Department store chain Dillard’s (NYSE:DDS) reported Q1 CY2024 results exceeding Wall Street analysts' expectations, with revenue down 2.5% year on year to $1.57 billion. It made a non-GAAP profit of $11.11 per share, down from its profit of $11.85 per share in the same quarter last year.

Dillard's (DDS) Q1 CY2024 Highlights:

- Revenue: $1.57 billion vs analyst estimates of $1.55 billion (1.5% beat)

- EPS (non-GAAP): $11.11 vs analyst estimates of $9.18 (21% beat)

- Gross Margin (GAAP): 45.5%, up from 44.8% in the same quarter last year

- Free Cash Flow of $209.2 million, down 15.8% from the same quarter last year

- Same-Store Sales were down 2% year on year

- Market Capitalization: $7.05 billion

With stores located largely in the Southern and Western US, Dillard’s (NYSE:DDS) is a department store chain that sells clothing, cosmetics, accessories, and home goods.

As the name suggests, a department store offers a wide variety of merchandise organized into different departments or sections. Before the introduction of department stores in the 19th century, consumers would have to visit three different stores to buy an evening dress, a bottle of perfume, and a picture frame.

Today, the Dillard’s customer is a middle to upper-income woman over 35 years old who is looking for high-quality products in a variety of categories. While other department stores may offer products from affordable to luxury, Dillard’s products tend to be in the middle of the price spectrum, with a focus on quality over trendiness. Brands such as Ralph Lauren, Coach, and Lancome can be found in stores or on its e-commerce site.

Stores vary in size but are roughly 150,000 square feet. They are typically located in suburban malls and shopping centers. Common departments in a store include women’s/men’s/children’s apparel, beauty/cosmetics, and home goods. Additionally, Dillard's has an active e-commerce presence, which was launched in 1998 and made Dillard’s a fairly early adopter in the department store category at the time.

Department Store

Department stores emerged in the 19th century to provide customers with a wide variety of merchandise under one roof, offering a convenient and luxurious shopping experience. They played an important role in the history of American retail and urbanization, and prior to department stores, retailers tended to sell narrow specialty and niche items. But what was once new is now old, and department stores are somewhat considered a relic of the past. They are being attacked from multiple angles–stagnant foot traffic at malls where they’ve served as anchors; more nimble off-price and fast-fashion retailers; and e-commerce-first competitors not burdened by large physical footprints.

Department store competitors include Macy’s (NYSE:M), Kohl’s (NYSE:KSS), and Nordstrom (NYSE:JWN).Sales Growth

Dillard's is larger than most consumer retail companies and benefits from economies of scale, giving it an edge over its competitors.

