Clothing company Kontoor Brands (NYSE:KTB) beat analysts' expectations in Q1 CY2024, with revenue down 5.4% year on year to $631.2 million. The company expects the full year's revenue to be around $2.6 billion, in line with analysts' estimates. Its non-GAAP profit of $1.16 per share was flat year on year.

Kontoor Brands (KTB) Q1 CY2024 Highlights:

- Revenue: $631.2 million vs analyst estimates of $607.9 million (3.8% beat)

- EPS (non-GAAP): $1.16 vs analyst estimates of $0.91 (27.8% beat)

- The company reconfirmed its revenue guidance for the full year of $2.6 billion at the midpoint

- Gross Margin (GAAP): 45.2%, up from 43% in the same quarter last year

- Free Cash Flow of $50.82 million, down 75% from the previous quarter

- Market Capitalization: $3.46 billion

Founded in 2019 after separating from VF Corporation, Kontoor Brands (NYSE:KTB) is a clothing company known for its high-quality denim products.

The company quickly carved out a niche with its denim-focused apparel brands, Wrangler and Lee. These brands’ products include jeans, jackets, and other apparel items.

Kontoor Brands has worldwide operations to effectively tap into different markets, catering to consumers' unique tastes and preferences. This international footprint is supported by a mix of sales channels, including brick and mortar stores, department stores, and e-commerce, enabling the company to increase its reach and enhance its customer engagement.

Apparel, Accessories and Luxury Goods

Within apparel and accessories, not only do styles change more frequently today than decades past as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel, accessories, and luxury goods companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

