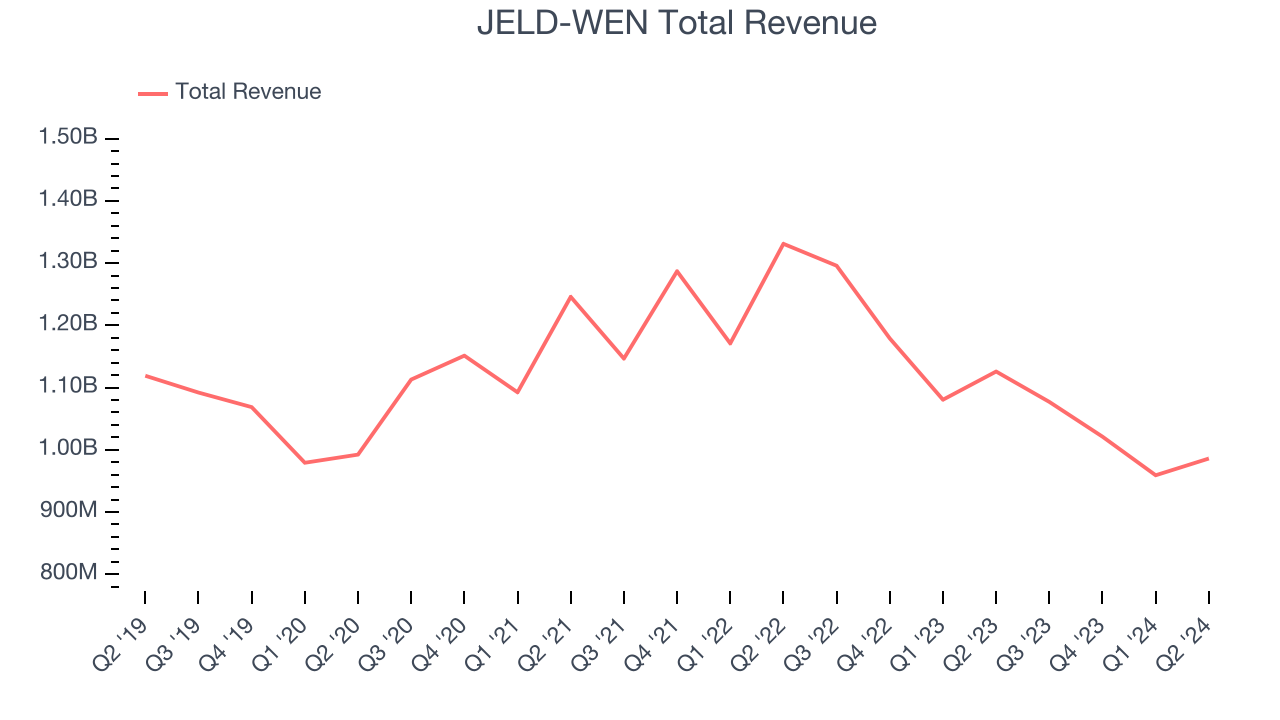

Building products manufacturer JELD-WEN (NYSE:JELD) fell short of analysts' expectations in Q2 CY2024, with revenue down 12.4% year on year to $986 million. On the other hand, the company's outlook for the full year was close to analysts' estimates with revenue guided to $4 billion at the midpoint. It made a non-GAAP profit of $0.34 per share, down from its profit of $0.44 per share in the same quarter last year.

Is now the time to buy JELD-WEN? Find out by accessing our full research report, it's free.

