Health and wellness products company Herbalife (NYSE:HLF) reported results in line with analysts' expectations in Q1 CY2024, with revenue flat year on year at $1.26 billion. It made a non-GAAP profit of $0.49 per share, down from its profit of $0.54 per share in the same quarter last year.

Herbalife (HLF) Q1 CY2024 Highlights:

- Revenue: $1.26 billion vs analyst estimates of $1.27 billion (small miss)

- EPS (non-GAAP): $0.49 vs analyst estimates of $0.37 (34.2% beat)

- Free Cash Flow was -$19.1 million, down from $60.8 million in the previous quarter

- Organic Revenue was up 2.4% year on year

- Sales Volumes were down 3.6% year on year

- Market Capitalization: $863.2 million

With the first products sold out of the trunk of the founder’s car, Herbalife (NYSE:HLF) today offers a portfolio of shakes, supplements, personal care products, and weight management programs to help customers reach their nutritional and fitness goals.

Specifically, the company was founded in 1980 by Mark Hughes, and the first Herbalife product was a protein shake mix called the "Formula 1 Nutritional Shake Mix”. It was designed to serve as a meal replacement for individuals looking to manage their weight.

Today, Herbalife still offers meal replacement shakes but also sells multivitamins, protein supplements, aloe drinks for gut health, and collagen drink mixes for skin and hair health, among others. The company continues to expand its product portfolio organically with health, wellness, and fitness as the unifying theme.

The company’s go-to-market is unique in that it is a multi-level marketing model. In essence, the products are sold through its network of customers who sign up to sell the product. They often operate from their homes, through dedicated Herbalife nutrition clubs, or via online channels.

This multi-level marketing approach has resulted in controversy, with some claiming the business is nothing more than a pyramid scheme. Pyramid schemes are illegal businesses where returns for older customers or investors are paid using the capital of newer customers and investors, rather than from profit earned. The structure relies heavily on recruitment to sustain itself, rather than actual demand for products.

Personal Care

While personal care products products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

Competitors offering health and wellness supplements and products include Usana Health Sciences (NYSE:USNA), Bellring Brands (NYSE:BRBR), and The Simply Good Foods Company (NASDAQ:SMPL).Sales Growth

Herbalife is larger than most consumer staples companies and benefits from economies of scale, giving it an edge over its smaller competitors.

