Global talent agency and entertainment company Endeavor (NYSE:EDR) fell short of analysts' expectations in Q1 CY2024, with revenue up 15.9% year on year to $1.85 billion. It made a GAAP loss of $0.46 per share, down from its profit of $0.03 per share in the same quarter last year.

Endeavor (EDR) Q1 CY2024 Highlights:

- Revenue: $1.85 billion vs analyst estimates of $1.87 billion (small miss)

- EPS: -$0.46 vs analyst estimates of $0.23 (-$0.69 miss)

- Gross Margin (GAAP): 54.4%, in line with the same quarter last year

- Market Capitalization: $7.99 billion

Owner of the UFC, WWE, and a client roster including Christian Bale, Endeavor (NYSE:EDR) is a diversified global entertainment, sports, and content company known for its talent representation and involvement in the entertainment industry.

The company was founded in 1995 by prominent Hollywood agent Ari Emanuel and former Disney executive Michael Ovitz. It was initially established as Endeavor Talent Agency and merged with William Morris Agency in 2009, enabling it to represent many famous athletes and celebrities.

Leveraging its success in the talent agency industry, Endeavor has expanded its services to include event management, content production, and media distribution. It is also the majority owner of World Wrestling Entertainment (WWE) and the Ultimate Fighting Championship (UFC) through its creation of TKO Group.

Endeavor generates revenue from various sources, including commissions from talent representation, event ticket sales, content production, and media rights distribution. The company's business model revolves around creating synergies among its different divisions to become a one-stop shop for talent and content. Endeavor appeals to artists, athletes, and content creators looking for a partner who can help them navigate the complexities of the entertainment and sports industries while maximizing their potential and reach.

Media

The advent of the internet changed how shows, films, music, and overall information flow. As a result, many media companies now face secular headwinds as attention shifts online. Some have made concerted efforts to adapt by introducing digital subscriptions, podcasts, and streaming platforms. Time will tell if their strategies succeed and which companies will emerge as the long-term winners.

Competitors in the media and entertainment industry include Live Nation (NYSE:LYV), Disney (NYSE:DIS), and Warner Bros. Discovery (NASDAQ:WBX).Sales Growth