JELD-WEN (JELD) Q2 CY2024 Highlights:

- Revenue: $986 million vs analyst estimates of $1 billion (1.4% miss)

- Adjusted EBITDA: $84.8 million vs analyst estimates of $79.0 million (7.3% beat)

- EPS (non-GAAP): $0.34 vs analyst estimates of $0.27 (24.7% beat)

- The company reconfirmed its revenue guidance for the full year of $4 billion at the midpoint

- EBITDA guidance for the full year is $360 million at the midpoint, above analyst estimates of $349.5 million

- Gross Margin (GAAP): 19.3%, down from 20% in the same quarter last year

- Adjusted EBITDA Margin: 8.6%, down from 9.7% in the same quarter last year

- Free Cash Flow of $18.3 million is up from -$45.7 million in the previous quarter

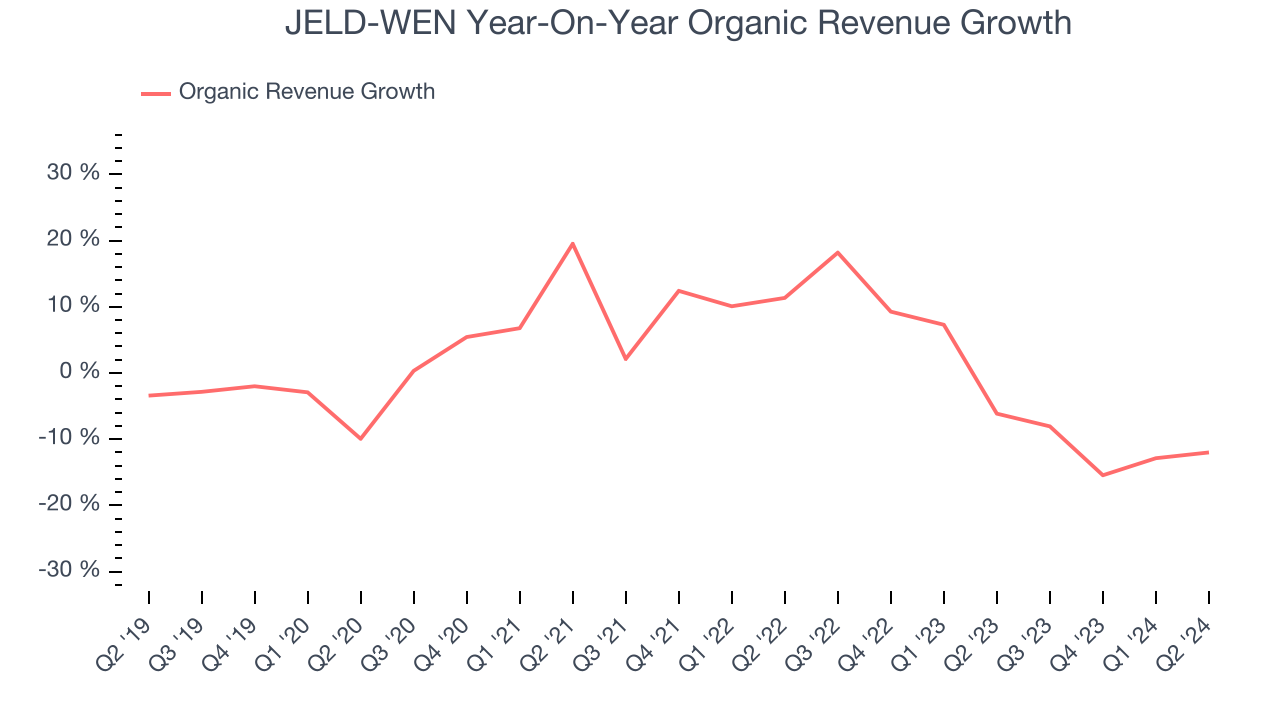

- Organic Revenue fell 12% year on year (-6.1% in the same quarter last year)

- Market Capitalization: $1.32 billion

"We continue to make strides in our transformation journey, positioning JELD-WEN for improved performance," said Chief Executive Officer William J. Christensen.

Founded in the 1960s as a general wood-making company, JELD-WEN (NYSE:JELD) manufactures doors, windows, and other related building products.