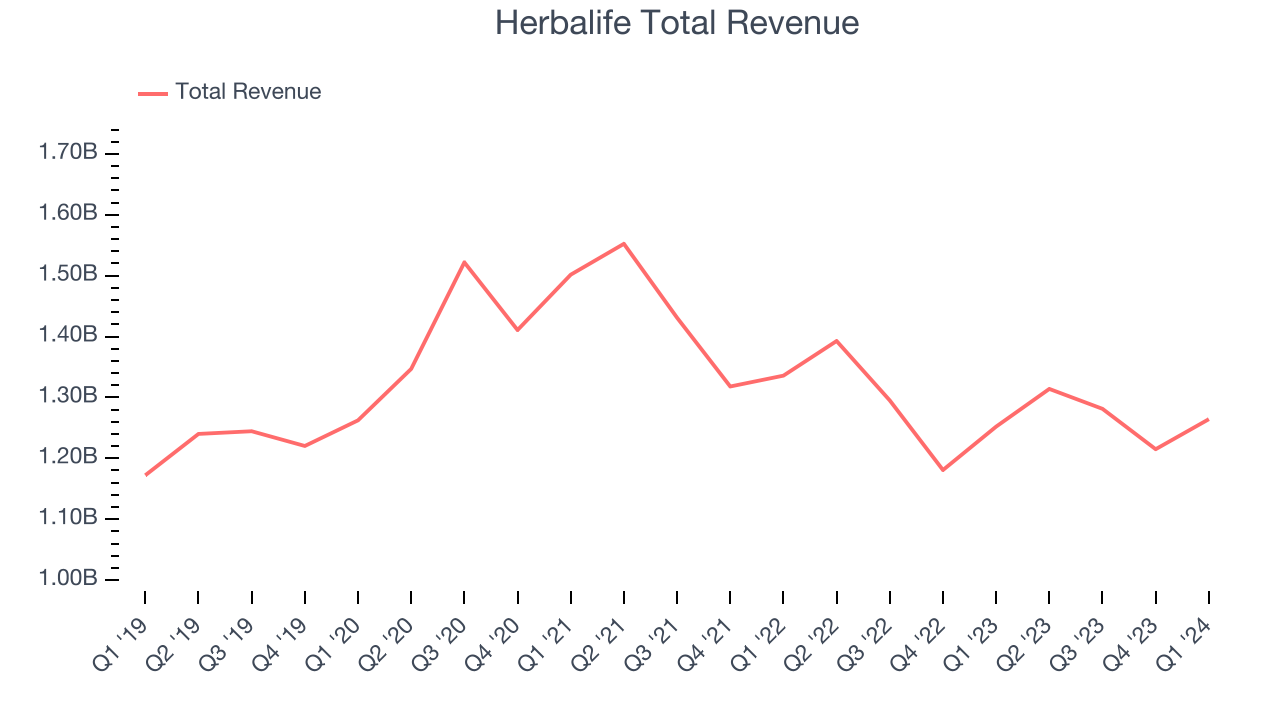

As you can see below, the company's revenue has declined over the last three years, dropping 4.3% annually as consumers bought less of its products.

This quarter, Herbalife's revenue grew 1% year on year to $1.26 billion, falling short of Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 2.1% over the next 12 months, an acceleration from this quarter.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

To analyze whether Herbalife generated its growth (or lack thereof) from changes in price or volume, we can compare its volume growth to its organic revenue growth, which excludes non-fundamental impacts on company financials like mergers and currency fluctuations.

