Packaged bakery food company Flower Foods (NYSE:FLO) reported results in line with analysts' expectations in Q4 FY2023, with revenue up 4.3% year on year to $1.13 billion. On the other hand, the company's full-year revenue guidance of $5.13 billion at the midpoint came in 1.5% below analysts' estimates. It made a non-GAAP profit of $0.20 per share, down from its profit of $0.23 per share in the same quarter last year.

Flowers Foods (FLO) Q4 FY2023 Highlights:

- Revenue: $1.13 billion vs analyst estimates of $1.13 billion (small beat)

- EPS (non-GAAP): $0.20 vs analyst expectations of $0.21 (4.5% miss)

- Management's revenue guidance for the upcoming financial year 2024 is $5.13 billion at the midpoint, missing analyst estimates by 1.5% and implying 0.8% growth (vs 5.9% in FY2023)

- Management's EPS guidance for the upcoming financial year 2024 is $1.25 at the midpoint, missing analyst estimates by 3.0%

- Free Cash Flow of $59.96 million, down 40.8% from the previous quarter

- Gross Margin (GAAP): 47.9%, up from 46.8% in the same quarter last year

- Sales Volumes were down 2.4% year on year

- Market Capitalization: $4.89 billion

With Wonder Bread as its premier brand, Flower Foods (NYSE:FLO) is a packaged foods company that focuses on bakery products such as breads, buns, and cakes.

The company traces its roots back to 1919, when brothers William Howard and Joseph Hampton Flowers commenced their operations with a single bakery and initially sold fresh bread directly to customers from a horse-drawn wagon. The company subsequently grew through organic means as well as through acquisitions, with the 2013 acquisition of Wonder Bread from Hostess as a notable one

Today, some notable products include Nature’s Own Whole Wheat and Honey Wheat Bread, Dave’s Killer Bread, Tastykake cupcakes and donuts, and Mrs. Freshley’s brownies and cakes. Flowers Foods’ core customer is the everyday American household. From the parent packing school lunches to the college student looking for a quick snack, their products have widespread appeal. Recognizing the evolving dietary needs and preferences of consumers, Flowers Foods has diversified its product range, including healthier bread options and organic choices.

The company’s baked goods can be found in many locations selling food and snacks. Wonder Bread and Flower Foods’ other brands are available in supermarkets, convenience stores, and mass retailers. Additionally, a significant portion of their products are sold to foodservice and vending companies.

Packaged Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods, prepared meals, or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences.The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Competitors in packaged bakery goods include Grupo Bimbo (BMV:BIMBO A), Hostess Brands, acquired by J.M. Smucker (NYSE:SJM), and Pepperidge Farm, a subsidiary of Campbell Soup (NYSE:CPB).Sales Growth

Flowers Foods is larger than most consumer staples companies and benefits from economies of scale, giving it an edge over its smaller competitors.

