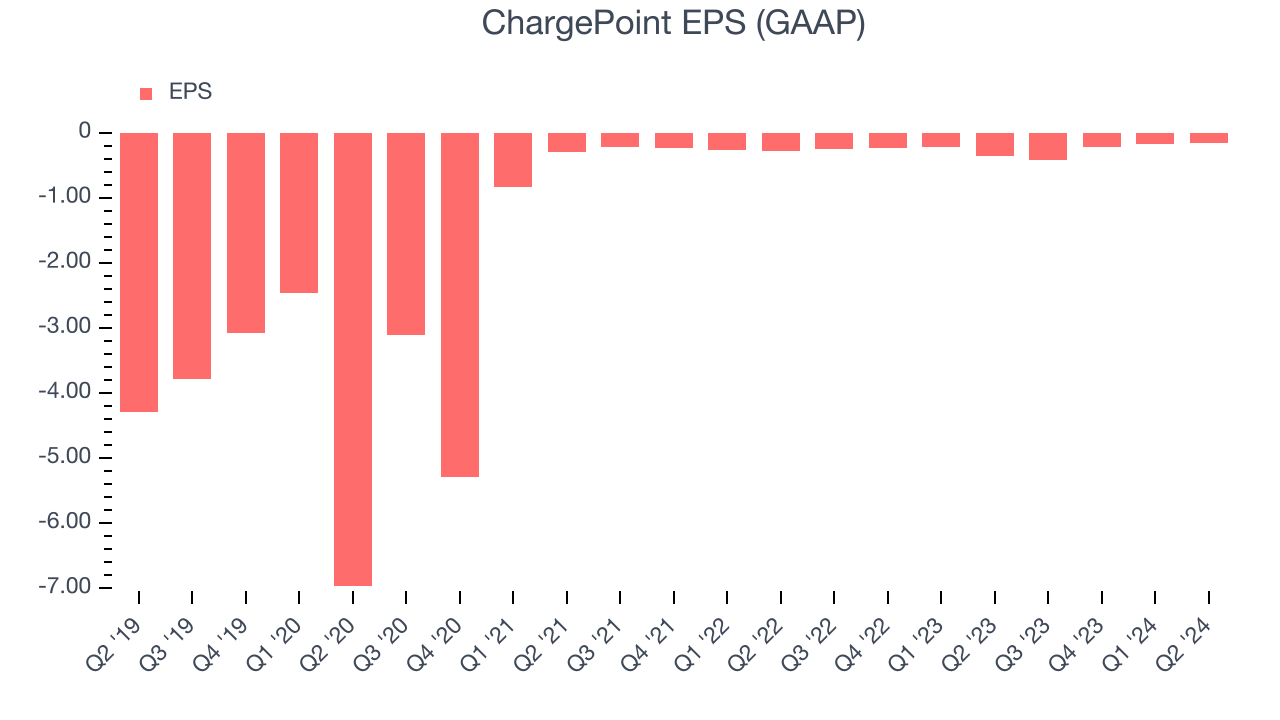

EV charging solutions provider ChargePoint Holdings (NYSE:CHPT) missed analysts’ expectations in Q2 CY2024, with revenue down 27.9% year on year to $108.5 million. Next quarter’s revenue guidance of $90 million also underwhelmed, coming in 33.8% below analysts’ estimates. It made a GAAP loss of $0.16 per share, improving from its loss of $0.35 per share in the same quarter last year.

Is now the time to buy ChargePoint? Find out by accessing our full research report, it’s free.

ChargePoint (CHPT) Q2 CY2024 Highlights:

- Revenue: $108.5 million vs analyst estimates of $113.5 million (4.4% miss)

- EPS: -$0.16 vs analyst expectations of -$0.16 (2.7% miss)

- Revenue Guidance for Q3 CY2024 is $90 million at the midpoint, below analyst estimates of $135.9 million

