Customer relationship management software maker Salesforce (NYSE:CRM) reported results in line with analysts' expectations in Q3 FY2024, with revenue up 11.3% year on year to $8.72 billion. The company's full-year revenue guidance of $34.78 billion at the midpoint came in slightly above analysts' estimates. It made a non-GAAP profit of $2.11 per share, improving from its profit of $1.40 per share in the same quarter last year.

Is now the time to buy Salesforce? Find out by accessing our full research report, it's free.

Salesforce (CRM) Q3 FY2024 Highlights:

- Revenue: $8.72 billion vs analyst estimates of $8.72 billion (small beat)

- Current RPO (remaining performance obligations, a leading indicator of revenue) of $23.9 billion vs. estimates of $23.2 billion

- EPS (non-GAAP): $2.11 vs analyst estimates of $2.06 (2.6% beat)

- Revenue Guidance for Q4 2024 is $9.21 billion at the midpoint, roughly in line with what analysts were expecting

- Full year guidance raised for operating margin, EPS, and operating cash flow

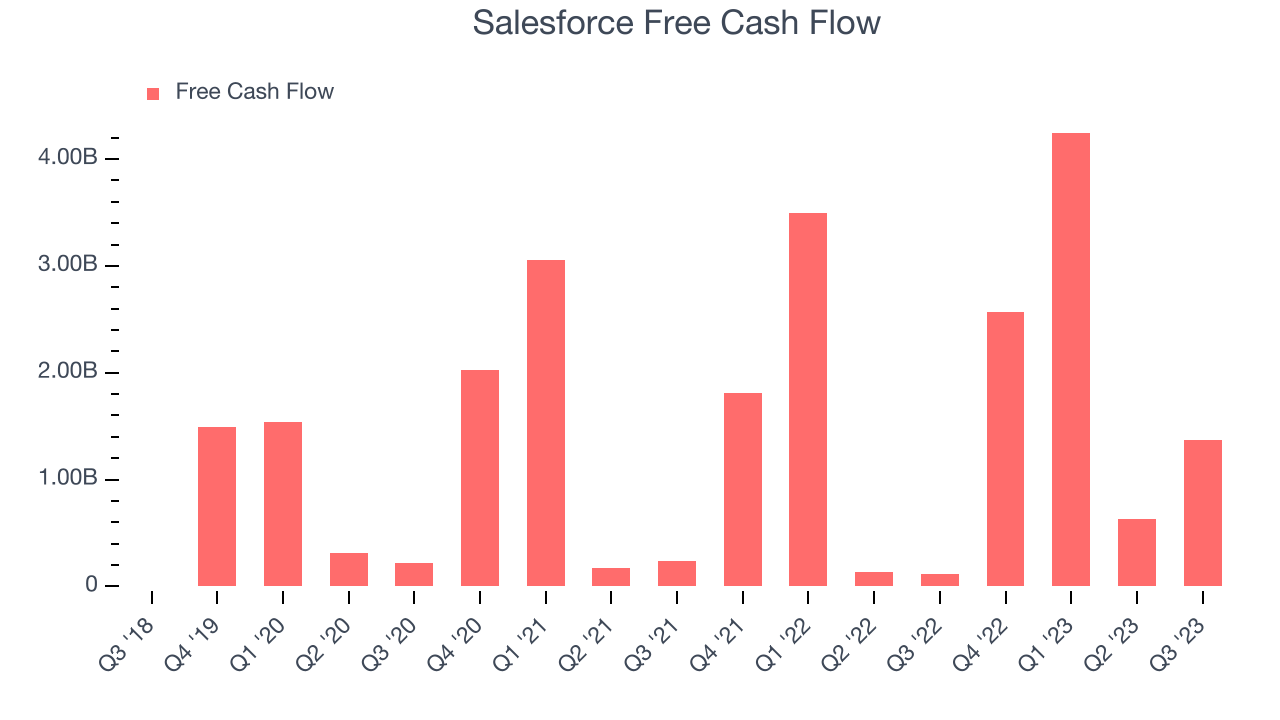

- Free Cash Flow of $1.37 billion, up 118% from the previous quarter (large beat vs. expectations of $683 million)

- Gross Margin (GAAP): 75.3%, up from 73.4% in the same quarter last year

“We had another strong quarter of executing on our profitable growth plan we set in motion last year, delivering $8.7 billion in revenue and again raising our operating margin guidance for this fiscal year,” said Marc Benioff, Chair and CEO, Salesforce.

Launched in 1999 from a rented one-bedroom apartment in San Francisco by Marc Benioff and his three co-founders, Salesforce (NYSE:CRM) is a software-as-a-service platform that helps companies access, manage, and share sales information.

Sales Software

Companies need to be able to interact with and sell to their customers as efficiently as possible. This reality coupled with the ongoing migration of enterprises to the cloud drives demand for cloud-based customer relationship management (CRM) software that integrates data analytics with sales and marketing functions.

