Fresh produce company Dole (NYSE:DOLE) reported results in line with analysts' expectations in Q1 CY2024, with revenue up 6.6% year on year to $2.12 billion. It made a non-GAAP profit of $0.43 per share, improving from its profit of $0.34 per share in the same quarter last year.

Dole (DOLE) Q1 CY2024 Highlights:

- Revenue: $2.12 billion vs analyst estimates of $2.12 billion (small beat)

- Adjusted EBITDA: $110.1 million vs analyst estimates of $99.4 million (10.8% beat)

- EPS (non-GAAP): $0.43 vs analyst estimates of $0.31 (38.3% beat)

- Full year guidance: adjusted EBITDA to be similar to full year 2023 (in line)

- Gross Margin (GAAP): 9.2%, up from 9% in the same quarter last year

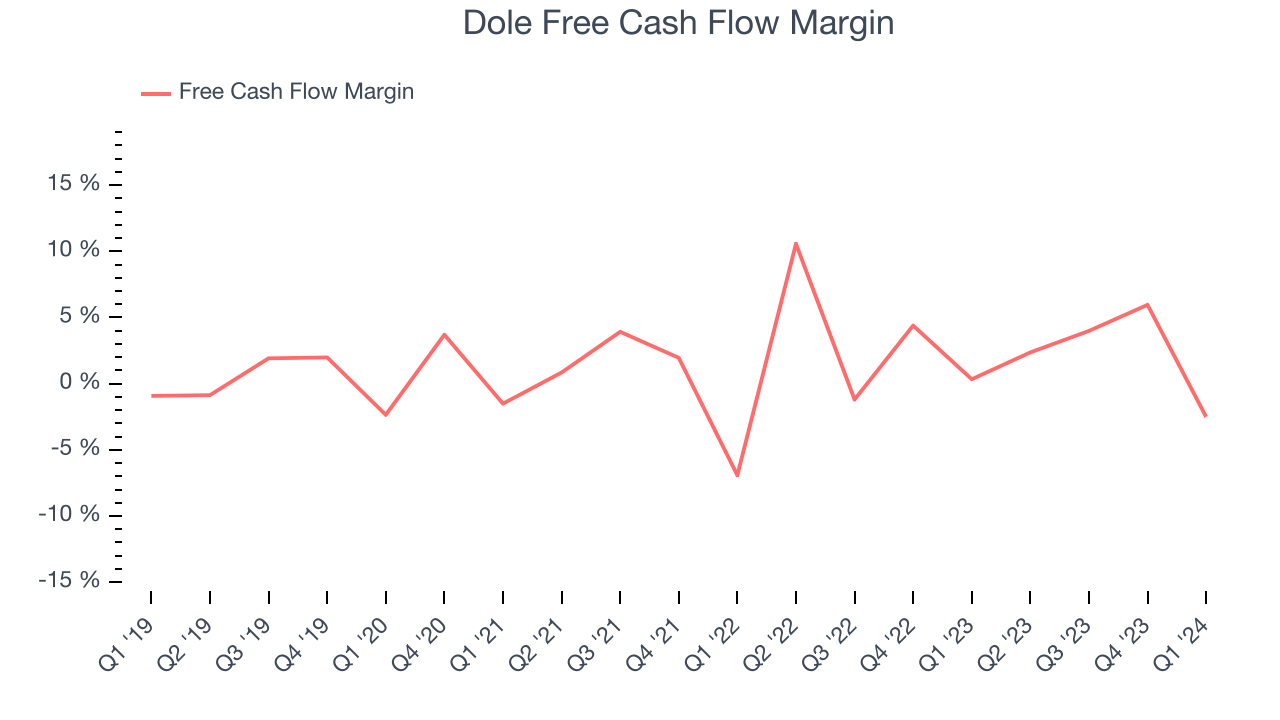

- Free Cash Flow was -$53.19 million, down from $123.4 million in the previous quarter

- Market Capitalization: $1.16 billion

Cherished for its delicious, world-famous pineapples and Hawaiian roots, Dole (NYSE:DOLE) is a global agricultural company specializing in fresh fruits and vegetables.

The company was founded in 1901 as the Hawaiian Pineapple Company by James Dole, the “Pineapple King”. Dole’s enterprise was acquired by Castle & Cooke in 1961, who diversified it into other areas of the food industry, and it was once again bought in 1985 by entrepreneur and businessman David Murdock, whose involvement marked a turning point in the company's history.