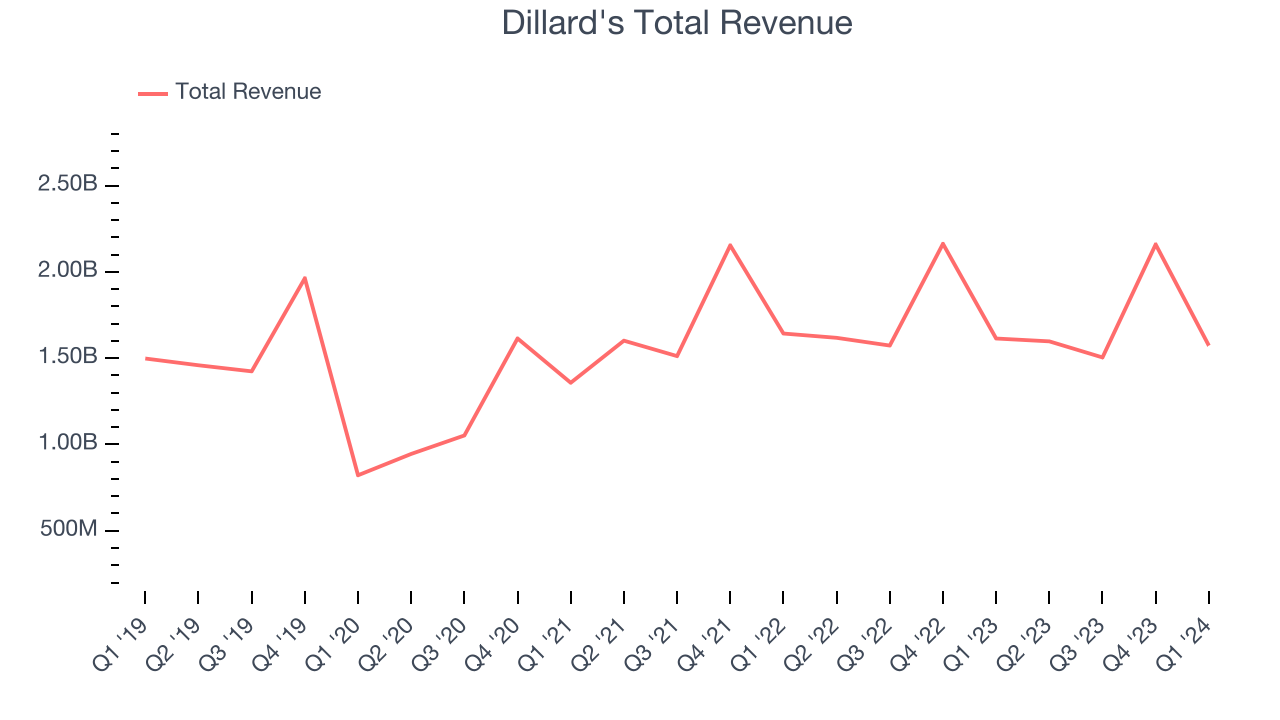

As you can see below, the company's revenue was flat over the last five years as its store count dropped.

This quarter, Dillard's revenue fell 2.5% year on year to $1.57 billion but beat Wall Street's estimates by 1.5%. Looking ahead, Wall Street expects revenue to decline 4.9% over the next 12 months, a deceleration from this quarter.

