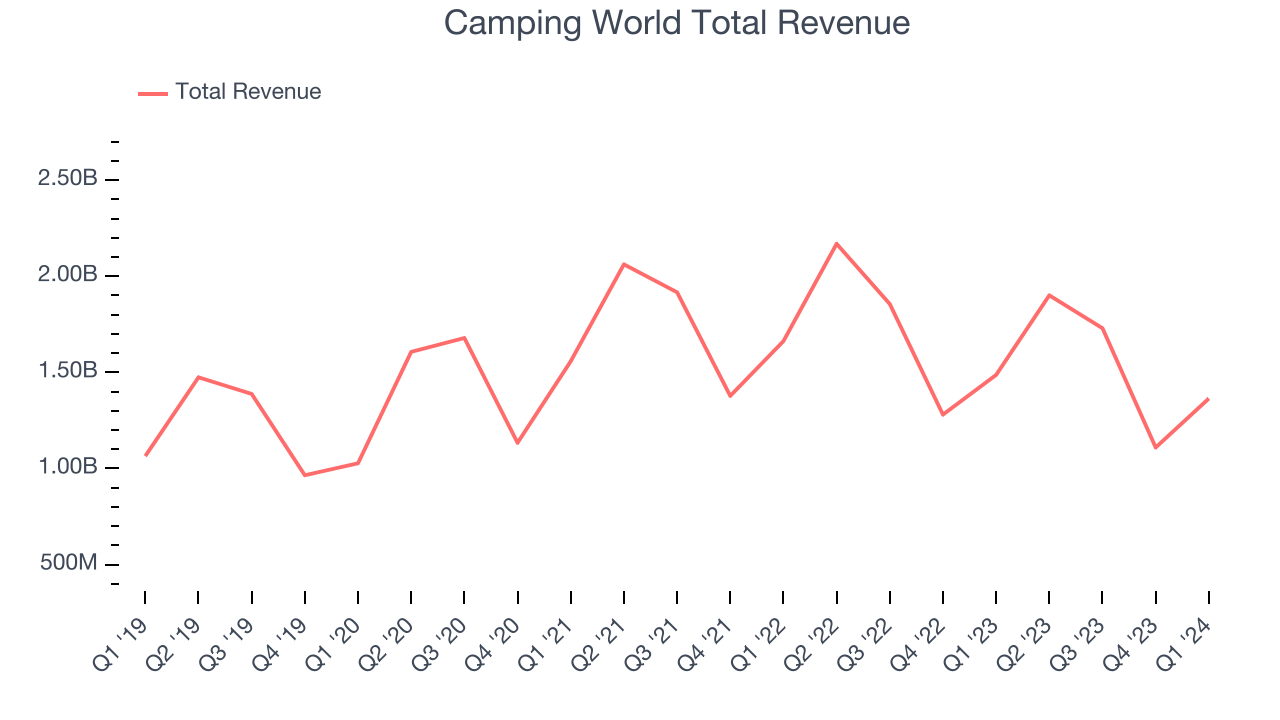

Recreational vehicle (RV) and boat retailer Camping World (NYSE:CWH) missed analysts' expectations in Q1 CY2024, with revenue down 8.3% year on year to $1.36 billion. It made a GAAP loss of $0.51 per share, down from its profit of $0.05 per share in the same quarter last year.

Camping World (CWH) Q1 CY2024 Highlights:

- Revenue: $1.36 billion vs analyst estimates of $1.43 billion (4.4% miss)

- Adjusted EBITDA: $8.2 million vs analyst estimates of $7.4 million (beat)

- EPS: -$0.51 vs analyst expectations of -$0.36 (miss)