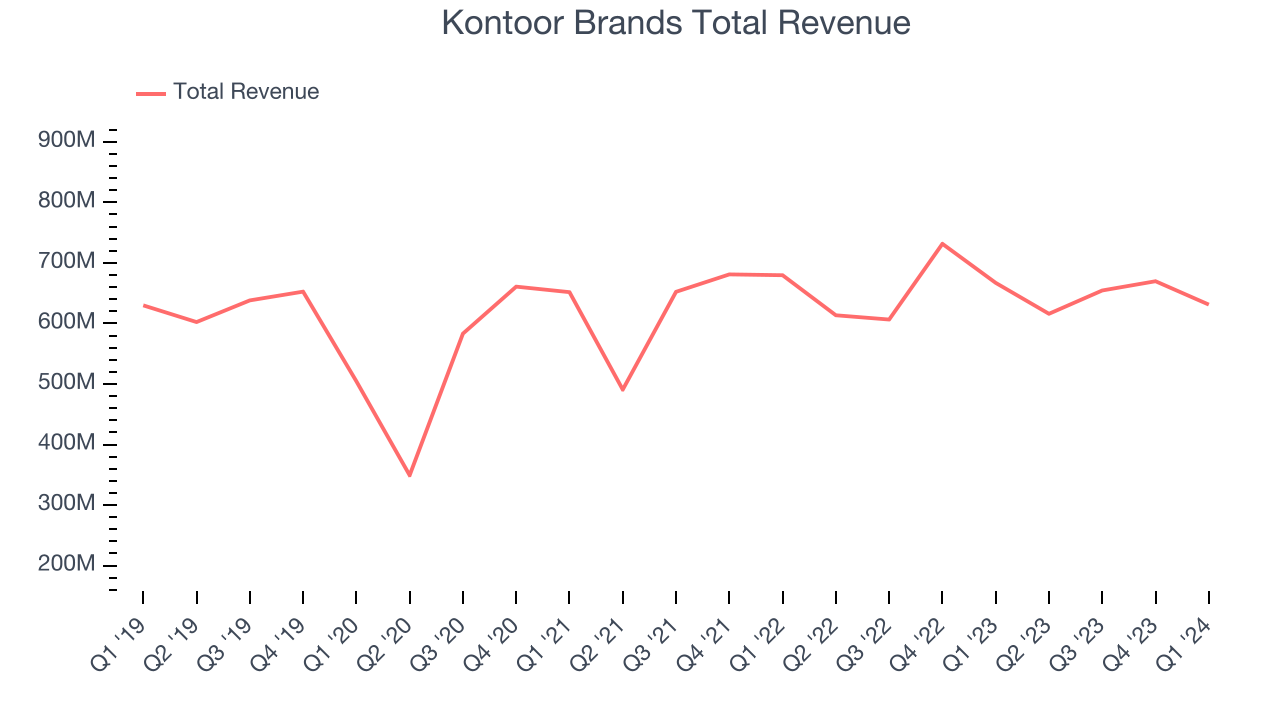

A company’s long-term performance can give signals about its business quality. Any business can put up a good quarter or two, but many enduring ones muster years of growth. Kontoor Brands's revenue was flat over the last five years.

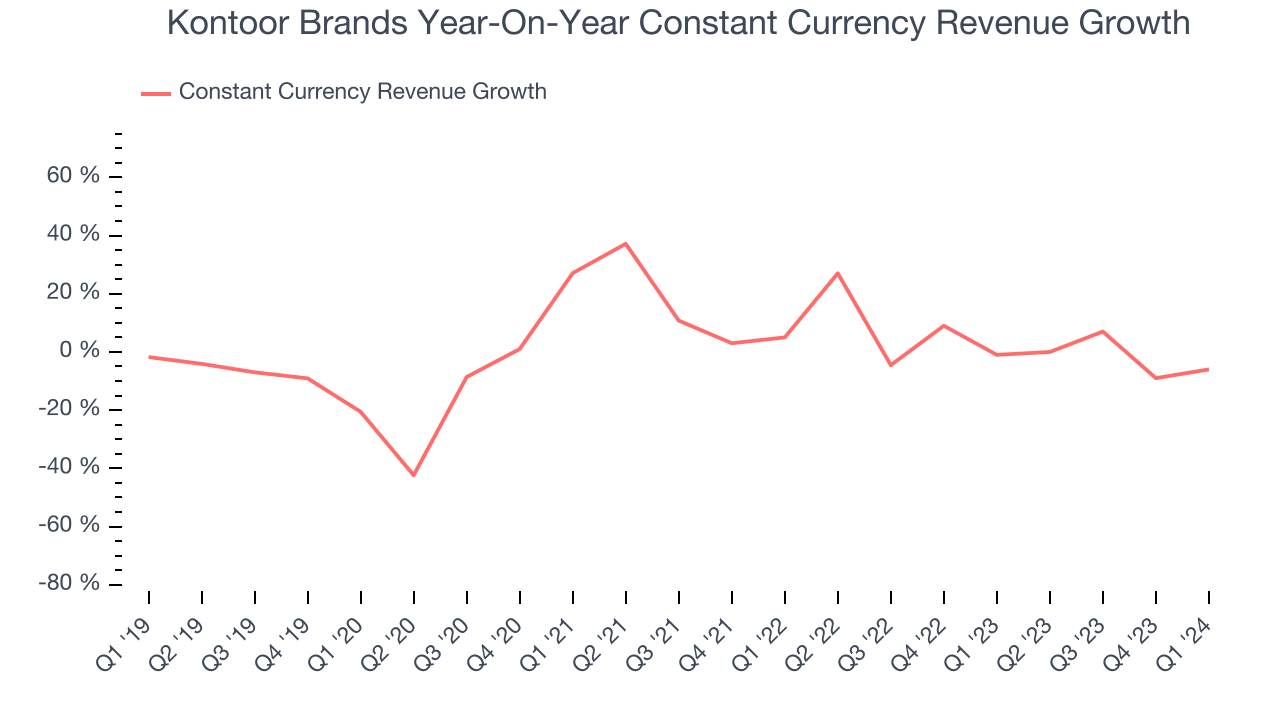

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Kontoor Brands's annualized revenue growth of 1.3% over the last two years is above its five-year trend, suggesting some bright spots.