Murdock recognized Dole’s potential for global growth and aggressively expanded its operations, transforming it into a multi-national corporation. Today, Dole is one of the world's largest producers and distributors of fresh fruits and vegetables, and its portfolio includes not only pineapples but also bananas, strawberries, salads, and more.

To maintain its complex operations, Dole leverages its well-established network of farms, packing facilities, and distribution centers spanning multiple continents, including North America, Latin America, Europe, Asia, and Africa. This extensive supply chain allows Dole to source fresh produce from different regions, ensuring a year-round supply of fruits and vegetables. Few competitors can match Dole's global presence and logistical capabilities.

The company partners with grocery stores, supermarkets, and convenience stores to sell its products. It also supplies restaurants, hotels, and catering companies with fresh produce.

Perishable Food

The perishable food industry is diverse, encompassing large-scale producers and distributors to specialty and artisanal brands. These companies sell produce, dairy products, meats, and baked goods and have become integral to serving modern American consumers who prioritize freshness, quality, and nutritional value. Investing in perishable food stocks presents both opportunities and challenges. While the perishable nature of products can introduce risks related to supply chain management and shelf life, it also creates a constant demand driven by the necessity for fresh food. Companies that can efficiently manage inventory, distribution, and quality control are well-positioned to thrive in this competitive market. Navigating the perishable food industry requires adherence to strict food safety standards, regulations, and labeling requirements.

Competitors in the fresh produce category include Calavo Growers (NASDAQGS:CVGW), Fresh Del Monte (NYSE:FDP), and Mission Produce (NASDAQGS:AVO) along with private companies Chiquita Brands International and Sunkist Growers.Sales Growth

Dole is one of the larger consumer staples companies and benefits from a well-known brand, giving it customer mindshare and influence over purchasing decisions.

