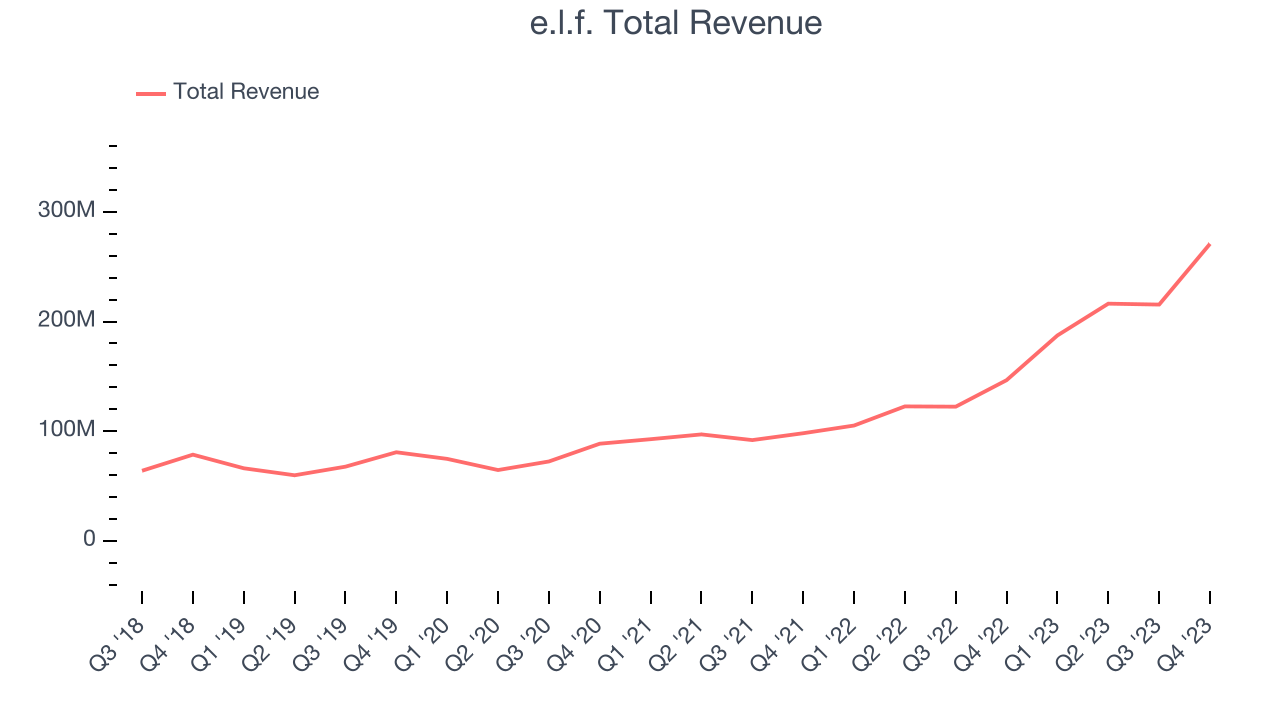

Cosmetics company e.l.f. Beauty (NYSE:ELF) reported results ahead of analysts' expectations in Q3 FY2024, with revenue up 84.9% year on year to $270.9 million. The company's full-year revenue guidance of $985 million at the midpoint also came in 6.2% above analysts' estimates. It made a non-GAAP profit of $0.74 per share, improving from its profit of $0.48 per share in the same quarter last year.

Is now the time to buy e.l.f.? Find out by accessing our full research report, it's free.

e.l.f. (ELF) Q3 FY2024 Highlights:

- Revenue: $270.9 million vs analyst estimates of $238.9 million (13.4% beat)

- EPS (non-GAAP): $0.74 vs analyst estimates of $0.56 (32.7% beat)

- The company lifted its revenue guidance for the full year from $901 million to $985 million at the midpoint, a 9.3% increase

- Free Cash Flow was -$21.65 million, down from $27.07 million in the previous quarter

- Gross Margin (GAAP): 70.8%, up from 67.4% in the same quarter last year

- Market Capitalization: $9.37 billion

e.l.f. Beauty (NYSE:ELF), which stands for ‘eyes, lips, face’, offers high-quality beauty products at accessible price points.

Personal Care

Personal care products include lotions, fragrances, shampoos, cosmetics, and nutritional supplements, among others. While these products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. As with other consumer staples categories, personal care brands must exude quality and be priced optimally given the crowded competitive landscape. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

Sales Growth

e.l.f. is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefitting from better brand awareness and economies of scale. On the other hand, one advantage is that its growth rates can be higher because it's growing off a small base.

As you can see below, the company's annualized revenue growth rate of 43.7% over the last three years was incredible for a consumer staples business. Contributing to this was the acquisition of drugstore skincare brand Naturium for $355 million in cash and stock in August 2023.

This quarter, e.l.f. reported magnificent year-on-year revenue growth of 84.9%, and its $270.9 million in revenue beat Wall Street's estimates by 13.4%. Looking ahead, Wall Street expects sales to grow 23.7% over the next 12 months, a deceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Key Takeaways from e.l.f.'s Q3 Results

We were impressed by how significantly e.l.f. blew past analysts' revenue expectations this quarter. We were also glad its full-year revenue guidance came in higher than Wall Street's estimates. On the other hand, its operating margin missed analysts' expectations. Overall, we think this was a really good quarter that should please shareholders. The stock is up 1.7% after reporting and currently trades at $176.26 per share.

e.l.f. may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.