Cloud computing provider DigitalOcean (NYSE: DOCN) reported results ahead of analysts' expectations in Q1 CY2024, with revenue up 11.9% year on year to $184.7 million. The company expects next quarter's revenue to be around $188.5 million, in line with analysts' estimates. It made a non-GAAP profit of $0.43 per share, improving from its profit of $0.26 per share in the same quarter last year.

DigitalOcean (DOCN) Q1 CY2024 Highlights:

- Revenue: $184.7 million vs analyst estimates of $182.6 million (1.2% beat)

- EPS (non-GAAP): $0.43 vs analyst estimates of $0.38 (12.9% beat)

- Revenue Guidance for Q2 CY2024 is $188.5 million at the midpoint, roughly in line with what analysts were expecting

- The company reconfirmed its revenue guidance for the full year of $767.5 million at the midpoint

- Gross Margin (GAAP): 60.7%, up from 56.5% in the same quarter last year

- Free Cash Flow of $21.47 million, down 25.5% from the previous quarter

- Annual Recurring Revenue: $749 million at quarter end, up 11.9% year on year

- Net Revenue Retention Rate: 97%, in line with the previous quarter

- Market Capitalization: $2.97 billion

Started by brothers Ben and Moisey Uretsky, DigitalOcean (NYSE: DOCN) provides a simple, low-cost platform that allows developers and small and medium-sized businesses to host applications and data in the cloud.

DigitalOcean offers a range of cloud computing options for developers and small businesses. Hyperscalers Amazon Web Services, Microsoft Azure, and Google Cloud Platform are the dominant providers of the cloud infrastructure that has become the standard for companies today.

For individual developers and small and medium businesses, the large cloud platforms present some hurdles to adoption: the actual onboarding and implementation processes can be difficult, pricing models can be complex and at times unpredictable, and there is a relatively low level of support for SMBs, as the cloud giants are focused on serving enterprise customers.

DigitalOcean focuses mainly on less application and website hosting use cases and differentiates itself from the hyperscale platforms through the intuitive simplicity of its user interface, which allows customers to spin up “Droplets” (their term for a virtual machine) in under a minute. The company offers a high level of live-person customer support regardless of spend levels, and utilizes open source software to keep costs low. For context, DigitalOcean’s bandwidth prices are a fraction of its hyperscale rivals.

Data Storage

Data is the lifeblood of the internet and software in general, and the amount of data created is accelerating. As a result, the importance of storing the data in scalable and efficient formats continues to rise, especially as its diversity and associated use cases expand from analyzing simple, structured datasets to high-scale processing of unstructured data such as images, audio, and video.

Digital Ocean’s main competitors are the hyperscale cloud providers: Amazon (NASDAQ:AMZN), Microsoft (NASDAQ: MSFT), and Alphabet’s Google Cloud Platform (NASDAQ: GOOGL). IBM (NYSE:IBM) and Oracle (NYSE:ORCL) round out the larger players. A second set of rivals are niche cloud providers that target certain verticals or geographies such as OVH, Vultr, Linode, and Heroku, which is owned by Salesforce.com (NYSE:CRM).

