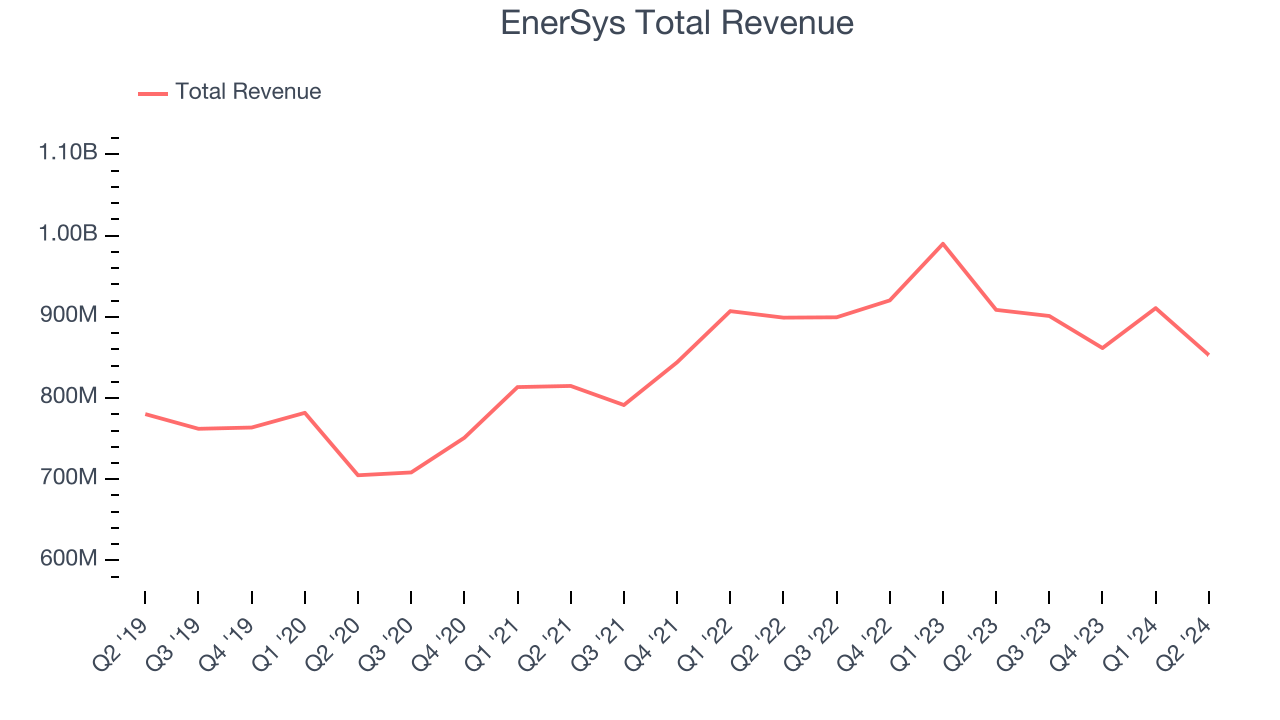

Battery manufacturer EnerSys (NYSE:ENS) fell short of analysts' expectations in Q2 CY2024, with revenue down 6.1% year on year to $852.9 million. On the other hand, the company expects next quarter's revenue to be around $900 million, in line with analysts' estimates. It made a non-GAAP profit of $1.98 per share, improving from its profit of $1.88 per share in the same quarter last year.

Is now the time to buy EnerSys? Find out by accessing our full research report, it's free.

