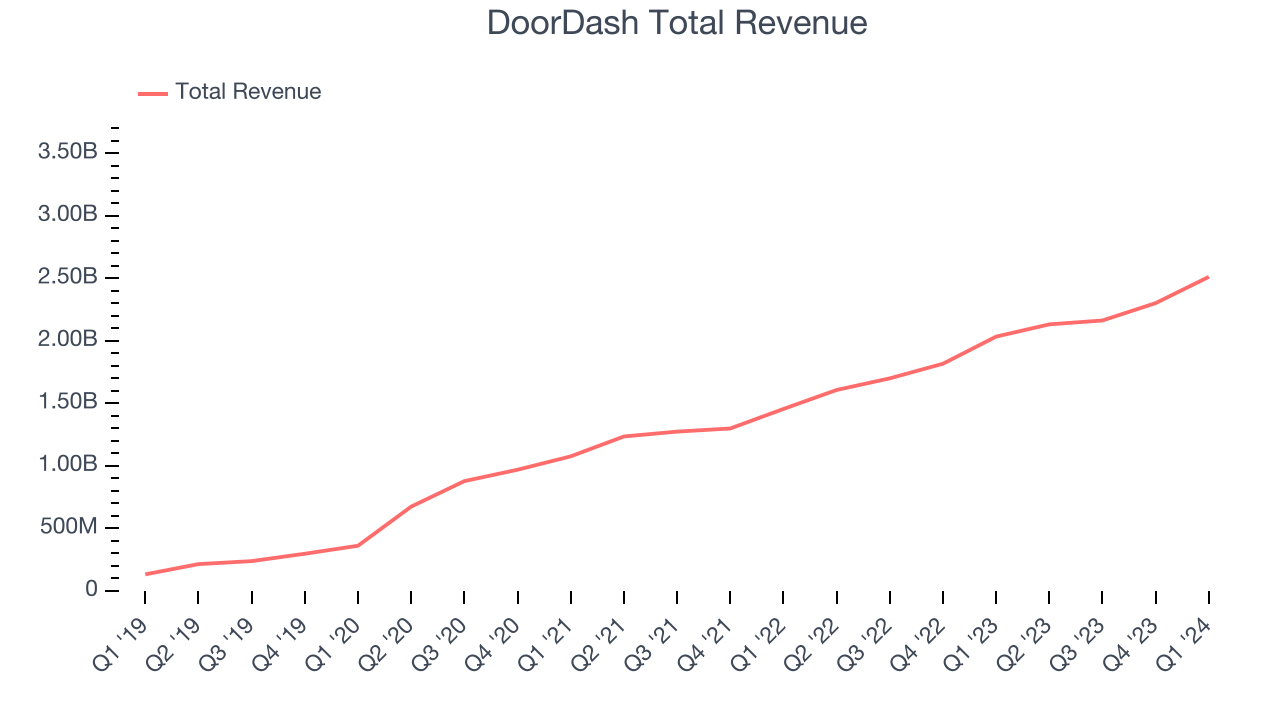

On-demand food delivery service DoorDash (NYSE:DASH) beat analysts' expectations in Q1 CY2024, with revenue up 23.5% year on year to $2.51 billion. It made a GAAP loss of $0.06 per share, improving from its loss of $0.41 per share in the same quarter last year.

Is now the time to buy DoorDash? Find out by accessing our full research report, it's free.

DoorDash (DASH) Q1 CY2024 Highlights:

- Revenue: $2.51 billion vs analyst estimates of $2.45 billion (2.5% beat)

- Adjusted EBITDA: $371 million vs analyst estimates of $365 million (1.6% beat)

- Adjusted EBITDA guidance for Q2 2024: $375 million vs analyst estimates of $390 million (3.8% miss)

- EPS: -$0.06 vs analyst expectations of -$0.05 (25.8% miss)

- Gross Margin (GAAP): 47.1%, in line with the same quarter last year

- Free Cash Flow of $487 million, up 22.4% from the previous quarter

- Orders: 620 million vs analyst expectations of 606.5 million (2.2% beat)

- Market Capitalization: $52.22 billion

Founded by Stanford students with the intent to build “the local, on-demand FedEx", DoorDash (NYSE:DASH) operates an on-demand food delivery platform.

Gig Economy

The iPhone changed the world, ushering in the era of the “always-on” internet and “on-demand” services - anything someone could want is just a few taps away. Likewise, the gig economy sprang up in a similar fashion, with a proliferation of tech-enabled freelance labor marketplaces, which work hand and hand with many on demand services. Individuals can now work on demand too. What began with tech enabled platforms that aggregated riders and drivers has expanded over the past decade to include food delivery, groceries, and now even a plumber or graphic designer are all just a few taps away.

