As sales software stocks’ Q1 earnings season wraps, let's dig into this quarter's best and worst performers, including Salesforce (NYSE:CRM) and its peers.

Companies need to be able to interact with and sell to their customers as efficiently as possible. This reality, coupled with the ongoing migration of enterprises to the cloud drives demand for cloud-based customer relationship management (CRM) software that integrate data analytics with sales and marketing functions.

The 4 sales software stocks we track reported a mixed Q1; on average, revenues beat analyst consensus estimates by 2.29%, while on average next quarter revenue guidance was 0.37% above consensus. There has been a stampede out of high valuation technology stocks as raising interest rates encourage investors to value profits over growth again, but sales software stocks held their ground better than others, with the share prices up 18.3% since the previous earnings results, on average.

Salesforce (NYSE:CRM)

Launched in 1999 from a rented one-bedroom apartment in San Francisco by Marc Benioff and his three co-founders, Salesforce (NYSE:CRM) is a software as a service platform that helps companies access, manage and share sales information.

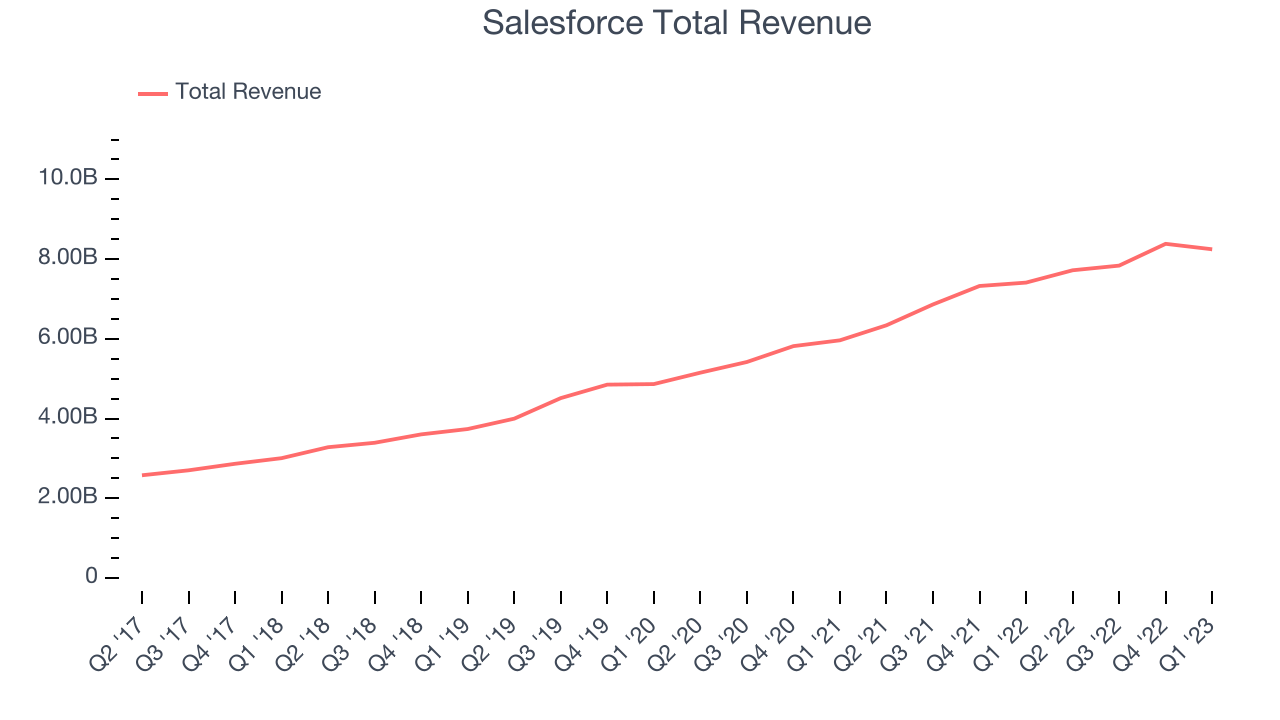

Salesforce reported revenues of $8.25 billion, up 11.3% year on year, in line with analyst expectations. It was a mixed quarter for the company, with revenue and remaining performance obligations (RPO, a leading indicator of revenue) beating analysts' estimates. However, revenue guidance for the full year was reiterated and slightly missed analysts' expectations.

“Salesforce significantly exceeded our non-GAAP margin target for the quarter — up 1,000 basis points year-over-year, and we are raising our FY24 non-GAAP operating margin guidance to a 550 basis point increase year-over-year,” said Marc Benioff, Chair and CEO of Salesforce.

Salesforce delivered the slowest revenue growth and weakest full year guidance update of the whole group. The stock is down 5.55% since the results and currently trades at $211.66.

Read our full report on Salesforce here, it's free.

Best Q1: HubSpot (NYSE:HUBS)

Started in 2006 by two MIT grad students, HubSpot (NYSE:HUBS) is a software as a service platform that helps small and medium-size businesses sell, market themselves, and get found on the internet.