Kontoor Brands also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 2.8% year-on-year growth. Because this number aligns with its revenue growth during the same period, we can see Kontoor Brands's foreign exchange rates have been steady.

This quarter, Kontoor Brands's revenue fell 5.4% year on year to $631.2 million but beat Wall Street's estimates by 3.8%. Looking ahead, Wall Street expects sales to grow 1.5% over the next 12 months, an acceleration from this quarter.

Operating Margin

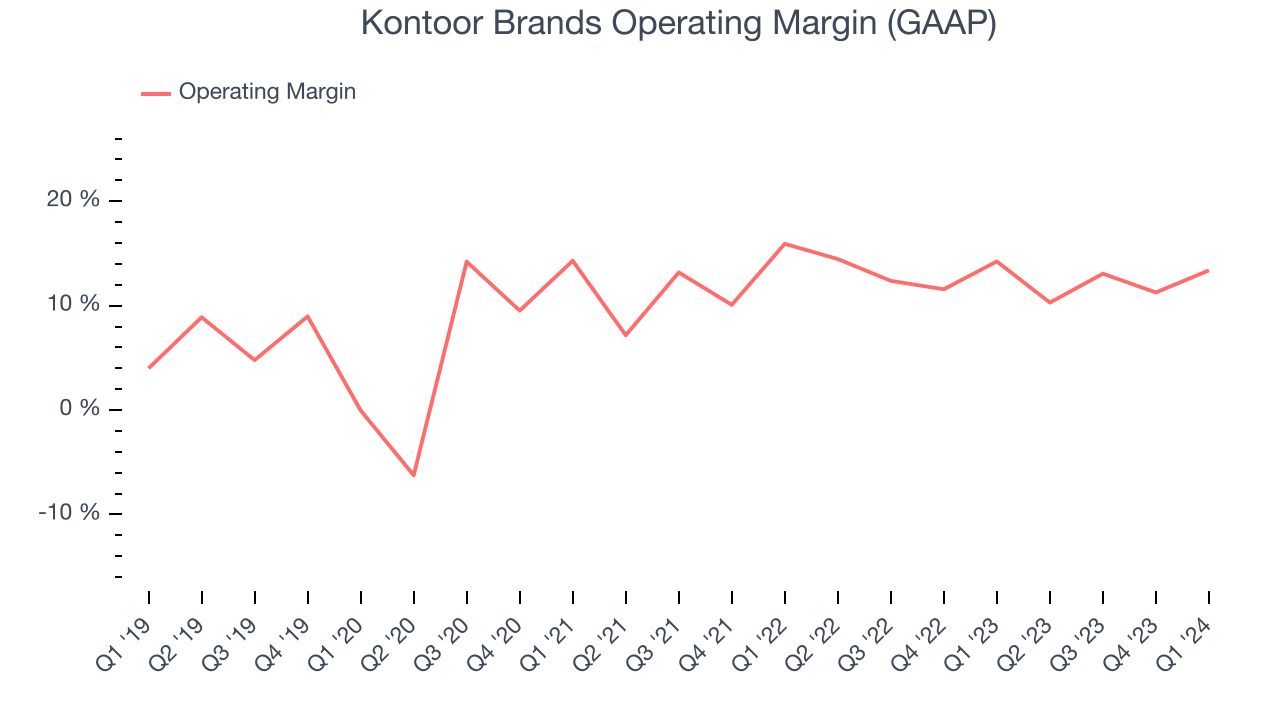

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Kontoor Brands has done a decent job managing its expenses over the last eight quarters. The company has produced an average operating margin of 12.6%, higher than the broader consumer discretionary sector.

In Q1, Kontoor Brands generated an operating profit margin of 13.4%, in line with the same quarter last year. This indicates the company's costs have been relatively stable.