Same-Store Sales

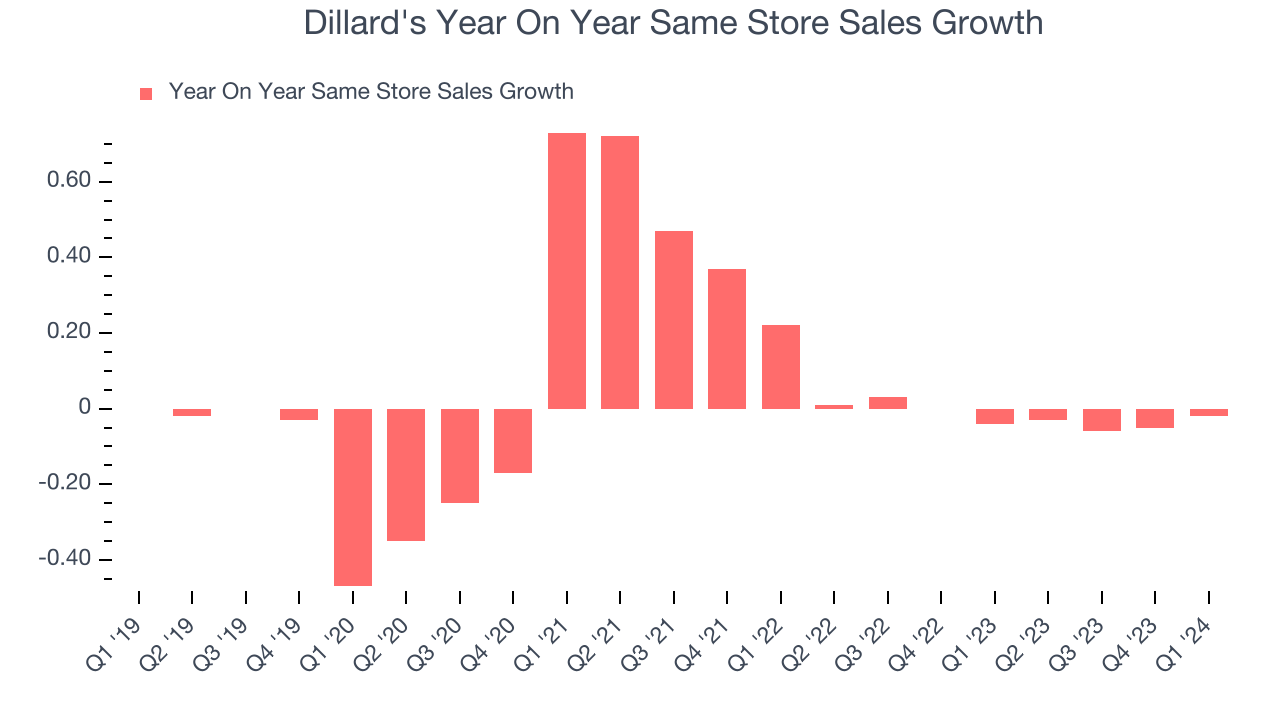

Same-store sales growth is an important metric that tracks demand for a retailer's established brick-and-mortar stores and e-commerce platform.

Dillard's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 2% year on year. The company has been reducing its store count as fewer locations sometimes lead to higher same-store sales, but that hasn't been the case here.

In the latest quarter, Dillard's same-store sales fell 2% year on year. This decrease was an improvement from the 4% year-on-year decline it posted 12 months ago. It's always great to see a business improve its prospects.