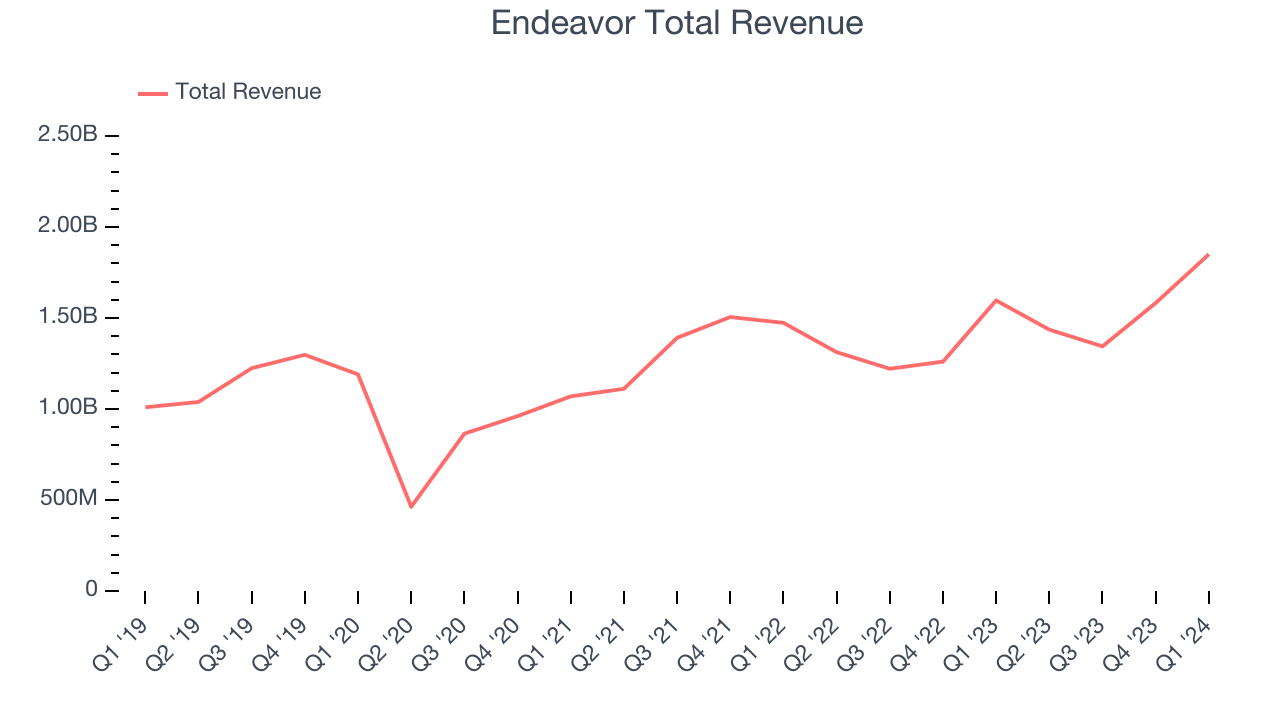

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Endeavor's annualized revenue growth rate of 6.9% over the last four years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Endeavor's annualized revenue growth of 6.5% over the last two years aligns with its four-year revenue growth, suggesting the company's demand has been stable.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Endeavor's annualized revenue growth of 6.5% over the last two years aligns with its four-year revenue growth, suggesting the company's demand has been stable.

We can dig even further into the company's revenue dynamics by analyzing its three most important segments: Events, Sports, and Representation, which are 40.3%, 37%, and 18.7% of revenue. Over the last two years, Endeavor's Sports revenue (UFC, Euroleague) averaged 40.5% year-on-year growth while its Events (live events) and Representation (WME talent agency, IMG Models) revenues averaged 3.8% and 8.6% declines.

This quarter, Endeavor's revenue grew 15.9% year on year to $1.85 billion, falling short of Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 27.1% over the next 12 months, an acceleration from this quarter.

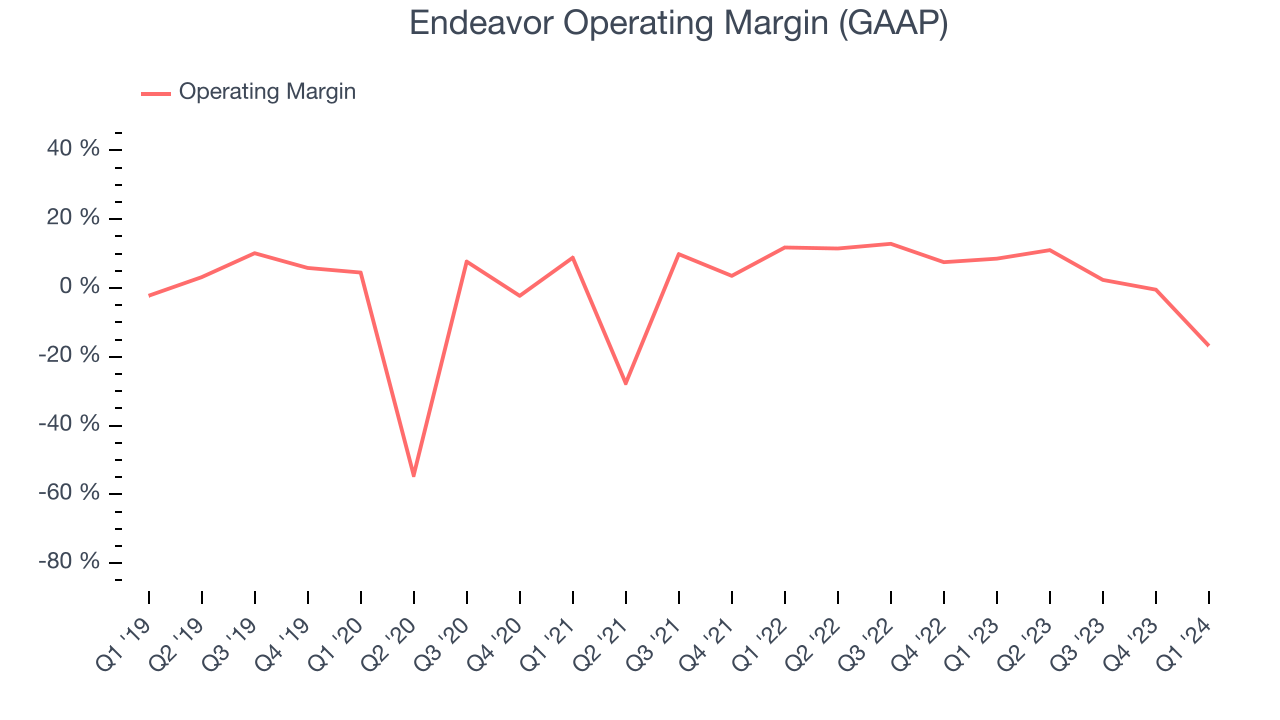

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Endeavor was profitable over the last two years but held back by its large expense base. Its average operating margin of 3.5% has been paltry for a consumer discretionary business.

