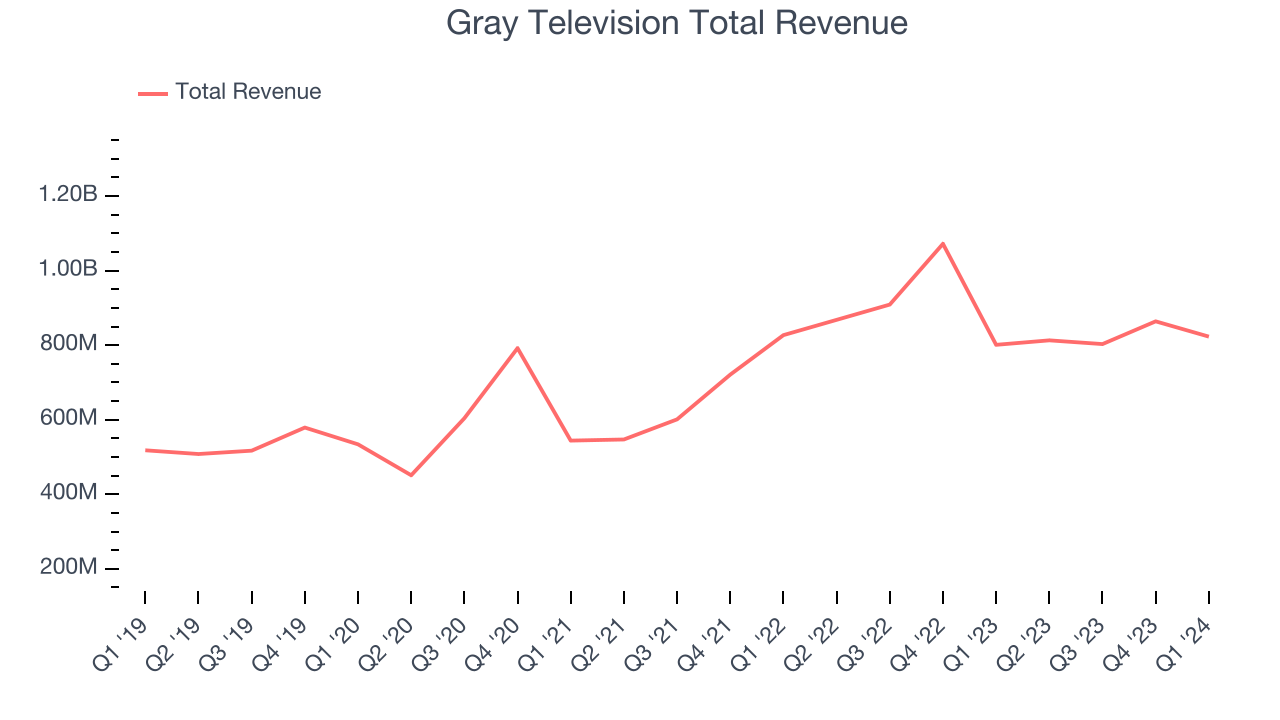

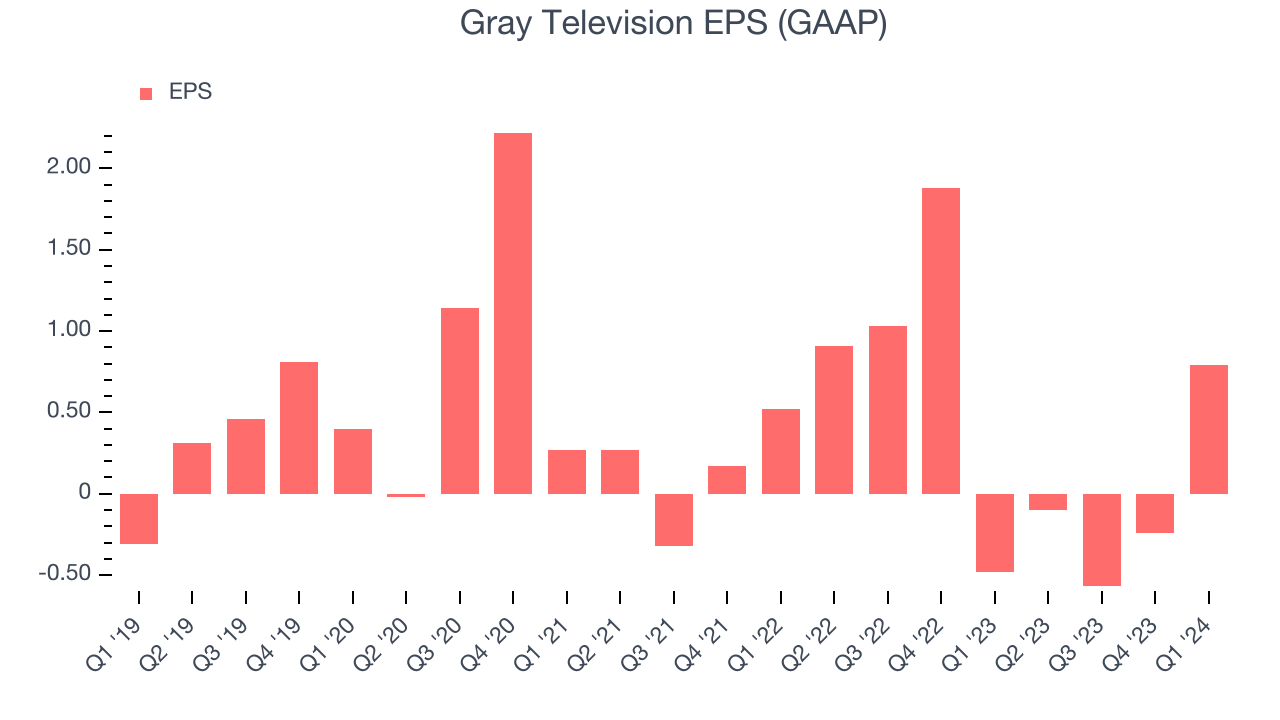

Local television broadcasting and media company Gray Television (NYSE:GTN) reported results in line with analysts' expectations in Q1 CY2024, with revenue up 2.7% year on year to $823 million. On the other hand, next quarter's revenue guidance of $837 million was less impressive, coming in 1.9% below analysts' estimates. It made a GAAP profit of $0.79 per share, improving from its loss of $0.48 per share in the same quarter last year.

Gray Television (GTN) Q1 CY2024 Highlights:

- Revenue: $823 million vs analyst estimates of $825 million (small miss)

- EPS: $0.79 vs analyst estimates of $0.26 (204% beat)

- Revenue Guidance for Q2 CY2024 is $837 million at the midpoint, below analyst estimates of $853.4 million

- Gross Margin (GAAP): 26.6%, up from 23.3% in the same quarter last year

- Free Cash Flow of $87 million, up 102% from the previous quarter

- Market Capitalization: $676.2 million

Specializing in local media coverage, Gray Television (NYSE:GTN) is a broadcast company supplying digital media to various markets in the United States.

Gray Television was established to provide localized television broadcasting to underserved markets. From its inception, the company has recognized the need for communities to have access to news, information, and entertainment that reflect their specific interests and needs.

The company's offerings include local news, weather, sports, and entertainment programming across its network of stations. This focus on local content fills a critical gap in a media landscape often dominated by national narratives, ensuring communities receive relevant, region-specific information.

The company generates revenue through advertising and digital media affiliate fees, where business partners pay Gray Television to access its content.

Broadcasting

Broadcasting companies have been facing secular headwinds in the form of consumers abandoning traditional television and radio in favor of streaming services. As a result, many broadcasting companies have evolved by forming distribution agreements with major streaming platforms so they can get in on part of the action, but will these subscription revenues be as high quality and high margin as their legacy revenues? Only time will tell which of these broadcasters will survive the sea changes of technological advancement and fragmenting consumer attention.

Competitors in the local television broadcasting industry include Nexstar Media (NASDAQ:NXST), Sinclair (NASDAQ: SBGI), and TEGNA (NYSE: TGNA).Sales Growth

A company’s long-term performance can give signals about its business quality. Any business can put up a good quarter or two, but many enduring ones muster years of growth. Gray Television's annualized revenue growth rate of 19.2% over the last five years was solid for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Gray Television's recent history shows its momentum has slowed as its annualized revenue growth of 10.7% over the last two years is below its five-year trend.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Gray Television's recent history shows its momentum has slowed as its annualized revenue growth of 10.7% over the last two years is below its five-year trend.

