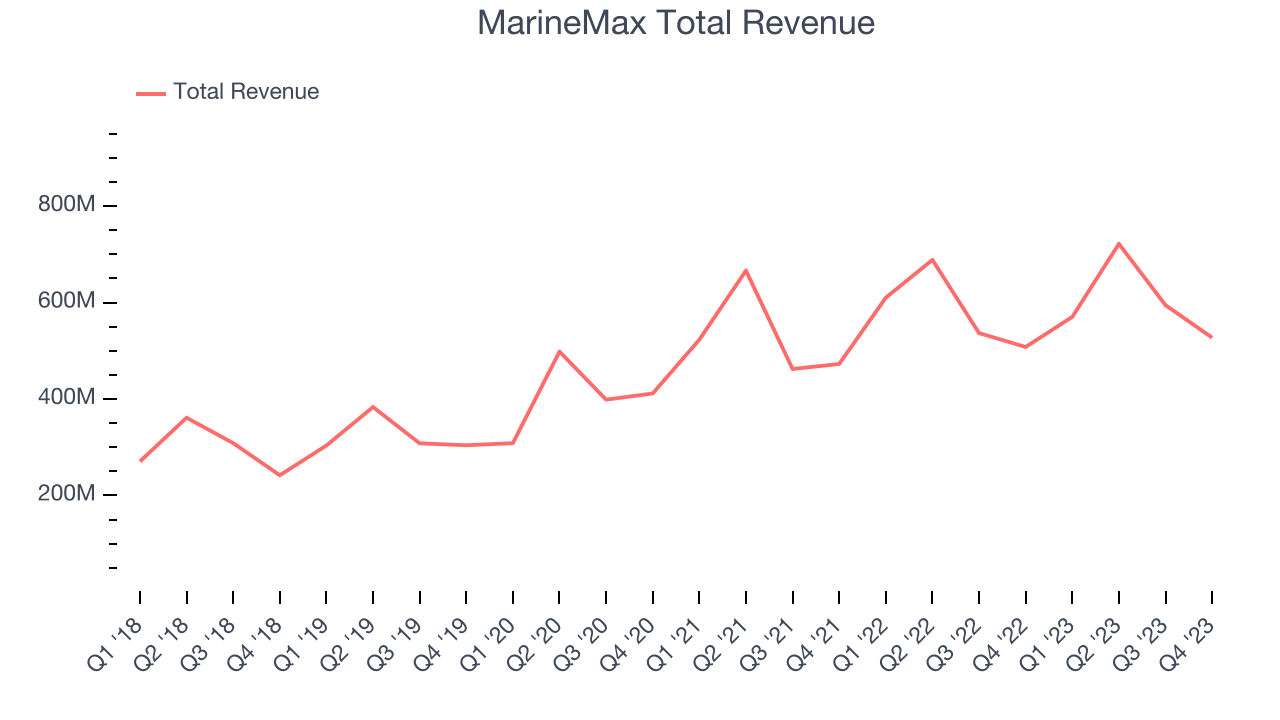

Boat and marine products retailer MarineMax (NYSE:HZO) reported results in line with analysts' expectations in Q1 FY2024, with revenue up 3.8% year on year to $527.3 million. It made a non-GAAP profit of $0.19 per share, down from its profit of $1.24 per share in the same quarter last year.

Is now the time to buy MarineMax? Find out by accessing our full research report, it's free.

MarineMax (HZO) Q1 FY2024 Highlights:

- Market Capitalization: $736.1 million

- Revenue: $527.3 million vs analyst estimates of $528.1 million (small miss)

- EPS (non-GAAP): $0.19 vs analyst estimates of $0.50 (-$0.31 miss)

- Guidance for EPS (non-GAAP): lowered to $3.25 per share at the midpoint, well below Consensus of $4.66 and previous guidance midpoint of $4.75

