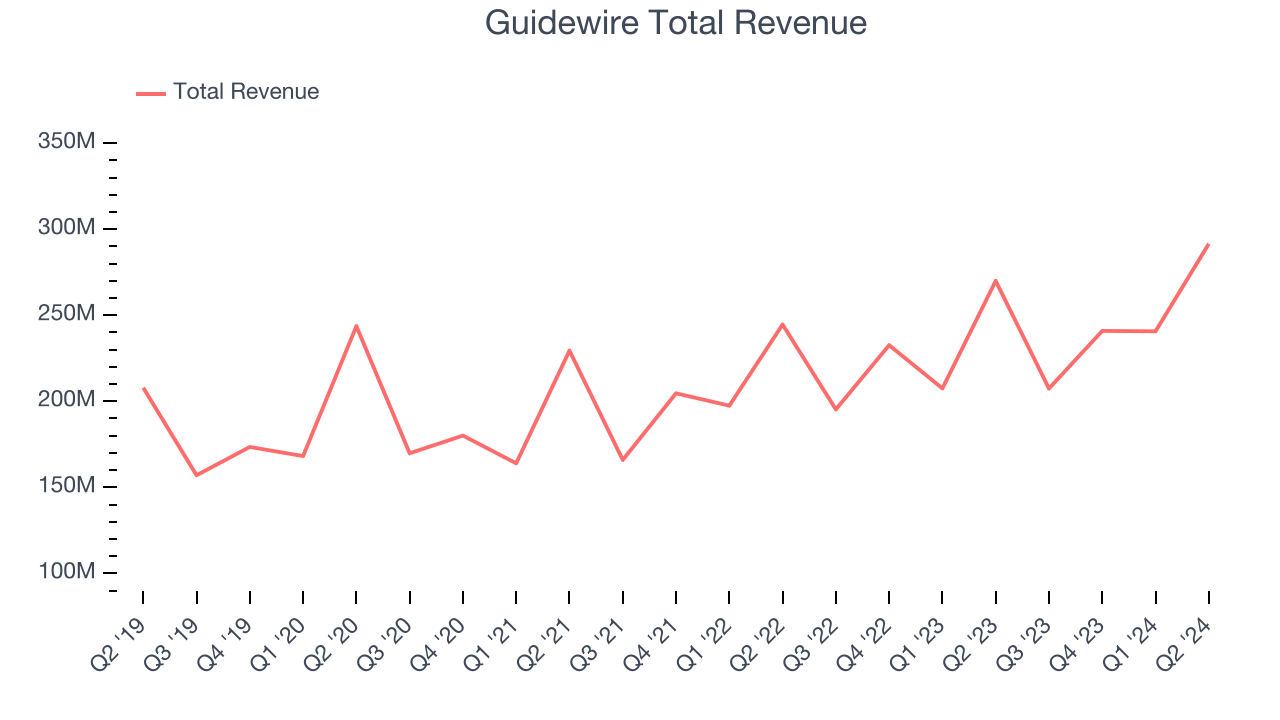

Insurance industry-focused software maker Guidewire (NYSE:GWRE) announced better-than-expected results in Q2 CY2024, with revenue up 8% year on year to $291.5 million. Guidance for next quarter’s revenue was also optimistic at $254 million at the midpoint, 7.5% above analysts’ estimates. It made a non-GAAP profit of $0.62 per share, down from its profit of $0.73 per share in the same quarter last year.

Is now the time to buy Guidewire? Find out by accessing our full research report, it’s free.

Guidewire (GWRE) Q2 CY2024 Highlights:

- Revenue: $291.5 million vs analyst estimates of $283.9 million (2.7% beat)

- Adjusted Operating Income: $48.97 million vs analyst estimates of $49.06 million (small miss)

- EPS (non-GAAP): $0.62 vs analyst estimates of $0.54 (14% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $1.14 billion at the midpoint, beating analyst estimates by 4.5% and implying 16.5% growth (vs 8.4% in FY2024)

