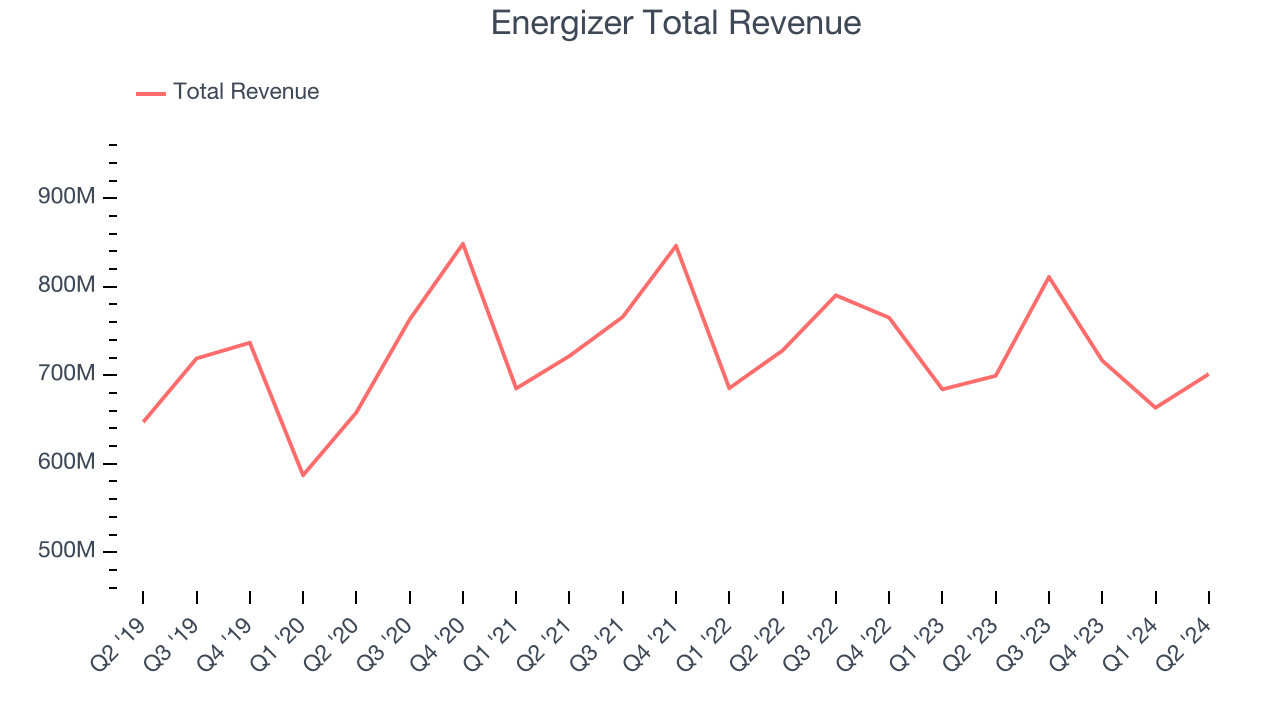

Battery and lighting company Energizer (NYSE:ENR) reported results in line with analysts' expectations in Q2 CY2024, with revenue flat year on year at $701.4 million. It made a non-GAAP profit of $0.79 per share, improving from its profit of $0.54 per share in the same quarter last year.

Is now the time to buy Energizer? Find out by accessing our full research report, it's free.

Energizer (ENR) Q2 CY2024 Highlights:

- Revenue: $701.4 million vs analyst estimates of $704.8 million (small miss)

- EPS (non-GAAP): $0.79 vs analyst estimates of $0.68 (16% beat)

- EPS (non-GAAP) guidance for Q3 CY2024 is $1.15 at the midpoint, below analyst estimates of $1.22

- EPS (non-GAAP) guidance for the full year is $3.25 at the midpoint, beating analyst estimates by 1.6%

