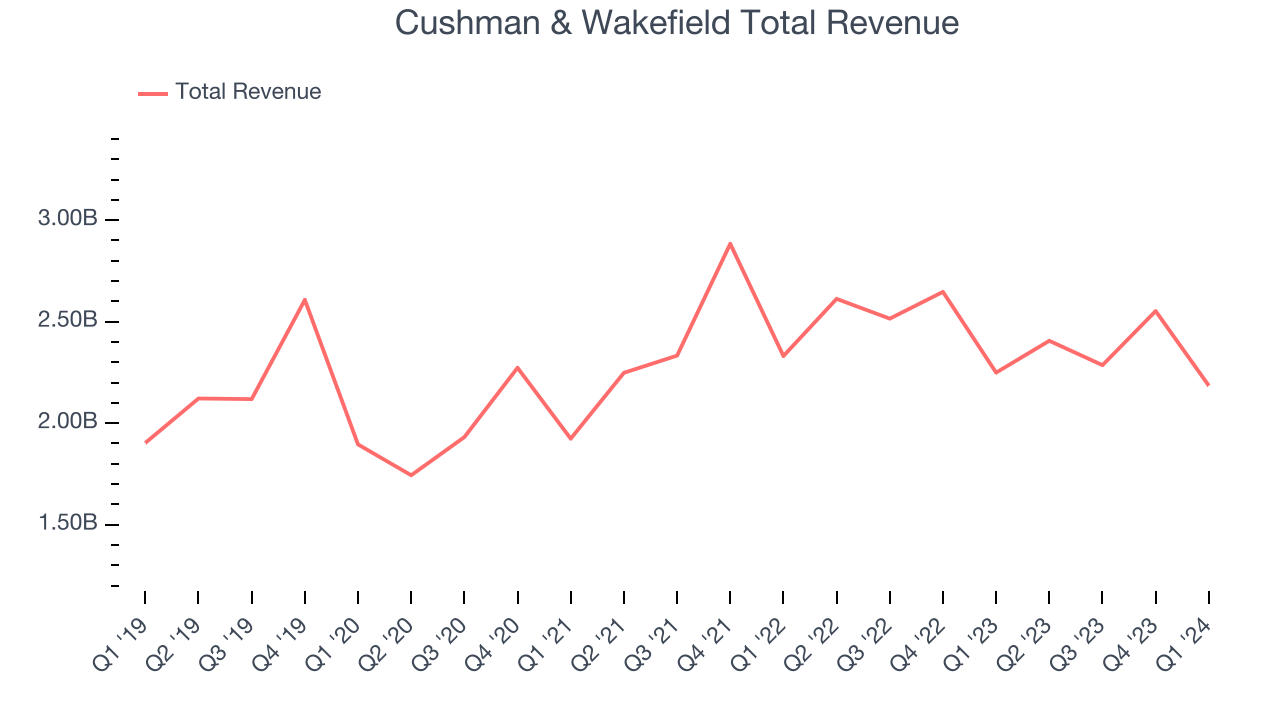

Real estate services firm Cushman & Wakefield (NYSE:CWK) reported results in line with analysts' expectations in Q1 CY2024, with revenue down 2.9% year on year to $2.18 billion. It made a non-GAAP loss of $0 per share, improving from its loss of $0.04 per share in the same quarter last year.

Is now the time to buy Cushman & Wakefield? Find out by accessing our full research report, it's free.

Cushman & Wakefield (CWK) Q1 CY2024 Highlights:

- Revenue: $2.18 billion vs analyst estimates of $2.17 billion (small beat)

- EPS (non-GAAP): $0 vs analyst estimates of -$0.01 ($0.01 beat)

- Gross Margin (GAAP): 16.1%, up from 15.2% in the same quarter last year

- Free Cash Flow was -$135.6 million, down from $199.6 million in the previous quarter

- Market Capitalization: $2.23 billion

“We reported strong first quarter results that demonstrate the breadth and strength of our service offerings as well as our commitment to executing consistently on our strategic priorities,” said Michelle MacKay, Cushman & Wakefield Chief Executive Officer.

With expertise in the commercial real estate sector, Cushman & Wakefield (NYSE:CWK) is a global Chicago-based real estate firm offering a comprehensive range of services to clients.

Real Estate Services

Technology has been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

Sales Growth

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Cushman & Wakefield's annualized revenue growth rate of 2.4% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Cushman & Wakefield's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 1.9% over the last two years.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Cushman & Wakefield's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 1.9% over the last two years.