Home Construction Materials

Traditionally, home construction materials companies have built economic moats with expertise in specialized areas, brand recognition, and strong relationships with contractors. More recently, advances to address labor availability and job site productivity have spurred innovation that is driving incremental demand. However, these companies are at the whim of residential construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of home construction materials companies.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one tends to grow for years. JELD-WEN struggled to generate demand over the last five years as its sales dropped by 1.5% annually, a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. JELD-WEN's recent history shows its demand has stayed suppressed as its revenue has declined by 9.5% annually over the last two years.

We can dig further into the company's sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations because they don't accurately reflect its fundamentals. Over the last two years, JELD-WEN's organic revenue averaged 2.5% year-on-year declines. Because this number is better than its normal revenue growth, we can see that some mixture of divestitures and foreign exchange rates dampened its headline performance.

This quarter, JELD-WEN missed Wall Street's estimates and reported a rather uninspiring 12.4% year-on-year revenue decline, generating $986 million of revenue. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Operating Margin

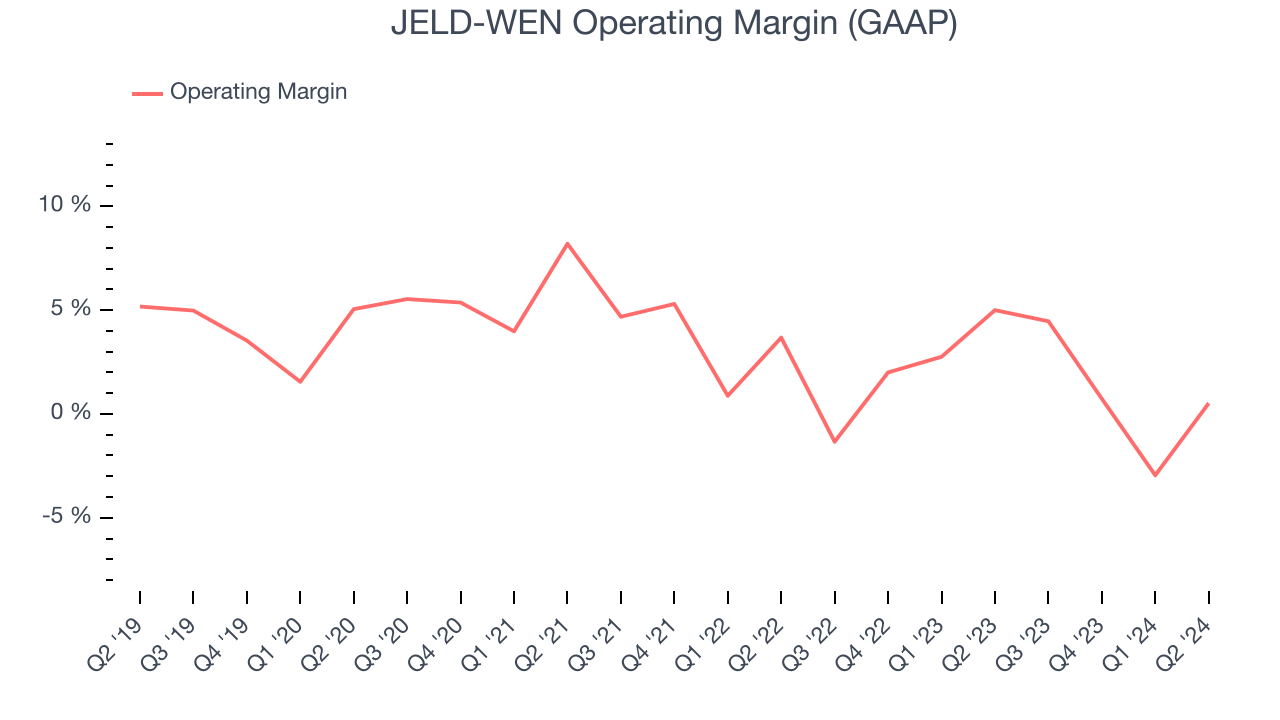

JELD-WEN was profitable over the last five years but held back by its large expense base. It demonstrated lousy profitability for an industrials business, producing an average operating margin of 3.3%. This result isn't too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, JELD-WEN's annual operating margin decreased by 3 percentage points over the last five years. The company's performance was poor no matter how you look at it. It shows operating expenses were rising and it couldn't pass those costs onto its customers.