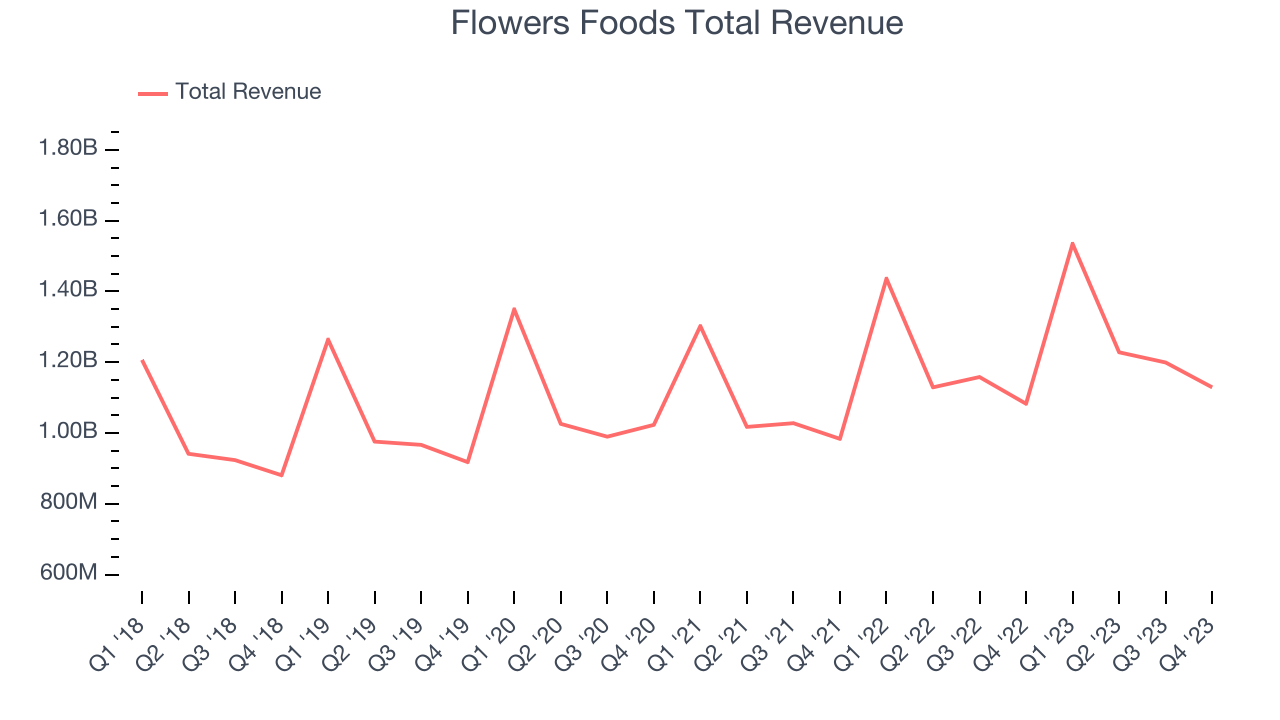

As you can see below, the company's annualized revenue growth rate of 5.1% over the last three years was weak, but to its credit, consumers bought more of its products.

This quarter, Flowers Foods grew its revenue by 4.3% year on year, and its $1.13 billion in revenue was in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 2.4% over the next 12 months, a deceleration from this quarter.

Gross Margin & Pricing Power

Gross profit margins tell us how much money a company gets to keep after paying for the direct costs of the goods it sells.

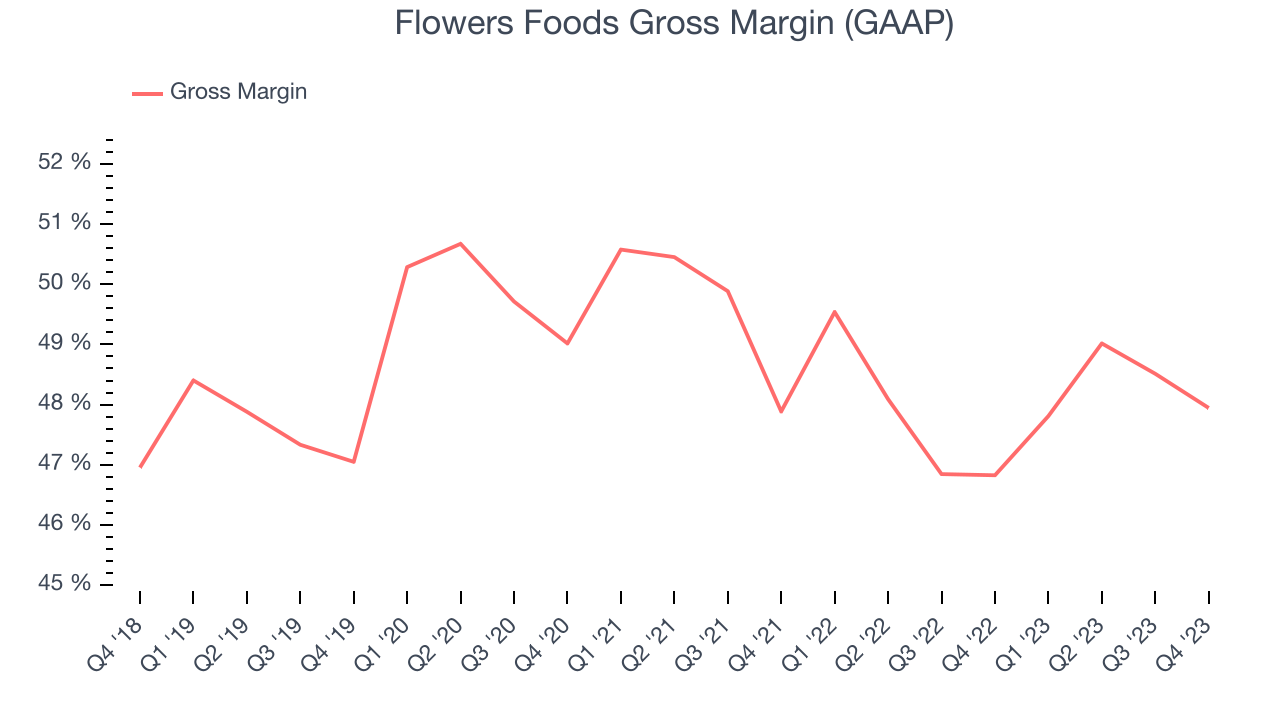

This quarter, Flowers Foods's gross profit margin was 47.9%, up 1.1 percentage points year on year. That means for every $1 in revenue, $0.52 went towards paying for raw materials, production of goods, and distribution expenses.