- Gross Margin (GAAP): 64%, up from 60.6% in the same quarter last year

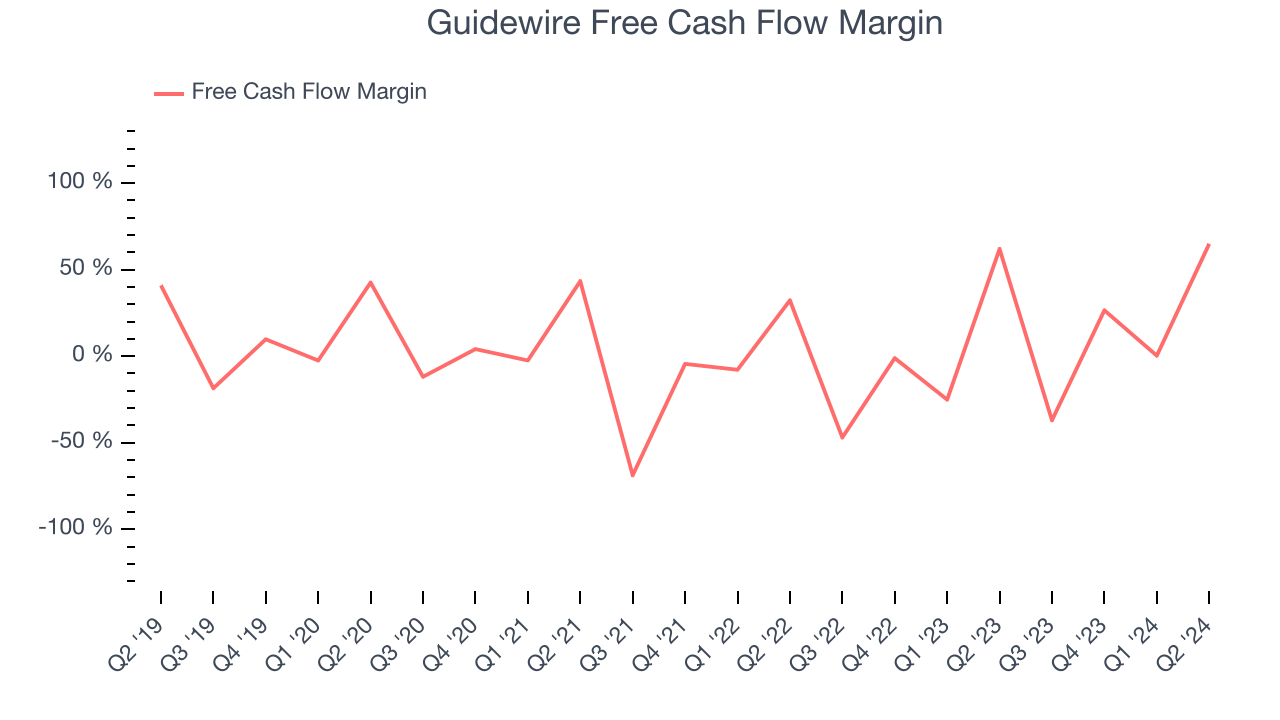

- Free Cash Flow Margin: 65%, up from 0.3% in the previous quarter

- Annual Recurring Revenue: $872 million at quarter end, up 14.3% year on year

- Billings: $392.1 million at quarter end, up 17.4% year on year

- Market Capitalization: $12.16 billion

“We finished the year with record fourth quarter sales activity and fully ramped ARR growth of 19%,” said Mike Rosenbaum, chief executive officer, Guidewire.

Founded by two individuals involved in the development of leading procurement software Ariba, Guidewire (NYSE:GWRE) offers insurance companies a software-as-a-service platform to help sell their products and manage their workflows.

Vertical Software

Software is eating the world, and while a large number of solutions such as project management or video conferencing software can be useful to a wide array of industries, some have very specific needs. As a result, vertical software, which addresses industry-specific workflows, is growing and fueled by the pressures to improve productivity, whether it be for a life sciences, education, or banking company.

Sales Growth

As you can see below, Guidewire’s 9.7% annualized revenue growth over the last three years has been weak, and its sales came in at $291.5 million this quarter.

Guidewire’s quarterly revenue was only up 8% year on year, which might disappoint some shareholders. However, its revenue increased $50.84 million quarter on quarter, a strong improvement from the $219,000 decrease in Q1 CY2024. This is a sign of acceleration of growth and very nice to see indeed.

Next quarter’s guidance suggests that Guidewire is expecting revenue to grow 22.5% year on year to $254 million, improving on the 6.2% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $1.14 billion at the midpoint, growing 16.5% year on year compared to the 8.3% increase in FY2024.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Guidewire has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 18.1% over the last year, quite impressive for a software business.

Guidewire’s free cash flow clocked in at $189.3 million in Q2, equivalent to a 65% margin. This quarter’s result was good as its margin was 3 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends trump fluctuations.

Over the next year, analysts predict Guidewire’s cash conversion will slightly fall. Their consensus estimates imply its free cash flow margin of 18.1% for the last 12 months will decrease to 16.1%.

Key Takeaways from Guidewire’s Q2 Results

We were impressed by how strongly Guidewire blew past analysts’ billings and EPS expectations this quarter. We were also glad its full-year revenue guidance topped Wall Street's estimates. Zooming out, we think this was a solid quarter. The stock traded up 6.4% to $152.98 immediately after reporting.

Guidewire may have had a good quarter, but does that mean you should invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.