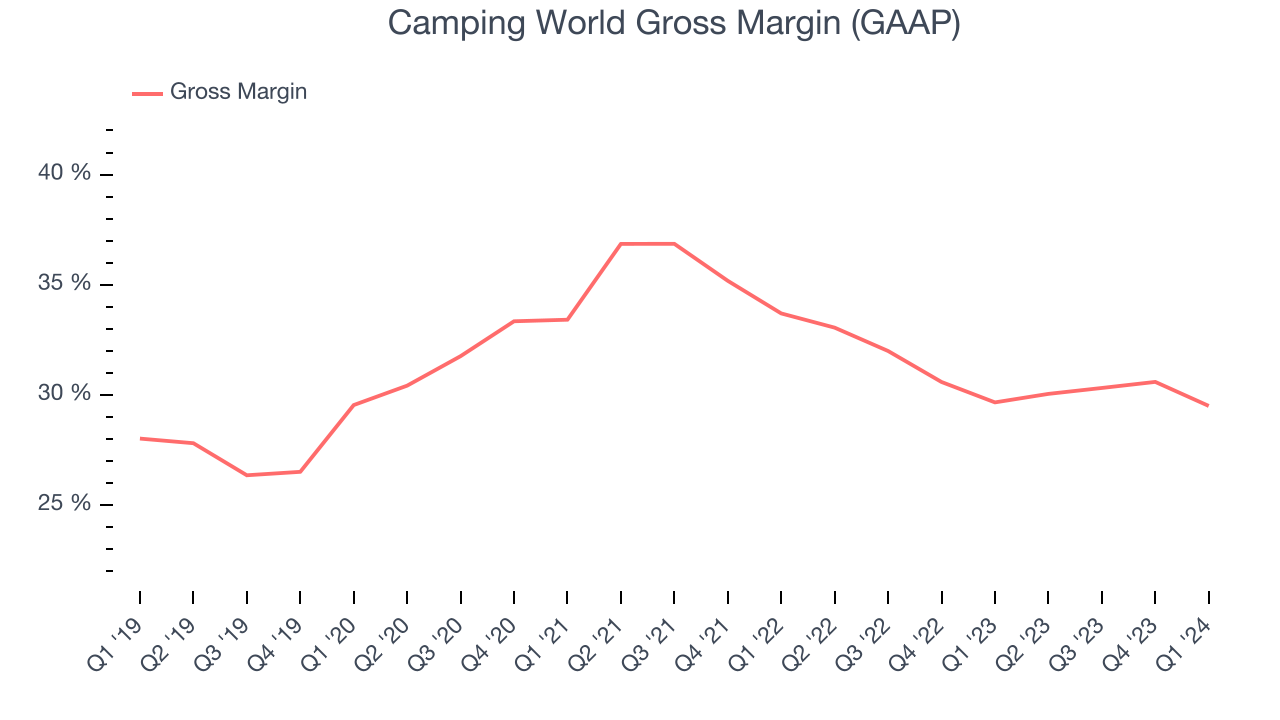

- Gross Margin (GAAP): 29.5%, in line with the same quarter last year

- Free Cash Flow was -$93.91 million, down from $173.9 million in the same quarter last year