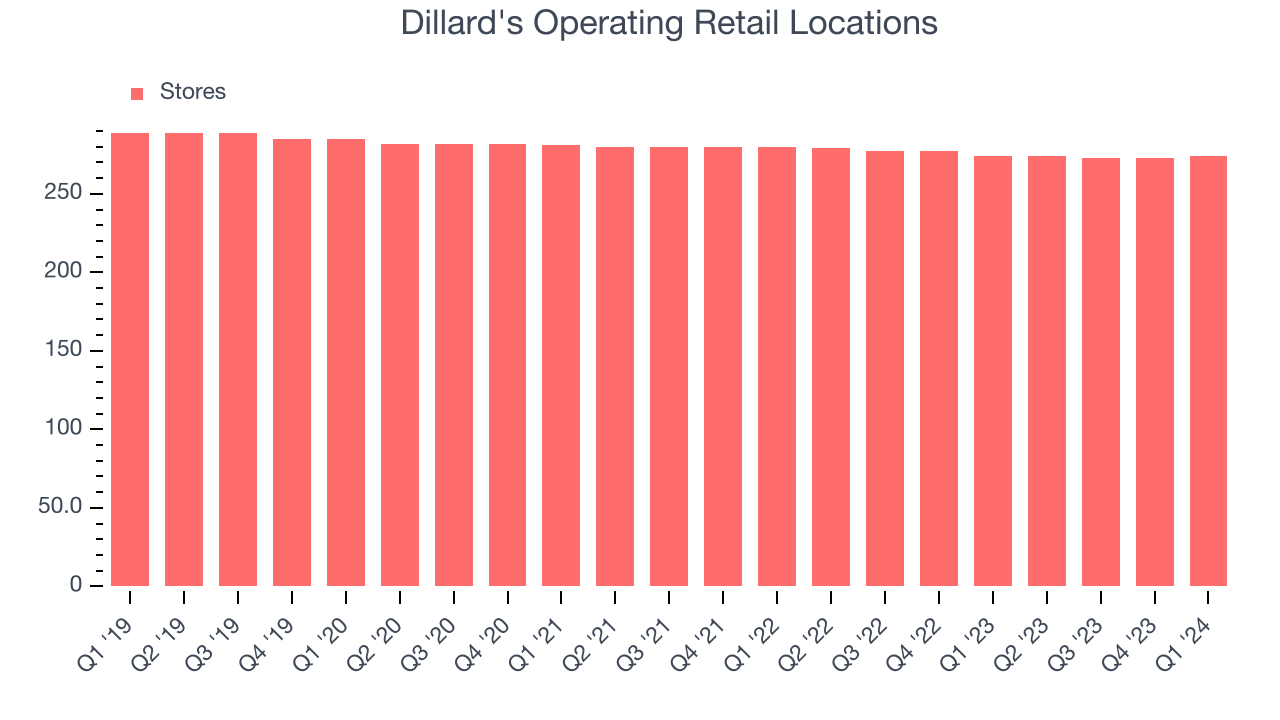

Number of Stores

When a retailer like Dillard's is shuttering stores, it usually means that brick-and-mortar demand is less than supply, and the company is responding by closing underperforming locations and possibly shifting sales online. As of the most recently reported quarter, Dillard's operated 274 total retail locations, in line with its store count a year ago.

Taking a step back, the company has generally closed its stores over the last two years, averaging a 1.2% annual decline in its physical footprint. A smaller store base means that the company must rely on higher foot traffic and sales per customer at its remaining stores as well as e-commerce sales to fuel revenue growth.

Gross Margin & Pricing Power

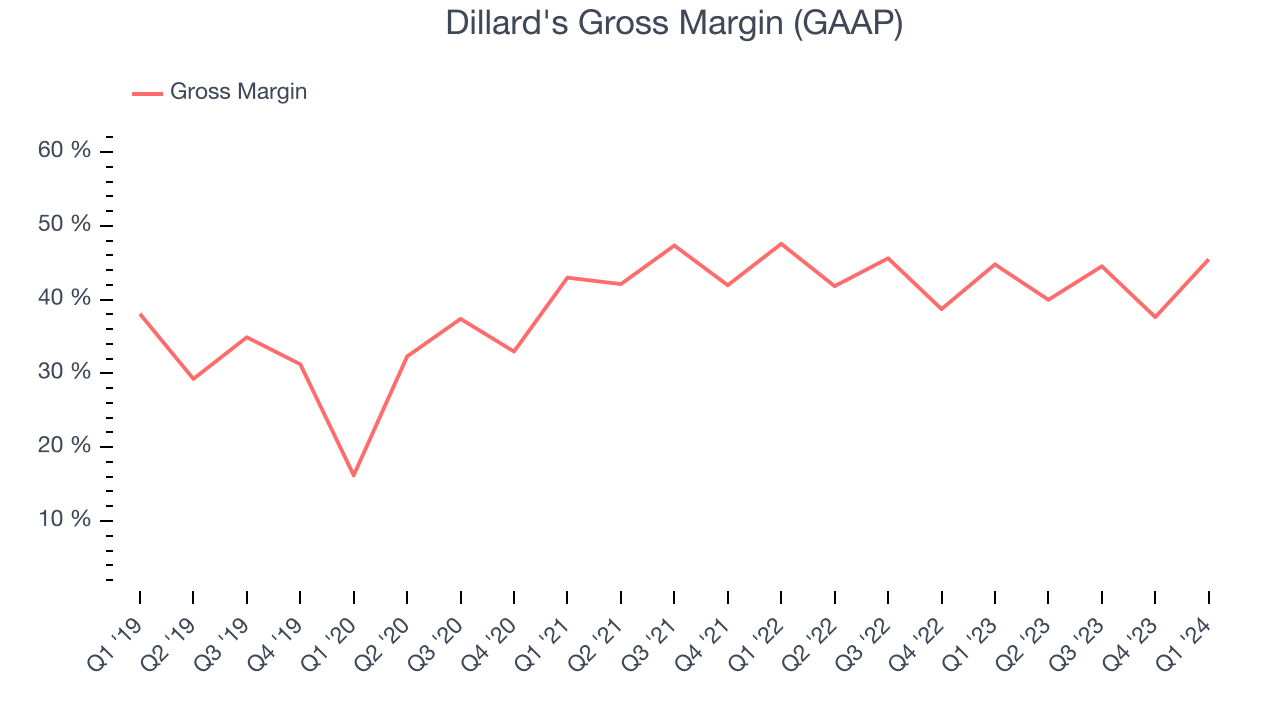

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate product differentiation, negotiating leverage, and pricing power.

