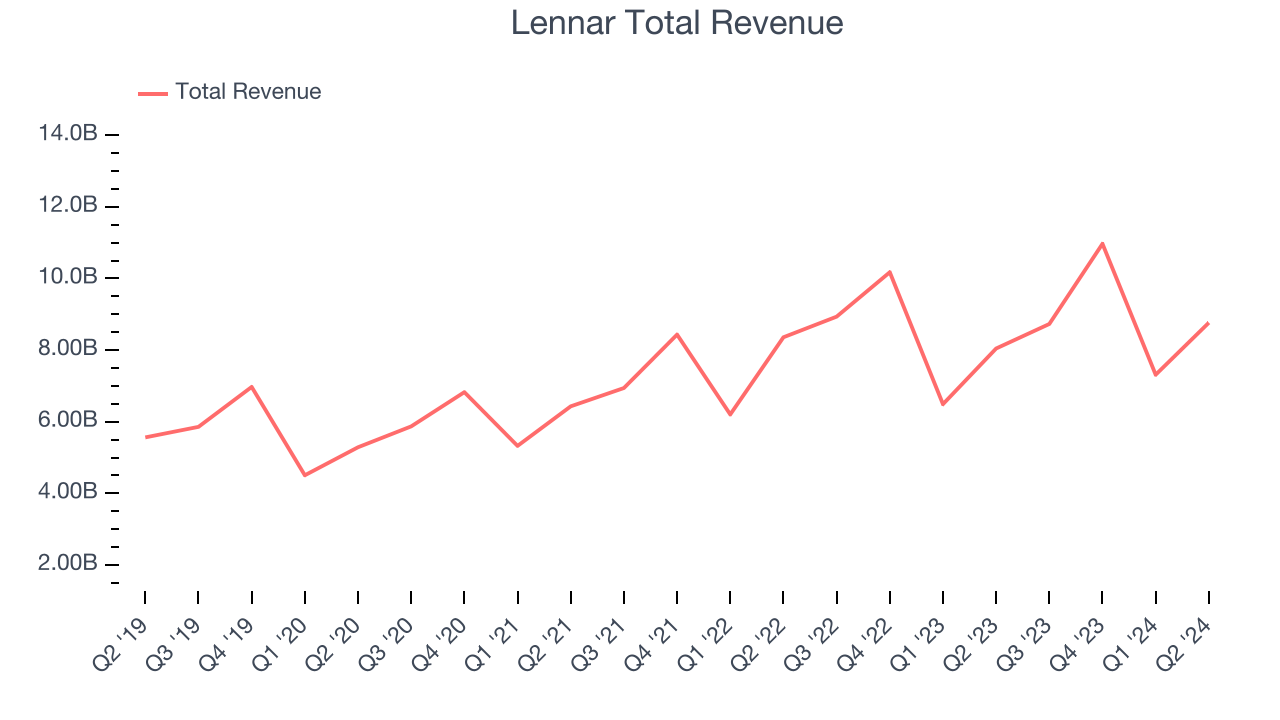

Homebuilder Lennar (NYSE:LEN) reported Q2 CY2024 results exceeding Wall Street analysts' expectations, with revenue up 9% year on year to $8.77 billion. It made a GAAP profit of $3.45 per share, improving from its profit of $3.06 per share in the same quarter last year.

Is now the time to buy Lennar? Find out by accessing our full research report, it's free.

Lennar (LEN) Q2 CY2024 Highlights:

- Revenue: $8.77 billion vs analyst estimates of $8.55 billion (2.5% beat)

- EPS: $3.45 vs analyst estimates of $3.25 (6.3% beat)

- Q3'24 new orders guidance: $8.77 billion vs analyst estimates of $8.89 billion (1.3% miss)