EnerSys (ENS) Q2 CY2024 Highlights:

- Revenue: $852.9 million vs analyst estimates of $876.4 million (2.7% miss)

- EPS (non-GAAP): $1.98 vs analyst estimates of $1.95 (1.4% beat)

- Revenue Guidance for Q3 CY2024 is $900 million at the midpoint, roughly in line with what analysts were expecting

- The company lifted its revenue guidance for the full year from $3.75 billion to $3.81 billion at the midpoint, a 1.6% increase

- EPS (non-GAAP) guidance for Q3 CY2024 is $2.10 at the midpoint, roughly in line with what analysts were expecting

- EPS (non-GAAP) guidance for the full year is $9 at the midpoint, beating analyst estimates by 3.7%

- Gross Margin (GAAP): 28%, up from 26.8% in the same quarter last year

- Adjusted EBITDA Margin: 14.2%, in line with the same quarter last year

- Free Cash Flow was -$25.74 million, down from $109.4 million in the previous quarter

- Market Capitalization: $3.85 billion

Supplying batteries that power equipment as big as mining rigs, EnerSys (NYSE:ENS) manufactures various kinds of batteries for a range of industries.

Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one tends to grow for years. Regrettably, EnerSys's sales grew at a weak 3.9% compounded annual growth rate over the last five years. This shows it failed to expand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. EnerSys's recent history shows its demand slowed as its annualized revenue growth of 1.2% over the last two years is below its five-year trend.

This quarter, EnerSys missed Wall Street's estimates and reported a rather uninspiring 6.1% year-on-year revenue decline, generating $852.9 million of revenue. For next quarter, the company is guiding for flat year on year revenue of $900 million, slowing from the 0.2% year-on-year increase it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 6.2% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

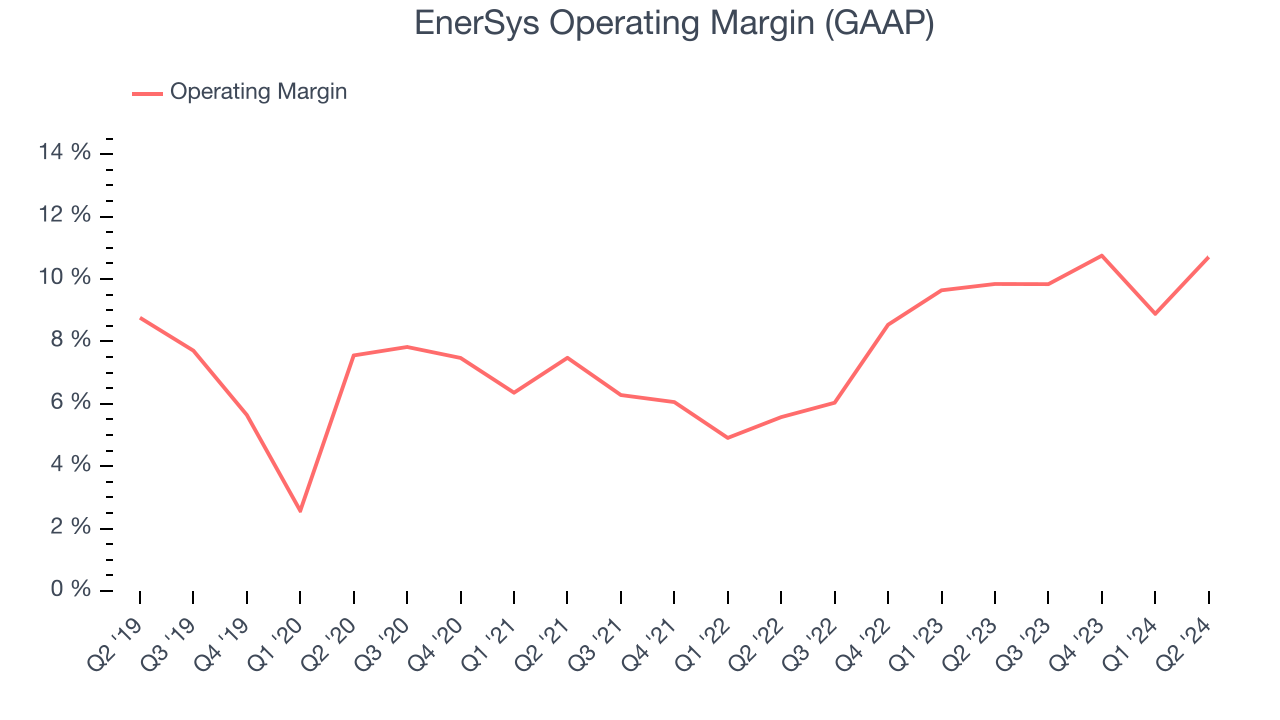

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling them, and, most importantly, keeping them relevant through research and development.