Dillard's has good unit economics for a retailer, giving it the opportunity to invest in areas such as marketing and talent to stay competitive. As you can see below, it's averaged a healthy 42% gross margin over the last two years. This means the company makes $0.42 for every $1 in revenue before accounting for its operating expenses.

Dillard's gross profit margin came in at 45.5% this quarter, flat with the same quarter last year. This steady margin stems from its efforts to keep prices low for consumers and signals that it has stable input costs (such as freight expenses to transport goods).

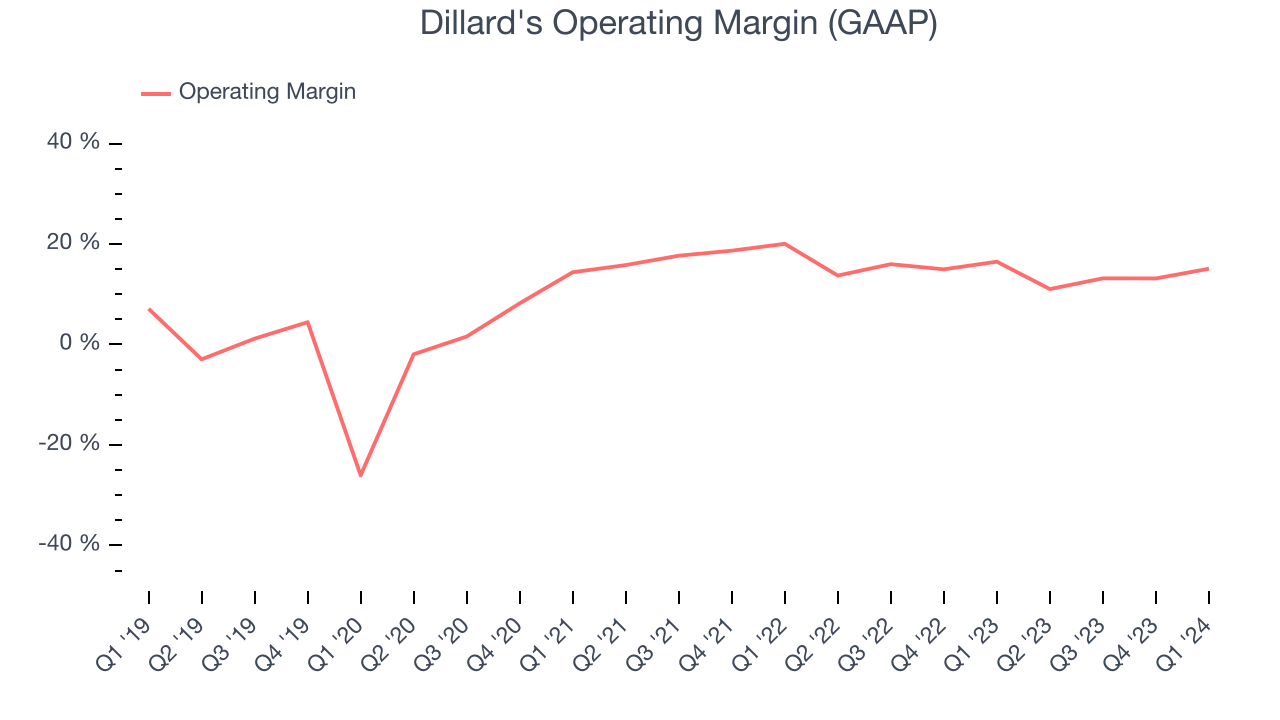

Operating Margin

Operating margin is an important measure of profitability for retailers as it accounts for all expenses keeping the lights on, including wages, rent, advertising, and other administrative costs.

In Q1, Dillard's generated an operating profit margin of 15.1%, down 1.4 percentage points year on year. Conversely, the company's gross margin actually increased, so we can assume the reduction was driven by inefficient cost controls or lower operating leverage on fixed costs.