- Gross Margin (GAAP): 23.6%, up from 0.7% in the same quarter last year

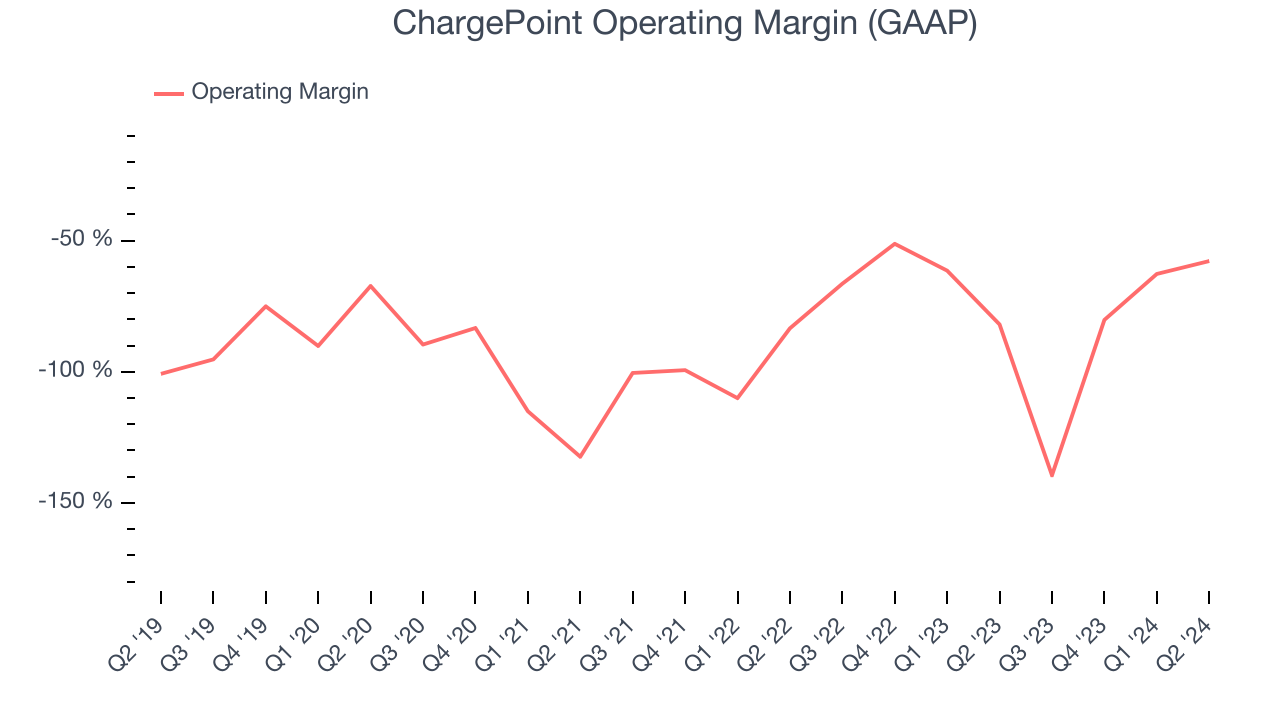

- EBITDA Margin: -31.4%, up from -53.9% in the same quarter last year

- Free Cash Flow was -$55 million compared to -$93.95 million in the same quarter last year

- Market Capitalization: $723 million

“ChargePoint continued to execute against its strategy and deliver results in line with our stated goals. Our second quarter revenue was within our stated guidance range and gross margin improved sequentially for the third consecutive quarter. Today, we have implemented an action plan to create efficiencies while reducing operating expenses,” said Rick Wilmer, CEO of ChargePoint.

The most prominent EV charging company during the COVID bull market, ChargePoint (NYSE:CHPT) is a provider of electric vehicle charging technology solutions in North America and Europe.

Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Sales Growth

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, ChargePoint’s 18.3% annualized revenue growth over the last five years was incredible. This is encouraging because it shows ChargePoint’s offerings resonate with customers, a helpful starting point.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. ChargePoint’s annualized revenue growth of 14.7% over the last two years is below its five-year trend, but we still think the results were good and suggest demand was strong.

ChargePoint also breaks out the revenue for its most important segments, Networked Charging Systems and Subscriptions, which are 59.1% and 33.3% of revenue. Over the last two years, ChargePoint’s Networked Charging Systems revenue averaged 21.5% year-on-year growth while its Subscriptions revenue averaged 41% growth.

This quarter, ChargePoint missed Wall Street’s estimates and reported a rather uninspiring 27.9% year-on-year revenue decline, generating $108.5 million of revenue. The company is guiding for a 18.4% year-on-year revenue decline next quarter to $90 million, a deceleration from the 12% year-on-year decrease it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 34.2% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Unprofitable industrials companies require extra attention because they could get caught swimming naked if the tide goes out. It’s hard to trust that ChargePoint can endure a full cycle as its high expenses have contributed to an average operating margin of negative 83% over the last five years. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, ChargePoint’s annual operating margin decreased by 3.4 percentage points over the last five years. The company’s performance was poor no matter how you look at it. It shows operating expenses were rising and it couldn’t pass those costs onto its customers.

In Q2, ChargePoint generated an operating profit margin of negative 57.8%, up 24.1 percentage points year on year. This increase was solid, and since the company’s operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as sales, marketing, R&D, and administrative overhead.

EPS

Analyzing long-term revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although ChargePoint’s full-year earnings are still negative, it reduced its losses and improved its EPS by 47.9% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

In Q2, ChargePoint reported EPS at negative $0.16, up from negative $0.35 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street is optimistic. Analysts are projecting ChargePoint’s EPS of negative $0.98 in the last year to reach break even.

Key Takeaways from ChargePoint’s Q2 Results

We struggled to find many strong positives in these results. Its revenue and EPS missed analysts' expectations, and its sales outlook for next quarter fell short. Overall, this quarter could have been better. The stock traded down 8% to $1.55 immediately following the results.

ChargePoint may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.