Sales Growth

DoorDash's revenue growth over the last three years has been very strong, averaging 37.5% annually. This quarter, DoorDash beat analysts' estimates and reported decent 23.5% year-on-year revenue growth.

Ahead of the earnings results, analysts were projecting sales to grow 16.3% over the next 12 months.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

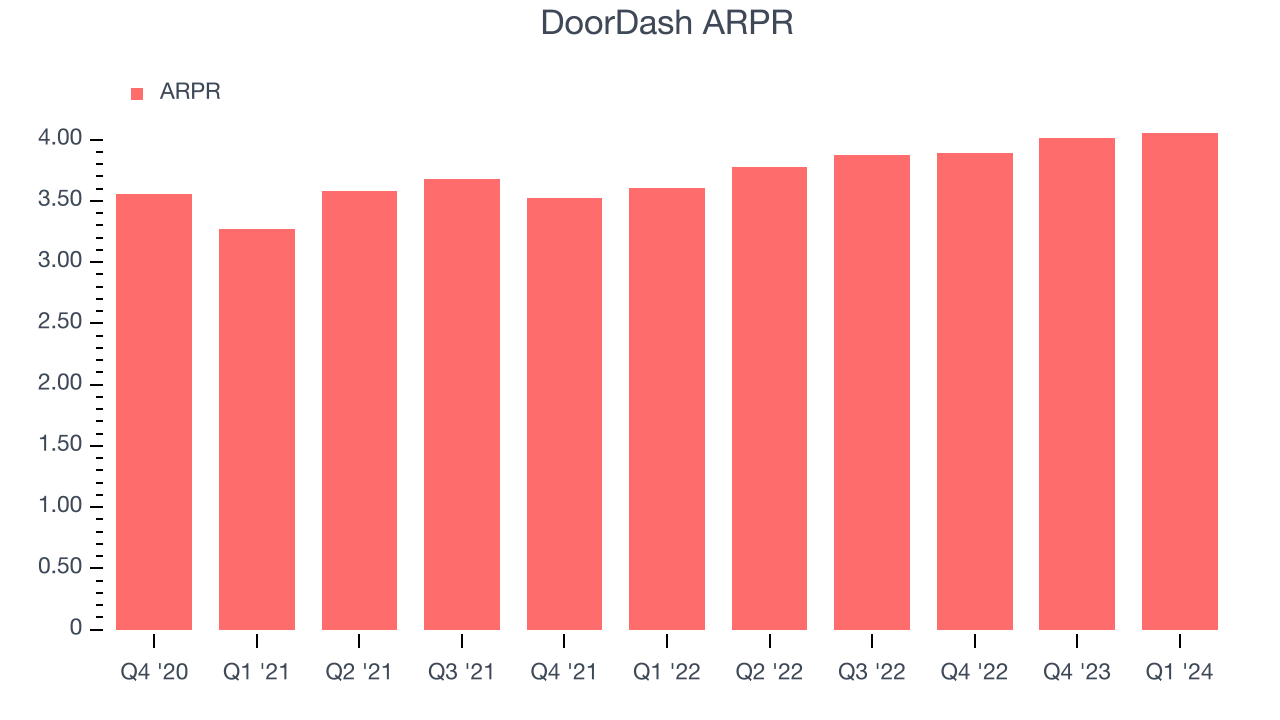

Revenue Per Request

Average revenue per request (ARPR) is a critical metric to track for consumer internet businesses like DoorDash because it measures how much the company earns in transaction fees from each request. This number also informs us about DoorDash's take rate, which represents its pricing leverage over the ecosystem, or "cut" from each transaction.

DoorDash's ARPR growth has been decent over the last two years, averaging 6.1%. The company's ability to increase prices while constantly growing its service requests demonstrates the value of its platform. This quarter, ARPR declined NaN% year on year to $4.05 per request.

Key Takeaways from DoorDash's Q1 Results

It was great to see DoorDash beat analysts' revenue and adjusted EBITDA expectations this quarter. We were also glad it produced solid revenue growth. On the other hand, next quarter's Maketplace GOV (gross order value) guidance was just in line and adjusted EBITDA guidance missed. Overall, this quarter's results seemed fairly positive but the outlook was less exciting, which for a growth stock at a premium valuation can spell trouble. The market was expecting more from the guide, and the stock is down 12.4% after reporting, trading at $111.53 per share.

So should you invest in DoorDash right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.