Flowers Foods has great unit economics for a consumer staples company, giving it ample room to invest in areas such as marketing and talent to grow its brand. As you can see above, it's averaged an impressive 48.1% gross margin over the last eight quarters. Its margin has also been trending up over the last 12 months, averaging 1.1% year-on-year increases each quarter. If this trend continues, it could suggest a less competitive environment where the company has better pricing power and more favorable input costs (such as raw materials).

Operating Margin

Operating margin is a key profitability metric for companies because it accounts for all expenses enabling a business to operate smoothly, including marketing and advertising, IT systems, wages, and other administrative costs.

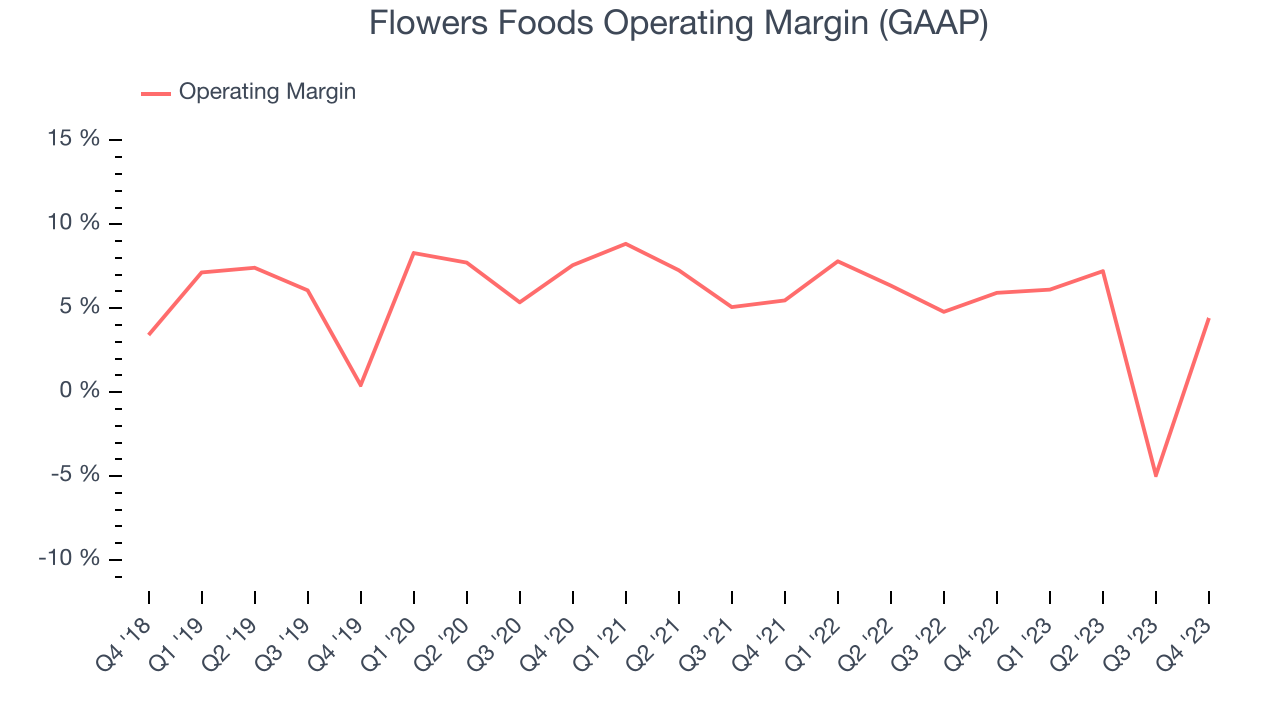

This quarter, Flowers Foods generated an operating profit margin of 4.4%, down 1.5 percentage points year on year. Conversely, the company's gross margin actually increased, so we can assume the reduction was driven by operational inefficiencies and a step up in discretionary spending in areas like corporate overhead and advertising.

Zooming out, Flowers Foods was profitable over the last two years but held back by its large expense base. It's demonstrated mediocre profitability for a consumer staples business, producing an average operating margin of 4.7%. On top of that, Flowers Foods's margin has declined by 2.9 percentage points on average over the last year. This shows the company is heading in the wrong direction, and investors are likely hoping for better results in the future.