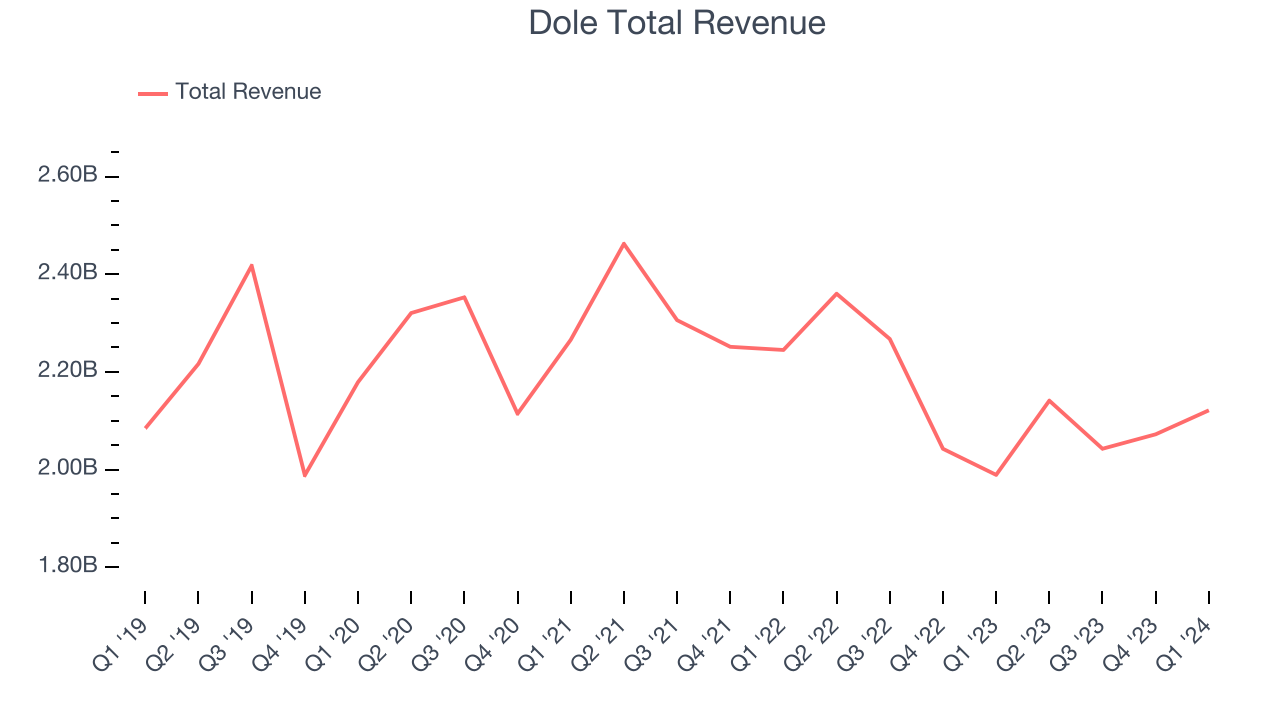

As you can see below, the company's revenue has declined over the last three years, dropping 2.6% annually. This is among the worst in the consumer staples industry, where demand is typically stable.

This quarter, Dole grew its revenue by 6.6% year on year, and its $2.12 billion in revenue was in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 2.7% over the next 12 months, a deceleration from this quarter.

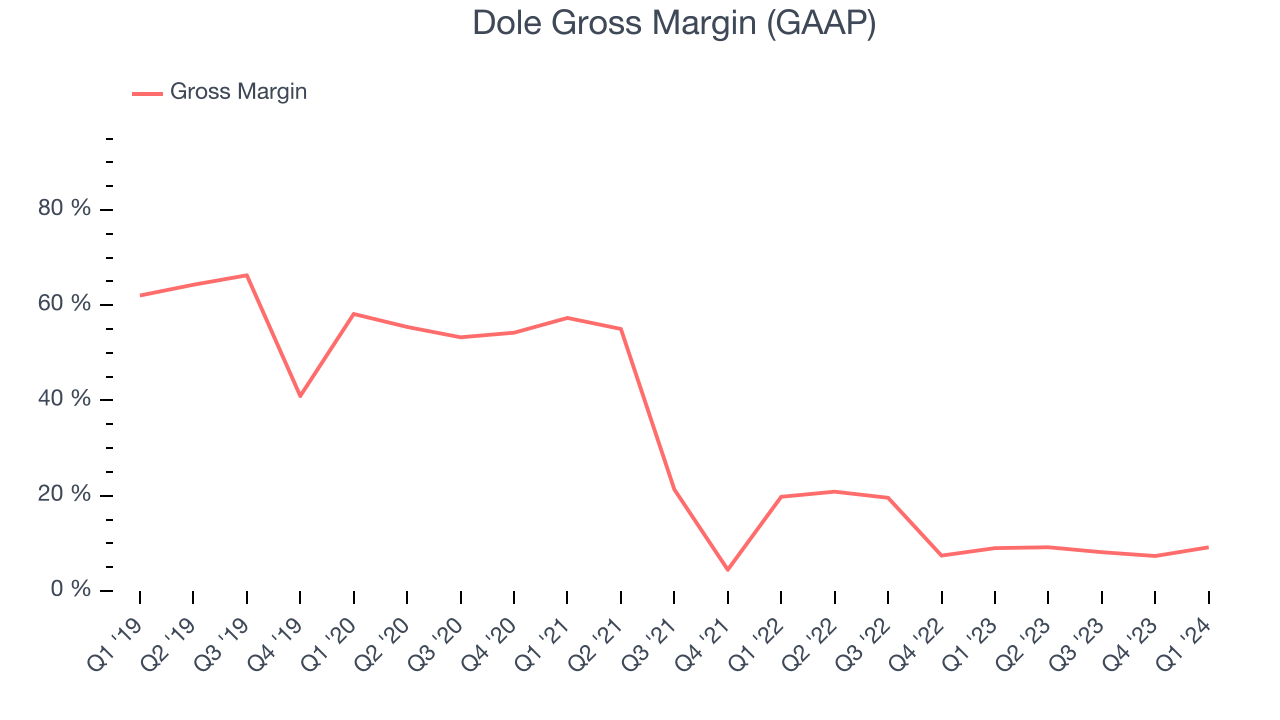

Gross Margin & Pricing Power

Gross profit margins tell us how much money a company gets to keep after paying for the direct costs of the goods it sells.

This quarter, Dole's gross profit margin was 9.2%, in line with the same quarter last year. That means for every $1 in revenue, a chunky $0.91 went towards paying for raw materials, production of goods, and distribution expenses.