Sales Growth

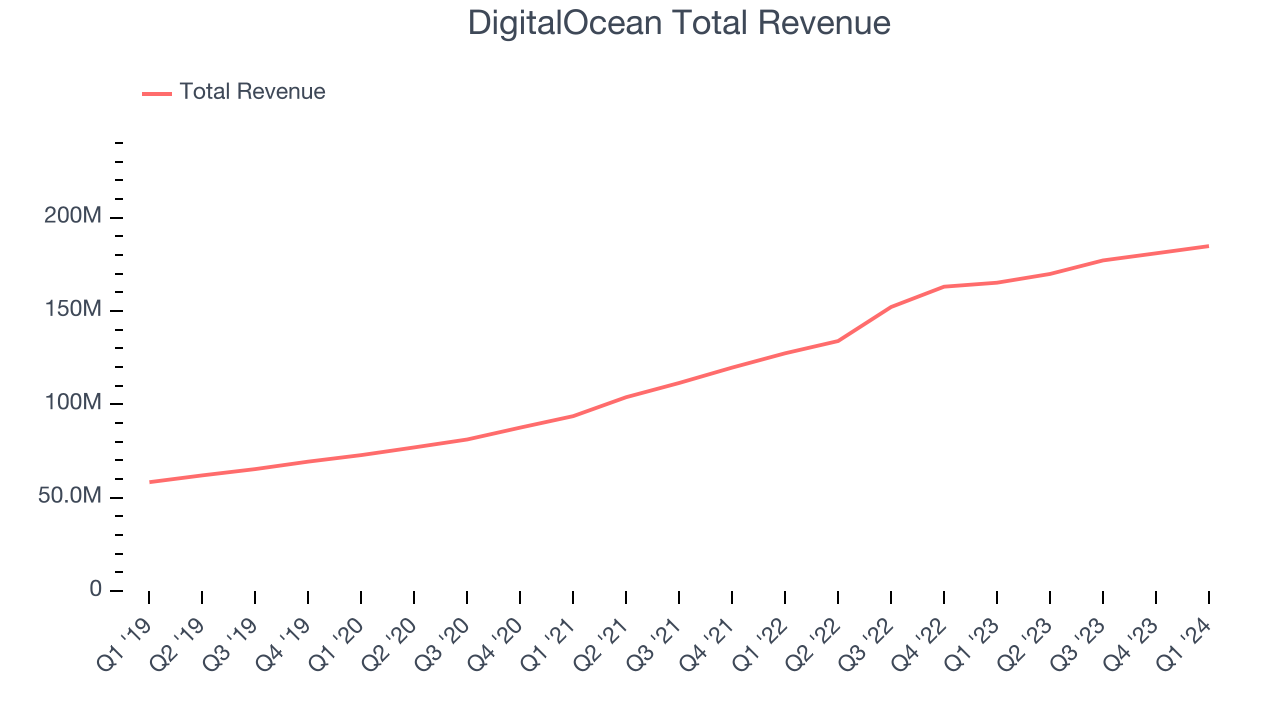

As you can see below, DigitalOcean's revenue growth has been strong over the last three years, growing from $93.66 million in Q1 2021 to $184.7 million this quarter.

This quarter, DigitalOcean's quarterly revenue was once again up 11.9% year on year. We can see that DigitalOcean's revenue increased by $3.86 million in Q1, which was roughly the same growth rate observed in Q4 CY2023. This steady quarter-on-quarter growth shows that the company can maintain its paced growth trajectory.

Next quarter's guidance suggests that DigitalOcean is expecting revenue to grow 11% year on year to $188.5 million, slowing down from the 26.8% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 10.6% over the next 12 months before the earnings results announcement.

Product Success

One of the best parts about the software-as-a-service business model (and a reason why SaaS companies trade at such high valuation multiples) is that customers typically spend more on a company's products and services over time.