- Gross Margin (GAAP): 26.1%, up from 22.9% in the same quarter last year

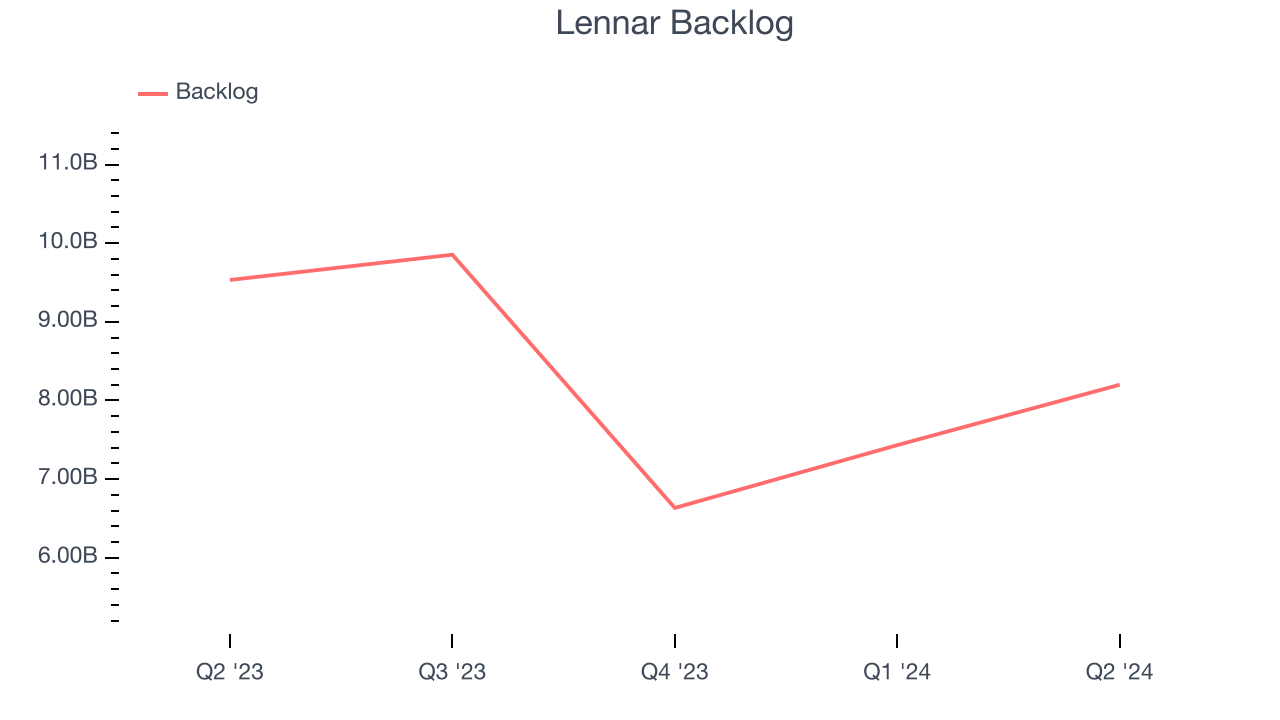

- Backlog: $8.2 billion at quarter end, down 14% year on year (miss)

- Market Capitalization: $42.75 billion

Stuart Miller, Executive Chairman and Co-Chief Executive Officer of Lennar, said, "We are pleased to report another strong quarter against the backdrop of evolving market conditions as interest rates rose for most of the quarter and then subsided as the quarter closed. Although affordability continued to be tested by interest rate movements and simultaneously challenged consumer sentiment, purchasers remained responsive to increased sales incentives, resulting in a 19% increase in our new orders and a 15% increase in our deliveries year over year. The macroeconomic environment remained relatively consistent with employment remaining strong, housing supply remaining chronically short due to production deficits over a decade, and demand strength driven by strong household formation. We remained focused on consistent production pace driving sales pace, while using pricing, incentives, marketing spend and margin adjustment to enable consistent sales volume in a fluctuating interest rate environment."

One of the largest homebuilders in America, Lennar (NYSE:LEN) is known for constructing affordable, move-up, and retirement homes across a range of markets and communities.

Home Builders

Traditionally, homebuilders have built competitive advantages with economies of scale that lead to advantaged purchasing and brand recognition among consumers. Aesthetic trends have always been important in the space, but more recently, energy efficiency and conservation are driving innovation. However, these companies are still at the whim of the macro, specifically interest rates that heavily impact new and existing home sales. In fact, homebuilders are one of the most cyclical subsectors within industrials.

Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one tends to sustain growth for years. Thankfully, Lennar's 10.7% annualized revenue growth over the last five years was impressive. This is encouraging because it shows Lennar's offerings resonate with customers, a helpful starting point for our assessment of quality.

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Lennar's annualized revenue growth of 9.3% over the last two years is below its five-year trend, but we still think the results were good and suggest demand was strong.

We can dig further into the company's revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Lennar's backlog reached $8.2 billion in the latest quarter and averaged 20.4% year-on-year declines over the last two years. Because this number is lower than its revenue growth, we can see the company fulfilled orders at a faster rate than it added new orders to the backlog. This implies Lennar was operating efficiently but also raises questions about the health of its sales pipeline.