Zooming out, Flowers Foods was profitable over the last two years but held back by its large expense base. It's demonstrated mediocre profitability for a consumer staples business, producing an average operating margin of 4.7%. On top of that, Flowers Foods's margin has declined by 2.9 percentage points on average over the last year. This shows the company is heading in the wrong direction, and investors are likely hoping for better results in the future.EPS

These days, some companies issue new shares like there's no tomorrow. That's why we like to track earnings per share (EPS) because it accounts for shareholder dilution and share buybacks.

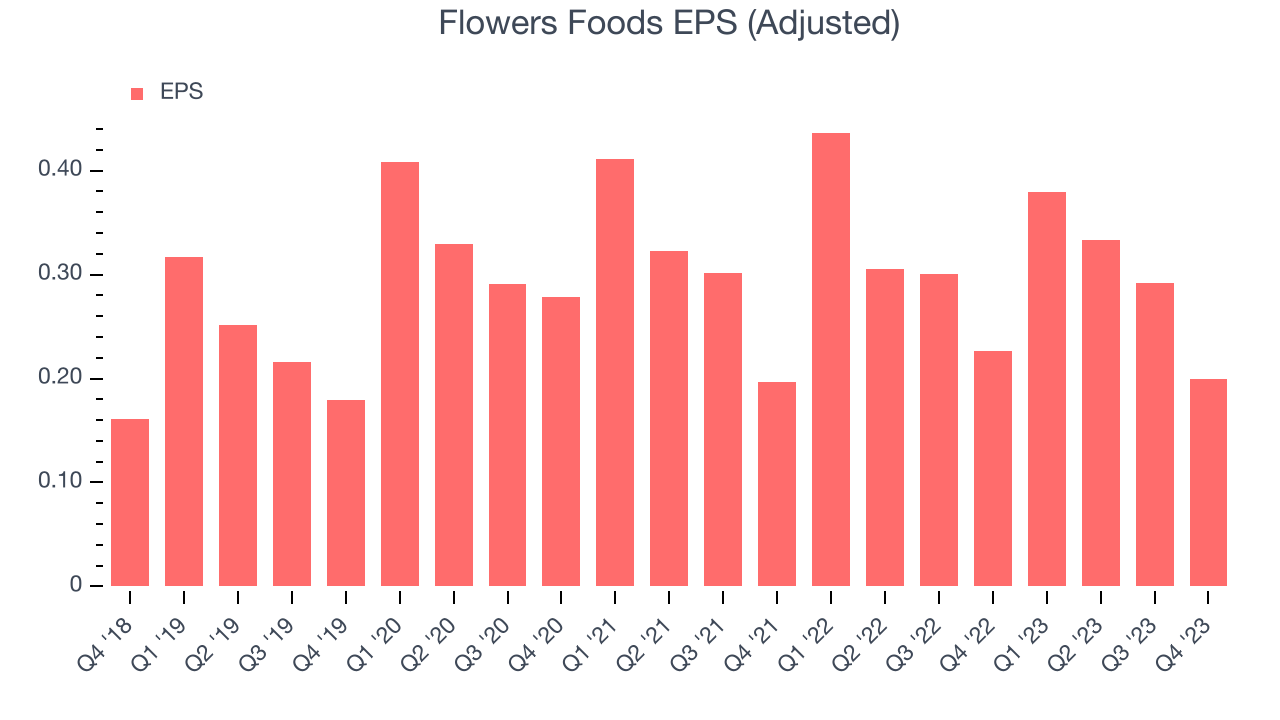

In Q4, Flowers Foods reported EPS at $0.20, down from $0.23 in the same quarter a year ago. This print unfortunately missed Wall Street's estimates, but we care more about long-term EPS growth rather than short-term movements.

Between FY2020 and FY2023, Flowers Foods's EPS dropped 7.9%, translating into 2.7% annualized declines. We tend to steer our readers away from companies with falling EPS, especially in the consumer staples sector, where shrinking earnings could imply changing secular trends or consumer preferences. If there's no earnings growth, it's difficult to build confidence in a business's underlying fundamentals, leaving a low margin of safety around the company's valuation (making the stock susceptible to large downward swings).

On the bright side, Wall Street expects the company's earnings to grow over the next 12 months, with analysts projecting an average 7.7% year-on-year increase in EPS.

