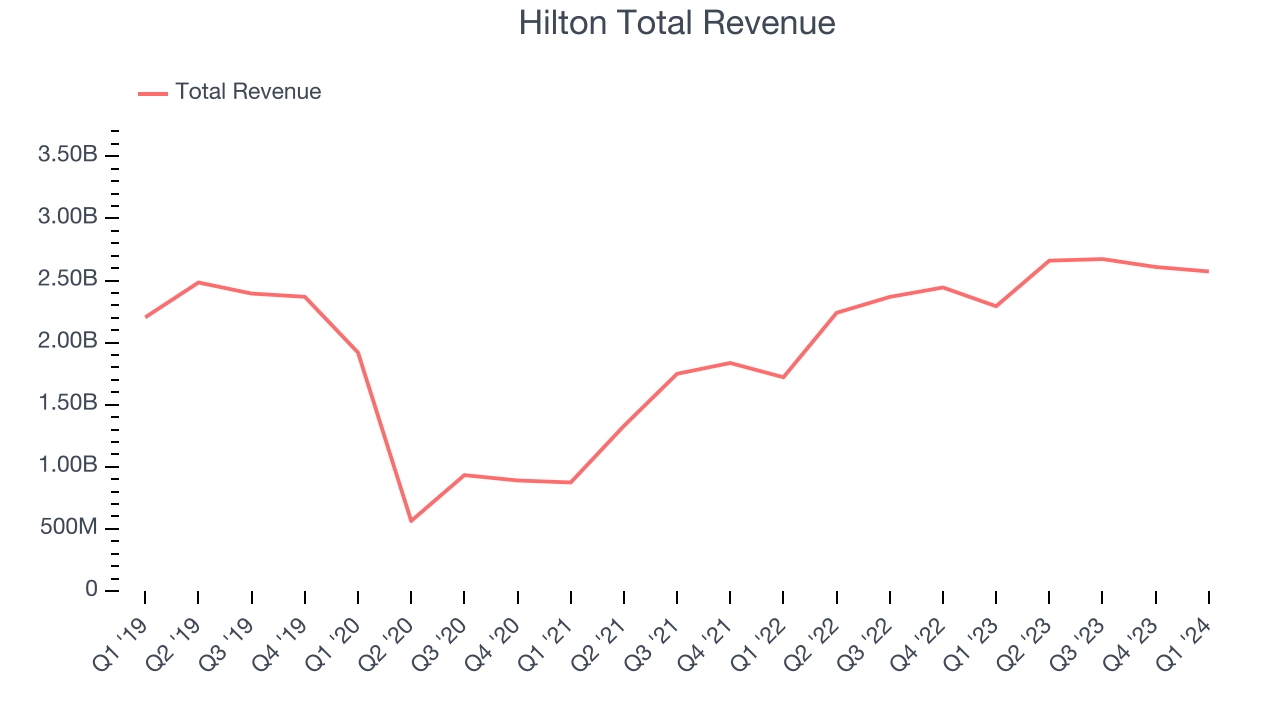

Hotel company Hilton (NYSE:HLT) announced better-than-expected results in Q1 CY2024, with revenue up 12.2% year on year to $2.57 billion. It made a non-GAAP profit of $1.53 per share, improving from its profit of $1.24 per share in the same quarter last year.

Is now the time to buy Hilton? Find out by accessing our full research report, it's free.

Hilton (HLT) Q1 CY2024 Highlights:

- Revenue: $2.57 billion vs analyst estimates of $2.53 billion (1.7% beat)

- EPS (non-GAAP): $1.53 vs analyst estimates of $1.42 (8% beat)

- EPS (non-GAAP) Guidance for Q2 CY2024 is $1.83 at the midpoint, below analyst estimates of $1.88

- Gross Margin (GAAP): 90.4%, up from 89.1% in the same quarter last year

- Free Cash Flow of $330 million, down 22% from the previous quarter

- Market Capitalization: $51.18 billion

Christopher J. Nassetta, President & Chief Executive Officer of Hilton, said, "We are pleased to report a strong first quarter with bottom line results meaningfully exceeding our expectations, further demonstrating the power of our resilient, fee-based business model and strong development story. During the first quarter, system-wide RevPAR increased 2.0 percent as renovations, inclement weather and unfavorable holiday shifts weighed on performance more than anticipated. On the development side, we continued to see great momentum across signings, starts and openings. As a result of our record pipeline and the growth pace we've seen to-date, we expect net unit growth of 6.0 percent to 6.5 percent for the full year, excluding the planned acquisition of the Graduate Hotels brand."

Founded in 1919, Hilton Worldwide (NYSE:HLT) is a global hospitality company with a portfolio of hotel brands.

Hotels, Resorts and Cruise Lines

Hotels, resorts, and cruise line companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted from buying "things" (wasteful) to buying "experiences" (memorable). In addition, the internet has introduced new ways of approaching leisure and lodging such as booking homes and longer-term accommodations. Traditional hotel, resorts, and cruise line companies must innovate to stay relevant in a market rife with innovation.