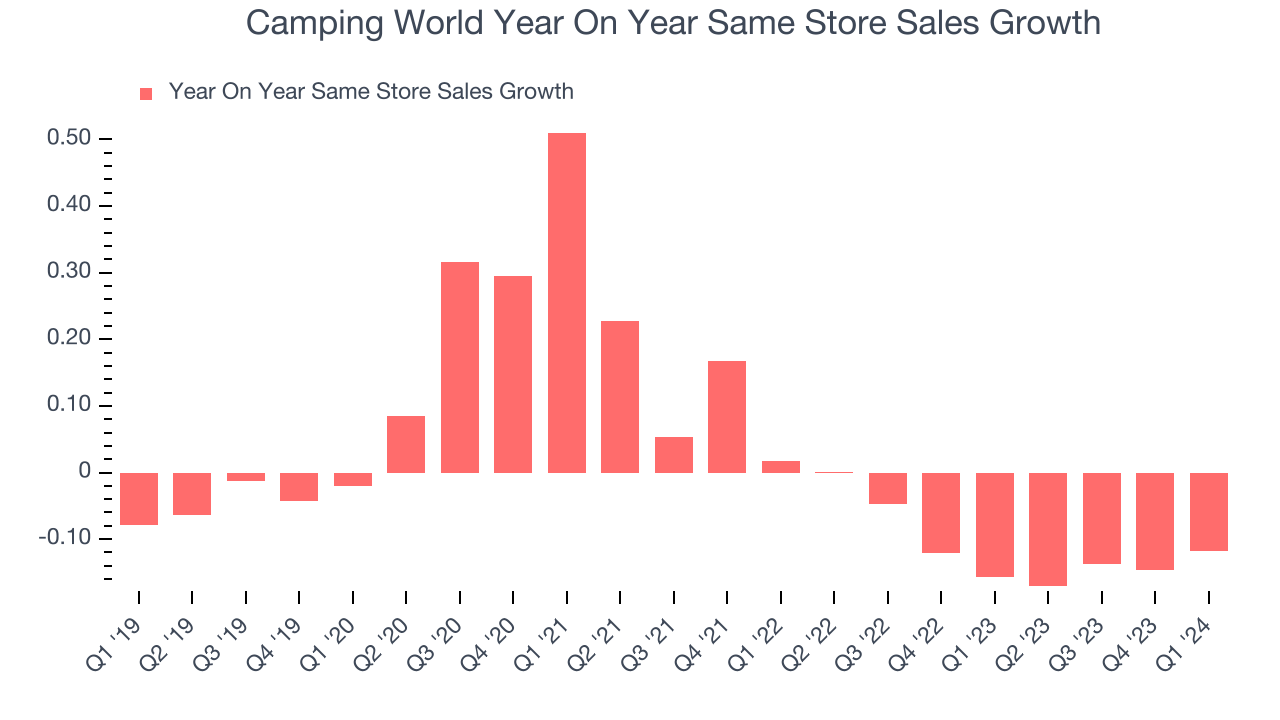

- Same-Store Sales were down 11.8% year on year (beat vs. expectations of down 14.3% year on year)