Over the next 12 months, Wall Street expects Kontoor Brands to become more profitable. Analysts are expecting the company’s LTM operating margin of 12% to rise to 14.4%.

EPS

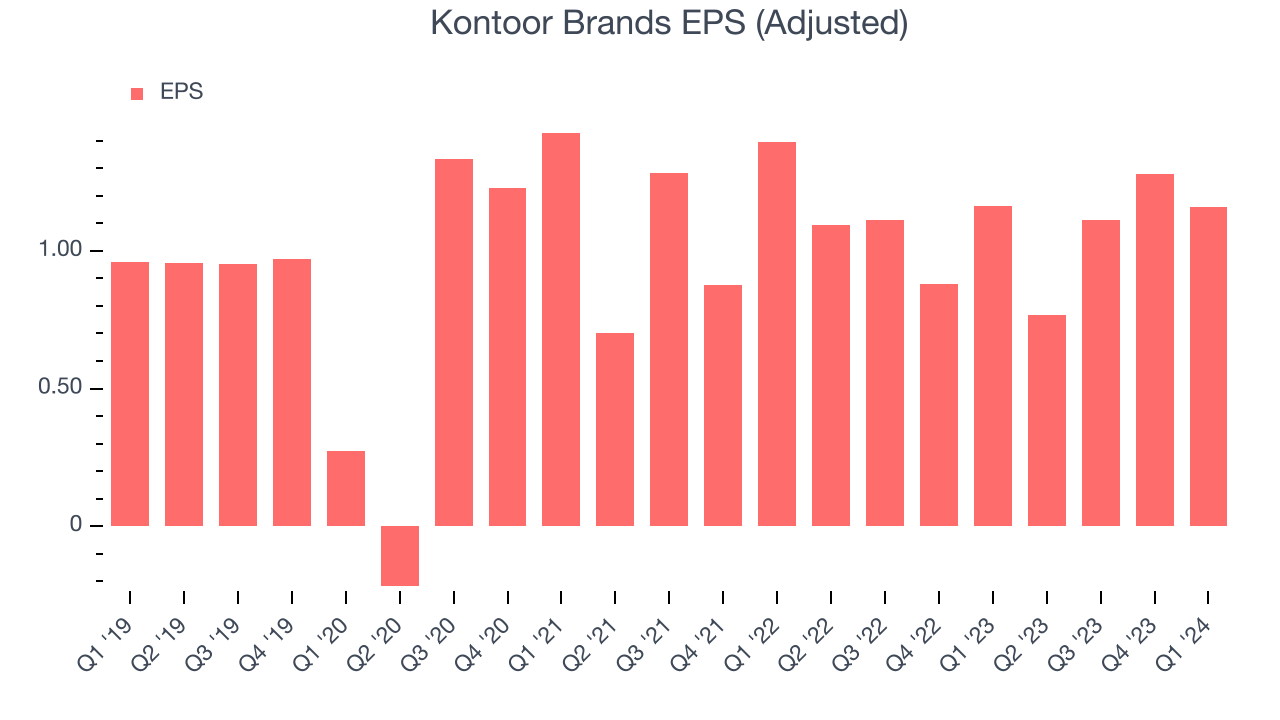

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last five years, Kontoor Brands's EPS was roughly flat, which isn't ideal. We hope the company can generate some earnings growth in the future.

In Q1, Kontoor Brands reported EPS at $1.16, in line with the same quarter last year. This print beat analysts' estimates by 27.8%. Over the next 12 months, Wall Street expects Kontoor Brands to grow its earnings. Analysts are projecting its LTM EPS of $4.32 to climb by 11.1% to $4.80.