Sales Growth

A company's long-term performance can indicate its business quality. Any business can enjoy short-lived success, but best-in-class ones sustain growth over many years. Hilton's annualized revenue growth rate of 3.1% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new property or emerging trend. That's why we also follow short-term performance. Hilton's annualized revenue growth of 25.9% over the last two years is above its five-year trend, suggesting some bright spots.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new property or emerging trend. That's why we also follow short-term performance. Hilton's annualized revenue growth of 25.9% over the last two years is above its five-year trend, suggesting some bright spots.

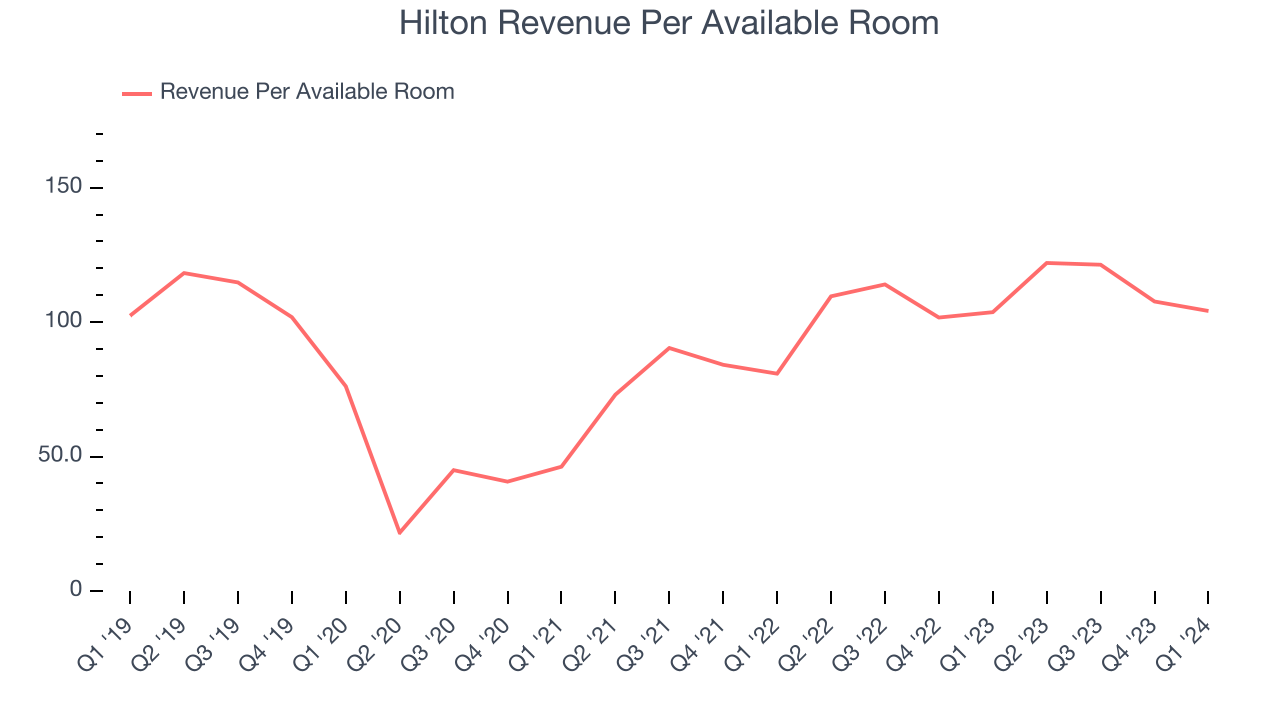

We can dig even further into the company's revenue dynamics by analyzing its revenue per available room, which clocked in at $104.16 this quarter and is a key metric accounting for average daily rates and occupancy levels. Over the last two years, Hilton's revenue per room averaged 18.7% year-on-year growth. Because this number is lower than its revenue growth, we can see its sales from other areas like restaurants, bars, and amenities outperformed its room bookings.

This quarter, Hilton reported robust year-on-year revenue growth of 12.2%, and its $2.57 billion of revenue exceeded Wall Street's estimates by 1.7%. Looking ahead, Wall Street expects sales to grow 9.9% over the next 12 months, a deceleration from this quarter.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, Hilton has shown strong cash profitability, giving it an edge over its competitors and the option to reinvest or return capital to investors while keeping cash on hand for emergencies. The company's free cash flow margin has averaged 18%, quite impressive for a consumer discretionary business.

Hilton's free cash flow came in at $330 million in Q1, equivalent to a 12.8% margin and up 15.4% year on year.

Key Takeaways from Hilton's Q1 Results

It was good to see Hilton beat analysts' revenue and EPS expectations this quarter. Additionally, adjusted EBITDA guidance for the full year 2024 was raised and came in above expectations. On the other hand, its operating margin missed and its full-year earnings guidance fell short of Wall Street's estimates. While not perfect, this was still a solid quarter for Hilton. The stock is up 1.7% after reporting and currently trades at $200.5 per share.

So should you invest in Hilton right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.