EnerSys was profitable over the last five years but held back by its large expense base. It demonstrated mediocre profitability for an industrials business, producing an average operating margin of 7.5%. This result isn't too surprising given its low gross margin as a starting point.

On the bright side, EnerSys's annual operating margin rose by 4.2 percentage points over the last five years

This quarter, EnerSys generated an operating profit margin of 10.7%, in line with the same quarter last year. This indicates the company's cost structure has recently been stable.

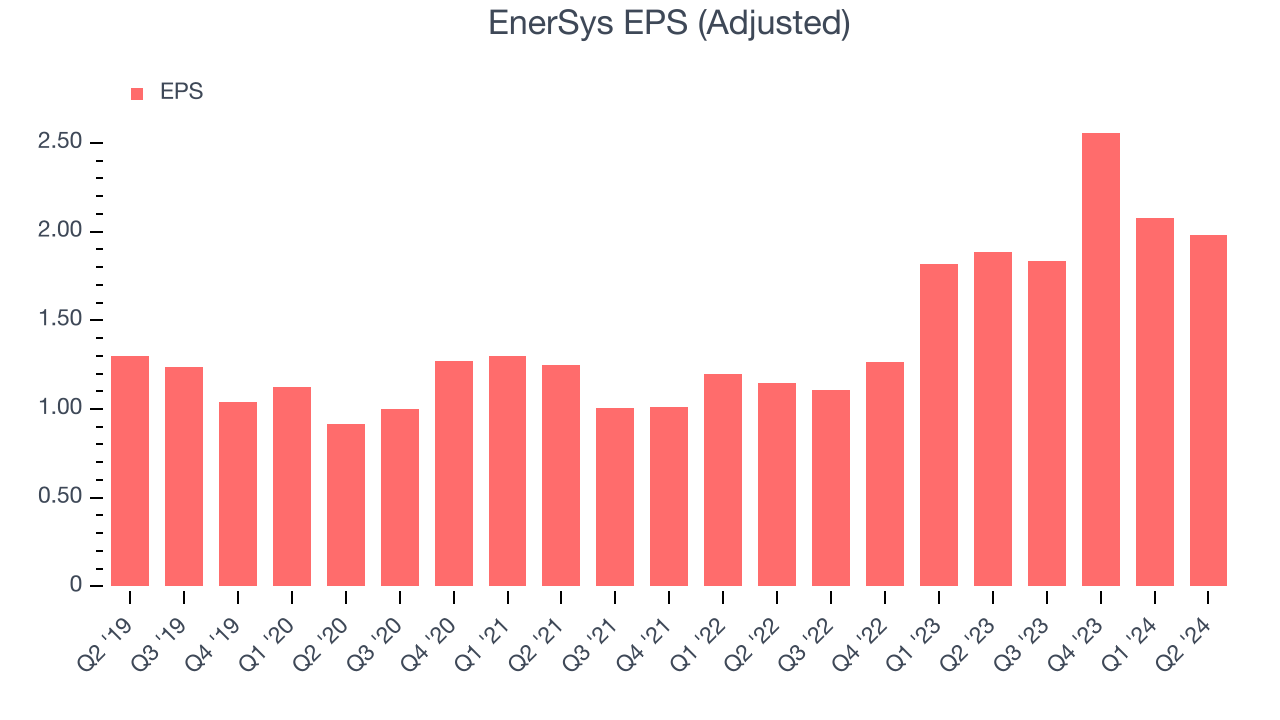

EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

EnerSys's EPS grew at a solid 10.8% compounded annual growth rate over the last five years, higher than its 3.9% annualized revenue growth. This tells us the company became more profitable as it expanded.

