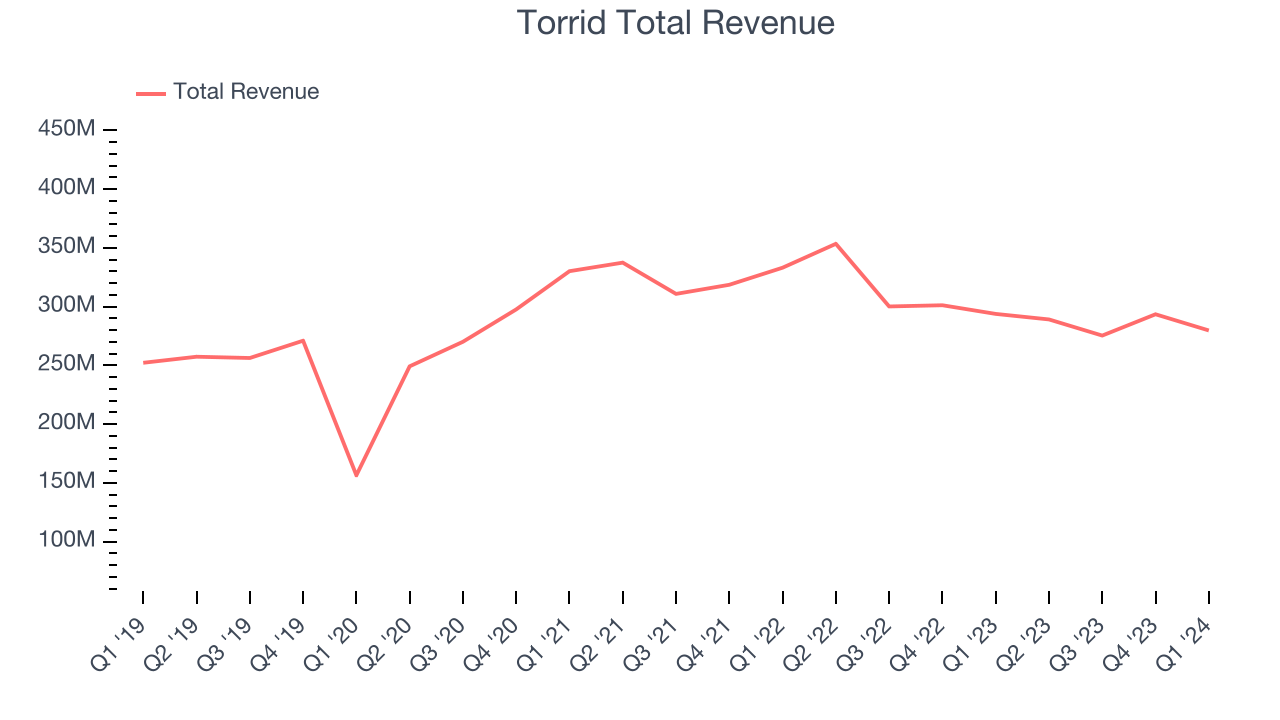

Women’s plus-size apparel retailer Torrid Holdings (NYSE:CURV) reported results in line with analysts' expectations in Q1 CY2024, with revenue down 4.8% year on year to $279.8 million. On the other hand, next quarter's revenue guidance of $282.5 million was less impressive, coming in 1.9% below analysts' estimates. It made a GAAP profit of $0.12 per share, improving from its profit of $0.11 per share in the same quarter last year.

Is now the time to buy Torrid? Find out by accessing our full research report, it's free.

Torrid (CURV) Q1 CY2024 Highlights:

- Revenue: $279.8 million vs analyst estimates of $280.5 million (small miss)

- Revenue Guidance for Q2 CY2024 is $282.5 million at the midpoint, below analyst estimates of $287.9 million

- The company reconfirmed its revenue guidance for the full year of $1.15 billion at the midpoint (slightly raised full year adjusted EBITDA guidance)

- Gross Margin (GAAP): 41.3%, up from 37.7% in the same quarter last year

- Free Cash Flow of $20.62 million, up from $5.56 million in the same quarter last year

- Locations: 658 at quarter end, up from 638 in the same quarter last year

- Same-Store Sales fell 9% year on year (-14% in the same quarter last year)

- Market Capitalization: $694.8 million

Lisa Harper, Chief Executive Officer, stated, “We are pleased with our start to fiscal 2024. In the first quarter we delivered higher-than-expected Adjusted EBITDA(1) driven by strong gross margin expansion, while maintaining our focus on tightly controlling inventory levels. Our customers responded positively to our ongoing assortment changes, leading to improved traffic and sales throughout the quarter.”

Promoting a message of body positivity and inclusiveness, Torrid Holdings (NYSE:CURV) is a plus-size women’s apparel and accessories retailer.

Apparel Retailer

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

Sales Growth

Torrid is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale.

As you can see below, the company's annualized revenue growth rate of 3.3% over the last five years was sluggish , but to its credit, it opened new stores and expanded its reach.

This quarter, Torrid missed Wall Street's estimates and reported a rather uninspiring 4.8% year-on-year revenue decline, generating $279.8 million in revenue. The company is guiding for a 2.3% year-on-year revenue decline next quarter to $282.5 million, an improvement from the 18.2% year-on-year decrease it recorded in the same quarter last year.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Same-Store Sales

A company's same-store sales growth shows the year-on-year change in sales for its brick-and-mortar stores that have been open for at least a year, give or take, and e-commerce platform. This is a key performance indicator for retailers because it measures organic growth and demand.

Torrid's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 8.8% year on year. This performance is quite concerning and the company should reconsider its strategy before investing its precious capital into new store buildouts.

In the latest quarter, Torrid's same-store sales fell 9% year on year. This decrease was a further deceleration from the 14% year-on-year decline it posted 12 months ago. We hope the business can get back on track.

Key Takeaways from Torrid's Q1 Results

We were impressed by how significantly Torrid blew past analysts' EPS expectations this quarter. We were also excited its gross margin outperformed Wall Street's estimates. On the other hand, its revenue guidance for next quarter was underwhelming. However, offsetting that negative was the fact that the company reaffirmed full year revenue guidance previously given while slightly raising full year adjusted EBITDA guidance previously given. Overall, we think this was a strong quarter that should satisfy shareholders. The stock is up 5.8% after reporting and currently trades at $7.06 per share.

Torrid may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.