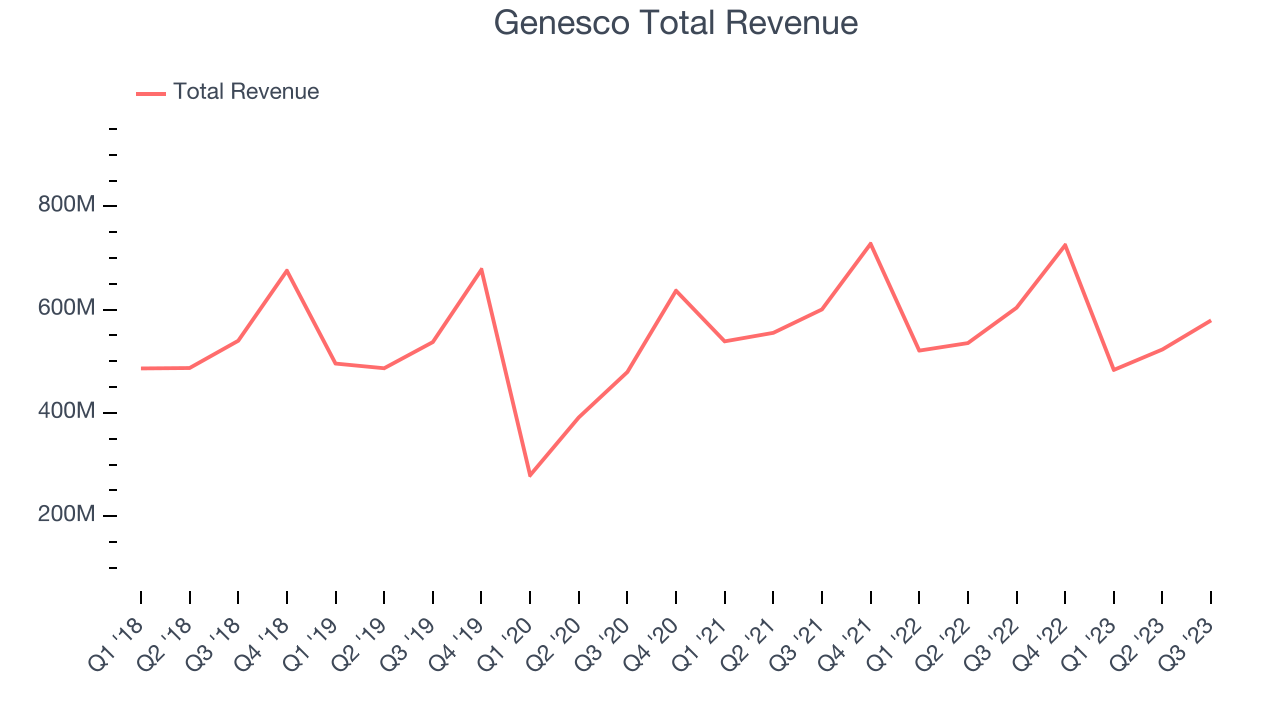

Footwear, apparel, and accessories retailer Genesco (NYSE:GCO) fell short of analysts' expectations in Q3 FY2024, with revenue down 4.1% year on year to $579.3 million. It made a non-GAAP profit of $0.57 per share, down from its profit of $1.65 per share in the same quarter last year.

Is now the time to buy Genesco? Find out by accessing our full research report, it's free.

Genesco (GCO) Q3 FY2024 Highlights:

- Revenue: $579.3 million vs analyst estimates of $588.6 million (1.6% miss)

- EPS (non-GAAP): $0.57 vs analyst expectations of $0.84 (31.6% miss)

- Fiscal year 2024 EPS meaningfully lowered ($1.75 at the midpoint from $2.25 previous, Consensus $2.31)