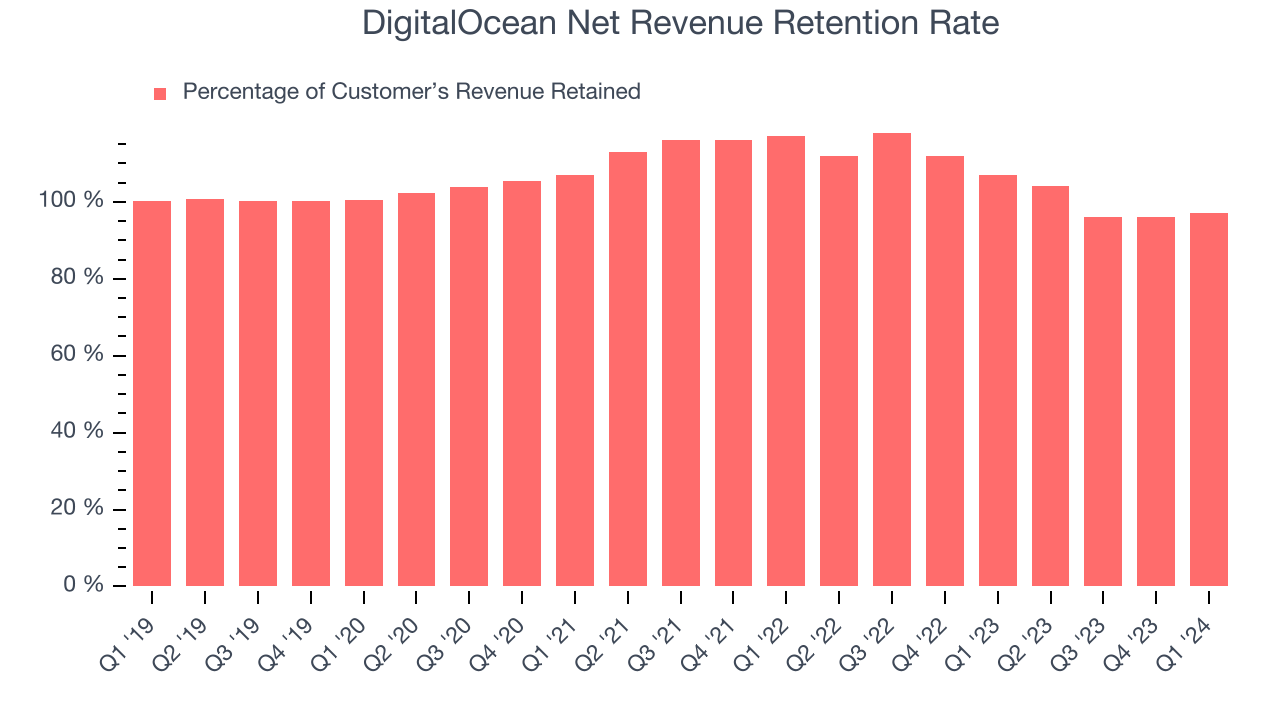

DigitalOcean's net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 97% in Q1. This means DigitalOcean's revenue would've decreased by 3% over the last 12 months if it didn't win any new customers.

Despite significantly increasing since the previous quarter, DigitalOcean still has a weak net retention rate, signaling that some customers aren't satisfied with its products, leading to lost contracts and revenue streams.

Profitability

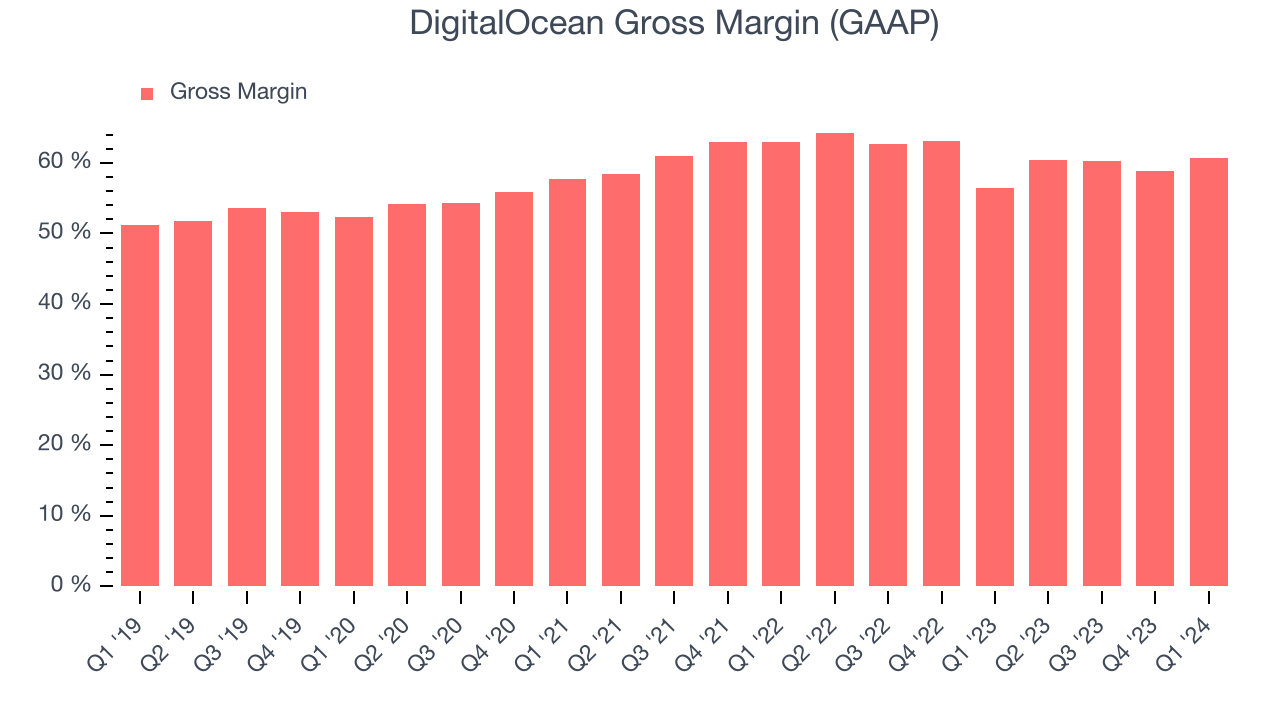

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. DigitalOcean's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 60.7% in Q1.

That means that for every $1 in revenue the company had $0.61 left to spend on developing new products, sales and marketing, and general administrative overhead. While its gross margin has improved significantly since the previous quarter, DigitalOcean's gross margin is still poor for a SaaS business. It's vital that the company continues to improve this key metric.