Dole has poor unit economics for a consumer staples company, leaving it with little room for error if things go awry. As you can see above, it's averaged a paltry 11.6% gross margin over the last two years. Its margin has also been trending down over the last year, averaging 28.4% year-on-year decreases each quarter. If this trend continues, it could suggest a more competitive environment where Dole has diminishing pricing power and less favorable input costs (such as raw materials).

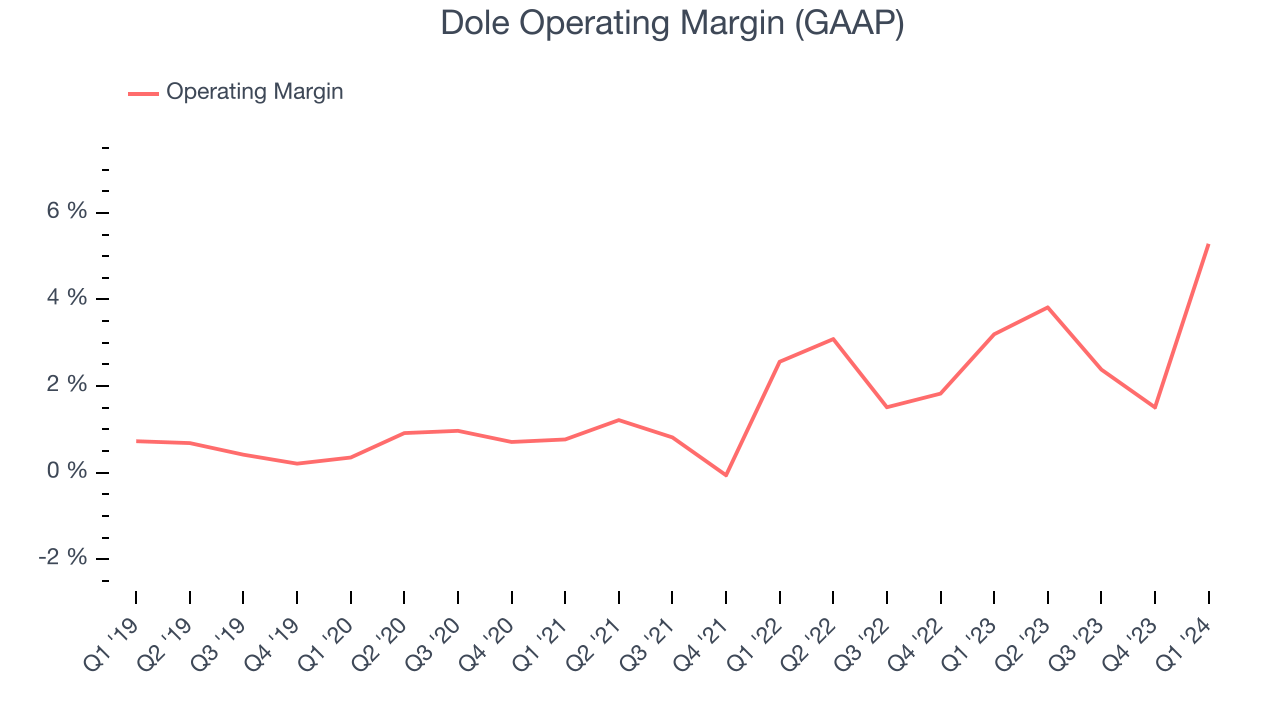

Operating Margin

Operating margin is a key profitability metric for companies because it accounts for all expenses enabling a business to operate smoothly, including marketing and advertising, IT systems, wages, and other administrative costs.

This quarter, Dole generated an operating profit margin of 5.3%, up 2.1 percentage points year on year. This increase was encouraging, and we can infer Dole was more efficient with its expenses because its operating margin expanded more than its gross margin.

Zooming out, Dole was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer staples business, producing an average operating margin of 2.8%. Its margin has also seen few fluctuations, meaning it will likely take a big change to improve profitability.