- Gross Margin (GAAP): 48.1%, down from 48.7% in the same quarter last year

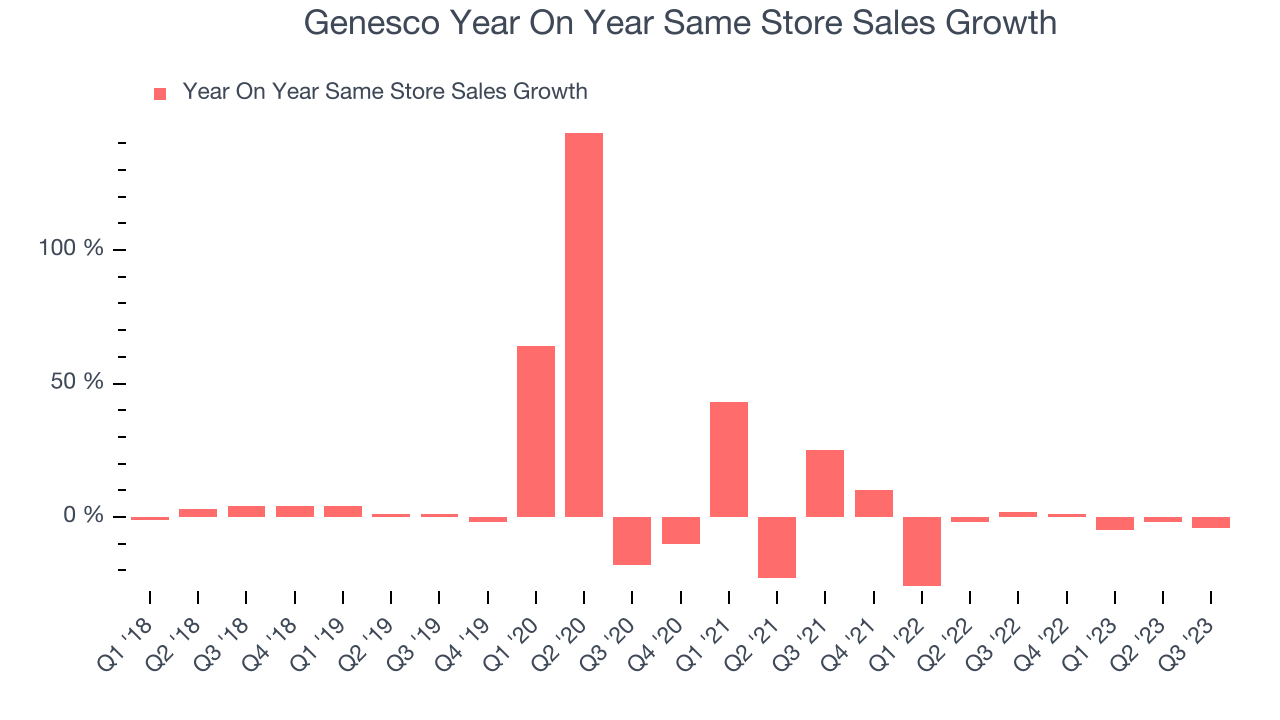

- Same-Store Sales were down 4% year on year (miss vs. expectations of down ~2% year on year)