We can better understand the company's revenue dynamics by analyzing its most important segments, Retransmission and Advertising, which are 46.3% and 45.2% of revenue. Over the last two years, Gray Television's Retransmission revenue (affiliate and licensing fees) averaged 15.3% year-on-year growth while its Advertising revenue (marketing services) averaged 9.5% growth.

This quarter, Gray Television grew its revenue by 2.7% year on year, and its $823 million of revenue was in line with Wall Street's estimates. The company is guiding for revenue to rise 3% year on year to $837 million next quarter, improving from the 6.3% year-on-year decrease it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 16.3% over the next 12 months, an acceleration from this quarter.

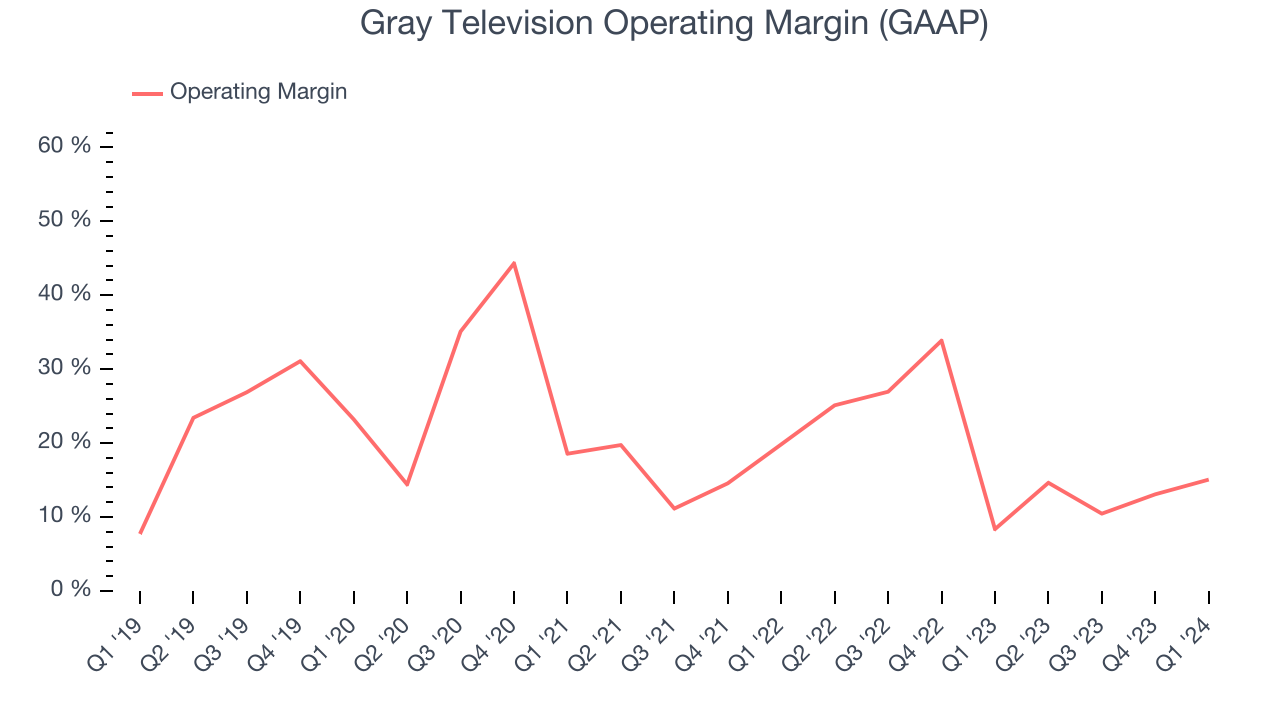

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Gray Television has been a well-managed company over the last eight quarters. It's demonstrated it can be one of the more profitable businesses in the consumer discretionary sector, boasting an average operating margin of 19.2%.

This quarter, Gray Television generated an operating profit margin of 15.1%, up 6.7 percentage points year on year.