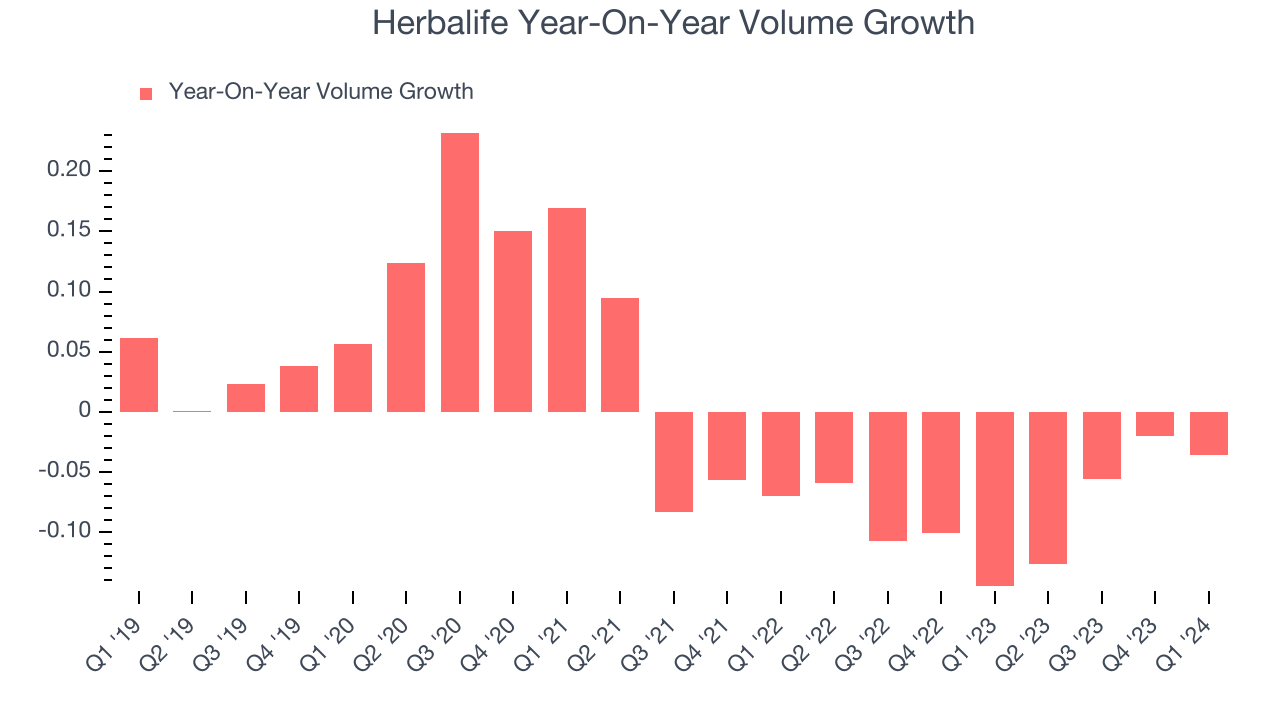

Over the last two years, Herbalife's average quarterly volumes have shrunk by 8.1%. This isn't ideal for a consumer staples company, where demand is typically stable. In the context of its 2.5% average organic sales declines, we can see that most of the company's losses have come from fewer customers purchasing its products.

In Herbalife's Q1 2024, sales volumes dropped 3.6% year on year. This result was a step in the right direction compared to its 14.5% year-on-year decline 12 months ago.

Operating Margin

Operating margin is a key profitability metric for companies because it accounts for all expenses enabling a business to operate smoothly, including marketing and advertising, IT systems, wages, and other administrative costs.

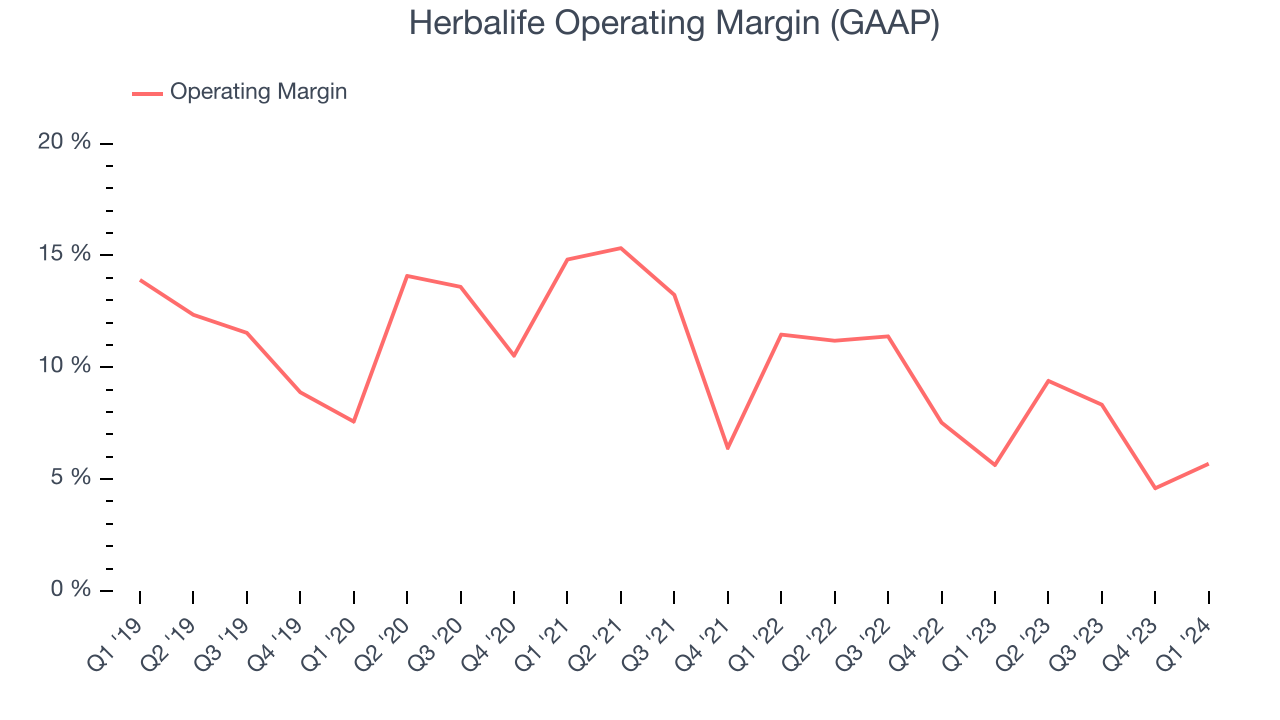

In Q1, Herbalife generated an operating profit margin of 5.7%, in line with the same quarter last year. This indicates the company's costs have been relatively stable.