- Gross Margin (GAAP): 39.5%, up from 38.8% in the same quarter last year

- Adjusted EBITDA Margin: 21.3%, up from 18.1% in the same quarter last year

- Free Cash Flow of $32.2 million, up from $10.3 million in the previous quarter

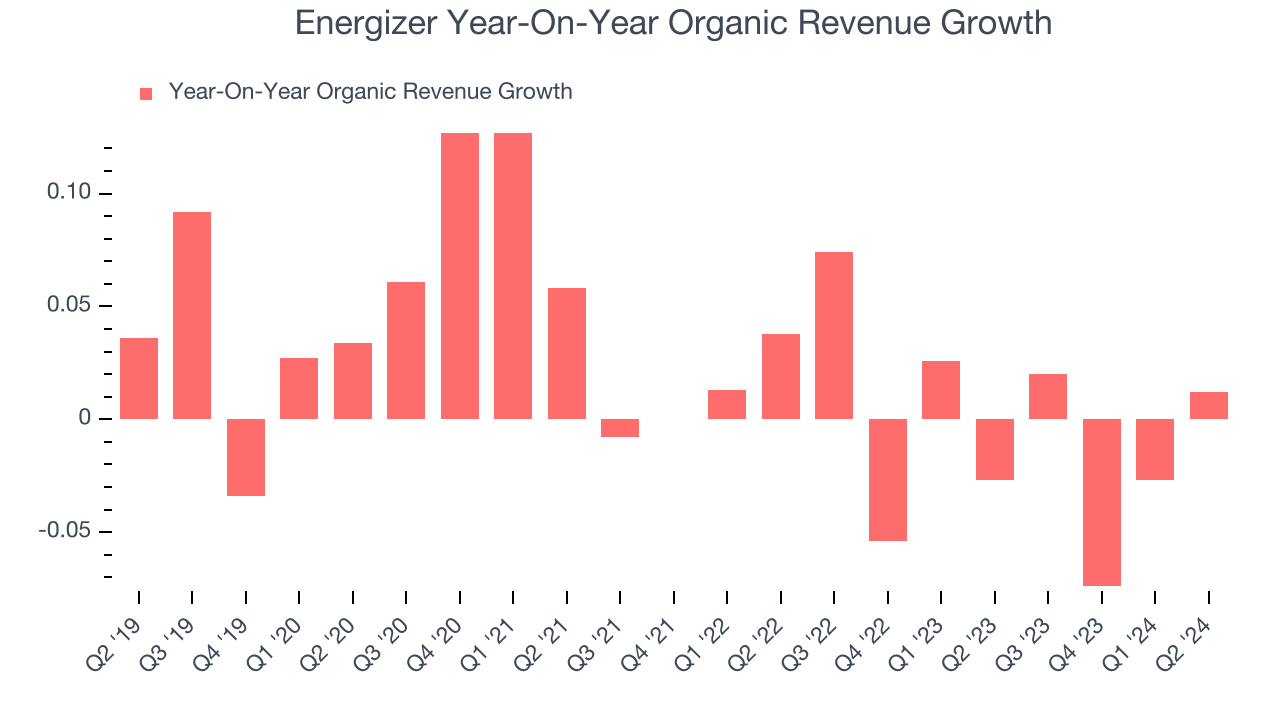

- Organic Revenue rose 1.2% year on year (-2.7% in the same quarter last year)

- Market Capitalization: $2.10 billion

"We are extremely pleased with our third quarter performance," said Mark LaVigne, Chief Executive Officer.

Masterminds behind the viral Energizer Bunny mascot, Energizer (NYSE:ENR) is one of the world's largest manufacturers of batteries.

Household Products

Household products stocks are generally stable investments, as many of the industry's products are essential for a comfortable and functional living space. Recently, there's been a growing emphasis on eco-friendly and sustainable offerings, reflecting the evolving consumer preferences for environmentally conscious options. These trends can be double-edged swords that benefit companies who innovate quickly to take advantage of them and hurt companies that don't invest enough to meet consumers where they want to be with regards to trends.

Sales Growth

Energizer carries some recognizable brands and products but is a mid-sized consumer staples company. Its size could bring disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the other hand, Energizer can still achieve high growth rates because its revenue base is not yet monstrous.

As you can see below, the company's revenue has declined over the last three years, dropping 1.4% annually. This is among the worst in the consumer staples industry, where demand is typically stable.

This quarter, Energizer's revenue grew 0.3% year on year to $701.4 million, falling short of Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 1.6% over the next 12 months, an acceleration from this quarter.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business's performance excluding the impacts of foreign currency fluctuations and one-time events such as mergers, acquisitions, and divestitures.

The demand for Energizer's products has barely risen over the last eight quarters. On average, the company's organic sales have been flat.

In the latest quarter, Energizer's organic sales rose 1.2% year on year. This growth was a well-appreciated turnaround from the 2.7% year-on-year decline it posted 12 months ago, showing the business is regaining momentum.

Key Takeaways from Energizer's Q2 Results

It was good to see Energizer beat analysts' EPS expectations this quarter. We were also glad its full-year earnings guidance exceeded Wall Street's estimates. On the other hand, its organic revenue unfortunately missed analysts' expectations and its gross margin missed Wall Street's estimates. Overall, this was a mixed quarter for Energizer. The stock remained flat at $29.24 immediately after reporting.

So should you invest in Energizer right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.