In Q1, Endeavor generated an operating profit margin of negative 16.8%, down 25.4 percentage points year on year.

Over the next 12 months, Wall Street expects Endeavor to become profitable. Analysts are expecting the company’s LTM operating margin of negative 2.1% to rise to positive 11.5%.EPS

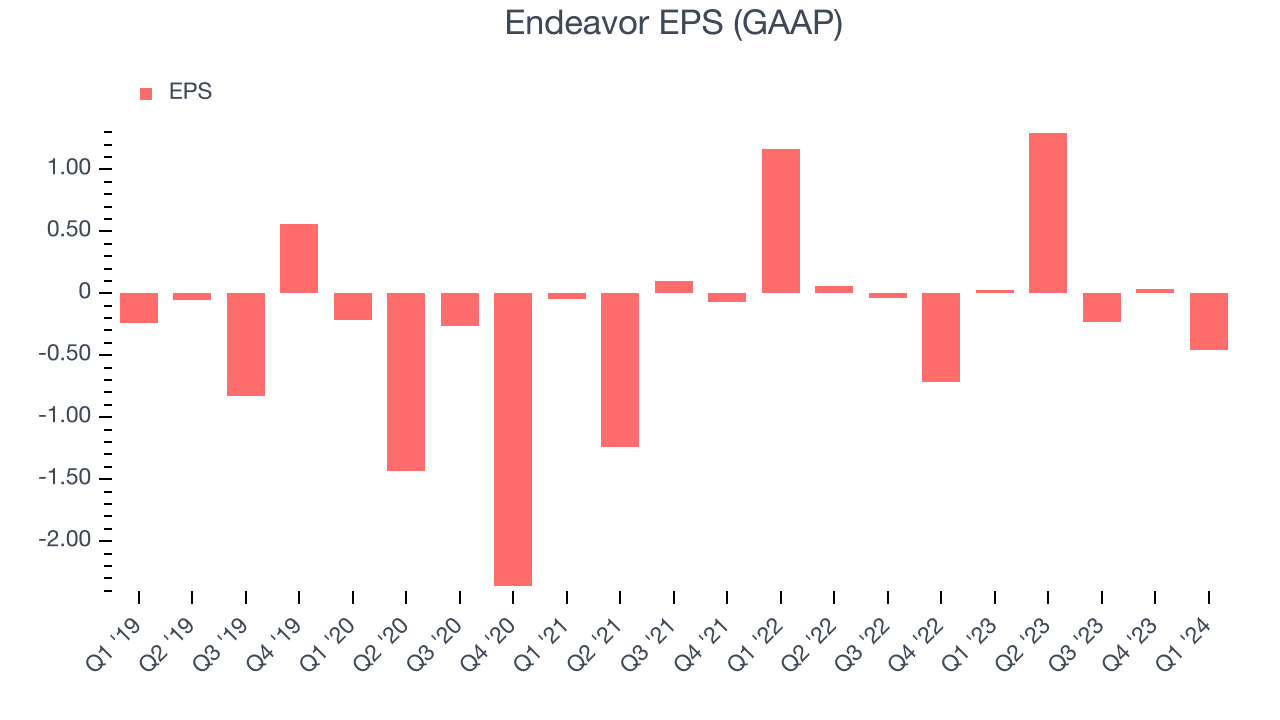

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last four years, Endeavor cut its earnings losses and improved its EPS by 33.6% each year.

In Q1, Endeavor reported EPS at negative $0.46, down from $0.03 in the same quarter last year. This print unfortunately missed analysts' estimates, but we care more about long-term EPS growth rather than short-term movements. Over the next 12 months, Wall Street expects Endeavor to grow its earnings. Analysts are projecting its LTM EPS of $0.64 to climb by 66.5% to $1.06.

