Footwear and apparel retailer Foot Locker (NYSE:FL) announced better-than-expected results in Q4 FY2023, with revenue up 2% year on year to $2.38 billion. It made a non-GAAP profit of $0.38 per share, down from its profit of $0.97 per share in the same quarter last year.

Is now the time to buy Foot Locker? Find out by accessing our full research report, it's free.

Foot Locker (FL) Q4 FY2023 Highlights:

- Revenue: $2.38 billion vs analyst estimates of $2.28 billion (4.6% beat)

- EPS (non-GAAP): $0.38 vs analyst estimates of $0.32 (18.6% beat)

- Guidance for full year EPS (non-GAAP): $1.70 vs analyst estimates of $1.95 (12.8% miss)

- Free Cash Flow of $112 million, down 18.8% from the same quarter last year

- Gross Margin (GAAP): 26.8%, down from 30.2% in the same quarter last year

- Same-Store Sales were down 0.7% year on year

- Store Locations: 2,523 at quarter end, decreasing by 191 over the last 12 months

- Market Capitalization: $3.23 billion

Mary Dillon, President and Chief Executive Officer, said, "We are pleased to report fourth quarter results ahead of our expectations, including meaningfully accelerated sales trends relative to the third quarter, earnings per share that exceeded our guidance range, and improvements across multiple KPIs. As we continued to deliver on the strategic imperatives of our Lace Up Plan, we built significant momentum through the holiday season, driven by full-price selling in addition to compelling promotions. We also proactively reinvested in markdowns to end the year with leaner inventory levels compared to our expectations."

Known for store associates whose uniforms resemble those of referees, Foot Locker (NYSE:FL) is a specialty retailer that sells athletic footwear, clothing, and accessories.

Athletic Apparel and Footwear Retailer

Apparel and footwear was once a category thought to be relatively safe from major e-commerce penetration because of the need to try on, touch, and feel products, but the category is now meaningfully transacted online. Everyone still needs clothes and shoes to go outside unless they want some curious (or horrified) looks. But this ongoing digitization is forcing apparel and footwear retailers–that once only had brick-and-mortar stores–to respond with omnichannel offerings. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stagnate, so the evolution of clothing and shoes sellers marches on.

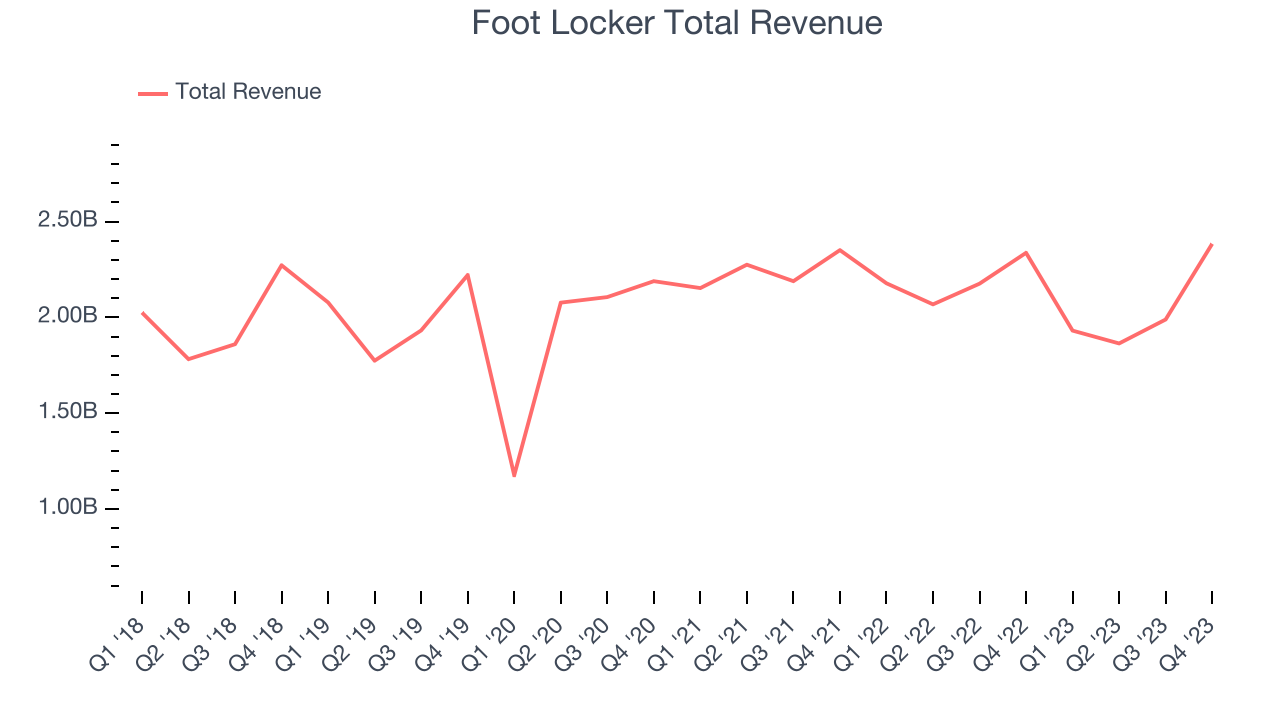

Sales Growth

Foot Locker is larger than most consumer retail companies and benefits from economies of scale, giving it an edge over its competitors.