Cash Is King

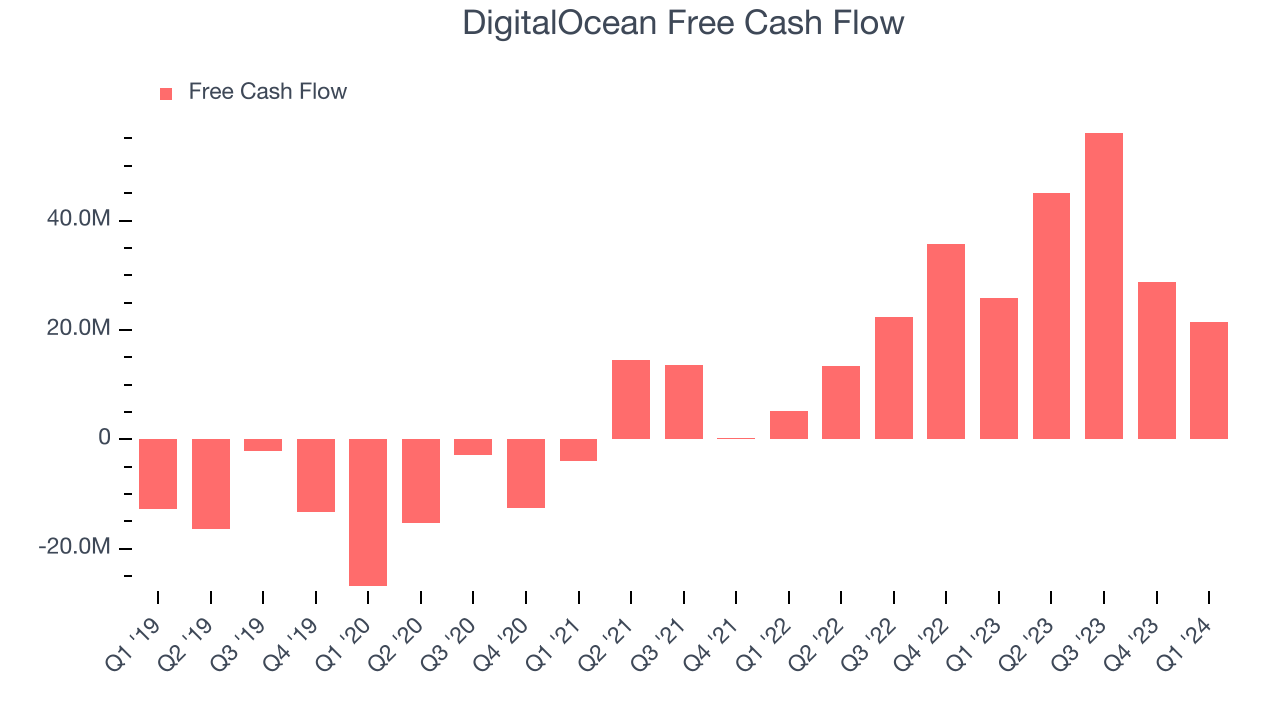

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. DigitalOcean's free cash flow came in at $21.47 million in Q1, down 16.6% year on year.

DigitalOcean has generated $151.5 million in free cash flow over the last 12 months, an impressive 21.3% of revenue. This high FCF margin stems from its asset-lite business model and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a cash cushion.

Key Takeaways from DigitalOcean's Q1 Results

We enjoyed seeing DigitalOcean materially improve its gross margin this quarter. We were also glad its ARR (annual recurring revenue) outperformed Wall Street's estimates. Guidance produced no surprises, with revenue for next quarter and the full year in line, showing that the company is on track. Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is up 2.9% after reporting and currently trades at $33.5 per share.

Is Now The Time?

When considering an investment in DigitalOcean, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

Although we have other favorites, we understand the arguments that DigitalOcean isn't a bad business. We'd expect growth rates to moderate from here, but its revenue growth has been strong over the last three years. And while its existing customers have been reducing their spending, which is a bit concerning, the good news is its efficient customer acquisition hints at the potential for strong profitability.

DigitalOcean's price-to-sales ratio based on the next 12 months is 3.9x, suggesting the market is expecting more moderate growth relative to the hottest software stocks. In the end, beauty is in the eye of the beholder. While DigitalOcean wouldn't be our first pick, if you like the business, it seems to be trading at a pretty compelling price right now.

Wall Street analysts covering the company had a one-year price target of $38.80 right before these results (compared to the current share price of $33.50).

To get the best start with StockStory, check out our most recent Stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released. Especially for companies reporting pre-market, this often gives investors the chance to react to the results before everyone else has fully absorbed the information.