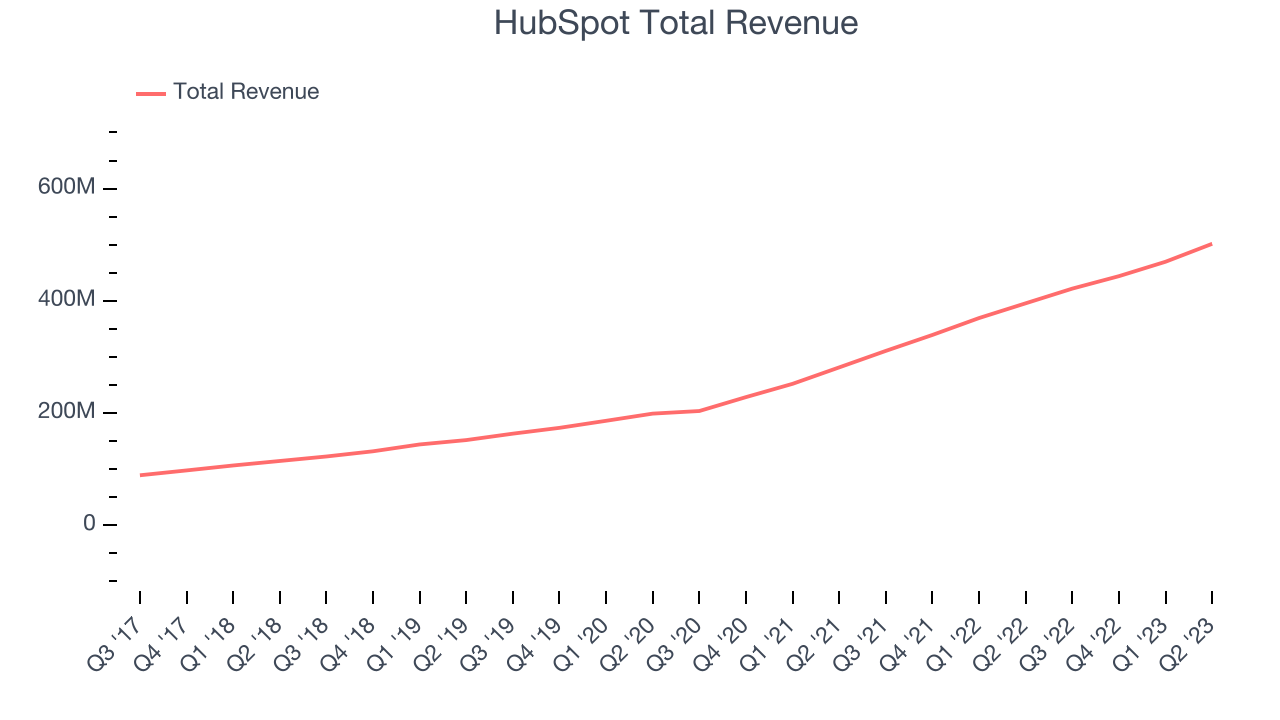

HubSpot reported revenues of $501.6 million, up 26.8% year on year, beating analyst expectations by 5.63%. It was a very strong quarter for the company, with a solid beat of analyst estimates and accelerating customer growth.

HubSpot delivered the strongest analyst estimates beat, fastest revenue growth, and highest full year guidance raise among its peers. The company added 9,912 customers to a total of 177,298. The stock is up 24.2% since the results and currently trades at $519.

Is now the time to buy HubSpot? Access our full analysis of the earnings results here, it's free.

Weakest Q1: ZoomInfo (NASDAQ:ZI)

Founded in 2007 as DiscoveryOrg and renamed after a merger in 2019, ZoomInfo (NASDAQ:ZI) is a software as a service product that provides sales departments with access to a database of prospective clients.

ZoomInfo reported revenues of $300.7 million, up 24.4% year on year, in line with analyst expectations. It was a weaker quarter for the company, with decelerating growth in large customers.

ZoomInfo had the weakest performance against analyst estimates in the group. The company lost 21 enterprise customers paying more than $100,000 annually and ended up with a total of 1,905. The stock is up 21.1% since the results and currently trades at $26.3.

Read our full analysis of ZoomInfo's results here.

Freshworks (NASDAQ:FRSH)

Founded in Chennai, India in 2010 with the idea of creating a “fresh” helpdesk product, Freshworks (NASDAQ: FRSH) offers a broad range of software targeted at small and medium sized businesses.

Freshworks reported revenues of $137.7 million, up 20.1% year on year, beating analyst expectations by 2.57%. It was a mixed quarter for the company, with a decent beat of key performance metrics but decelerating growth in large customers.

The company added 719 enterprise customers paying more than $5,000 annually to a total of 18,441. The stock is up 33.7% since the results and currently trades at $17.22.

Read our full, actionable report on Freshworks here, it's free.

The author has no position in any of the stocks mentioned