Gorman-Rupp (NYSE:GRC) manufactures and sells pumps globally. fell short of the market’s revenue expectations in Q3 CY2024, with sales flat year on year at $168.2 million. Its GAAP profit of $0.49 per share was also 5.8% below analysts’ consensus estimates.

Is now the time to buy Gorman-Rupp? Find out by accessing our full research report, it’s free.

Gorman-Rupp (GRC) Q3 CY2024 Highlights:

- Revenue: $168.2 million vs analyst estimates of $172.5 million (2.5% miss)

- EPS: $0.49 vs analyst expectations of $0.52 (5.8% miss)

- EBITDA: $32 million vs analyst estimates of $33.42 million (4.3% miss)

- Gross Margin (GAAP): 31.3%, up from 28.7% in the same quarter last year

- Operating Margin: 14.2%, up from 12.9% in the same quarter last year

- EBITDA Margin: 19%, up from 15.3% in the same quarter last year

- Backlog: $207.8 million at quarter end

- Market Capitalization: $976.5 million

Company Overview

Powering fluid dynamics since 1934, Gorman-Rupp (NYSE:GRC) has evolved from its Ohio origins into a global manufacturer and seller of pumps and pump systems.

Gas and Liquid Handling

Gas and liquid handling companies possess the technical know-how and specialized equipment to handle valuable (and sometimes dangerous) substances. Lately, water conservation and carbon capture–which requires hydrogen and other gasses as well as specialized infrastructure–have been trending up, creating new demand for products such as filters, pumps, and valves. On the other hand, gas and liquid handling companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