Zooming out, Herbalife has done a decent job managing its expenses over the last eight quarters. The company has produced an average operating margin of 8%, higher than the broader consumer staples sector. However, Herbalife's margin has declined by 2 percentage points on average over the last year. Although this isn't the end of the world, investors are likely hoping for better results in the future.

Zooming out, Herbalife has done a decent job managing its expenses over the last eight quarters. The company has produced an average operating margin of 8%, higher than the broader consumer staples sector. However, Herbalife's margin has declined by 2 percentage points on average over the last year. Although this isn't the end of the world, investors are likely hoping for better results in the future. EPS

Earnings growth is a critical metric to track, but for long-term shareholders, earnings per share (EPS) is more telling because it accounts for dilution and share repurchases.

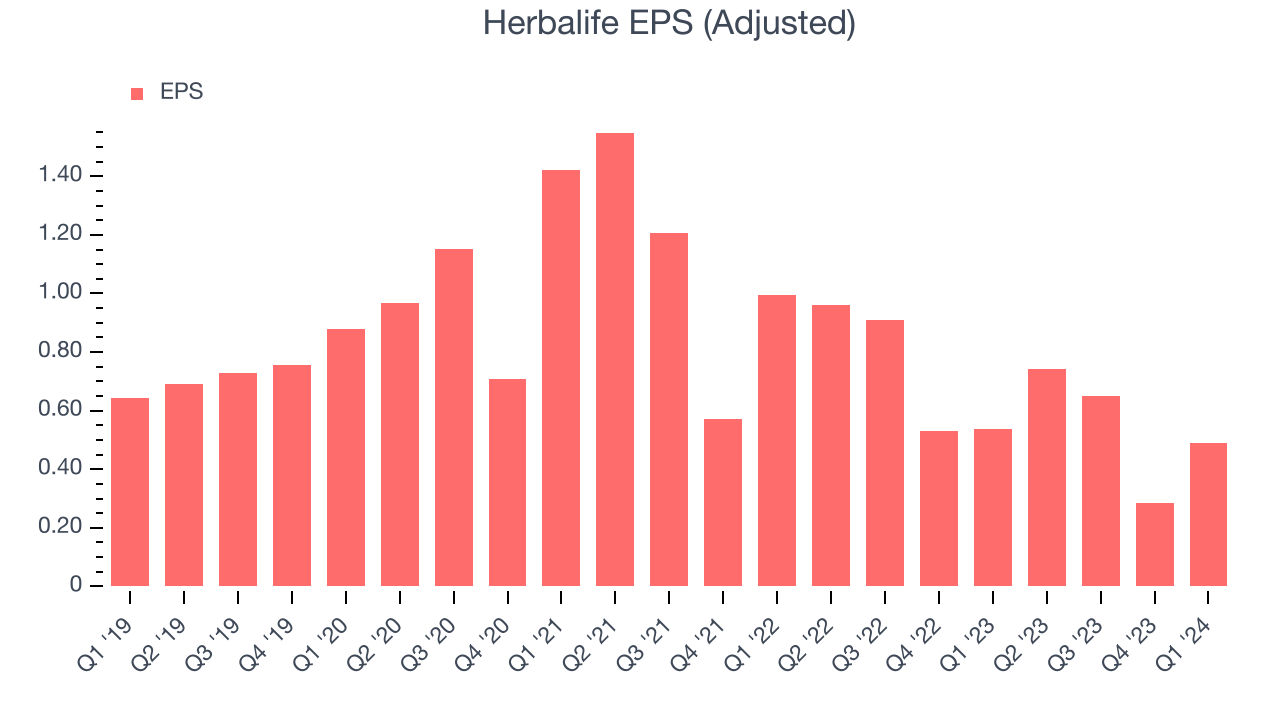

In Q1, Herbalife reported EPS at $0.49, down from $0.54 in the same quarter a year ago. This print beat Wall Street's estimates by 34.2%.

Between FY2021 and FY2024, Herbalife's EPS dropped 49%, translating into 20.1% annualized declines. We tend to steer our readers away from companies with falling EPS, especially in the consumer staples sector, where shrinking earnings could imply changing secular trends or consumer preferences. If there's no earnings growth, it's difficult to build confidence in a business's underlying fundamentals, leaving a low margin of safety around the company's valuation (making the stock susceptible to large downward swings).