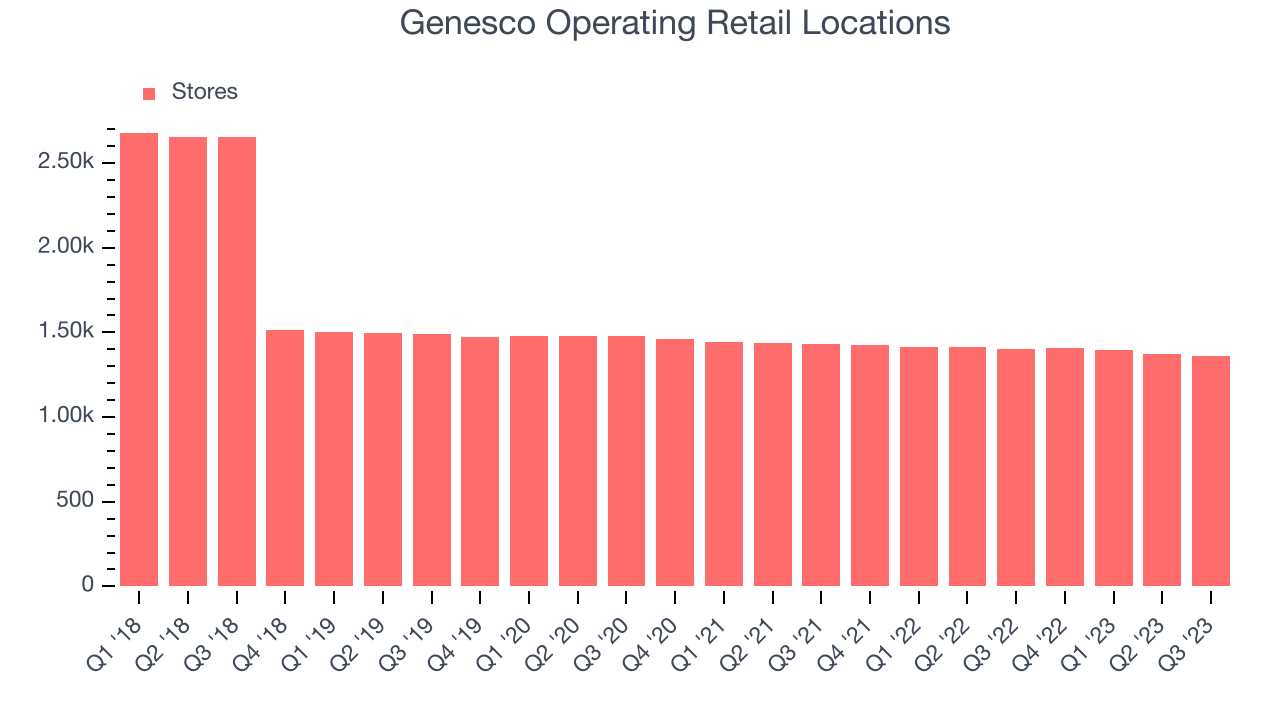

- Store Locations: 1,360 at quarter end, decreasing by 44 over the last 12 months

Mimi E. Vaughn, Genesco’s Board Chair, President and Chief Executive Officer, said, “Following a good Back-to-School season, demand in October softened in an ongoing challenging operating environment, along with a delayed start to the fall selling season. Disruptions related to implementation of a new ERP system for our branded businesses added to the pressure, all leading to results that were below our expectations. Despite these headwinds, we were pleased to see sales trends within our Journeys business continue to sequentially improve, and Schuh and Johnston & Murphy deliver record third-quarter sales. In the meantime, we continued to inject Journeys’ product assortment with more of the newness and must-have items our customer desires, while also executing on our cost reduction and store closure plans.”

Spanning a broad range of styles, brands, and prices, Genesco (NYSE:GCO) sells footwear, apparel, and accessories through multiple brands and banners.

Footwear Retailer

Footwear sales–like their apparel counterparts–are driven by seasons, trends, and innovation more so than absolute need and similarly face the bigger-picture secular trend of e-commerce penetration. Footwear plays a part in societal belonging, personal expression, and occasion, and retailers selling shoes recognize this. Therefore, they aim to balance selection, competitive prices, and the latest trends to attract consumers. Unlike their apparel counterparts, footwear retailers most sell popular third-party brands (as opposed to their own exclusive brands), which could mean less exclusivity of product but more nimbleness to pivot to what’s hot.

Sales Growth

Genesco is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale.

As you can see below, the company's annualized revenue growth rate of 1.3% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was weak as its store count dropped.

This quarter, Genesco reported a rather uninspiring 4.1% year-on-year revenue decline, missing Wall Street's expectations. Looking ahead, analysts expect sales to grow 1.6% over the next 12 months.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Number of Stores

When a retailer like Genesco is shuttering stores, it usually means that brick-and-mortar demand is less than supply, and the company is responding by closing underperforming locations and possibly shifting sales online. Since last year, Genesco's store count shrank by 44 locations, or 3.1%, to 1,360 total retail locations in the most recently reported quarter.

Taking a step back, the company has generally closed its stores over the last two years, averaging a 2.1% annual decline in its physical footprint. A smaller store base means that the company must rely on higher foot traffic and sales per customer at its remaining stores as well as e-commerce sales to fuel revenue growth.

Same-Store Sales

A company's same-store sales growth shows the year-on-year change in sales for its brick-and-mortar stores that have been open for at least a year, give or take, and e-commerce platform. This is a key performance indicator for retailers because it measures organic growth and demand.

Genesco's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 3.3% year on year. The company has been reducing its store count as fewer locations sometimes lead to higher same-store sales, but that hasn't been the case here.

In the latest quarter, Genesco's same-store sales fell 4% year on year. This decline was a reversal from the 2% year-on-year increase it posted 12 months ago. We'll be keeping a close eye on the company to see if this turns into a longer-term trend.

Key Takeaways from Genesco's Q3 Results

With a market capitalization of $430 million, Genesco is among smaller companies, but its more than $21.69 million in cash on hand and near break-even free cash flow margins puts it in a stable financial position.

We struggled to find many strong positives in these results. Same-store sales, revenue, EPS all missed. Management blamed "a challenging operating environment" and a delayed ERP system implementation internally for the weakness. Consumer demand remains "choppy" and Genesco plans to increase promotions to bring in shoppers, which will likely lead to weaker gross margins. The most worrisome aspect of the quarter was that the company's full-year earnings forecast was lowered drastically and underwhelmed. Overall, this was a mediocre quarter for Genesco. The company is down 12.2% on the results and currently trades at $32.85 per share.

Genesco may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.