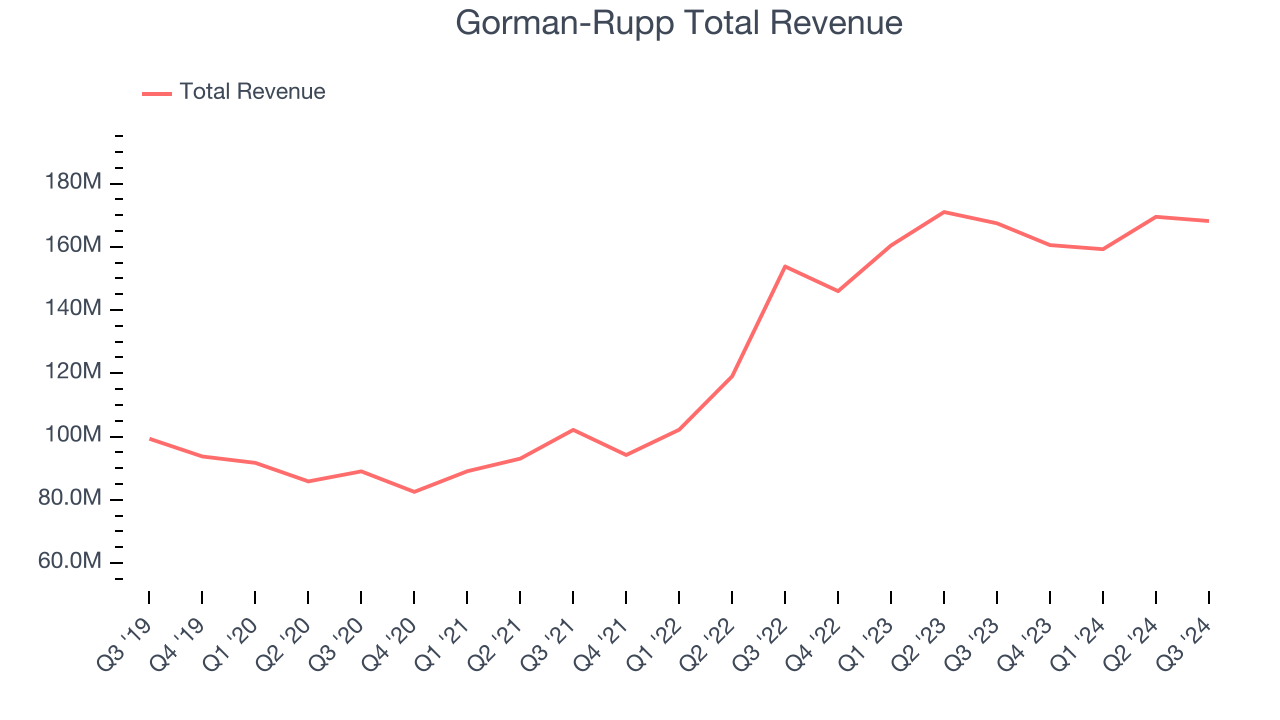

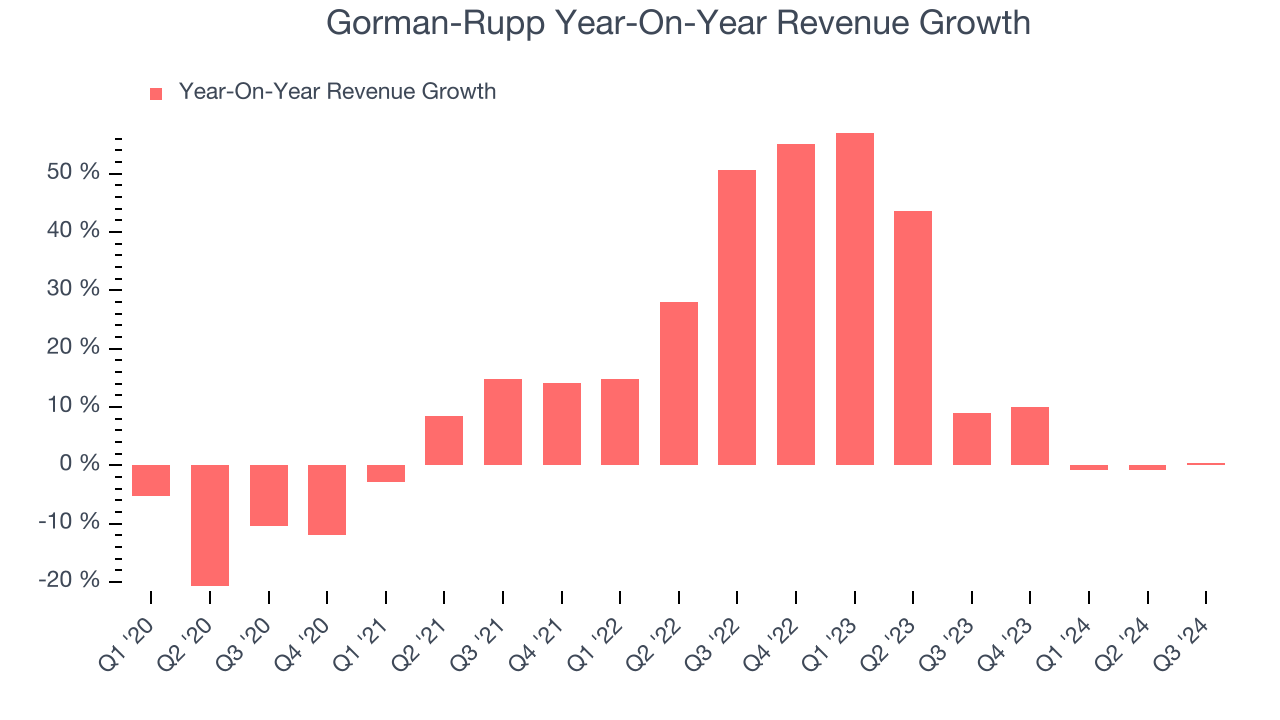

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Gorman-Rupp grew its sales at a solid 10.3% compounded annual growth rate. This is encouraging because it shows Gorman-Rupp was more successful in expanding than most industrials companies.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Gorman-Rupp’s annualized revenue growth of 18.4% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Gorman-Rupp’s $168.2 million of revenue was flat year on year, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.3% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates the market thinks its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