Zooming out, Dillard's has exercised operational efficiency over the last eight quarters. The company has demonstrated it can be wildly profitable for a consumer retail business, boasting an average operating margin of 14.2%. However, Dillard's margin has slightly declined by 2.2 percentage points year on year (on average). This shows the company has faced some small speed bumps along the way.

Zooming out, Dillard's has exercised operational efficiency over the last eight quarters. The company has demonstrated it can be wildly profitable for a consumer retail business, boasting an average operating margin of 14.2%. However, Dillard's margin has slightly declined by 2.2 percentage points year on year (on average). This shows the company has faced some small speed bumps along the way. EPS

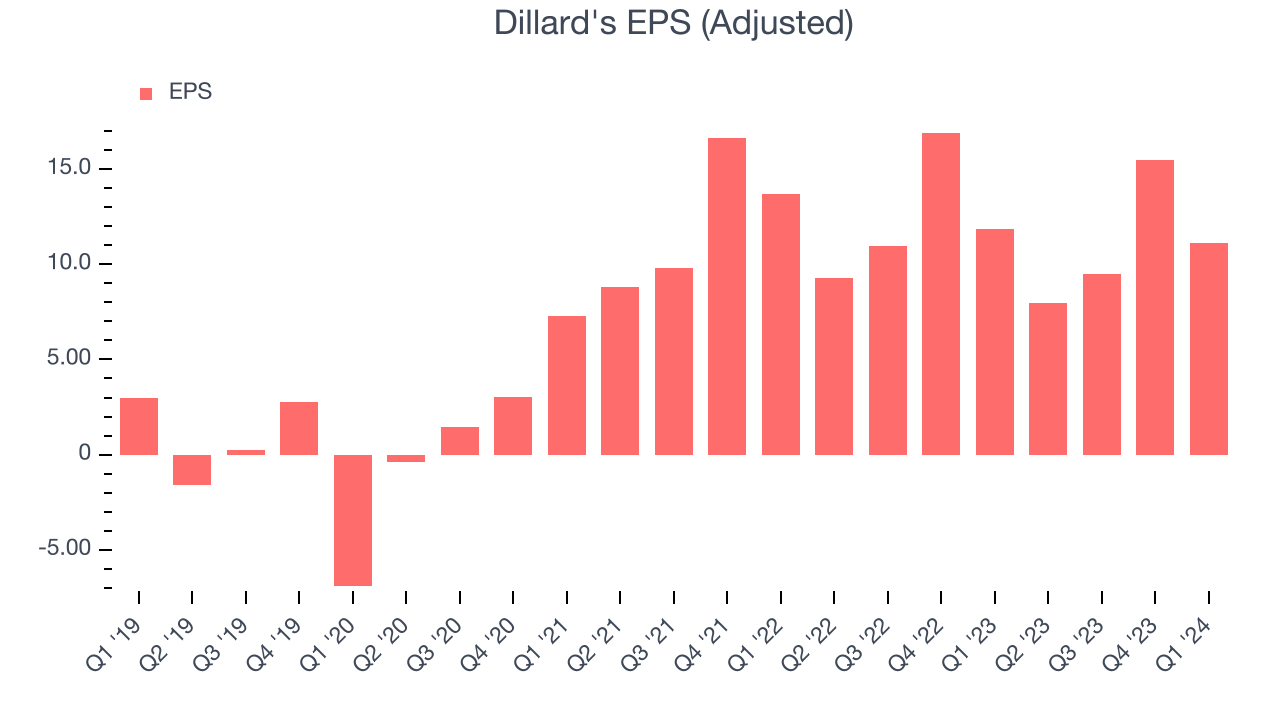

These days, some companies issue new shares like there's no tomorrow. That's why we like to track earnings per share (EPS) because it accounts for shareholder dilution and share buybacks.

In Q1, Dillard's reported EPS at $11.11, down from $11.85 in the same quarter a year ago. This print beat Wall Street's estimates by 21%.

