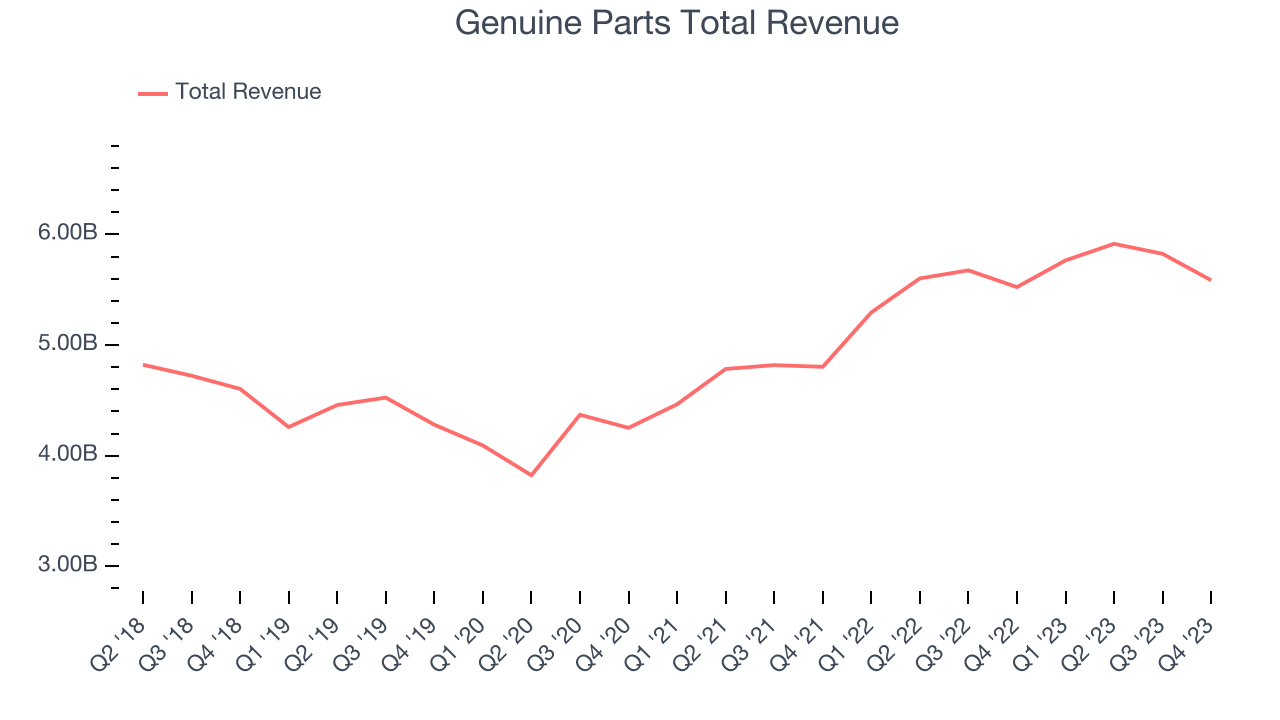

Auto and industrial parts retailer Genuine Parts (NYSE:GPC) fell short of analysts' expectations in Q4 FY2023, with revenue up 1.1% year on year to $5.59 billion. It made a non-GAAP profit of $2.26 per share, improving from its profit of $2.05 per share in the same quarter last year.

Is now the time to buy Genuine Parts? Find out by accessing our full research report, it's free.

Genuine Parts (GPC) Q4 FY2023 Highlights:

- Revenue: $5.59 billion vs analyst estimates of $5.66 billion (1.4% miss)

- EPS (non-GAAP): $2.26 vs analyst estimates of $2.20 (2.7% beat)