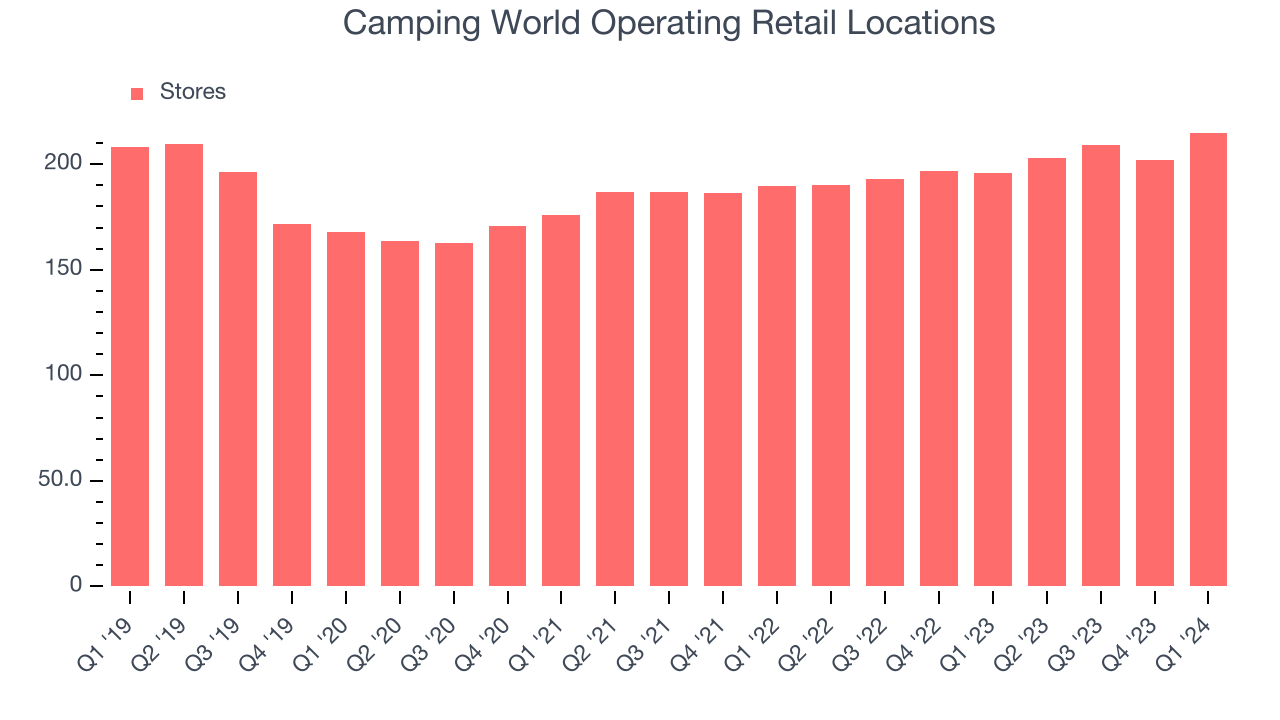

- Store Locations: 215 at quarter end, increasing by 19.3 over the last 12 months

- Market Capitalization: $913.6 million

Founded in 1966 as a single recreational vehicle (RV) dealership, Camping World (NYSE:CWH) still sells RVs along with boats and general merchandise for outdoor activities.

The core customer is someone in the market for an RV, someone who already owns an RV, or a general outdoor enthusiast. At a Camping World location or on the company’s website, this core customer can buy RVs, boats, camping tents, fishing rods, and all manner of equipment to accompany your RV or boat.

The average Camping World store is around 20,000 square feet and is typically located in or near popular camping destinations or along major highways. RVs are displayed outside, while camping gear and accessories are arranged inside the store in sections. States such as Florida, Texas, and Ohio have the highest concentration of Camping World stores while Northeastern states, where the weather isn’t as conducive to outdoor activities, have the lowest.

Camping World’s e-commerce presence was launched in 2008, and today, customers can buy the company’s offerings online for direct shipment. Camping World's e-commerce platform has been an important part of reaching customers who may not have easy access to a physical store.

Vehicle Retailer

Buying a vehicle is a big decision and usually the second-largest purchase behind a home for many people, so retailers that sell new and used cars try to offer selection, convenience, and customer service to shoppers. While there is online competition, especially for research and discovery, the vehicle sales market is still very fragmented and localized given the magnitude of the purchase and the logistical costs associated with moving cars over long distances. At the end of the day, a large swath of the population relies on cars to get from point A to point B, and vehicle sellers are acutely aware of this need.

Competitors offering merchandise for outdoor activities or recreational vehicles include Thor Industries (NYSE:THO) and Winnebago Industries (NYSE:WGO) as well as private competitors such as Lazydays Holdings and General RV Center.Sales Growth

Camping World is larger than most consumer retail companies and benefits from economies of scale, giving it an edge over its competitors.

As you can see below, the company's annualized revenue growth rate of 4.9% over the last five years was weak , but to its credit, it opened new stores and expanded its reach.

This quarter, Camping World missed Wall Street's estimates and reported a rather uninspiring 8.3% year-on-year revenue decline, generating $1.36 billion in revenue. Looking ahead, Wall Street expects sales to grow 9.9% over the next 12 months, an acceleration from this quarter.

Same-Store Sales

Camping World's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 11.2% year on year. This performance is quite concerning and the company should reconsider its strategy before investing its precious capital into new store buildouts.

In the latest quarter, Camping World's same-store sales fell 11.8% year on year. This decrease was a further deceleration from the 15.7% year-on-year decline it posted 12 months ago. We hope the business can get back on track.

Number of Stores

A retailer's store count often determines on how much revenue it can generate.

When a retailer like Camping World is opening new stores, it usually means it's investing for growth because demand is greater than supply. Camping World's store count increased by 19.3 locations, or 9.8%, over the last 12 months to 215 total retail locations in the most recently reported quarter.

Over the last two years, the company has opened new stores quickly and averaged 5.2% annual growth in new locations, meaningfully higher than other consumer retail businesses. With an expanding store base and demand, revenue growth can come from multiple vectors: sales from new stores, sales from e-commerce, or increased foot traffic and higher sales per customer at existing stores.

Gross Margin & Pricing Power

Gross profit margins tell us how much money a retailer gets to keep after paying for the goods it sells.