Over the next 12 months, Wall Street expects Gray Television to become more profitable. Analysts are expecting the company’s LTM operating margin of 13.3% to rise to 23.6%.EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last five years, Gray Television's EPS dropped 107%, translating into 15.6% annualized declines. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends or consumer preferences. Consumer discretionary companies are particularly exposed to this, leaving a low margin of safety around the company (making the stock susceptible to large downward swings).

In Q1, Gray Television reported EPS at $0.79, up from negative $0.48 in the same quarter last year. This print easily cleared analysts' estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts are projecting Gray Television's LTM EPS of negative $0.12 to flip to positive $3.32.

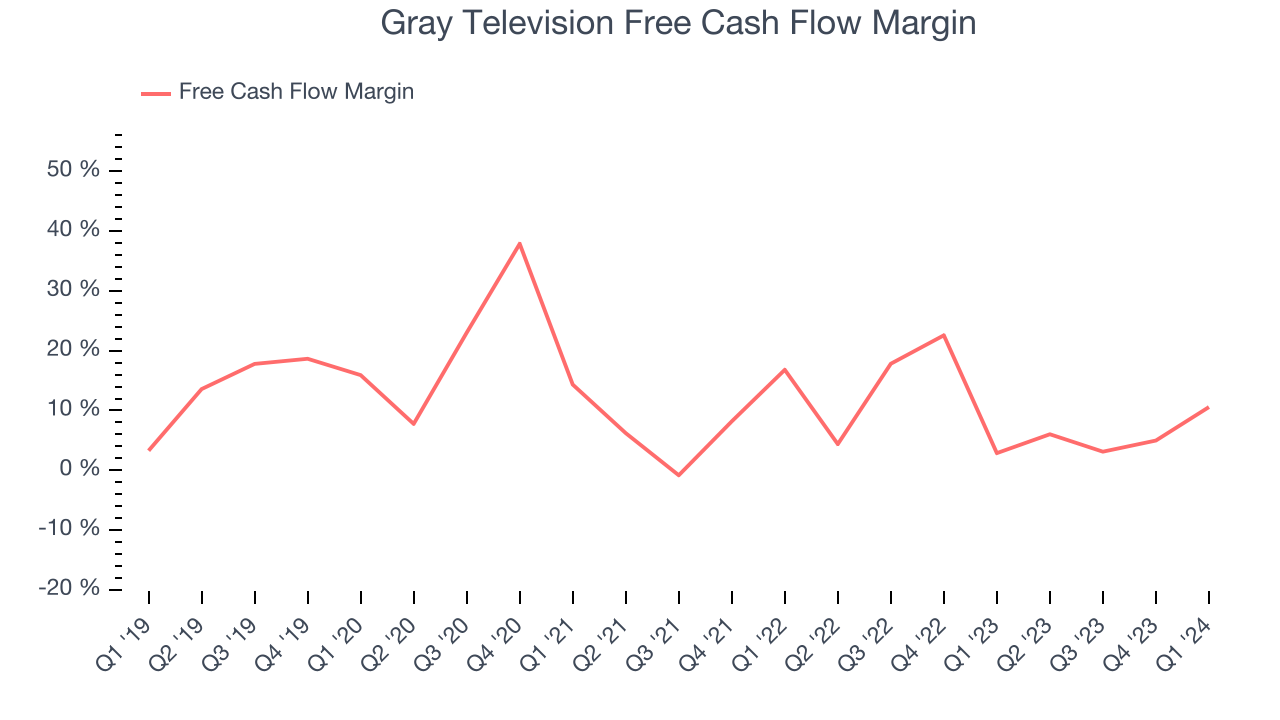

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, Gray Television has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 9.6%, subpar for a consumer discretionary business.

Gray Television's free cash flow came in at $87 million in Q1, equivalent to a 10.6% margin and up 278% year on year. Over the next year, analysts predict Gray Television's cash profitability will improve. Their consensus estimates imply its LTM free cash flow margin of 6.2% will increase to 12.9%.