As you can see below, the company's revenue was flat over the last four years (we compare to 2019 to normalize for COVID-19 impacts) as its store count dropped.

This quarter, Foot Locker reported decent year-on-year revenue growth of 2%, and its $2.38 billion in revenue topped Wall Street's estimates by 4.6%. Looking ahead, Wall Street expects revenue to decline 2% over the next 12 months, a deceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

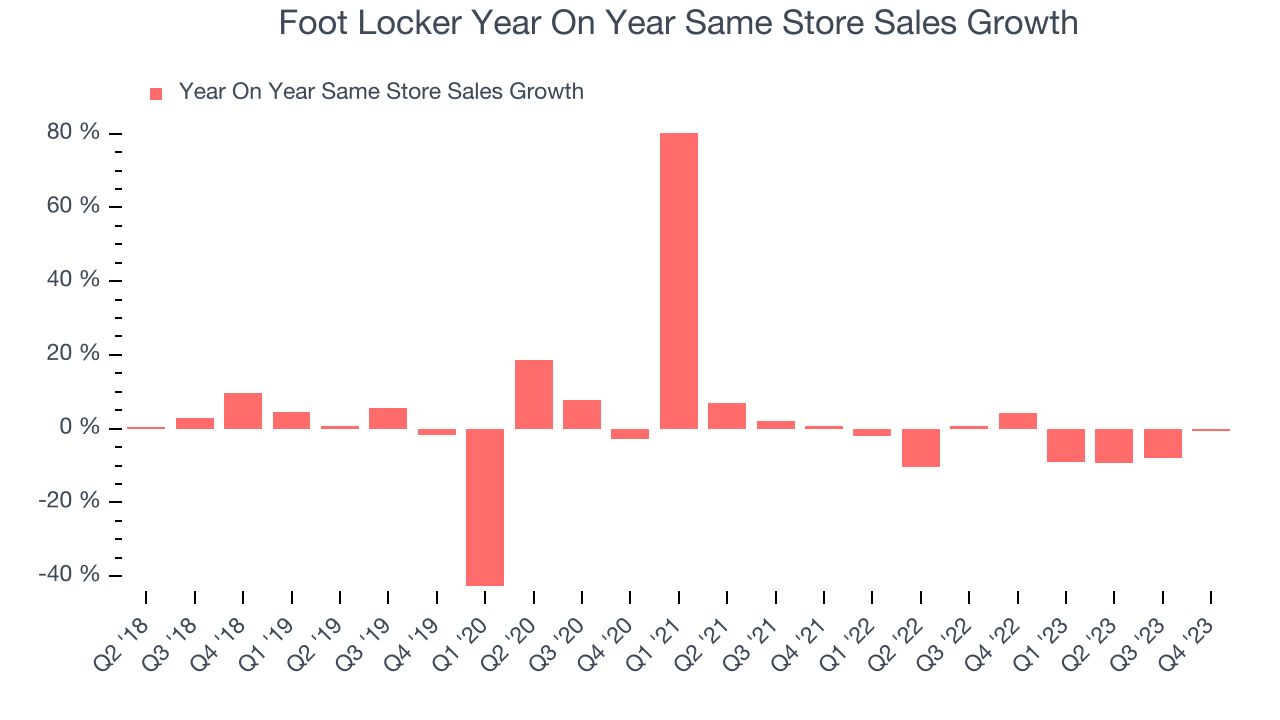

Same-Store Sales

Same-store sales growth is an important metric that tracks demand for a retailer's established brick-and-mortar stores and e-commerce platform.

Foot Locker's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 4.3% year on year. The company has been reducing its store count as fewer locations sometimes lead to higher same-store sales, but that hasn't been the case here.

In the latest quarter, Foot Locker's year on year same-store sales were flat. By the company's standards, this growth was a meaningful deceleration from the 4.2% year-on-year increase it posted 12 months ago. We'll be watching Foot Locker closely to see if it can reaccelerate growth.

Key Takeaways from Foot Locker's Q4 Results

We liked how revenue and EPS outperformed Wall Street's estimates. On the other hand, its full-year earnings forecast missed analysts' expectations by a large amount, and this is dragging the stock down. The stock is down 18.7% after reporting, trading at $27.9 per share.

So should you invest in Foot Locker right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.