Zooming out, Dole was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer staples business, producing an average operating margin of 2.8%. Its margin has also seen few fluctuations, meaning it will likely take a big change to improve profitability.EPS

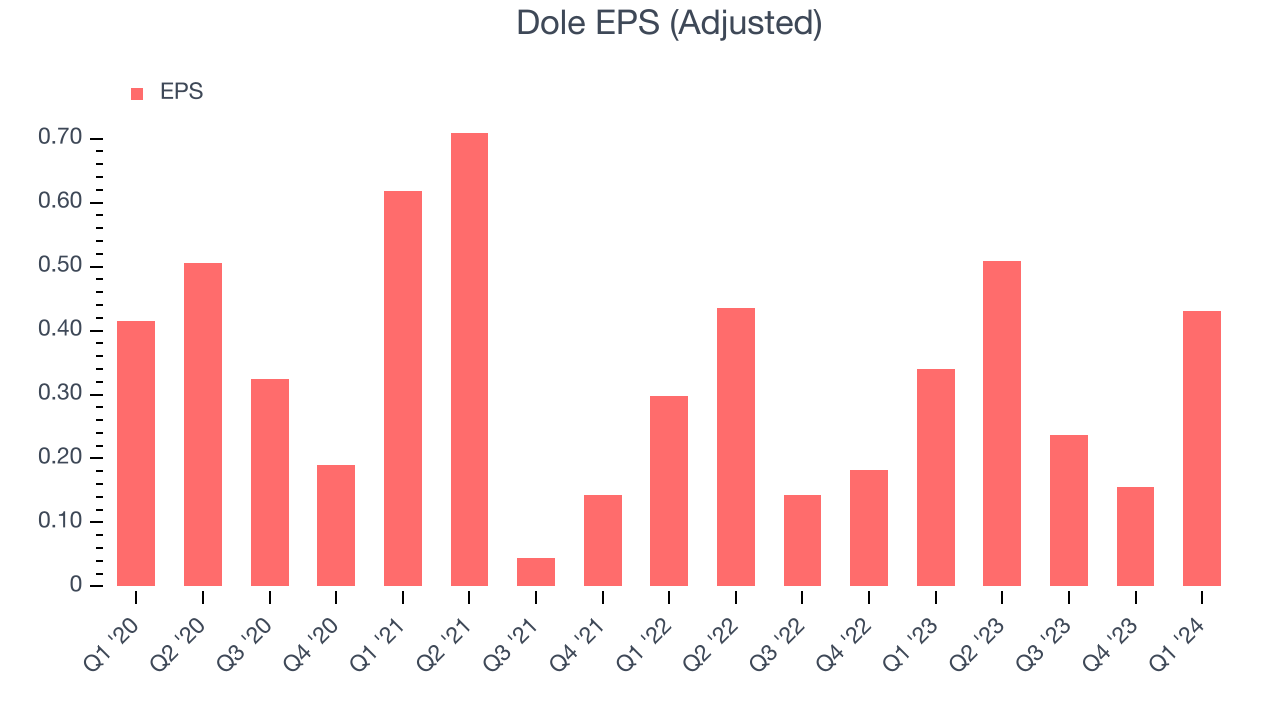

Earnings growth is a critical metric to track, but for long-term shareholders, earnings per share (EPS) is more telling because it accounts for dilution and share repurchases.

In Q1, Dole reported EPS at $0.43, up from $0.34 in the same quarter a year ago. This print beat Wall Street's estimates by 38.3%.

Between FY2021 and FY2024, Dole's EPS dropped 18.7%, translating into 6.7% annualized declines. We tend to steer our readers away from companies with falling EPS, especially in the consumer staples sector, where shrinking earnings could imply changing secular trends or consumer preferences. If there's no earnings growth, it's difficult to build confidence in a business's underlying fundamentals, leaving a low margin of safety around the company's valuation (making the stock susceptible to large downward swings).

Wall Street expects Dole to continue performing poorly over the next 12 months, with analysts projecting an average 11.1% year-on-year decline in EPS.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Dole burned through $53.19 million of cash in Q1, representing a negative 2.5% free cash flow margin. The company shifted to cash flow negative from cash flow positive in the same quarter last year, which caught our eye as we'd like consumer staples companies to have more consistent performance.

Over the last eight quarters, Dole has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 3.1%, subpar for a consumer staples business. Furthermore, its margin has averaged year-on-year declines of 1.3 percentage points over the last 12 months.

