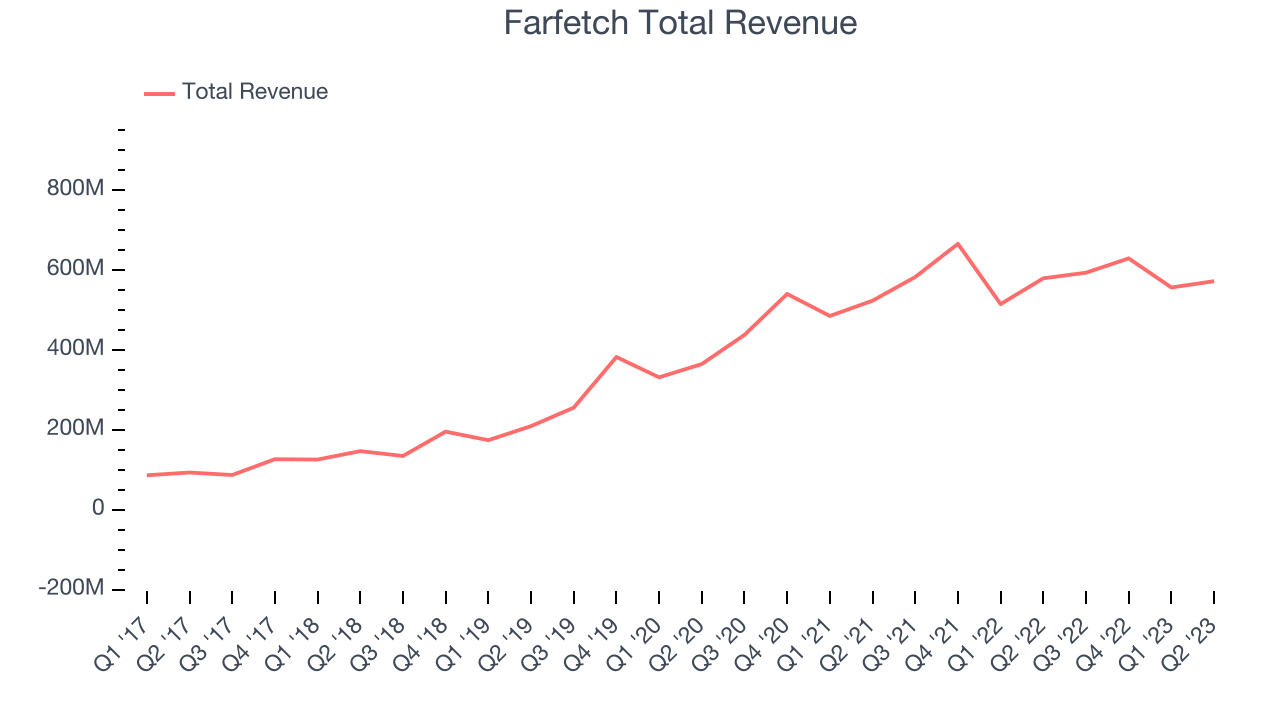

Online luxury marketplace Farfetch (NYSE: FTCH) missed analysts' expectations in Q2 FY2023, with revenue down 1.25% year on year to $572.1 million. Farfetch made a GAAP loss of $281.3 million, down from its profit of $67.7 million in the same quarter last year.

Is now the time to buy Farfetch? Find out by accessing our full research report, it's free.

Farfetch (FTCH) Q2 FY2023 Highlights:

- Revenue: $572.1 million vs analyst estimates of $650.7 million (12.1% miss)

