Customer relationship management software maker Salesforce (NYSE:CRM) reported results in line with analyst expectations in Q3 FY2023 quarter, with revenue up 14.1% year on year to $7.83 billion. The company expects that next quarter's revenue would be around $7.98 billion, which is the midpoint of the guidance range. That was in roughly line with analyst expectations. Salesforce made a GAAP profit of $210 million, down on its profit of $468 million, in the same quarter last year.

Is now the time to buy Salesforce? Access our full analysis of the earnings results here, it's free.

Salesforce (CRM) Q3 FY2023 Highlights:

- Revenue: $7.83 billion vs analyst estimates of $7.83 billion (small beat)

- EPS (non-GAAP): $1.40 vs analyst estimates of $1.22 (14.4% beat)

- Revenue guidance for Q4 2023 is $7.98 billion at the midpoint, below analyst estimates of $8.04 billion

- Free cash flow of $115 million, down 12.2% from previous quarter

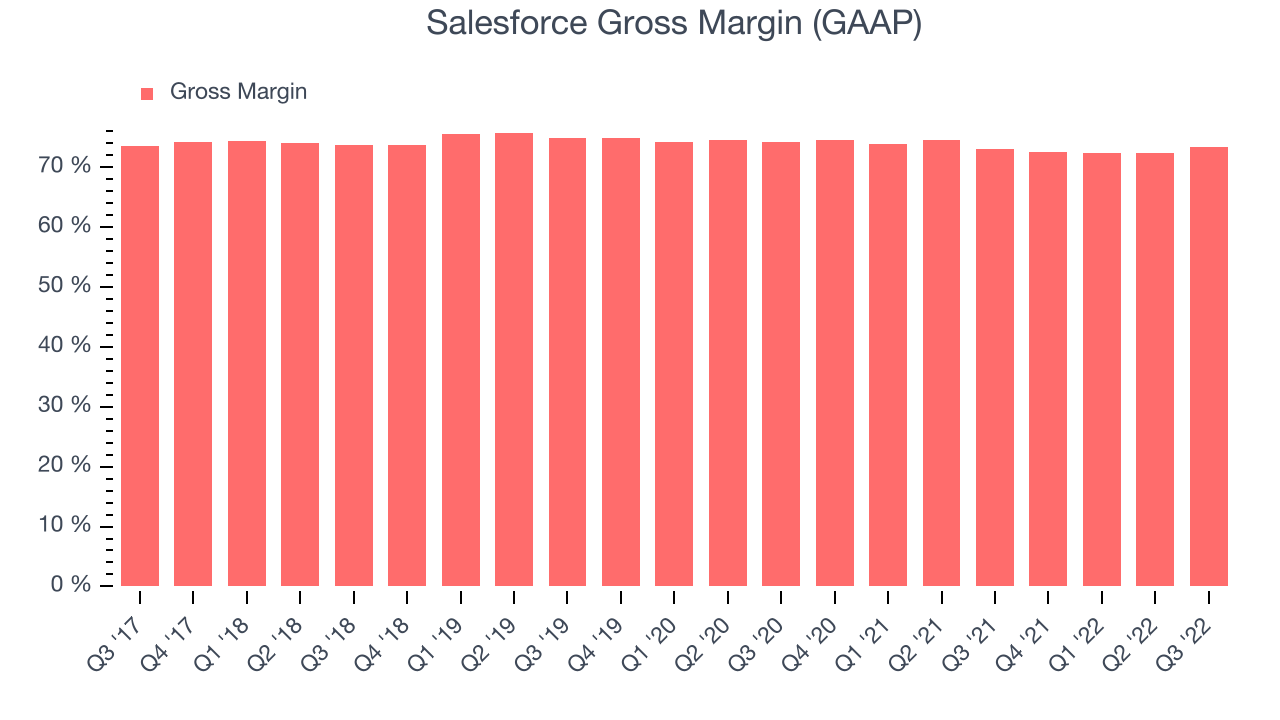

- Gross Margin (GAAP): 73.3%, in line with same quarter last year

Launched in 1999 from a rented one-bedroom apartment in San Francisco by Marc Benioff and his three co-founders, Salesforce (NYSE:CRM) is a software as a service platform that helps companies access, manage and share sales information.

Companies need to be able to interact with and sell to their customers as efficiently as possible. This reality, coupled with the ongoing migration of enterprises to the cloud drives demand for cloud-based customer relationship management (CRM) software that integrate data analytics with sales and marketing functions.