- Gross Margin (GAAP): 33.3%, down from 36.8% in the same quarter last year

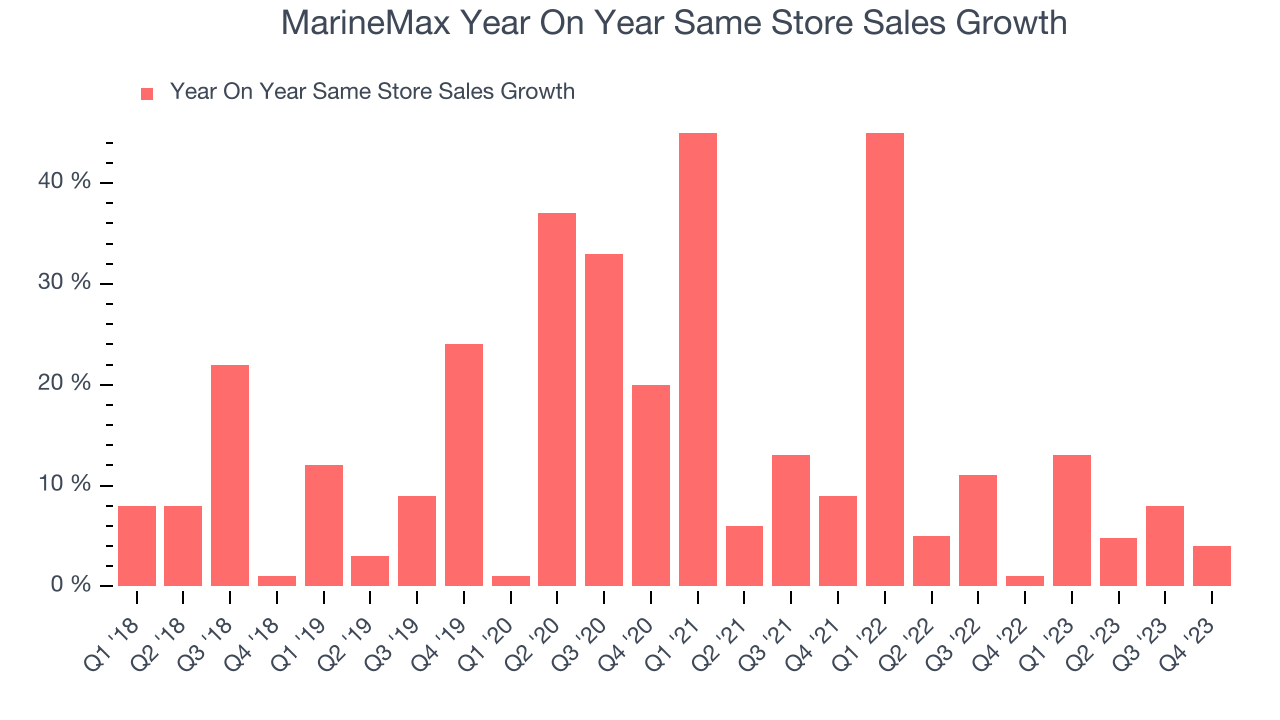

- Same-Store Sales were up 4% year on year

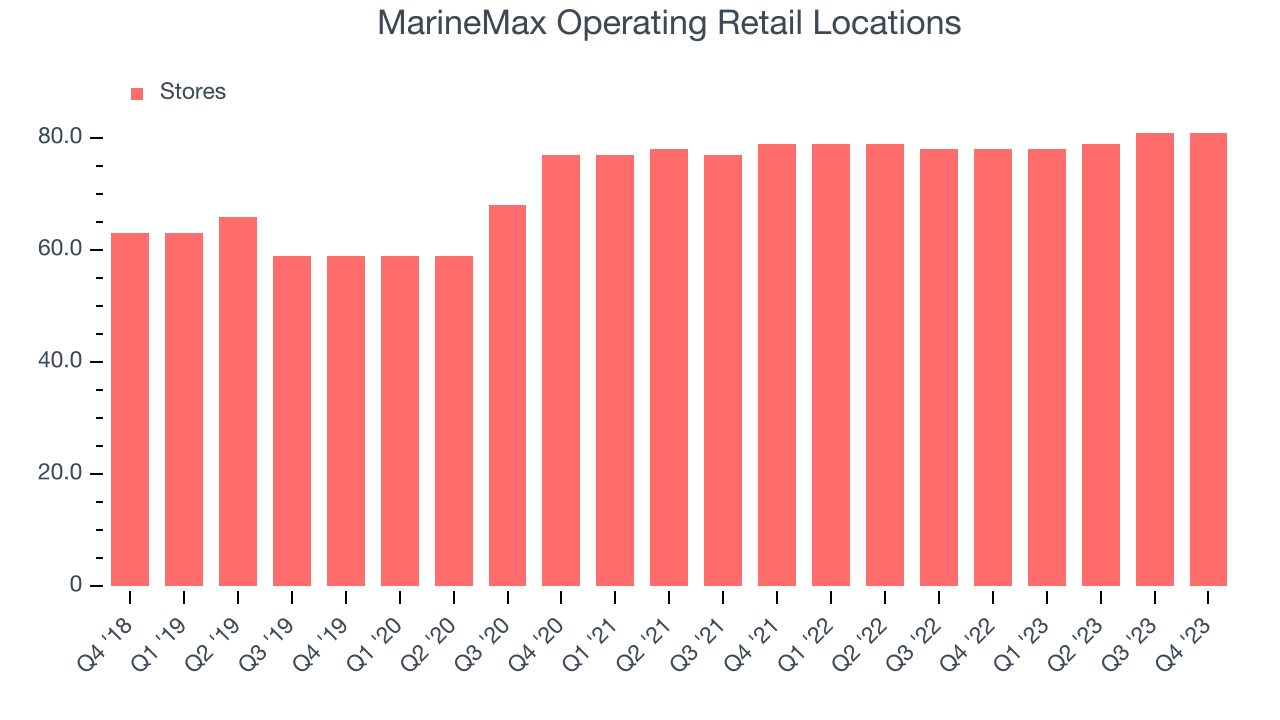

- Store Locations: 81 at quarter end, increasing by 3 over the last 12 months

“I’m proud of our team’s ability to drive a strong close to the December quarter, generating the highest first quarter revenue in our history. This growth came despite a challenging retail environment which required us to take more aggressive pricing actions than expected,” said Brett McGill, Chief Executive Officer and President of MarineMax.

Appropriately headquartered in Clearwater, Florida, MarineMax (NYSE:HZO) sells boats, yachts, and other marine products.

Boat & Marine Retailer

Retailers that sell boats and marine products sell products, sure, but they also sell an image and lifestyle to an often wealthier customer. Unlike a car–which many use daily to get to/from work and to run personal and family errands–a boat or yacht is certainly a discretionary, luxury, nice-to-have purchase. While there is online competition, especially for research and discovery, the boat and yacht market is still very brick-and-mortar based given the magnitude of the purchase and the logistical costs associated with moving these products over long distances.

Sales Growth

MarineMax is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale. On the other hand, one advantage is that its growth rates can be higher because it's growing off a small base.

As you can see below, the company's annualized revenue growth rate of 16.7% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was excellent despite not opening many new stores, implying that growth was driven by increased sales at existing, established stores.

This quarter, MarineMax's revenue grew 3.8% year on year to $527.3 million, falling short of Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 4% over the next 12 months, an acceleration from this quarter.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Number of Stores

The number of stores a retailer operates is a major determinant of how much it can sell, and its growth is a critical driver of how quickly company-level sales can grow.