- EPS (non-GAAP): -$0.21 vs analyst estimates of -$0.23

- Free Cash Flow of $42 million is up from -$163 million in the previous quarter

- Gross Margin (GAAP): 42.5%, down from 46.2% in the same quarter last year

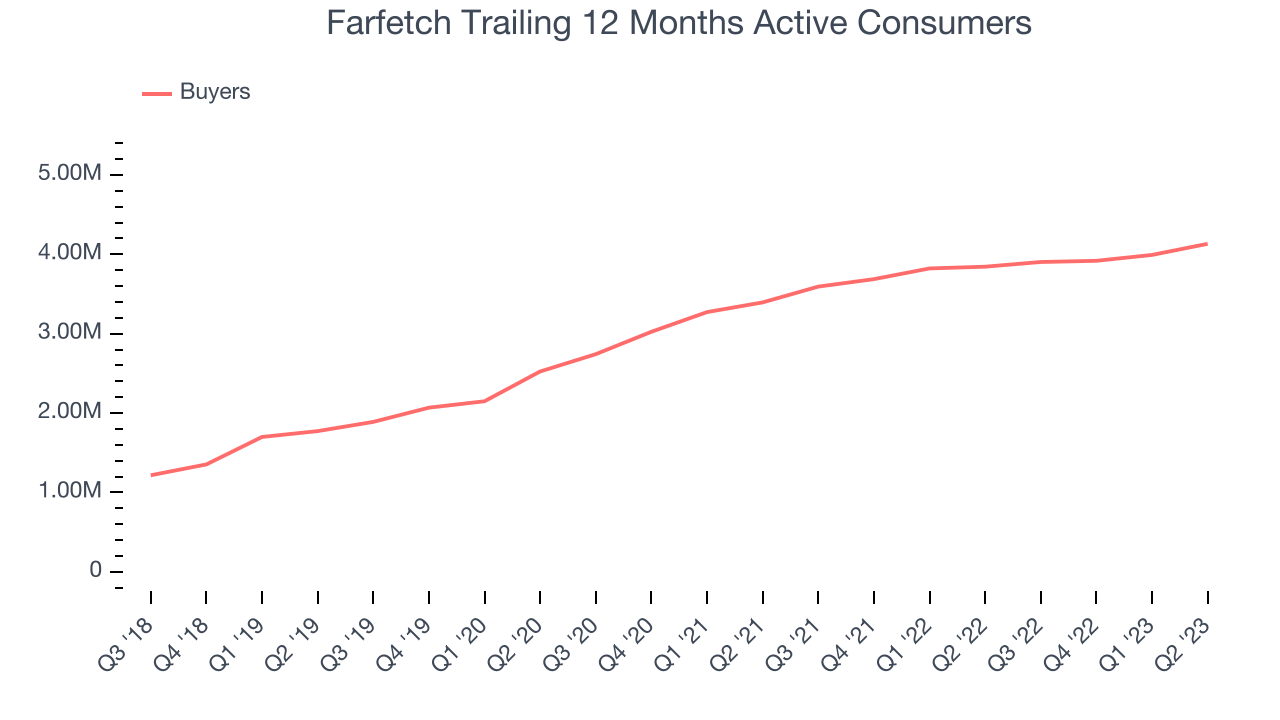

- Trailing 12 Months Active Consumers: 4.13 million, up 288 thousand year on year

José Neves, Farfetch Founder, Chairman and CEO, said: “Our Q2 results show Farfetch is growing, becoming more efficient, and executing on our key strategic priorities. We have also taken decisive action to adapt to the macro environment of the last 18 months. 2023 is set up to be a great year for Farfetch, toward strong GMV growth, Adjusted EBITDA profitability and positive free cash flow. All the while we remain steadfast on delivering our strategic vision of becoming the global platform for luxury.”

Inspired by the idea of allowing anyone to buy clothes from landmark boutiques of cities like Paris or Milan without having to leave their couch, Farfetch (NYSE: FTCH) is a global marketplace for luxury fashion, connecting boutiques, brands and consumers.

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission paying sellers, generating flywheel scale effects which feed back into further customer acquisition.

Sales Growth

Farfetch's revenue growth over the last three years has been strong, averaging 23.2% annually. This quarter, Farfetch reported a year on year revenue decline of 1.25%, missing analysts' expectations.

Ahead of the earnings results, analysts covering the company were projecting sales to grow 31.1% over the next 12 months.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Usage Growth

As an online marketplace, Farfetch generates revenue growth by increasing both the number of buyers on its platform and the average order size in dollars.

Over the last two years, Farfetch's active buyers, a key performance metric for the company, grew 13.7% annually to 4.13 million. This is solid growth for a consumer internet company.

In Q2, Farfetch added 288 thousand active buyers, translating into 7.49% year-on-year growth.

Key Takeaways from Farfetch's Q2 Results

Although Farfetch, which has a market capitalization of $1.91 billion, has been burning cash over the last 12 months, its more than $671.3 million in cash on hand gives it the flexibility to continue prioritizing growth over profitability.

We struggled to find many strong positives in these results. The company missed on key metrics such as gross merchandise value (GMV), active consumers, revenue, and adjusted EBITDA. Its revenue missed by a significant margin and growth also slowed. Looking ahead, the company lowered its full year GMV guidance meaningfully and also cut adjusted EBITDA guidance for the same period. Overall, the results were quite bad, with little to no major positives. The company is down 33.5% on the results and currently trades at $3.17 per share.

Farfetch may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.