Wall Street expects Herbalife to continue performing poorly over the next 12 months, with analysts projecting an average 5.5% year-on-year decline in EPS.

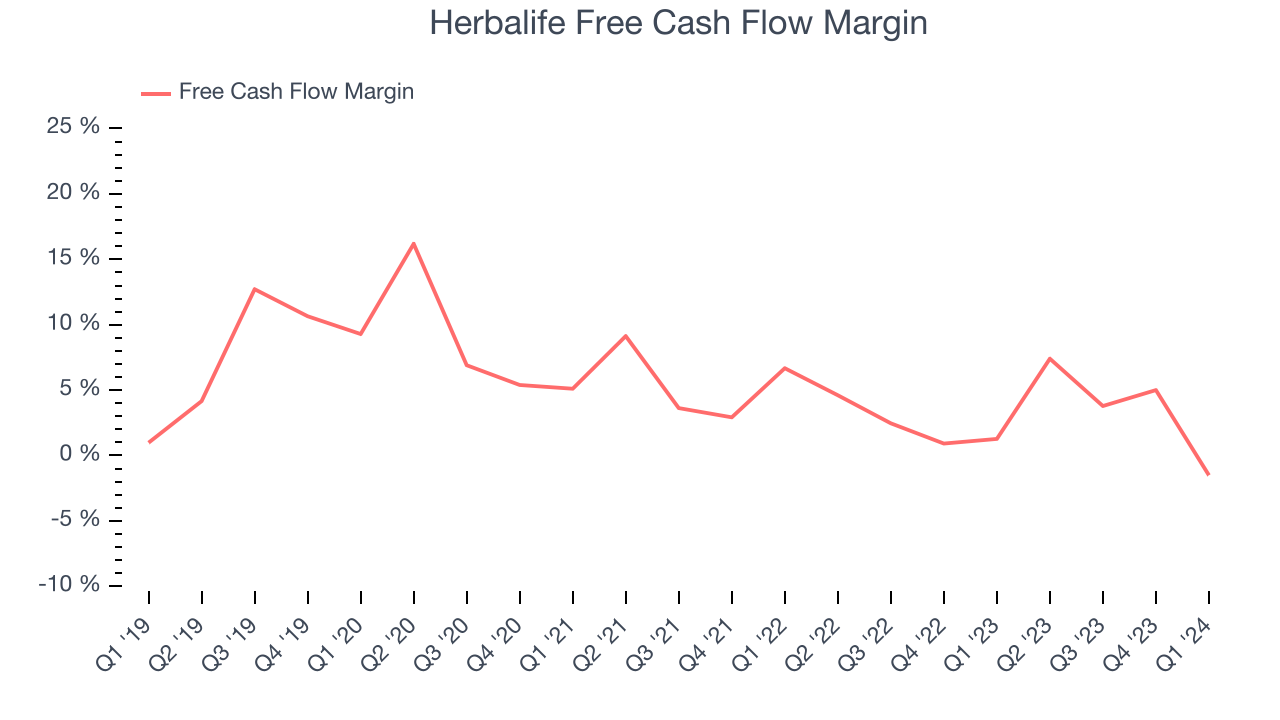

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Herbalife burned through $19.1 million of cash in Q1, representing a negative 1.5% free cash flow margin. The company shifted to cash flow negative from cash flow positive in the same quarter last year, which caught our eye as we'd like consumer staples companies to have more consistent performance.

Over the last eight quarters, Herbalife has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 3%, subpar for a consumer staples business. However, its margin has averaged year-on-year increases of 1.3 percentage points over the last 12 months. Continued momentum should improve its cash flow prospects.