- Free Cash Flow of $190.3 million, up 50.2% from the same quarter last year

- Gross Margin (GAAP): 36.4%, up from 35.6% in the same quarter last year

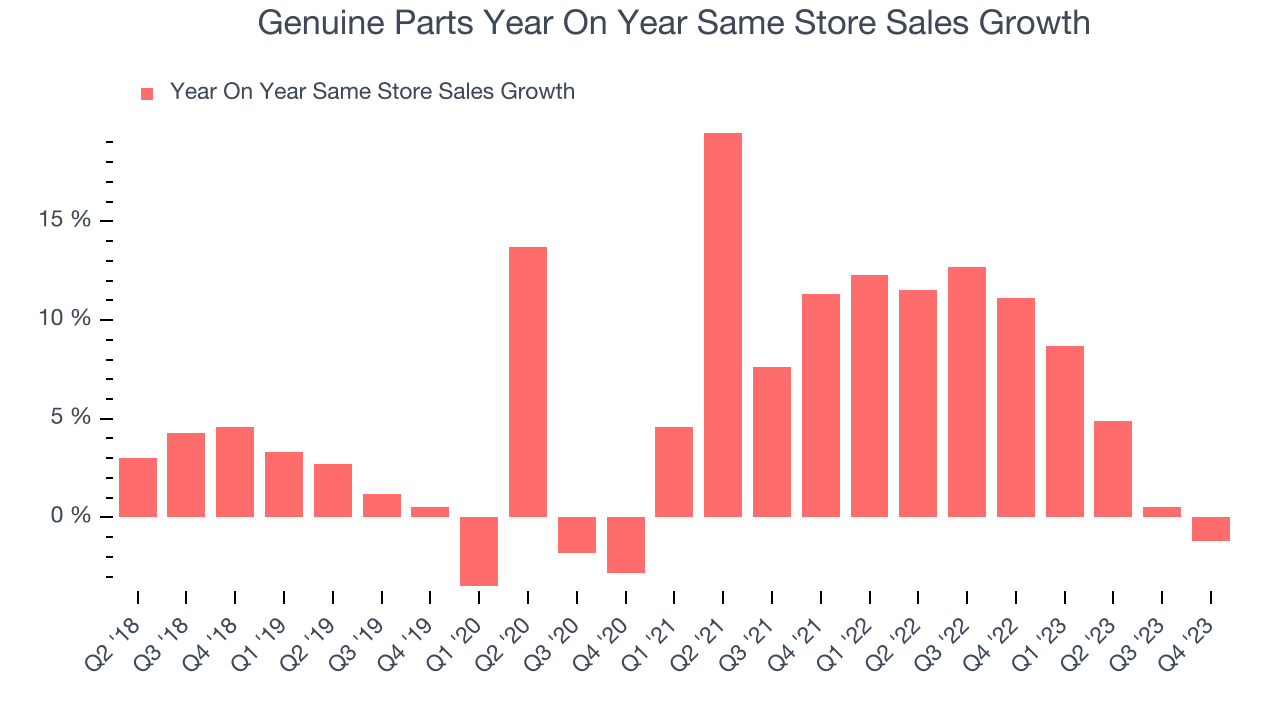

- Same-Store Sales were down 1.2% year on year

- Store Locations: 10,700 at quarter end, increasing by 700 over the last 12 months

- Market Capitalization: $20.19 billion

"We are pleased to report that GPC delivered on our financial commitments in 2023 and finished the year with a solid fourth quarter. We reported mid-single-digit total sales growth and our third consecutive year of double-digit earnings growth," said Paul Donahue, Chairman and Chief Executive Officer.

Largely targeting the professional customer, Genuine Parts (NYSE:GPC) sells auto and industrial parts such as batteries, belts, bearings, and machine fluids.

Auto Parts Retailer

Cars are complex machines that need maintenance and occasional repairs, and auto parts retailers cater to the professional mechanic as well as the do-it-yourself (DIY) fixer. Work on cars may entail replacing fluids, parts, or accessories, and these stores have the parts and accessories or these jobs. While e-commerce competition presents a risk, these stores have a leg up due to the combination of broad and deep selection as well as expertise provided by sales associates. Another change on the horizon could be the increasing penetration of electric vehicles.

Sales Growth

Genuine Parts is one of the larger companies in the consumer retail industry and benefits from economies of scale, enabling it to gain more leverage on fixed costs and offer consumers lower prices.

As you can see below, the company's annualized revenue growth rate of 7.1% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was weak despite not opening many new stores, implying that growth was driven by higher sales at existing, established stores.

This quarter, Genuine Parts's revenue grew 1.1% year on year to $5.59 billion, falling short of Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 3.9% over the next 12 months, an acceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Same-Store Sales

Same-store sales growth is an important metric that tracks demand for a retailer's established brick-and-mortar stores and e-commerce platform.

Genuine Parts's demand within its existing stores has generally risen over the last two years but lagged behind the broader consumer retail sector. On average, the company's same-store sales have grown by 7.6% year on year. Given its flat store count over the same period, this performance stems from increased foot traffic at existing stores or higher e-commerce sales as the company shifts demand from in-store to online.

In the latest quarter, Genuine Parts's same-store sales fell 1.2% year on year. This decline was a reversal from the 11.1% year-on-year increase it posted 12 months ago. We'll be keeping a close eye on the company to see if this turns into a longer-term trend.

Key Takeaways from Genuine Parts's Q4 Results

It was good to see Genuine Parts beat analysts' gross margin and EPS expectations this quarter. That stood out as a positive in these results. On the other hand, its revenue unfortunately missed analysts' expectations as its same-store sales shrunk. The company would have posted revenue declines it if weren't for the 2% boost it received from its acquisitions. Lastly, GPC's full-year 2024 revenue and earnings guidance fell short of Wall Street's estimates. Overall, this was a mediocre quarter for Genuine Parts. The company is down 4.4% on the results and currently trades at $137.78 per share.

So should you invest in Genuine Parts right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.