Over the next 12 months, however, Wall Street is projecting an average 26.4% year-on-year decline in EPS.

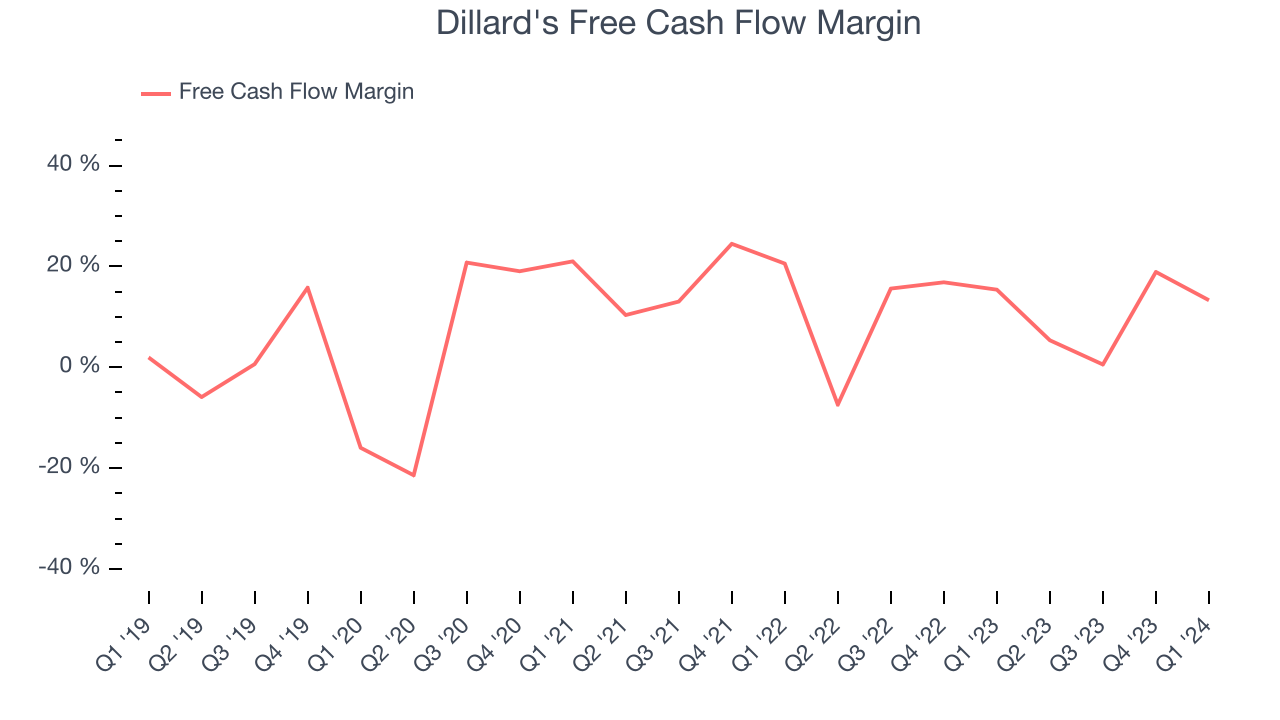

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Dillard's free cash flow came in at $209.2 million in Q1, down 15.8% year on year. This result represents a 13.3% margin.

Over the last eight quarters, Dillard's has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining a robust cash balance. The company's free cash flow margin has been among the best in consumer retail, averaging 10.5%. Furthermore, its margin has been flat, showing that the company's cash flows are relatively stable.