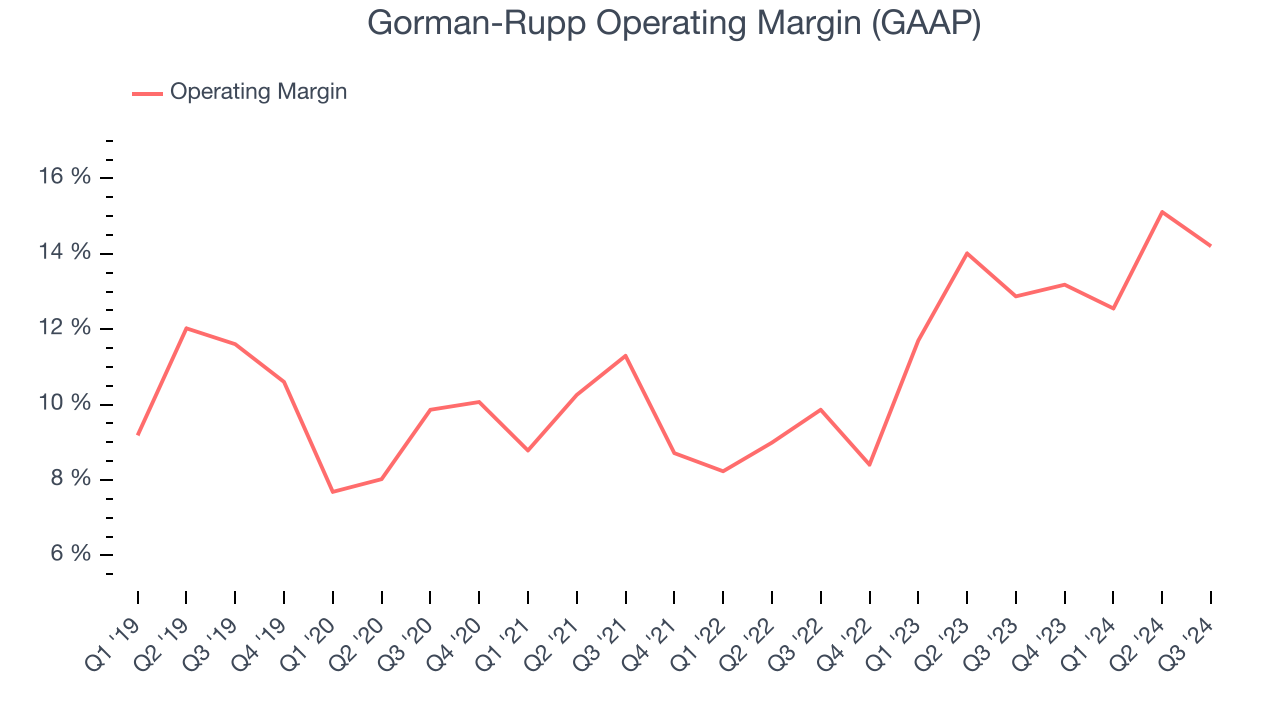

Operating Margin

Gorman-Rupp has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 11.2%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Gorman-Rupp’s annual operating margin rose by 4.7 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q3, Gorman-Rupp generated an operating profit margin of 14.2%, up 1.3 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

Earnings Per Share

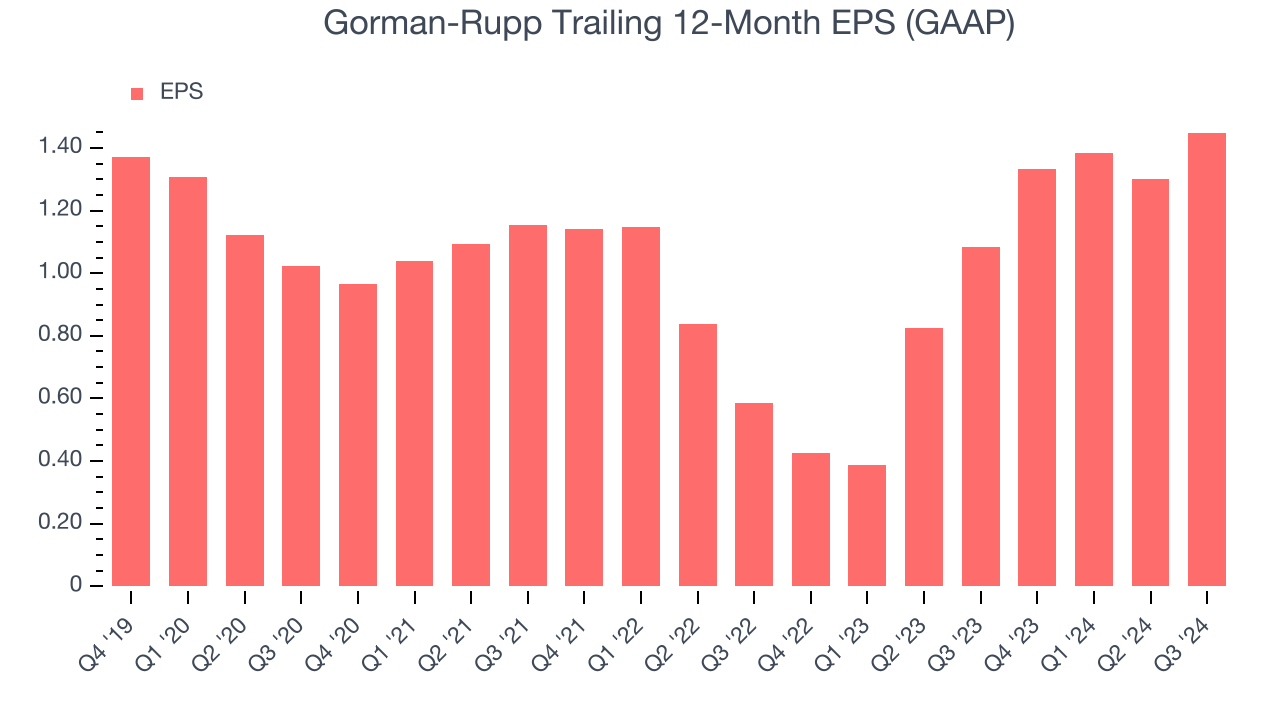

Analyzing revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Gorman-Rupp’s EPS grew at a weak 1.1% compounded annual growth rate over the last five years, lower than its 10.3% annualized revenue growth. However, its operating margin actually expanded during this timeframe, telling us that non-fundamental factors affected its ultimate earnings.

Like with revenue, we analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business.

Gorman-Rupp’s two-year annual EPS growth of 57.2% was fantastic and topped its 18.4% two-year revenue growth.In Q3, Gorman-Rupp reported EPS at $0.49, up from $0.34 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Gorman-Rupp’s full-year EPS of $1.45 to grow by 34.6%.

Key Takeaways from Gorman-Rupp’s Q3 Results

We struggled to find many strong positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 1.9% to $36.50 immediately after reporting.

The latest quarter from Gorman-Rupp’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.