Sales Growth

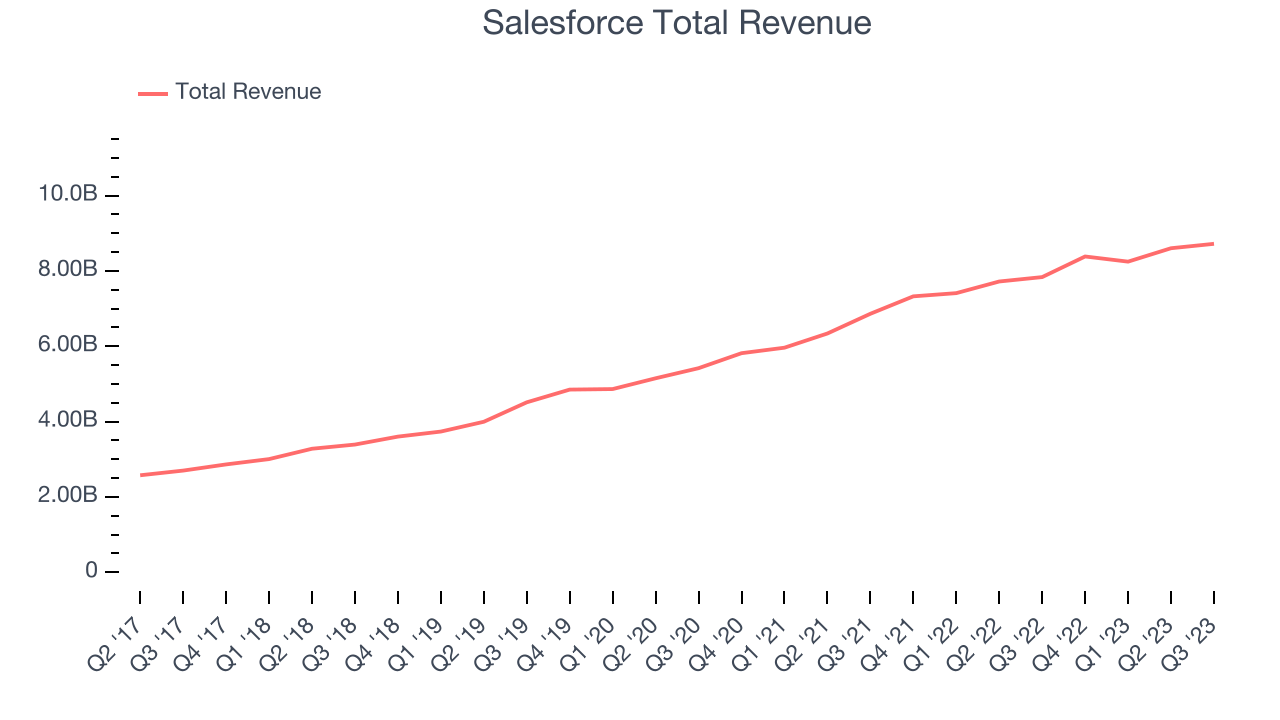

As you can see below, Salesforce's revenue growth has been mediocre over the last two years, growing from $6.86 billion in Q3 FY2022 to $8.72 billion this quarter.

This quarter, Salesforce's quarterly revenue was once again up 11.3% year on year. However, its growth did slow down compared to last quarter as the company's revenue increased by just $117 million in Q3 compared to $356 million in Q2 2024. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Next quarter, Salesforce is guiding for a 8.9% year-on-year revenue decline to $9.21 billion, a further deceleration from the 14.4% year-on-year decrease it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 10.5% over the next 12 months before the earnings results announcement.

Our recent pick has been a big winner, and the stock is up more than 2,000% since the IPO a decade ago. If you didn’t buy then, you have another chance today. The business is much less risky now than it was in the years after going public. The company is a clear market leader in a huge, growing $200 billion market. Its $7 billion of revenue only scratches the surface. Its products are mission critical. Virtually no customers ever left the company. You can find it on our platform for free.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Salesforce's free cash flow came in at $1.37 billion in Q3, up 1,088% year on year.

Salesforce has generated $8.81 billion in free cash flow over the last 12 months, an eye-popping 26.3% of revenue. This robust FCF margin stems from its asset-lite business model, scale advantages, and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a healthy cash balance.

Key Takeaways from Salesforce's Q3 Results

Sporting a market capitalization of $218.8 billion, more than $11.86 billion in cash on hand, and positive free cash flow over the last 12 months, we believe that Salesforce is attractively positioned to invest in growth.

Revenue beat by a narrow amount but both current and total RPO (remaining performance obligations, a leading indicator of revenue) beat more convincingly. In addition, non-GAAP operating profit and non-GAAP EPS outperformed expectations. Free cash flow was yet another bright spot, outperforming by a large magnitude and giving the company ample firepower to invest organically or return capital to shareholders. While next quarter's revenue guidance was roughly in line, non-GAAP EPS guidance was ahead. Finally, full year fiscal 2024 guidance was raised slightly for revenue but more convincingly for operating margin, EPS, and operating cash flow. Overall, the results were not perfect but were very solid. The stock is up 5% after reporting and currently trades at $242.05 per share.

So should you invest in Salesforce right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.