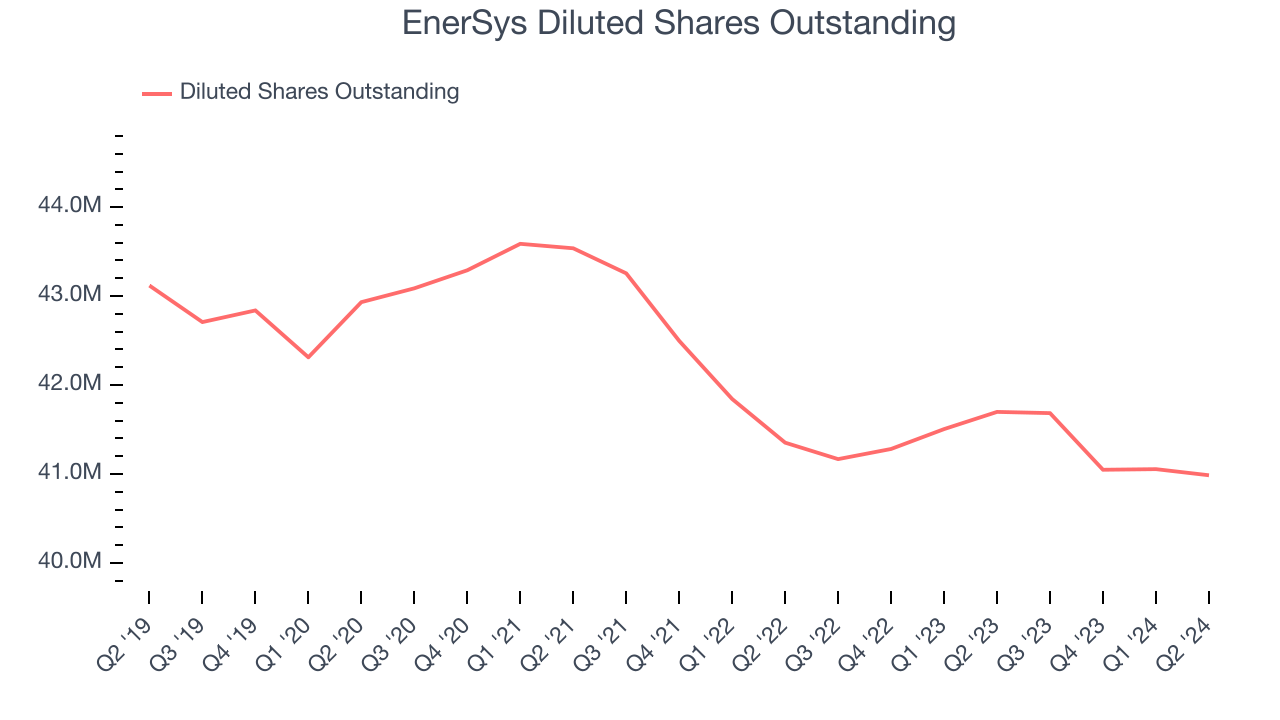

Diving into EnerSys's quality of earnings can give us a better understanding of its performance. As we mentioned earlier, EnerSys's operating margin was flat this quarter but expanded by 4.2 percentage points over the last five years. On top of that, its share count shrank by 4.9%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we also analyze EPS over a shorter period to see if we are missing a change in the business. For EnerSys, its two-year annual EPS growth of 39.1% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q2, EnerSys reported EPS at $1.98, up from $1.88 in the same quarter last year. This print beat analysts' estimates by 1.4%. Over the next 12 months, Wall Street expects EnerSys to grow its earnings. Analysts are projecting its EPS of $8.45 in the last year to climb by 4.5% to $8.83.

Key Takeaways from EnerSys's Q2 Results

It was great to see EnerSys's positive full-year sales outlook, which exceeded analysts' expectations. We were also glad its full-year EPS guidance exceeded Wall Street's estimates. On the other hand, its revenue unfortunately missed. Zooming out, we think this was a mixed quarter. The areas below expectations seem to be driving the move, and the stock traded down 2% to $93.30 immediately after reporting.

So should you invest in EnerSys right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.