Camping World has weak unit economics for a retailer, making it difficult to reinvest in the business. As you can see below, it's averaged a 30.9% gross margin over the last eight quarters. This means the company makes $0.31 for every $1 in revenue before accounting for its operating expenses.

Camping World produced a 29.5% gross profit margin in Q1, flat with the same quarter last year. This steady margin stems from its efforts to keep prices low for consumers and signals that it has stable input costs (such as freight expenses to transport goods).

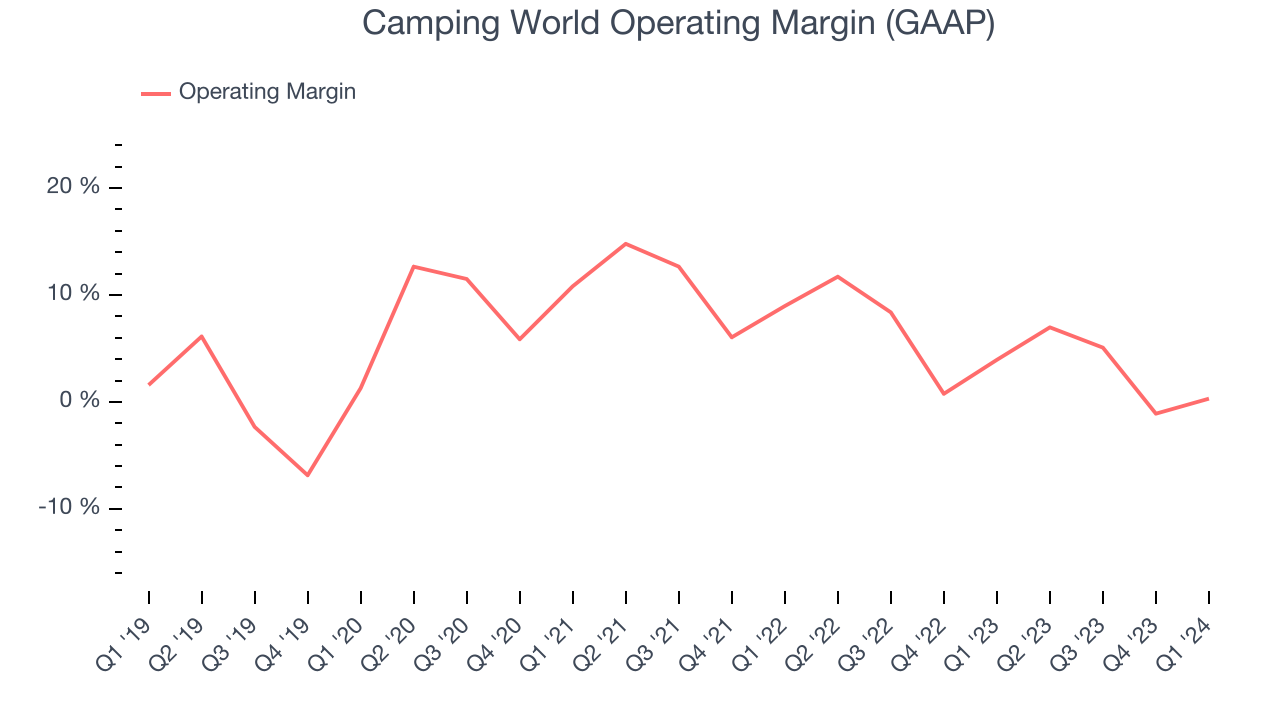

Operating Margin

Operating margin is an important measure of profitability for retailers as it accounts for all expenses keeping the lights on, including wages, rent, advertising, and other administrative costs.

This quarter, Camping World generated an operating profit margin of 0.3%, down 3.6 percentage points year on year. We can infer Camping World was less efficient with its expenses or had lower leverage on its fixed costs because its operating margin decreased more than its gross margin.

Zooming out, Camping World was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer retail business, producing an average operating margin of 5.4%. On top of that, Camping World's margin has declined, on average, by 3.6 percentage points year on year. This shows the company is heading in the wrong direction, and investors were likely hoping for better results.