When a retailer like MarineMax keeps its store footprint steady, it usually means that demand is stable and it's focused on improving operational efficiency to increase profitability. MarineMax's store count increased by 3 locations, or 3.8%, over the last 12 months to 81 total retail locations in the most recently reported quarter.

Taking a step back, the company has only opened a few new stores over the last eight quarters, averaging 1.3% annual growth in new locations. Although it's expanded its presence, this sluggish store growth lags other retailers. A flat store base means that revenue growth must come from increased e-commerce sales or higher foot traffic and sales per customer at existing stores.

Same-Store Sales

MarineMax's demand within its existing stores has been relatively stable over the last eight quarters but fallen behind the broader consumer retail sector. On average, the company's same-store sales have grown by 1.4% year on year. Given its flat store count over the same period, this performance stems from increased foot traffic at existing stores or higher e-commerce sales as the company shifts demand from in-store to online.

In the latest quarter, MarineMax's same-store sales rose 4% year on year. This growth was a well-appreciated turnaround from the 1% year-on-year decline it posted 12 months ago, showing the business is regaining momentum.

Key Takeaways from MarineMax's Q1 Results

We struggled to find many strong positives in these results. Its full-year earnings forecast was lowered and significantly missed analysts' expectations and its gross margin missed Wall Street's estimates. Management called out "a challenging retail environment which required us to take more aggressive pricing actions...pricing actions did result in lower gross margins and profitability. This was primarily due to increased discounting on certain boat models in response to the softer retail environment" Overall, the results could have been better. The company is down 15.2% on the results and currently trades at $28.15 per share.

MarineMax may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.