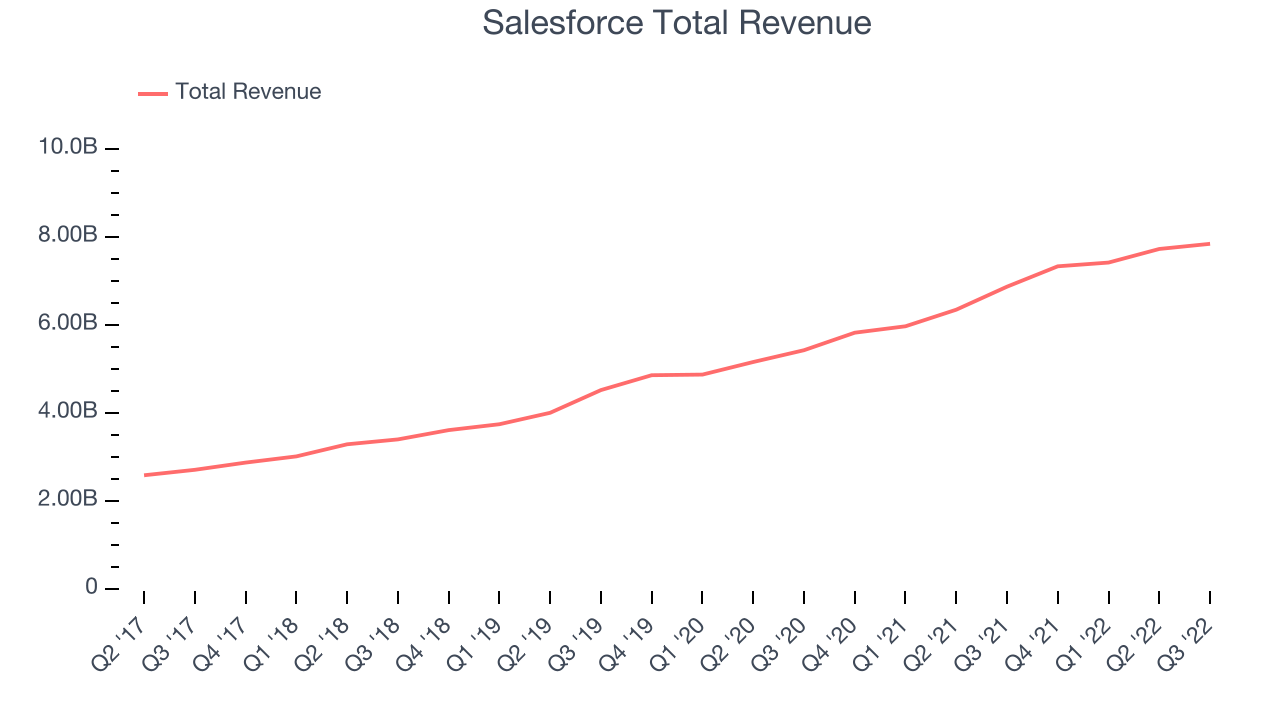

Sales Growth

As you can see below, Salesforce's revenue growth has been strong over the last two years, growing from quarterly revenue of $5.41 billion in Q3 FY2021, to $7.83 billion.

This quarter, Salesforce's quarterly revenue was once again up 14.1% year on year. But the growth did slow down compared to last quarter, as the revenue increased by just $117 million in Q3, compared to $309 million in Q2 2023. We'd like to see revenue increase by a greater amount each quarter, but a one-off fluctuation is usually not concerning.

Guidance for the next quarter indicates Salesforce is expecting revenue to grow 8.95% year on year to $7.98 billion, slowing down from the 25.9% year-over-year increase in revenue the company had recorded in the same quarter last year. Ahead of the earnings results the analysts covering the company were estimating sales to grow 11.7% over the next twelve months.

In volatile times like these we look for robust businesses with strong pricing power. Unknown to most investors, this company is one of the highest-quality software companies in the world, and their software products have been the default standard in critical industries for decades. The result is an impressive business that is up an incredible 18,152% since the IPO. You can find it on our platform for free.

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Salesforce's gross profit margin, an important metric measuring how much money there is left after paying for servers, licenses, technical support and other necessary running expenses was at 73.3% in Q3.

That means that for every $1 in revenue the company had $0.73 left to spend on developing new products, marketing & sales and the general administrative overhead. Significantly up from the last quarter, this is around the average of what we typically see in SaaS businesses. Gross margin has a major impact on a company’s ability to invest in developing new products and sales & marketing, which may ultimately determine the winner in a competitive market, so it is important to track.

Key Takeaways from Salesforce's Q3 Results

Sporting a market capitalization of $151 billion, more than $11.9 billion in cash and with positive free cash flow over the last twelve months, we're confident that Salesforce has the resources it needs to pursue a high growth business strategy.

It was nice that Salesforce improved their gross margin, even if just slightly. That feature of these results really stood out as a positive. On the other hand, it was unfortunate to see that the revenue guidance for the next quarter slightly missed analysts' expectations and revenue growth is slower these days. Overall, this quarter's results could have been better. The company is down 5.37% on the results and currently trades at $151.17 per share.

Salesforce may have had a tough quarter, but does that actually create an opportunity to invest right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.