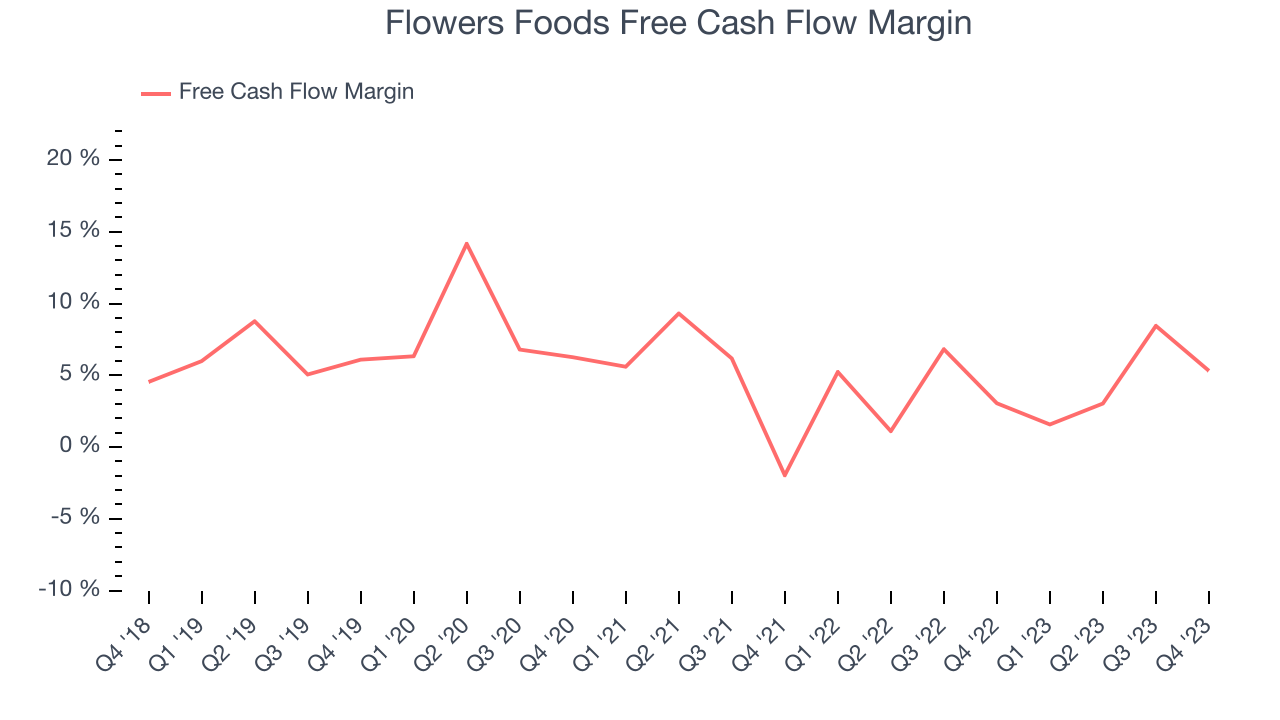

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Flowers Foods's free cash flow came in at $59.96 million in Q4, up 81.7% year on year. This result represents a 5.3% margin.

Over the last eight quarters, Flowers Foods has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 4.3%, subpar for a consumer staples business. Flowers Foods's margin has also been flat during that time, showing the company needs to take action and improve its cash profitability.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Flowers Foods's five-year average ROIC was 9.8%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, over the last two years, Flowers Foods's ROIC has averaged a 2.7 percentage point decrease each year. In conjunction with its already low returns, these declines suggest the company's profitable business opportunities are few and far between.

Key Takeaways from Flowers Foods's Q4 Results

It was encouraging to see Flowers Foods slightly top analysts' gross margin expectations this quarter. That stood out as a positive in these results. On the other hand, its operating margin missed analysts' expectations and both its full-year revenue and full-year EPS guidance missed Wall Street's estimates. The company called out a challenging backdrop for operations, but one bright spot was that their 'Dave's Killer Bread' brand became a $1 billion brand, which is a major milestone in the consumer staples world. Overall, the results were mixed but could have been better with regards to the outlook. The stock is up 1.5% after reporting and currently trades at $23.75 per share.

Is Now The Time?

Flowers Foods may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Flowers Foods, we'll be cheering from the sidelines. Its revenue growth has been a little slower over the last three years, and analysts expect growth to deteriorate from here. And while its gross margins are a strong starting point for the overall profitability of the business, the downside is its declining EPS over the last three years makes it hard to trust. On top of that, its operating margins are below average compared to other consumer staples companies.

Flowers Foods's price-to-earnings ratio based on the next 12 months is 18.0x. While we've no doubt one can find things to like about Flowers Foods, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $24 per share right before these results (compared to the current share price of $23.75).

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.