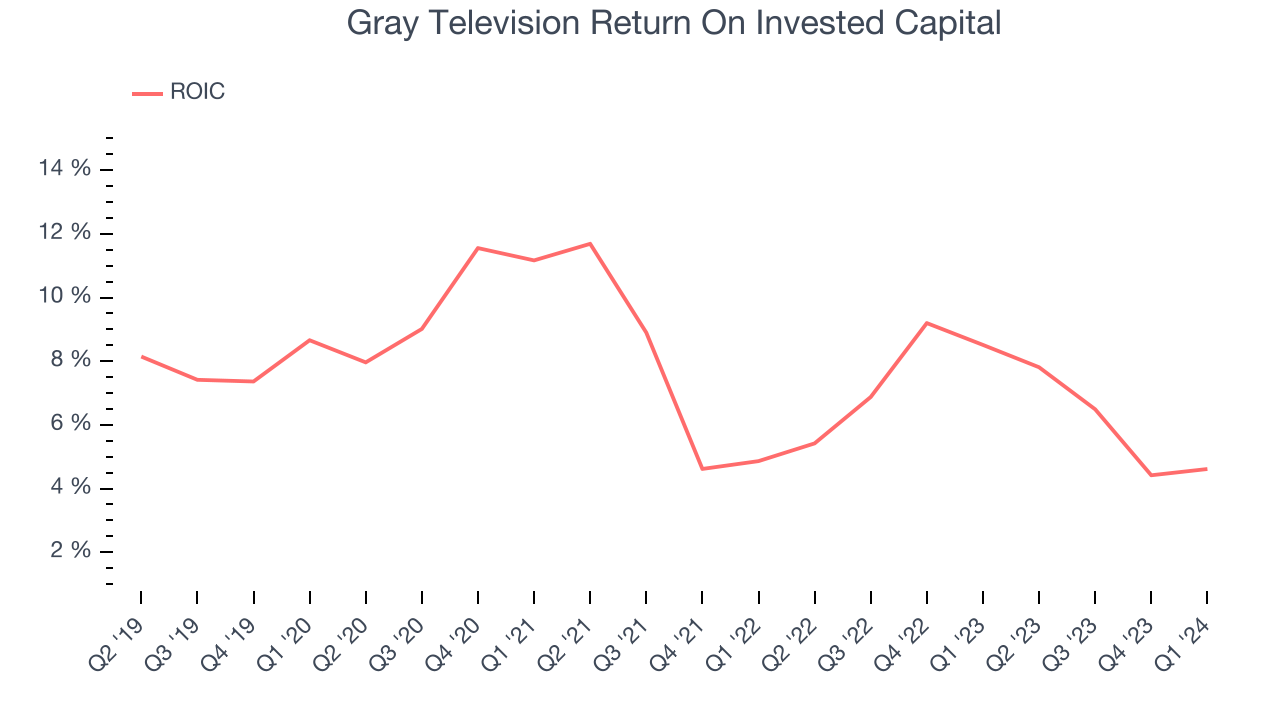

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Gray Television's five-year average return on invested capital was 7.6%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Gray Television's ROIC averaged 3.4 percentage point decreases over the last few years. Paired with its already low returns, these declines suggest the company's profitable business opportunities are few and far between.

Key Takeaways from Gray Television's Q1 Results

We were impressed by how significantly Gray Television blew past analysts' EPS expectations this quarter. On the other hand, its operating margin missed and its revenue guidance for next quarter came in slightly below Wall Street's estimates. Zooming out, we think this was still a decent, albeit mixed, quarter, showing that the company is staying on track. The stock is up 2.9% after reporting and currently trades at $6.85 per share.

Is Now The Time?

Gray Television may have had a favorable quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

Gray Television isn't a bad business, but it probably wouldn't be one of our picks. Although its revenue growth has been good over the last five years, its declining EPS over the last five years makes it hard to trust. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its relatively low ROIC suggests it has historically struggled to find compelling business opportunities.

Gray Television's price-to-earnings ratio based on the next 12 months is 2.0x. In the end, beauty is in the eye of the beholder. While Gray Television wouldn't be our first pick, if you like the business, the shares are trading at a pretty interesting price right now.

Wall Street analysts covering the company had a one-year price target of $10.42 per share right before these results (compared to the current share price of $6.85).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.