In Q2, JELD-WEN's breakeven margin was down 4.5 percentage points year on year. Since JELD-WEN's operating margin decreased more than its gross margin, we can assume the company was recently less efficient because expenses such as sales, marketing, R&D, and administrative overhead increased.

EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

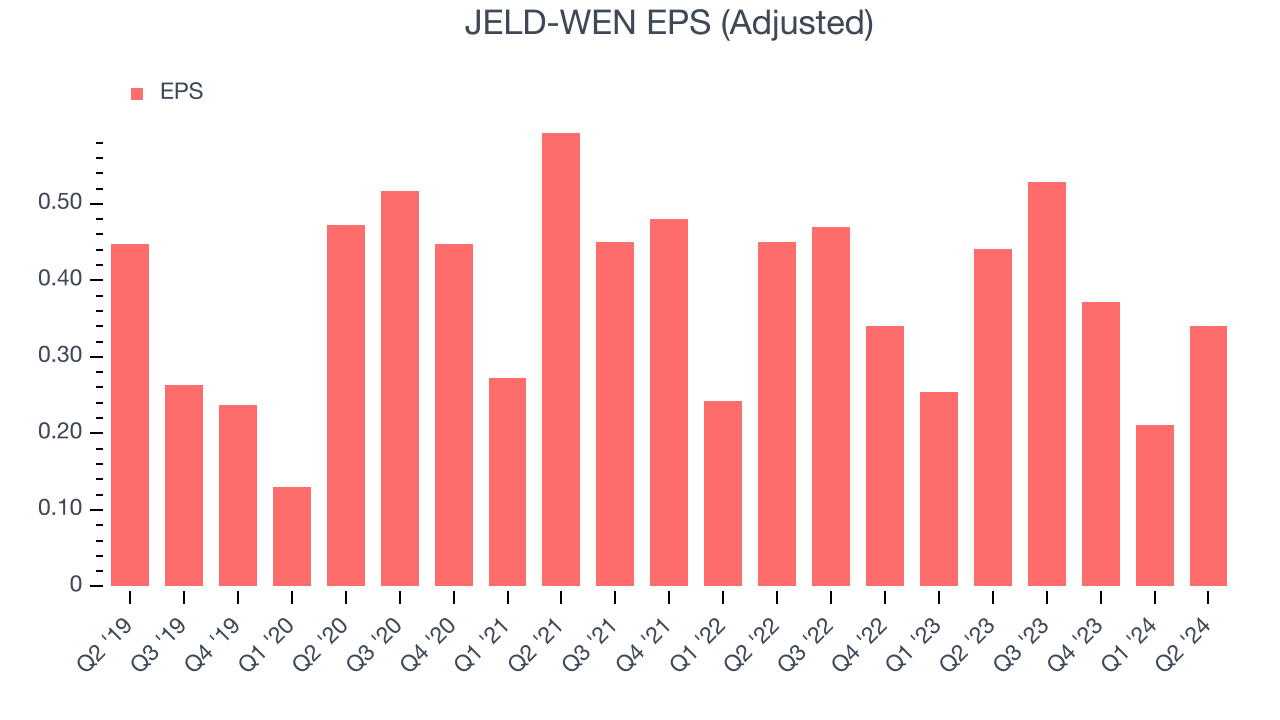

JELD-WEN's flat EPS over the last five years was weak but better than its 1.5% annualized revenue declines. However, this alone doesn't tell us much about its day-to-day operations because its operating margin didn't expand.