We can dig even further into the company's revenue dynamics by analyzing its three most important segments: Management, Leasing, and Capital Markets, which are 39.9%, 17.5%, and 6.5% of revenue. Over the last two years, Cushman & Wakefield's Management revenue (property management) averaged 4.5% year-on-year growth while its Leasing (sourcing tenants) and Capital Markets (financial advisory) revenues averaged declines of 3% and 25.8%.

This quarter, Cushman & Wakefield reported a rather uninspiring 2.9% year-on-year revenue decline to $2.18 billion of revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 3.4% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

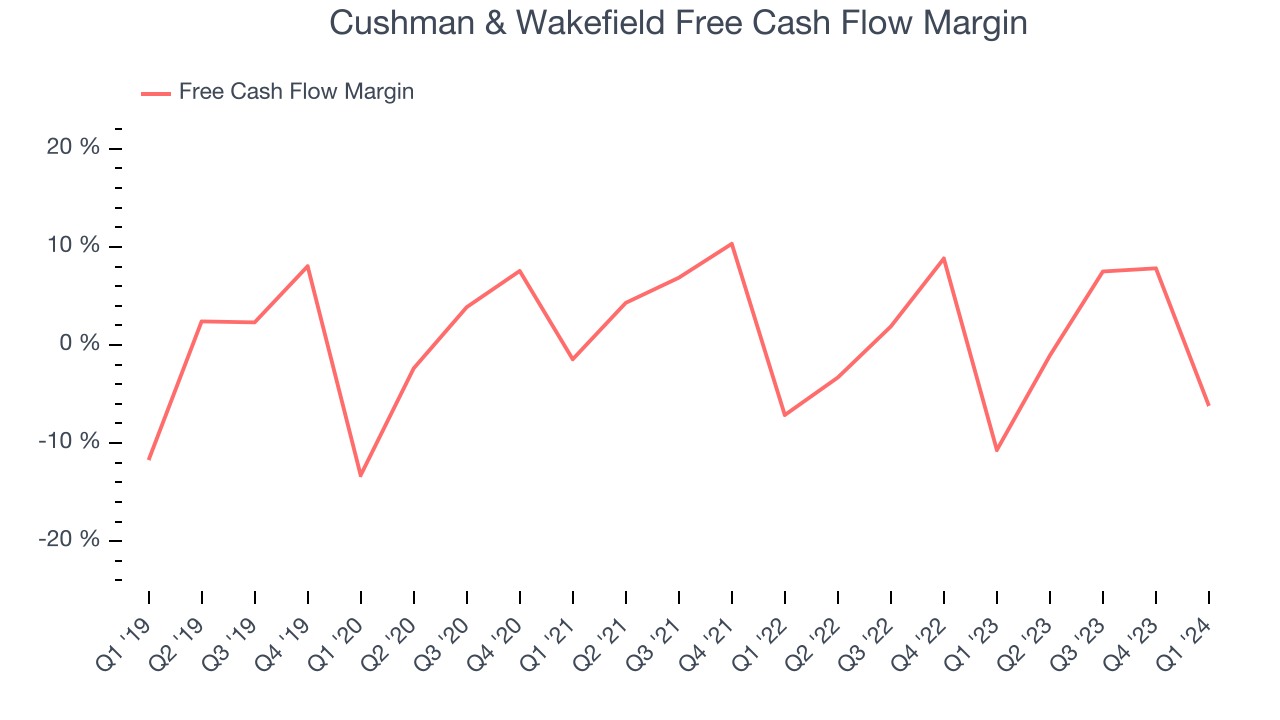

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, Cushman & Wakefield broke even from a free cash flow perspective, subpar for a consumer discretionary business.

Cushman & Wakefield burned through $135.6 million of cash in Q1, equivalent to a negative 6.2% margin, increasing its cash burn by 43.7% year on year.

Key Takeaways from Cushman & Wakefield's Q1 Results

It was good to see Cushman & Wakefield beat analysts' revenue, EPS, and EBITDA expectations this quarter, driven by better-than-expected performance in its capital markets segment. The company also restructured $1 billion of debt, which is projected to save $6 million annually. Overall, this quarter's results seemed fairly positive. The stock is flat after reporting and currently trades at $9.91 per share.

So should you invest in Cushman & Wakefield right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.