Zooming out, Camping World was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer retail business, producing an average operating margin of 5.4%. On top of that, Camping World's margin has declined, on average, by 3.6 percentage points year on year. This shows the company is heading in the wrong direction, and investors were likely hoping for better results.EPS

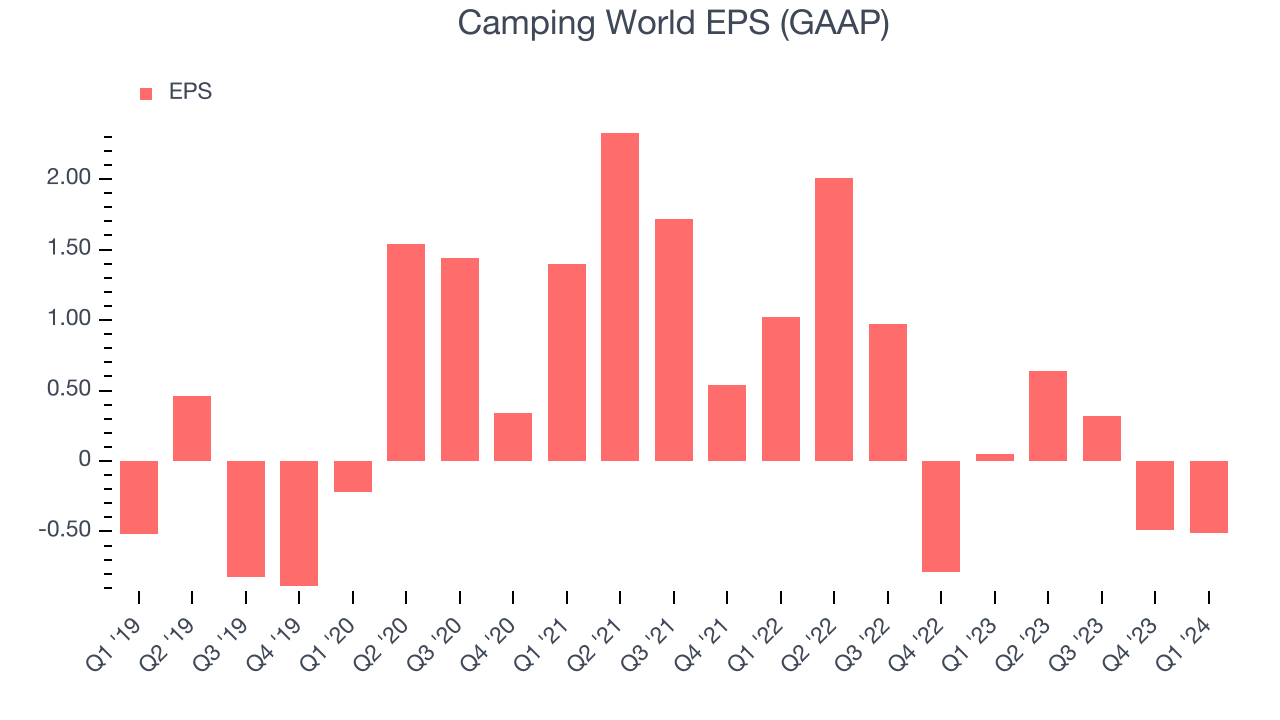

These days, some companies issue new shares like there's no tomorrow. That's why we like to track earnings per share (EPS) because it accounts for shareholder dilution and share buybacks.

In Q1, Camping World reported EPS at negative $0.51, down from $0.05 in the same quarter a year ago. This print unfortunately missed Wall Street's estimates, but we care more about long-term EPS growth rather than short-term movements.

Wall Street expects the company to continue growing earnings over the next 12 months, with analysts projecting an average 3,148% year-on-year increase in EPS.