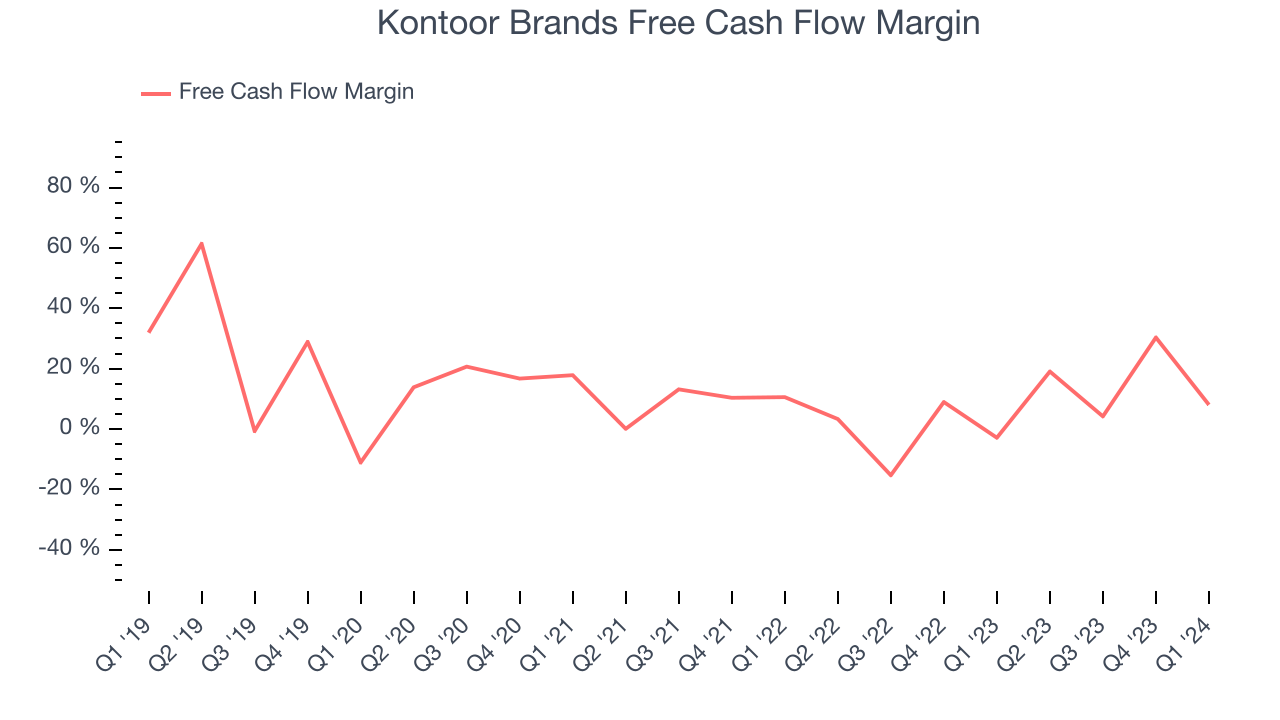

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, Kontoor Brands has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 7.2%, subpar for a consumer discretionary business.

Kontoor Brands's free cash flow came in at $50.82 million in Q1, equivalent to a 8.1% margin. This result was great for the business as it flipped from cash flow negative in the same quarter last year to cash flow positive this quarter.