Return on Invested Capital (ROIC)

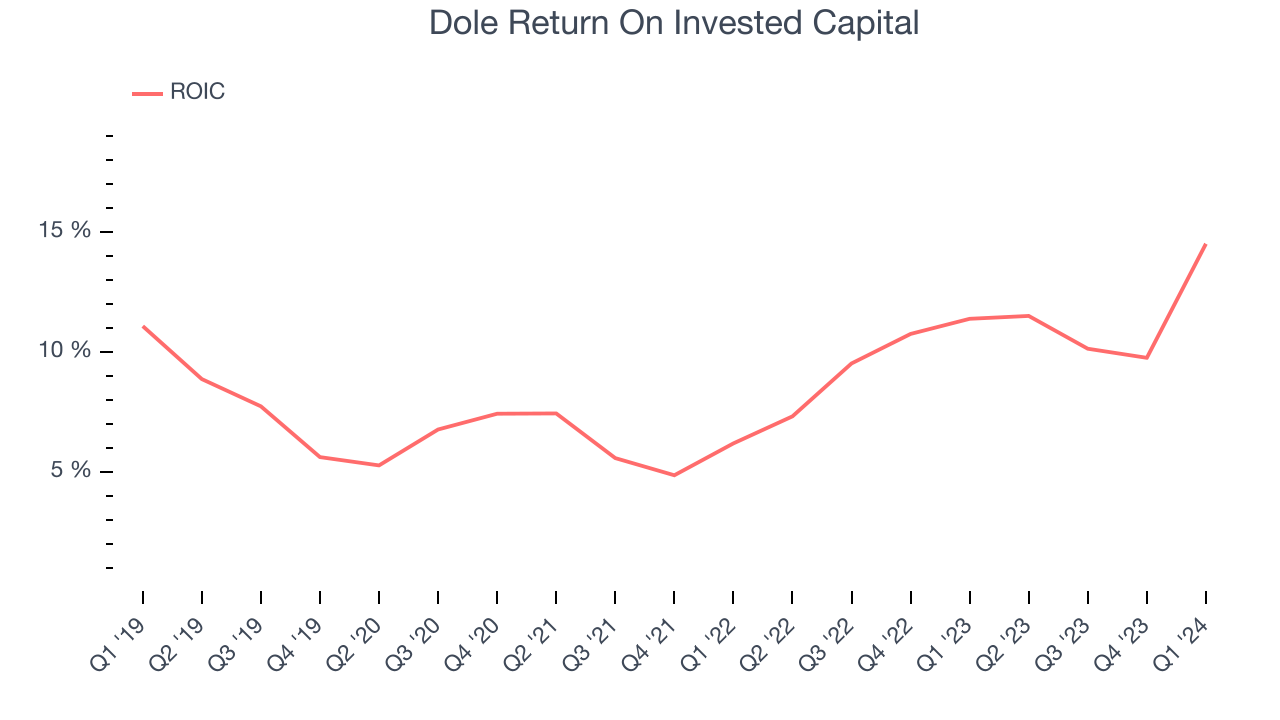

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Dole's five-year average ROIC was 10.7%, slightly better than the broader sector. Just as you’d like your investment dollars to generate returns, Dole's invested capital has produced decent profits.

Balance Sheet Risk

As long-term investors, the risk we care most about is the permanent loss of capital. This can happen when a company goes bankrupt or raises money from a disadvantaged position and is separate from short-term stock price volatility, which we are much less bothered by.

Dole reported $245.5 million of cash and $989.6 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $353.1 million of EBITDA over the last 12 months, we view Dole's 2.1x net-debt-to-EBITDA ratio as safe. We also see its $51.63 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from Dole's Q1 Results

We were impressed by how significantly Dole blew past analysts' operating margin and adjusted EBITDA expectations this quarter. Full year adjusted EBITDA was in line with expectations, showing that the company is on track. On the other hand, its gross margin missed analysts' expectations. Overall, we think this was a fine quarter. The stock is flat after reporting and currently trades at $12.3 per share.

Is Now The Time?

Dole may have had a good quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Dole, we'll be cheering from the sidelines. Its revenue has declined over the last three years, but at least growth is expected to increase in the short term. And while its well-known brand makes it a household name consumers consistently turn to, the downside is its projected EPS for the next year is lacking. On top of that, its gross margins make it more challenging to reach positive operating profits compared to other consumer staples businesses.

Dole's price-to-earnings ratio based on the next 12 months is 10.4x. While there are some things to like about Dole and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $15.57 per share right before these results (compared to the current share price of $12.30).

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.