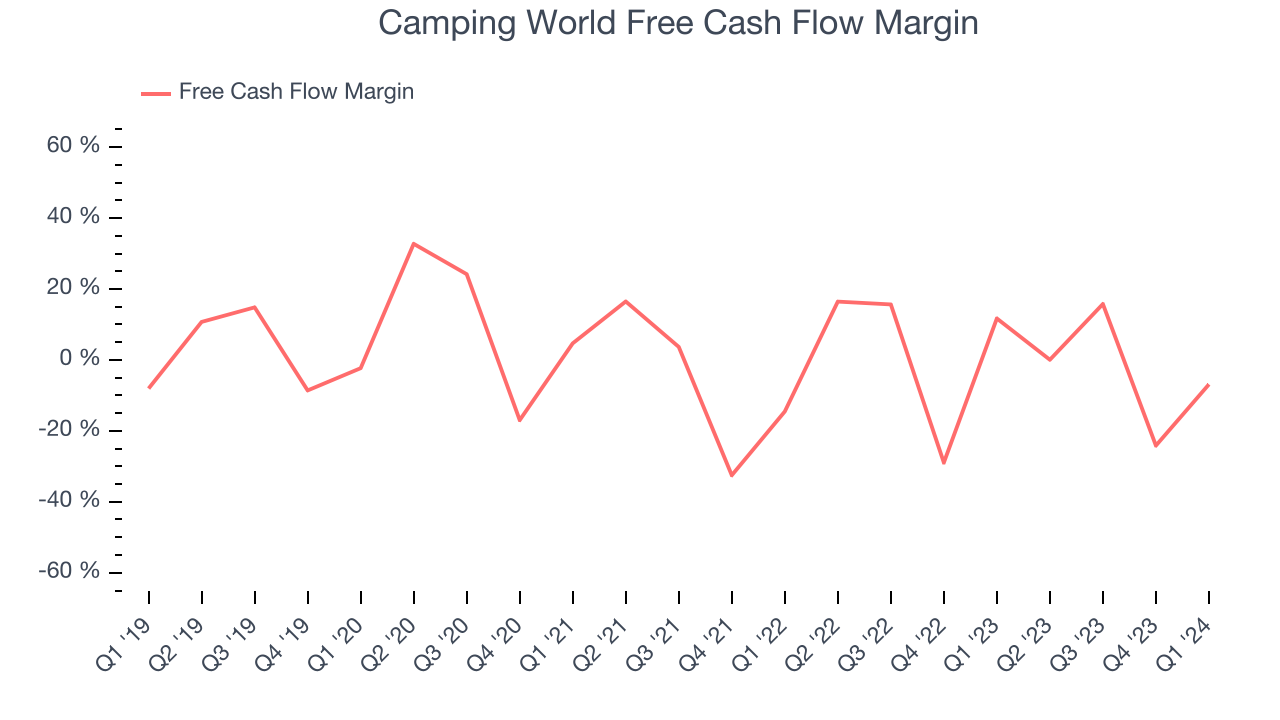

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Camping World burned through $93.91 million of cash in Q1, representing a negative 6.9% free cash flow margin. The company shifted to cash flow negative from cash flow positive in the same quarter last year, which happened for several reasons including (but not limited to) the stockpiling of inventory in anticipation of higher demand or unforeseen, one-time events.

Over the last two years, Camping World has shown decent cash profitability, giving it some reinvestment opportunities. The company's free cash flow margin has averaged 2.8%, slightly better than the broader consumer retail sector. However, its margin has averaged year-on-year declines of 8.1 percentage points. Some investors are likely unhappy with this and would hope to see a reversal soon.