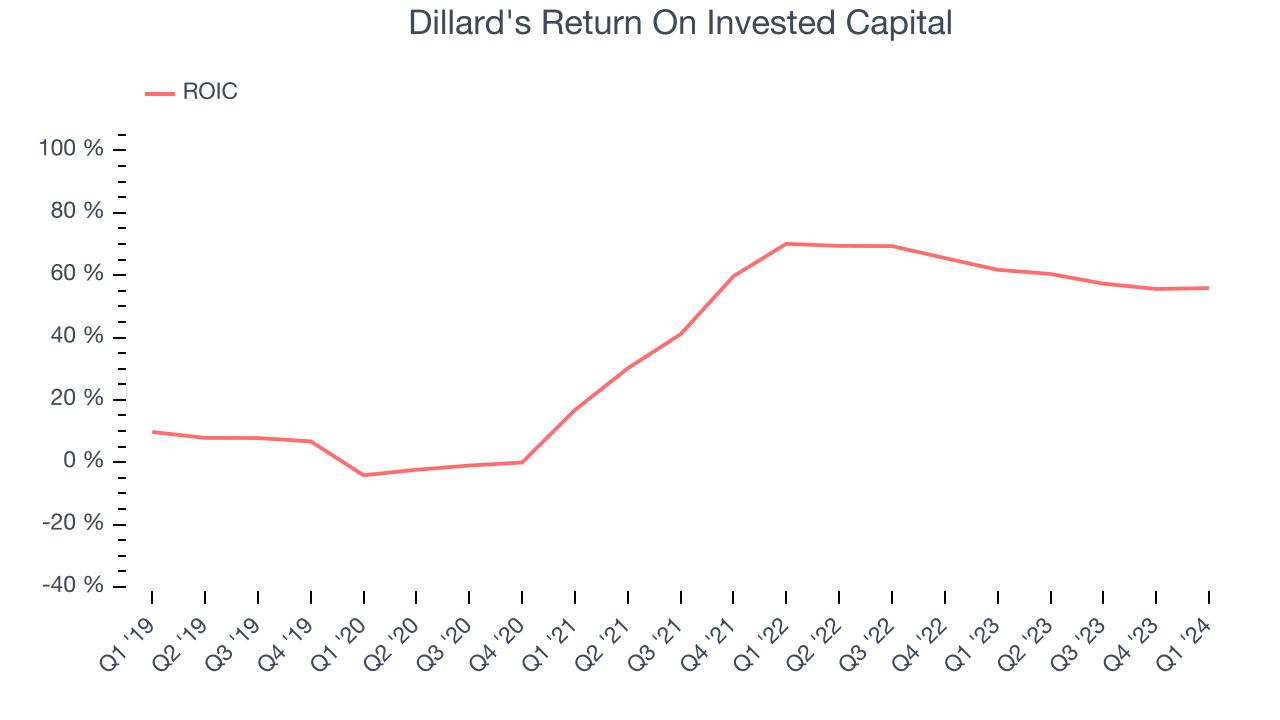

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to how much money the business raised (debt and equity).

Although Dillard's hasn't been the highest-quality company lately because of its poor top-line performance, it historically did a wonderful job investing in profitable business initiatives. Its five-year average ROIC was 40%, splendid for a retail business.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last few years, Dillard's ROIC has significantly increased. This is a good sign, and we hope the company can continue improving.

Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly.

Dillard's is a profitable, well-capitalized company with $1.17 billion of cash and $563.4 million of debt, meaning it could pay back all its debt tomorrow and still have $601.6 million of cash on its balance sheet. This net cash position gives Dillard's the freedom to raise more debt, return capital to shareholders, or invest in growth initiatives.

Key Takeaways from Dillard's Q1 Results

We were impressed by how significantly Dillard's blew past analysts' gross margin expectations this quarter. We were also excited its EPS outperformed Wall Street's estimates. Zooming out, we think this was a fantastic quarter that should have shareholders cheering. The stock is flat after reporting and currently trades at $434.45 per share.

Is Now The Time?

Dillard's may have had a good quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Dillard's, we'll be cheering from the sidelines. Its revenue growth has been uninspiring over the last five years, and analysts expect growth to deteriorate from here. And while its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits, the downside is its shrinking same-store sales suggests it'll need to change its strategy to succeed. On top of that, its declining physical locations suggests its demand is falling.

While we've no doubt one can find things to like about Dillard's, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $312 per share right before these results (compared to the current share price of $434.45), implying they didn't see much short-term potential in Dillard's.

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.