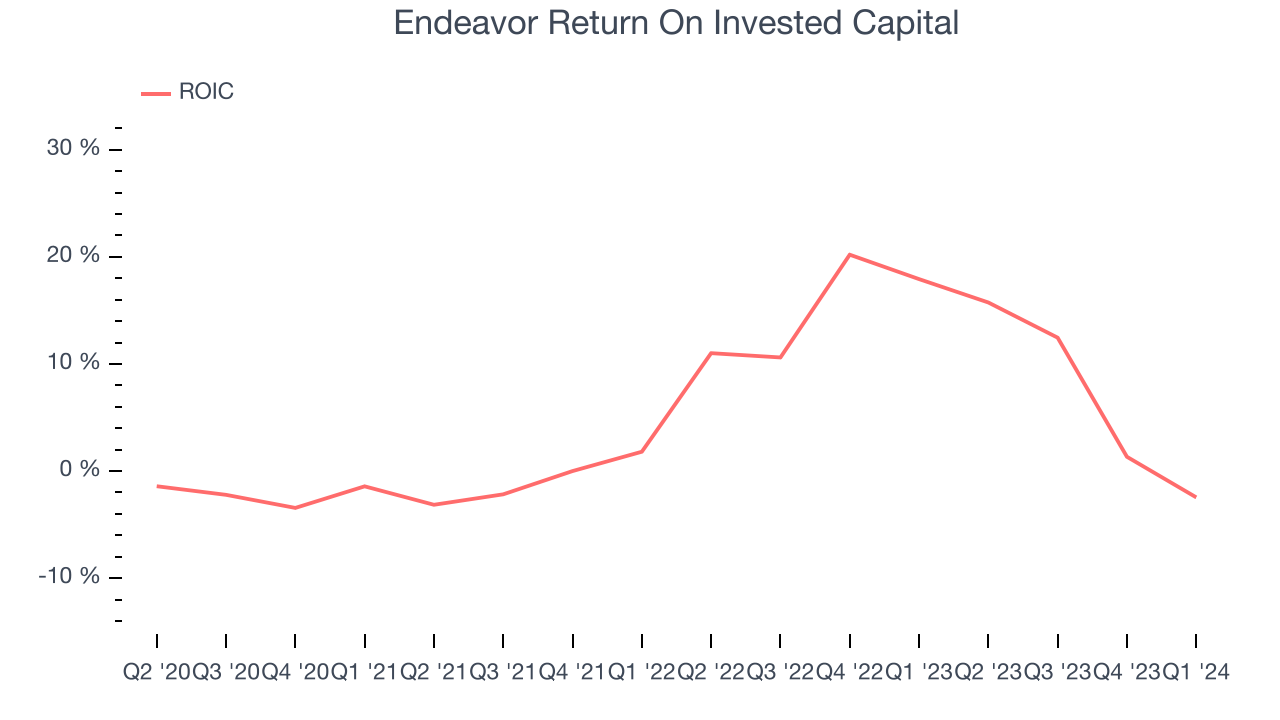

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Endeavor's five-year average return on invested capital was 4%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last few years, Endeavor's ROIC averaged 7.5 percentage point increases. This is a good sign, and if the company's returns keep rising, there's a chance it could evolve into an investable business.

Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly.

Endeavor reported $778.6 million of cash and $5.49 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $1.28 billion of EBITDA over the last 12 months, we view Endeavor's 3.7x net-debt-to-EBITDA ratio as safe. We also see its $357.1 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from Endeavor's Q1 Results

We struggled to find many strong positives in these results. Its operating margin missed and its EPS fell short of Wall Street's estimates. Overall, this was a mediocre quarter for Endeavor. The stock is flat after reporting and currently trades at $26.53 per share.

Is Now The Time?

Endeavor may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

Endeavor isn't a bad business, but it probably wouldn't be one of our picks. Its revenue growth has been uninspiring over the last four years, but at least growth is expected to increase in the short term. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its relatively low ROIC suggests it has historically struggled to find compelling business opportunities. On top of that, its operating margins reveal poor profitability compared to other consumer discretionary companies.

Endeavor's price-to-earnings ratio based on the next 12 months is 10.9x. In the end, beauty is in the eye of the beholder. While Endeavor wouldn't be our first pick, if you like the business, the shares are trading at a pretty interesting price right now.

Wall Street analysts covering the company had a one-year price target of $28.50 per share right before these results (compared to the current share price of $26.53).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.