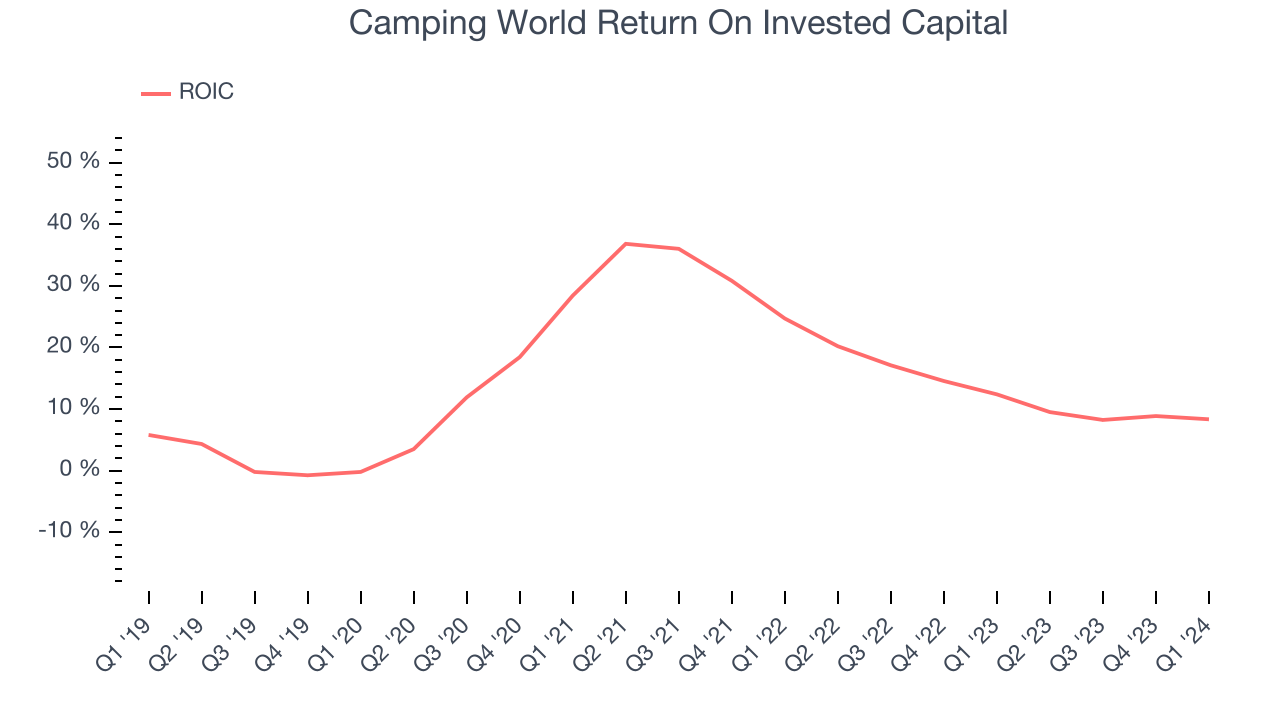

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Camping World's five-year average ROIC was 14.7%, somewhat low compared to the best retail companies that consistently pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Camping World's ROIC averaged 3.7 percentage point decreases over the last few years. Paired with its already low returns, these declines suggest the company's profitable business opportunities are few and far between.

Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly.

Camping World's $1.60 billion of debt exceeds the $29.72 million of cash on its balance sheet. Furthermore, its 6x net-debt-to-EBITDA ratio (based on its EBITDA of $283.2 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Camping World could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Camping World can improve its balance sheet and remain cautious until it increases its profitability or reduces its debt.

Key Takeaways from Camping World's Q1 Results

The results were mixed as the environment in which the company operates remains in flux. While same store sales were down meaningfully and have been down for multiple quarters, this quarter's figure beat expectations. Adjusted EBITDA also exceeded expectations. Management stated that the company has been “...successful in rebalancing our used inventory position and now that market pricing has stabilized, we intend to reinvest in building our stocking levels in a disciplined manner over the coming months. We continue to expect our used business to improve as we move through the balance of the year.” The stock is up 1.2% after reporting and currently trades at $20.29 per share.

Is Now The Time?

Camping World may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

Camping World isn't a bad business, but it probably wouldn't be one of our picks. Its revenue growth has been a little slower over the last five years, but at least growth is expected to increase in the short term. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its shrinking same-store sales suggests it'll need to change its strategy to succeed. On top of that, its gross margins make it more difficult to reach positive operating profits compared to other consumer retail businesses.

Camping World's price-to-earnings ratio based on the next 12 months is 12.9x. We don't really see a big opportunity in the stock at the moment, but in the end, beauty is in the eye of the beholder. If you like Camping World, it seems to be trading at a reasonable price.

Wall Street analysts covering the company had a one-year price target of $30.09 per share right before these results (compared to the current share price of $20.29).

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.