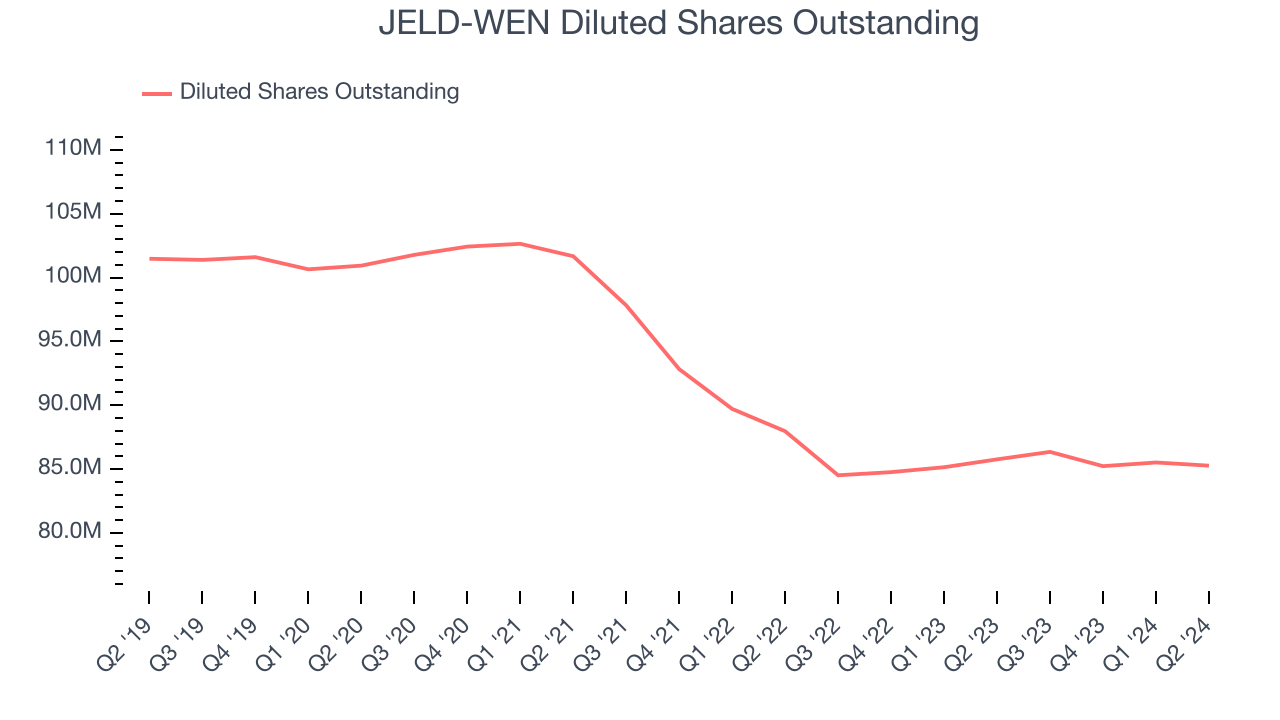

We can take a deeper look into JELD-WEN's earnings to better understand the drivers of its performance. A five-year view shows that JELD-WEN has repurchased its stock, shrinking its share count by 16%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we also analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business. For JELD-WEN, its two-year annual EPS declines of 5.5% show its recent history was to blame for its underperformance over the last five years. These results were bad no matter how you slice the data.

In Q2, JELD-WEN reported EPS at $0.34, down from $0.44 in the same quarter last year. Despite falling year on year, this print easily cleared analysts' estimates. Over the next 12 months, Wall Street expects JELD-WEN to grow its earnings. Analysts are projecting its EPS of $1.45 in the last year to climb by 5.9% to $1.54.

Key Takeaways from JELD-WEN's Q2 Results

We were impressed by how significantly JELD-WEN blew past analysts' organic revenue and adjusted EBITDA expectations this quarter. We were also excited its EPS outperformed Wall Street's estimates. Full year adjusted EBITDA guidance was above expectations, which is another positive. Overall, we think this was a strong quarter that should satisfy shareholders. The stock remained flat at $14.68 immediately after reporting.

So should you invest in JELD-WEN right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.