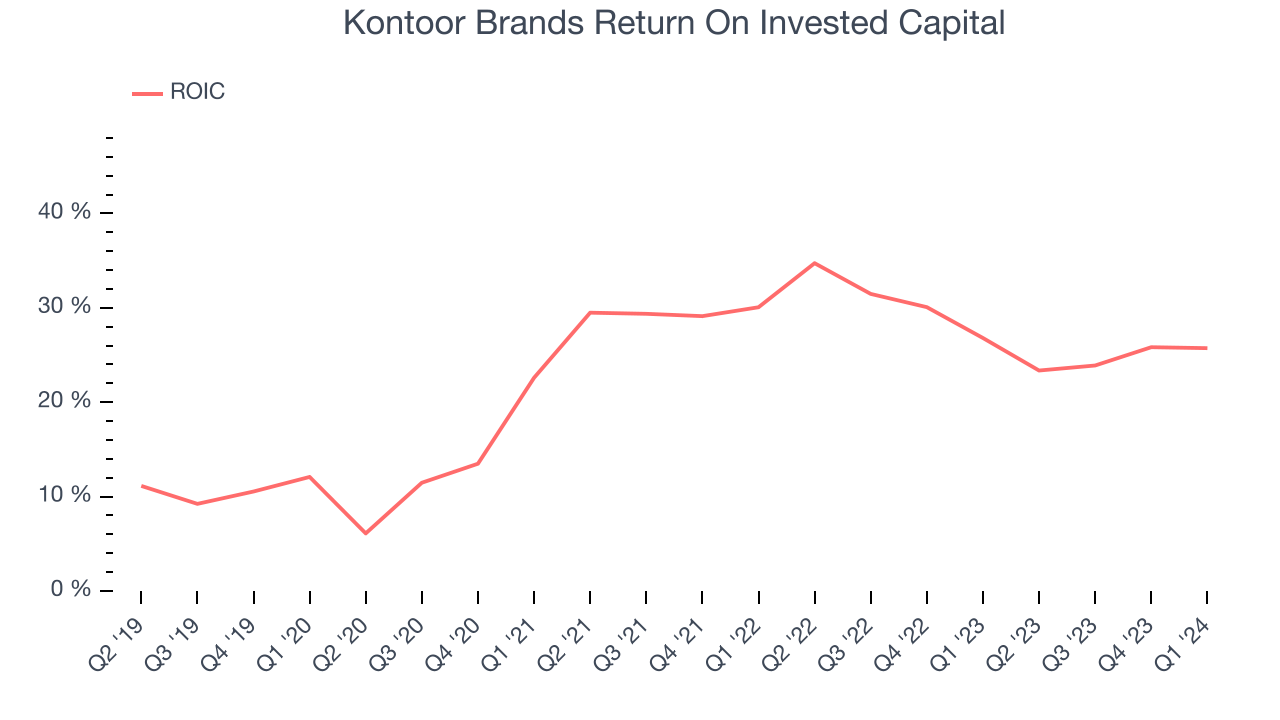

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to how much money the business raised (debt and equity).

Although Kontoor Brands hasn't been the highest-quality company lately because of its poor top-line performance, it historically did a wonderful job investing in profitable business initiatives. Its five-year average return on invested capital was 23.5%, splendid for a consumer discretionary business.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last few years, Kontoor Brands's ROIC averaged 8.9 percentage point increases. This is a good sign, and we hope the company can continue improving.

Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly.

Kontoor Brands reported $215.1 million of cash and $838.4 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $367.7 million of EBITDA over the last 12 months, we view Kontoor Brands's 1.7x net-debt-to-EBITDA ratio as safe. We also see its $33.63 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from Kontoor Brands's Q1 Results

We were impressed by how significantly Kontoor Brands blew past analysts' EPS expectations this quarter, driven by outperformance in its constant currency revenue growth and gross margin. It also reduced its inventory levels by 24% year on year. Looking ahead, Kontoor Brands raised its full-year EPS guidance, a great sign for investors (especially amongst a weaker consumer discretionary market backdrop). Overall, we think this was still a really good quarter that should please shareholders. The stock is up 4.8% after reporting and currently trades at $65.05 per share.

Is Now The Time?

Kontoor Brands may have had a favorable quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Kontoor Brands, we'll be cheering from the sidelines. Its revenue has declined over the last five years, but at least growth is expected to increase in the short term. And while its stellar ROIC suggests it has been a well-run company historically, the downside is its constant currency sales performance has been disappointing. On top of that, its declining EPS over the last five years makes it hard to trust.

Kontoor Brands's price-to-earnings ratio based on the next 12 months is 12.9x. While there are some things to like about Kontoor Brands and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $64.43 per share right before these results (compared to the current share price of $65.05).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.