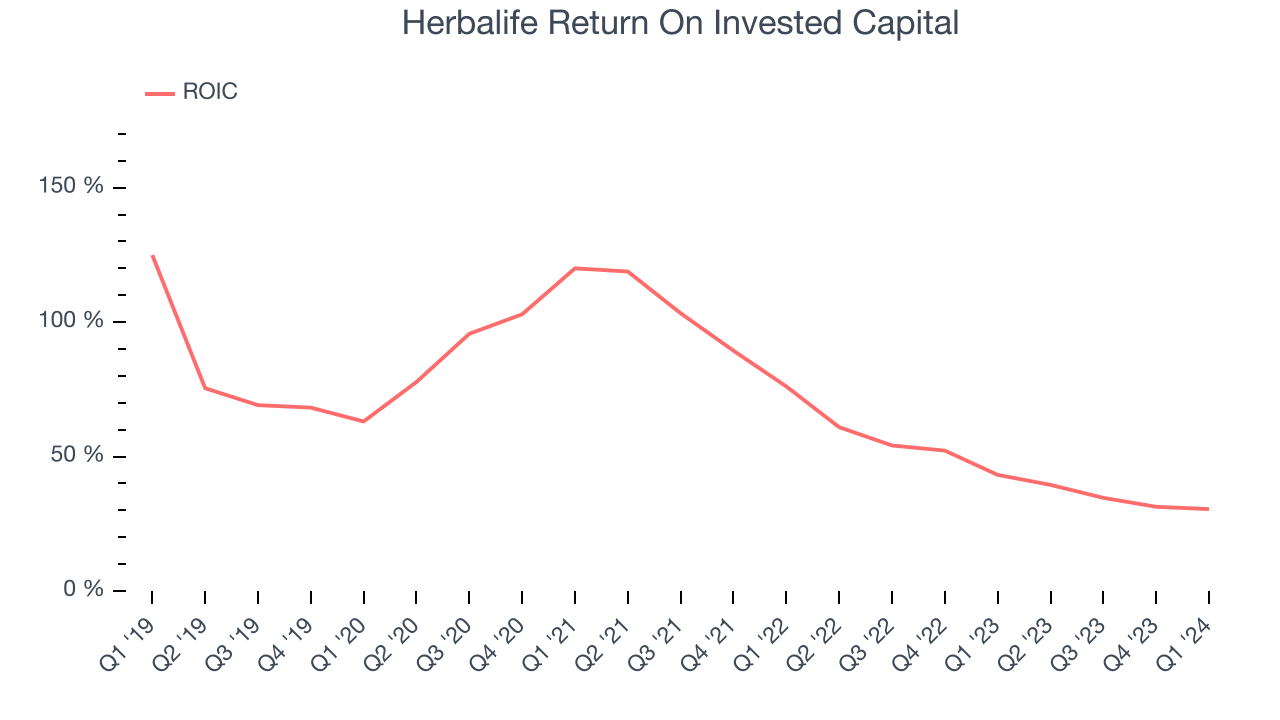

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to how much money the business raised (debt and equity).

Although Herbalife hasn't been the highest-quality company lately because of its poor top-line performance, it historically did a wonderful job investing in profitable business initiatives. Its five-year average ROIC was 53.2%, splendid for a consumer staples business.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Herbalife's ROIC significantly decreased over the last few years. We like what management has done historically but are concerned its ROIC is declining, perhaps a symptom of waning business opportunities to invest profitably.

Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly.

Herbalife reported $398.3 million of cash and $2.41 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $580 million of EBITDA over the last 12 months, we view Herbalife's 3.5x net-debt-to-EBITDA ratio as safe. We also see its $77.1 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from Herbalife's Q1 Results

We were impressed by how significantly Herbalife blew past analysts' EPS expectations this quarter. On the other hand, its organic revenue unfortunately missed analysts' expectations. That didn't matter too much, however, as Herbalife's guidance was the star of the show - the company raised its adjusted EBITDA outlook and lowered its capital expenditure forecast, both of which beat analysts' estimates. It also completed a $1.6 billion refinancing on April 12th. Overall, this quarter's results were solid. The stock is up 10.2% after reporting and currently trades at $9.58 per share.

Is Now The Time?

Herbalife may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Herbalife, we'll be cheering from the sidelines. Its revenue has declined over the last three years, but at least growth is expected to increase in the short term. And while its stellar ROIC suggests it has been a well-run company historically, the downside is its declining EPS over the last three years makes it hard to trust. On top of that, its shrinking sales volumes suggest it'll need to change its strategy to succeed.

Herbalife's price-to-earnings ratio based on the next 12 months is 4.2x. While there are some things to like about Herbalife and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $11.90 per share right before these results (compared to the current share price of $9.58).

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.