This quarter, Lennar reported solid year-on-year revenue growth of 9%, and its $8.77 billion of revenue outperformed Wall Street's estimates by 2.5%. Looking ahead, Wall Street expects sales to grow 1.3% over the next 12 months, a deceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Operating Margin

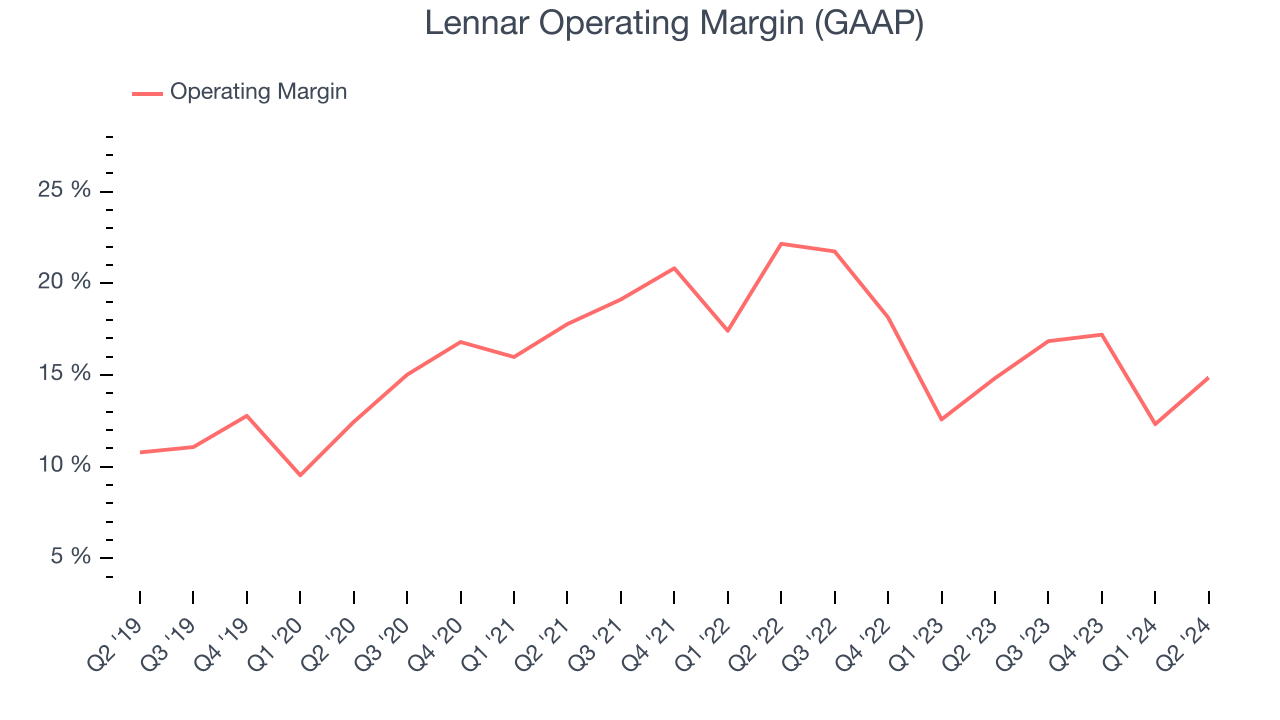

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Lennar has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 16.4%. Furthermore, Lennar's operating profitability was impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it's a show of strength if they're high when gross margins are low.

Analyzing the trend in its profitability, Lennar's annual operating margin rose by 3.9 percentage points over the last five years, showing its efficiency has improved.

This quarter, Lennar generated an operating profit margin of 14.9%, in line with the same quarter last year. This indicates the company's cost structure has recently been stable.

Key Takeaways from Lennar's Q2 Results

We enjoyed seeing Lennar exceed analysts' revenue and operating margin outperformed Wall Street's estimates. On the other hand, its backlog missed, and this is an important revenue leading indicator. Additionally, guidance for next quarter's new orders also missed expectations, and the company said that "affordability continued to be tested by interest rate movements and simultaneously challenged consumer sentiment." Zooming out, we think this was still a a tepid quarter showing that the company is not out of the woods yet with regards to the macro and consumer health. The market was likely expecting more, and the stock is down 1.7% after reporting, trading at $153.85 per share.

So should you invest in Lennar right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.